By Dale Roberts

Special to Financial Independence Hub

Imagine retiring, and then you have to head back to work, or you cancel your planned trips and greatly curtail your lifestyle. That’s what happened to too many who retired at or near the recesssions created by the dot com crash and the financial crisis. Risk in retirement is perhaps the flipside of risk in the accumulation stage. In the accumulation stage, lower stock prices can be very good. Lower prices in retirement can impair retirement. The equity risk in retirement is called sequence of returns risk. Poor stock market returns early in retirement can create a situation where the portfolio value has decreased, and selling more shares at lower prices might be hazardous to your retirement health. That’s why retirees own bonds, cash and GICs.

I will start off with a few charts that demonstrate the path of a retiree’s portfolio who retired at the start of the dot com crash (late 90s) and the financial crisis (2007-2009).

Here’s the drawdown history in recessions using the U.S. market as an example.

Yes, two of the most recent major corrections were epic and extraordinary. In the dot com crash and the financial crisis, stock markets were down 50%. In the early 2000s U.S. stock markets were down 3 years in a row.

The “average” decline in a recession is close to 25%. But as we know, average rarely happens when it comes to investing and stock markets.

The dot com crash retirement scenario

In the following scenario the retiree has a C$1,000,000 portfolio and spends 4.2% of the portfolio value in year one. The $1,000,000 creates $42,000 of income. The spending rate then increases, adjusted for inflation. If inflation is 3%, the retiree gets a 3% raise.

The portfolio is 50% U.S. stocks and 50% global.

We can see that it was “over” quickly for the equity portfolio in this scenario. Even the strong market returns from 2003 to 2008 could not bring the portfolio back to health. In late 2007 the portfolio value was $870,000 but the spend rate would have been considerable. We have a portfolio value much lower than $1,000,000 and the amount taken out of the portfolio has increased at the rate of inflation. It is a dead portfolio walking, even in 2007. The financial crisis essentially finished it off, and was limping through the 2010s. 2024 would be its final year.

Unfortunate start date

The retiree was a victim of bad luck. They strolled into a very unfortunate start date – at the beginning of a recession and a severe stock market correction.

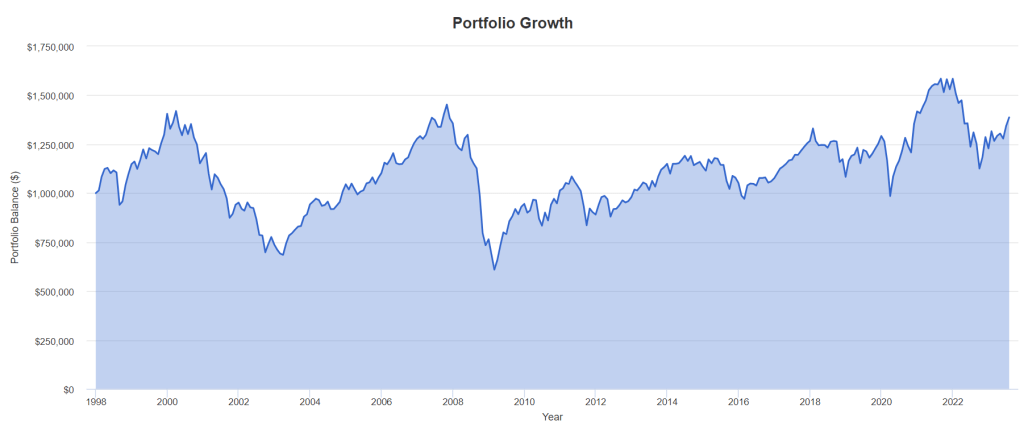

Let’s head back two years to see what happens to a retiree who retired in 1998.

What a difference two years makes. That said, I would suggest that the portfolio was impaired in 2003 and 2008. It was outrageous stock market gains that brought the portfolio back to the land of the living. There is no guarantee that after 40% and 50% portfolio declines that 30% and 20% annual stock market gains will ride to the rescue.

It’s also likely that a retiree who has watched 30% to 40% of their portfolio value disappear is not comfortable keeping up the spend rate. They have cancelled trips, dinners, gifting and more. They might have self-imposed retirement withdrawal.

Risk is different and feels different in retirement.

That self-imposed retirement withdrawal may have occurred during the financial crisis as well.

Who is going to keep the spend rate when the portfolio is down over 50%? I’d suggest no one. And I’d count that as a retirement failure, having to change your retirement plans.

Are you feeling lucky?

Now, let’s give the retiree a very fortunate start date. 1991.

The portfolio never sees new lows. And obvioulsy, the retiree could have treated themself to a much higher spend rate of 4.2% inflation-adjusted. That’s called a variable withdrawal strategy. You spend more when times are very good. And you spend less during recessions. More on that later.

Adding bonds to the retirement portfolio

Most retirees will hold a generous allotment to cash and bonds. One reason is to avoid that mathematical portfolio impairment. The second reason is for comfort, for emotional reasons. We don’t want to see the portfolio value drop 30%, 40%, 50%. Most would not be comfortable spending when a large portion of their net worth has evaporated.

Bonds usually work as portfolio shock absorbers. Bonds are the adult in the room.

Here’s an example with a classic 60/40 stocks to bonds balanced portfolio.

While the retiree would still expericence significant declines, the portfolio has maintained a significant portion of its value. It would have been able to provide sustainable income for 30 years, and likely 35 years.

If we start at 1998, we see that there is no opportunity cost (by holding bonds) compared to the all-stock model from 1998. In fact, it is simply a much easier ride, with less volatility. The end values in 2023 are similar for the balanced portfolio and the all-stock models.

Getting very defensive with lots of bonds

Here’s a scenario with a 70% bond allotment, and 30% stocks. We can call that a balanced income portfolio.

That’s a much smoother ride that many retirees would embrace.

But what about opportunity cost with a generous bond allotment?

One might suggest that there was no opportunity cost. If the goal was to spend at 4.2% inflation adjusted, mission accomplished. And as per the all-stock model from 1991, the retiree would have been able to increase the spend rate.

Of course, we should acknowledge that the bond bull market from 1982 enabled the favourable outcome. There’s no guarantee of a repeat.

Here’s the balanced income model from 2007. One could argue that the ride has been smooth, but there’s not enough growth. I would not argue with someone who suggests that the portfolio is impaired after the COVID correction. One would be wise to adopt that variable withdrawal strategy.

A balanced or balanced growth portfolio model would have been more favourable. So the “answer” is more stocks and growth, if one has the risk tolerance.

What about the stagflation era?

Surprisingly, a global stock portfolio and a balanced portfolio would have done the trick during the stagflation era of the 1970s and early 1980s. That is to say, the models would have sustained the spend rate for 30 years, inflation adjusted.

That said, a retiree would have done much better with an allocation to dedicated inflation fighers, such as gold, oil and gas stocks and commodities. And the balanced portfolio would have needed the inflation fighters to extend the retirement timeline beyond 30 years.

Gold has been a benefit to balanced portfolios from the time of the stagflation era. That is, even with a start date in the 80s or 90s or 2000s.

Readers will know that I am a fan of an all-weather portfolio model for retirees.

We can also use defensive sectors in retirement within the all-weather approach.

I like the idea of a 5% weighting to oil and gas stocks, and 5% to a a multi-asset bundle such as that found in the Purpose Real Asset ETF – (PRA/TSX).

I will be back with more on the inflation era, with content added to this post. We’ll then move on to the D-word, Depression era.

Choose your retirement ride

It’s not just about the charts and probabilities. It’s about your comfort level with portfolio volatility, watching your nest egg decline as you remove funds. The successful retirement portfolio will balance growth and your risk tolerance, while aligned with your greater financial and cash flow plan.

Many Cut The Crap Investing readers, and other self-directed investors check in with Cashflows & Portfolios to discover the optimal order and account type spend rates (harvesting funds). That is, the strategic use of RRIF vs TFSA vs Taxable vs Pensions and other income.

I would suggest that you at least consider de-risking your portfolio enough so that you start your retirement in a stress-free manner. That may mean holding enough bonds and cash – even (at least) a cash wedge of 3 years of spending needs.

Check out the rates at EQ Bank.

Don’t let a recession or severe bear market cancel any of your retirement plans.

Thanks for reading. Please drop by the comment section.

You can follow this blog, it’s free. Simply enter your email address in the Subscribe area.

As always this post is not advice. Think of the above as ideas for consideration.

Dale Roberts is the owner operator of the Cut The Crap Investing blog, and a columnist for MoneySense and MillionDollarJourney. This blog originally appeared on MillionDollarJourney on Aug. 17, 2023 and is republished on the Hub with permission.

Dale Roberts is the owner operator of the Cut The Crap Investing blog, and a columnist for MoneySense and MillionDollarJourney. This blog originally appeared on MillionDollarJourney on Aug. 17, 2023 and is republished on the Hub with permission.