By Brandon Hill, CFP

By Brandon Hill, CFP

Special to the Financial Independence Hub

I’ll never forget when I was growing up hearing my parents talking about “buying RSPs” (I got excited about saving money. I know… I’m a weirdo).

In my mind, they were this magical investment that people bought so they could multiply their money to one day retire. This term, “buying RSPs” is still used today; however, I think it adds to the confusion of what a RRSP really is.

I’m here to explain in plain English the difference between the RRSP (Registered Retirement Savings Plan) and the TFSA (Tax Free Savings Account).

What are they?

The best way to think of an RRSP or a TFSA is simply as an account that has special tax benefits. Just like your chequing account, you are able to deposit and withdraw money into a RRSP or TFSA; however, the special tax benefits make it slightly more complicated.

RRSP: When you deposit money into an RRSP, you’re allowed to deduct this amount on your tax return, saving you tax and increasing your refund. However, when you withdraw money from your RRSP, you have to pay tax on this amount.

TFSA: When you deposit money into a TFSA you do not get a tax deduction, although when you withdraw from your TFSA, you do not have to pay any tax.

All growth within an RRSP and TFSA is tax free.

You can invest in many different ways inside the RRSP or TFSA, including: stocks, bonds, GIC’s, Mutual Funds, ETFs, and other more advanced options.

A common misconception occurs for the Tax Free Savings Account due to how most banks promote their TFSA “savings” rates. It is much wiser to take advantage of the tax benefits and invest the money in your TFSA to earn 6-10%, rather than earning 1% in a “savings” program. The only time I would recommend holding your TFSA money in a savings program is if you haven’t maxed out your contributions yet and have room for short-term savings (i.e. house down-payment or upcoming vacation).

The main point to understand is these are very important tools to help you pay less tax!

Which account do I use?

Okay, so you’ve finally decided to start saving but need to figure out which is best for your situation: THE RRSP or TFSA?

Easy, just max out both contributions so you don’t have to decide . OK I wish it were this easy, but for most of us (me!), this is just not possible.

The quick answer in most cases is to maximize your TFSA contributions first before using the RRSP. The TFSA is a much more flexible option (no tax when you withdraw) and provides the same tax-free growth. Also, your TFSA investments can always be rolled over into an RRSP at any time.

The exception is when you are in a higher income tax bracket ($75,000 – $90,000+). The reason for this is because the best use of an RRSP is to contribute during years when you are paying a high tax rate (prime earning years) and to withdraw during years with a low tax rate (retirement). You also do not have to use the deduction in the year you contribute. You can save these for future “high-tax” years.

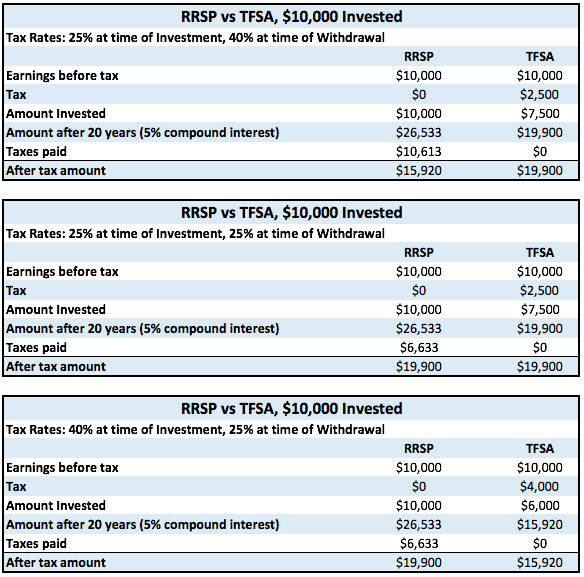

The tables below demonstrate the importance of contributing to a RRSP (vs a TFSA) in a higher tax rate and withdrawing in a lower tax rate.

If you are currently a high-income earner and are expecting a large pension in retirement, maximizing your TFSA first will allow for more flexibility when it comes to retirement tax planning (The Old Age Security pension is “eliminated” at a certain income level, but this is beyond the scope of this article).

TAKE NOTE: You must invest the tax refund/savings you receive from contributing to your RRSP to make it worthwhile – if you see this tax refund as the means for a spontaneous vacation or shopping spree, you completely wipe out any benefit of using an RRSP.

If you are in a position where you are earning high income and contribute to both, one interesting strategy is to invest a large portion in your RRSPs and use the tax refund/savings to fund your TFSA.

RRSPs can offer “protection” from yourself as the tax consequences to withdraw can be a powerful deterrent from touching your long-term savings.

There are two government programs that allow you to “borrow” from your RRSP tax free. These can be very valuable strategies if you already have contributed to your RRSP and are looking to buy a home (HBP – Home Buyers Plan) or enroll in an educational program (LLP – Lifelong Learning Plan). Our friends at Bay Street Blog do an awesome job breaking down these two options.

How much can you contribute?

TFSA: If you were born in 1991 or earlier, you have the maximum TFSA contribution room available to Canadians, which is $52,000. Each year the government allows you to contribute an additional $5,500 and contributions can be made at any time.

One caveat to TFSA withdrawals is that you do not recoup the contribution room until January 1st of the next year, so just be wary of over-contributing.

RRSP: You start gaining RRSP contribution room once you start filing a tax return with earned income. Each year your contribution room increases by 18% of your previous year’s earned income up to a maximum of $25,370 (in 2016), and does not expire. To get a tax deduction for a specific year, you must deposit money into your RRSP in that calendar year or before the end of February of the following year.

NOTE: If you make a RRSP withdrawal that is not part of the HBP or LLP, you have officially lost that contribution room.

A great way to keep track of your RRSP and TFSA contribution room is to use the online CRA My Account Tool. The CRA has partnered with most of the big banks to allow you to access this tool using your online banking login.

Conclusion

If you still aren’t sure which one to use, just start with your TFSA. You can always move from a TFSA to RRSP without triggering any tax (although you can’t go the opposite way).

I encourage you to start saving and investing as early as you can. The most important components to being a successful investor is having time on your side, and being disciplined with your savings and investment plan!

If you have any questions, feel free to email me: brandon@alifeofwealth.com

P.S. I know this article was a little more technical than any of us like. Don’t worry, we will be covering a lot more exciting topics in the future!

Disclaimer: This article is for educational purposes only and should not be relied upon as professional tax advice. Everyone’s situation is different and you should consult your financial or tax professional (or me!) before making a decision.

Brandon Hill is a certified financial planner and founder of ALifeofWealth.com, a Toronto-based fee-only advisory service targeting Millennials. His investment model leverages the technology of the Wealthsimple robo-adviser platform. This blog originally appeared on Brandon’s site on Feb. 9th and is republished here with permission.

Brandon Hill is a certified financial planner and founder of ALifeofWealth.com, a Toronto-based fee-only advisory service targeting Millennials. His investment model leverages the technology of the Wealthsimple robo-adviser platform. This blog originally appeared on Brandon’s site on Feb. 9th and is republished here with permission.

Nice breakdown of this continuing duel! Tables are especially useful. I wanted to bring attention to additional RRSP benefits that usually aren’t considered.

If you are a parent with:

– household income >30k

– receiving the Canada Child Benefit

Then contributing to a RRSP lowers your net income, which is used to calculate your monthly Canada Child Benefit payments. The lower net income increases the CCB for the next year.

The increase depends on how much you make and how many kids you have (see link below) – but ranges from 7% to 23% of your RRSP contribution for reducing your net income in the 30-65k range and then 3-9.5% beyond that. This is on top of the tax deferment at your marginal rate.

http://www.cra-arc.gc.ca/bnfts/ccb/clcltyrccb-eng.html

A bit of math there – but the extra percent saved may be enough to sway the vote in this situation.

Josh