By Michael J. Wiener

By Michael J. Wiener

Special to the Findependence Hub

Canadians who collect Old Age Security (OAS) now get a 10% increase in benefits when they reach age 75. The amount of the increase isn’t huge, but it’s better than nothing. A side effect of this increase is that it makes delaying OAS benefits past age 65 a little more compelling.

The standard age for starting OAS benefits is 65, but you can delay them for up to 5 years in return for a 0.6% increase in benefits for each month you delay. So, the maximum increase is 36% if you take OAS at 70.

A strategy some retirees use when it comes to the Canada Pension Plan (CPP) and OAS is to take them as early as possible and invest the money. They hope to outperform the CPP and OAS increases they would get if they delayed starting their benefits. In a previous post I looked at how well their investments would have to perform for this strategy to win. Here I update the OAS analysis to take into account the 10% OAS increase at age 75.

This analysis is only relevant for those who have enough other income or savings to live on if they delay OAS. Others with no significant savings and insufficient other income have little choice but to take OAS at 65.

OAS payments are indexed to price inflation, and the increases before you start collecting are also indexed to price inflation. So, the returns that come from delaying OAS are “real” returns, meaning that they are above inflation. An investment that earns a 5% real return when inflation is 3% has a nominal return of (1.05)(1.03)-1=8.15%.

In many ways, the OAS rules are much simpler than they are for CPP, but two things are more complex: the OAS clawback and OAS-linked benefits. For those retirees fortunate enough to have high incomes, OAS is clawed back at the rate of 15% of income over a certain threshold. This complicates the decision of when to take OAS. Low-income retirees may be eligible for other benefits once they start collecting OAS. These factors are outside the scope of my analysis here.

A One-Month Delay Example

Suppose you’re deciding whether to take OAS at age 65 or wait one more month. For the one month delay, the OAS rules say you’d get an additional 0.6%. So, for the cost of one missed payment, you’d get 0.6% more until you reach 75. After that, you’d be getting 0.66% more.

For a planning age of 100, the real return from this delay is a little over 7%. So, your investments would have to average 7% plus inflation to keep up if you chose to take OAS right away and invest the money.

All the One-Month Delays

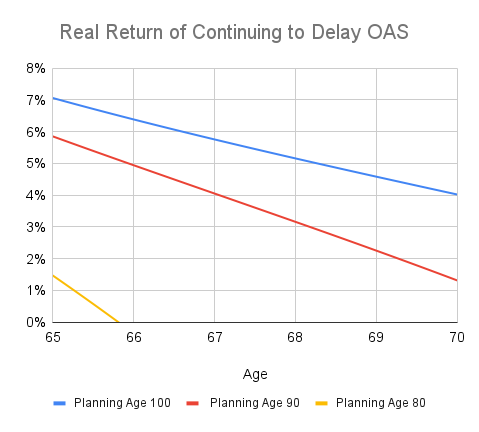

The following chart shows the real return of delaying OAS each month for a range of retirement planning ages, based on the assumption that the OAS clawback and delaying additional benefits don’t apply. The returns are slightly higher than they were before CPP payments rose 10% at age 75.

The case for delaying OAS isn’t nearly as compelling as it is for delaying CPP. However, those with a retirement planning age of 100 get real returns above 4% for delaying all the way to age 70. I plan to wait until I’m 70 to take OAS.

For a retirement planning age of 90, delaying OAS to 68 or 69 makes sense. However, those whose health is poor enough that they plan to age 80 or less should just take OAS at 65.

Michael J. Wiener runs the web site Michael James on Money, where he looks for the right answers to personal finance and investing questions. He’s retired from work as a “math guy in high tech” and has been running his website since 2007. He’s a former mutual fund investor, former stock picker, now index investor. This blog originally appeared on his site on March 16, 2023 and is republished on the Hub with his permission.

Michael J. Wiener runs the web site Michael James on Money, where he looks for the right answers to personal finance and investing questions. He’s retired from work as a “math guy in high tech” and has been running his website since 2007. He’s a former mutual fund investor, former stock picker, now index investor. This blog originally appeared on his site on March 16, 2023 and is republished on the Hub with his permission.