Once you achieve Financial Independence, you may choose to leave salaried employment but with decades of vibrant life ahead, it’s too soon to do nothing. The new stage of life between traditional employment and Full Retirement we call Victory Lap, or Victory Lap Retirement (also the title of a new book to be published in August 2016. You can pre-order now at VictoryLapRetirement.com). You may choose to start a business, go back to school or launch an Encore Act or Legacy Career. Perhaps you become a free agent, consultant, freelance writer or to change careers and re-enter the corporate world or government.

If you are Canadian and you buy or sell U.S. stocks, you need to remember that arbitrage in the stock market is your friend, all the more so when it has an assist from AI, or Artificial Intelligence.

Arbitrage is the simultaneous purchase and sale of an asset in different markets, to exploit tiny differences in prices. We take advantage of it for our Portfolio Management clients whenever we can, to cut their trading costs. Here’s how it works:

If we’re selling a Canadian stock for a client and plan to use the proceeds to buy a U.S. stock, we offer the Canadian stock (on a Canadian or U.S. exchange) for sale in U.S. funds. When we want to sell a U.S. stock to buy Canadian, we reverse the order and offer the U.S. stock for sale in Canadian funds.

Now that you can buy and sell in either currency on both sides of the border, arbitrageurs (also known as “arbs” — traders who buy and sell in two different currencies simultaneously) constantly monitor trading activity to spot slight differences in one currency versus the other. When they spot any such difference, they simultaneously buy the stock where it’s cheaper and sell it where it’s more expensive, eking out a tiny profit on the difference.

This trading activity serves to cut cross-border share-price differences to the point where they are, for practical purposes, negligible. This makes the markets more liquid. It cuts trading costs for everybody. Continue Reading…

By Dana Anspach for Fritz Gilbert and The Retirement Manifesto

Special to Financial Independence Hub

Like many teenage girls, I had my high school bedroom walls covered in posters. Actor Rob Lowe took center stage, with a bit of Matt Dillon sprinkled in. (Ladies of the ’80s … any of you relate?)

Mixed in with the heartthrobs were glossy posters of red sports cars. Ferrari. Lamborghini. Later, in college, an Acura NSX.

Looking back, it’s strange. I’ve never been much of a car person: especially not sports cars. I don’t see well out of them. They’re low to the ground. I scrape rims, bump curbs, and the quick handling leaves me feeling slightly queasy.

So why the fascination?

I think those cars represented success. Flashy. Fast. The kind of thing people ‘oohed’ and ‘ahhed’ over.

Defining success by external standards is dangerous business. Thankfully, I outgrew that particular distortion: though I’m sure plenty of others remain.

As an adult, I gravitate toward practical, balanced cars. What I think of as the all-weather vehicle. I don’t need to go 200 mph down the autobahn. But I do want traction in heavy rain. I don’t care about making a statement at the valet. I care about glancing in the rearview mirror and seeing my dog’s smiling face as we head to his favorite place on earth: the park.

That preference for balance turns out to matter far beyond cars. It’s also the way I believe we should approach retirement planning and investing.

The Case for an All-Weather Approach

In hindsight, those sports car dreams and investing have something in common. Sometimes, it’s hard not to hop into the shiny red sports car and drive away.

In investing, a shiny investment (like the shiny red sports car) promises speed and excitement. It may not be as reliable, but for a brief moment, it makes us feel brilliant. Powerful. Maybe even a little invincible. In touch with our inner James Bond. And who doesn’t want to feel like a secret service spy just once in their lifetime?

Often, it shows up as a single stock. Sometimes it’s a real estate deal. Or a business venture. It feels adventurous. Sophisticated. Like we’re seeing something others don’t.

In the late 1990s, tech stocks were the shiny red sports car.

The firm I worked for at the time offered a Science and Technology Fund that rose 99% in twelve months. One day, a middle-aged couple came in and asked me to move their entire portfolio into it.

Durability vs. Speed

Their portfolio had been built for durability:

blue-chip stock funds,

international exposure,

a few bond funds,

and a small allocation to the Science and Tech Fund.

They had spent a year watching the tech fund soar, while everything else stood still.

I balked at their request. I explained the logic of balance. Sure, in perfect weather, the shiny red sports car looked great. But the weather wouldn’t always be so accommodating.

My logic sounded silly to them: like a mom insisting you put on your helmet to ride your bike down the street.

They insisted on the change. I acquiesced on one condition: they sign a disclosure acknowledging that this was against my recommendation. They signed without hesitation.

I left that firm before the dot-com crash and the miserable weather that followed. I’ve often wondered what happened to that couple. The allure of speed was too strong.

Today, I see that allure creep in when retirees keep a “play” account. They go all in on a few stocks and attribute their success to their stock-picking prowess.

You can go all in with a play account. But a professional financial advisor can get sued if they do the same thing with your entire life savings. That should give you pause. Risk and return are sides of the same coin. But each time you flip, if it’s several years of heads, it is all too easy to forget that the coin even has another side.

Beware the Slight Upgrade

Not everyone is tempted by flashy sports cars. Sometimes the pull is subtler.

We start to think maybe a small upgrade will help. Something just a little faster. A little more responsive. Even if it doesn’t handle storms quite as well.

I watched this at the end of 2024 when a long-time client, whose retirement plan and portfolio were in solid shape, left because they felt they should be earning higher returns. Continue Reading…

I originally wrote this article about buying a house in Canada back in 2021: right as the price of housing was picking up. I’ve kept it updated over the last few years as it caught the attention of Rob Carrick over at the Globe and Mail, as well as a few other big names. Five years after writing the initial version of this article, the value proposition on buying a house in Canada has certainly changed!

2026 Editor’s Note: I still don’t own a home, and while I’m not 100% averse to the idea of owning one day, that day is definitely not in the near future

Image by satheeshsankaran from Pixabay

By the end of the summer I will no longer be a homeowner.

In many countries that statement would be a simple matter of personal finance. Selling an asset, paying off a loan (mortgage) and moving on to another living space.

But not in Canada.

No, in Canada selling our house means that my wife and I are making a massive change to our identities. A core shift in our very essence.

Many would say we are taking a careless step backward on the path to living a fulfilled “real adult” life.

Several friends and family will likely believe that we are crazy for tossing away “the best investment one can ever make.”

The absolute obsession with homeownership in Canada continues to astound me. The emotional connection between Canadians and their real estate has been well documented, but that doesn’t make it any more logical! Even though my wife and I have owned a home for years, this was much less because we subscribed to the traditional “own at all costs” mentality, and more due to the fact that rural Manitoba housing vs rent decisions are quite different than most places in Canada.

We’ll certainly miss some of the small luxuries (goodbye big garage) of our old home, but here’s some of the reasons why we believe selling our house will be a weight off of our shoulders.

1) Endless Fear of Hearing a Strange Noise

Is that the furnace taking its last breath?

Perhaps it’s the water treatment system deciding to spring a leak?

Is that rain I hear: is it possible our septic system is backing up?!

My dad loves fixing stuff. His day is not complete until he has improved the physical world around him.

I am not my dad.

My lack of handyman skills has now become a joke that I’m comfortable laughing at, but for years I was incredibly self-conscious about possessing nearly zero masculinity-affirming fix-it ability. You want someone to work hard doing menial chores such as cutting lawns, raking leaves, shovelling snow, or lifting heavy things from Point A to Point B: I got you covered.

Anything that requires technical skills or mechanical problem-solving ability … not so much.

Because my father’s handyman-dominant brain was not passed down to his oldest son, I lived in perpetual fear of things breaking when I owned a home. I never really got this “pride of ownership” thing. For me it was definitely more of a “fear of ownership.” I had so much of my net worth tied up in this one asset – which required constant maintenance – and I really had no idea what it was doing. “Learning by doing” constantly scared me as errors were quite costly.

Hiring any specialized help on something like an air conditioning unit always seemed to cost triple what was estimated, so that just exponentially added to my anxiety levels around maintenance.

Renting = not my problem!!!

2) Is Renting still a Better Financial Decision than Buying in 2026?

Back in 2021 I wrote that it was “quantifiably true” that renting was better than buying. In fact, I went on to say:

I know … that’s a big statement.

It’s probably worth an article all on its own.

It will probably lead to crazy comments (as all real estate articles in Canada do): Editor’s Note: It did!

iii) Here’s Ben Felix’s 5% rule in action. I personally believe that Ben is shooting a bit high on real estate estimates (today’s giant houses are not comparable to historical returns data he quotes), and a bit low on property taxes + maintenance costs. He also isn’t factoring in closing costs (which are a pretty big deal when you move the number of times the average Canadian does), nor the difference between renters insurance and home insurance.

I do like his methodology, but the 5% rule of thumb for non-recoverable costs is pretty badly slanted towards real estate due to the factors mentioned above. I could probably live with a 6% rule: (speaking as a soon-to-be former homeowner of ten years).

Editor’s Note: Ben has done a ton of work in the rent-vs-buy realm since 2021. I still think he’s underestimating maintenance costs, as inflation rates on tradespeople over the last 10 years are really high even relative to overall inflation. His most recent deep dive shows that renting still wins out the majority of the time (even during a massive boom for housing in Canada vs the Great Recession in stocks in 2008).

iv) I’ve talked to many real estate experts who claim “the 1%” rule of thumb is a great filter for a potential landlord looking to add a revenue-generating property to their real estate portfolio.” That means that if you can’t get at least 1% of your purchase price in monthly rent, then it’s not really worth considering the property.

The flip side of that is that if you’re renting for substantially less than 1% of the purchase price of a comparable home: then you’re getting a good deal. Bryce over at Millennial Revolution explains his rule of 150 which comes to similar conclusions.

Those are all great looks at accurately comparing financial costs vs benefits of purchasing a house to live in.

2026 Update: I continue to think these are great rules of thumb for comparing renting and buying. So let’s take a look at how these rules would guide us as we look at rent and buying across Canada in 2026.

Toronto Real Estate

The average price of a property sold in the GTA in March of 2026 was $1,017,796. Interestingly, that’s actually slightly less than when we looked at this in 2021 ($1,108,453) while the average rent is closer to $2,250 (up slightly from $2,100 in 2021). Before we crunch the numbers, it’s interesting to note that both purchase price and rent have went up at a rate less than general inflation since 2021!

Our 1% rule landlord of thumb says that a $1,050,000 house better get you $10,500 per month in rent: or it’s not a good buy.

Using John’s or Preet’s calculators we see that renting is WAY ahead given these parameters.

My modified Ben Felix 6% rule tells us that if we can rent for $5,250 or less: then it’s a pretty good deal to rent. If we stick to his original 5% rule, we need to rent for less than $4,375 to be a good deal.

Bryce’s preferred rule of 150 means that the $2,250 rental average, would dictate a mortgage payment of $1,500 as a good measuring stick for if they should buy.

Conclusion: By any measure … It’s still a better deal to rent in Toronto, even though the price of homes hasn’t gone anywhere in 4 years!

Buying a House in Calgary

Back in 2021, Calgary was still recovering from the oil shock. These days, we see that rents and property values have increased substantially.

The average rent in Calgary is roughly $1,700 (compared to $1,200 back in 2021) and the average cost of a property has gone from $510,000 to about $616,000.

Our 1% rule of thumb says that a $616,000 house better get you $6,160 per month in rent; or it’s not a good buy.

Using John’s or Preet’s calculators we see that renting is substantially ahead given these parameters.

My modified Ben Felix 6% rule tells us that if we can rent for $3,080 or less: then it’s a pretty good deal to rent. If we stick to his original 5% rule, we need to rent for less than $2,567 to be a good deal.

Bryce’s preferred rule of 150 means that the $1,700 rental average, would dictate a mortgage payment of $1,133 as a good measuring stick for if they should buy or not. A $1,133 mortgage would correlate to a purchase price of roughly $250,000.

Even with rental prices going up at a much faster rate than home prices, it’s still a good deal to rent in Calgary!

Home Prices in Halifax

Back in 2021 I decided to throw Halifax into the mix as a substantially different housing market than the big cities like Toronto and Calgary.

In 2026 the average rent in Halifax is about $1,900 per month (versus $1,600 back in 2021) and the average cost of property has risen from $465,000 to about $560,000. (Just a note, these are weighted averages taken from across all home types.)

Our 1% rule of thumb says that a $560,000 house better get you $5,600 per month in rent: or it’s not a good buy.

Using John’s or Preet’s calculators we see that renting is substantially ahead given these parameters.

My modified Ben Felix 6% rule tells us that if we can rent for $2,800 or less: then it’s a pretty good deal to rent. If we stick to his original 5% rule, we need to rent for less than $2,333 to be a good deal.

Bryce’s preferred rule of 150 means that the $1,900 rental average, would dictate a mortgage payment of $1,267 as a good measuring stick for if they should buy or not. A $1,267 mortgage would correlate to a purchase price of under $300,000.

Canada’s current price-to-rent levels are 574% higher than they were in 1970.

Since 1970, Canada’s price-to-rent level has risen at roughly 21x as quickly as the USA’s.

Canada’s current price-to-rent levels are substantially higher now than the USA’s was before their 2008/09 housing crash.

In 2026, I’d add to this:

Our current price-to-rent levels aren’t much changed in 2025, and are still WAY higher than in 1970 (we’re now at about 587% versus 1970).

Since 2021, the U.S. market has cooled slightly more than the Canadian market has, thus exacerbating that comparison point.

Rent dynamics are flipping as supply catches up. After rents jumped 6.3% in 2023 and 7.9% in 2024, vacancy rose from 1.5% (2023) to ~2.3% (2024). Rents have now declined in Canada for 18 consecutive months according to Rentals.ca. Result: asking-rent growth is easing, especially in older stock.

Population policy is easing some demand pressure. Ottawa lowered permanent-resident targets and, for the first time, set caps on temporary residents (aiming to reduce the temp-resident share toward 5% of the population). CMHC explicitly baked in “weakening migration” into its 2025 call for higher rental vacancies.

Clearly, while the numbers have changed slightly, there aren’t really any new conclusions to draw from the rent vs buy math alone.

3) Opportunity Cost of being Rooted into Place

I grew up in a single house: owned by a homeowner. (My parents were unique in that my dad built his own house on a very cheap piece of rural land and never took out a mortgage. Feel free to try and copy that strategy in 2021.)

It was really nice. I get that there can be some very pleasant reasons to own the house/condo that you live in.

But let’s be honest about the big picture here: there are some large trade-offs involved.

Buying a home makes you much less likely to move in order to accept a promotion or career opportunity. That’s impossible to quantify, but it’s a really significant consideration.

One of the quickest ways to climb in any industry (or even make an advantageous jump to a new industry) is to be willing to move to where the opportunity is. The cost to your career of feeling as if you are anchored to the house you worked so hard to get into could be massive!

4) Our Brains Work Differently when we think about Renting a Place to Live vs “Buying a Forever Home” – Lifestyle Inflation is Almost Inevitable.

Funny things begin to happen as we approach the leap from renter to homeowner. Suddenly, cost-benefit calculations we were doing about third bedrooms or fancy kitchens fly out the window … only the best will do for our “forever home” after all.

Weird mantras like, “We’ll grow into it,” begin to creep into our heads and suddenly we’re looking at fancy countertops, upgrading bathrooms, etc.

I’m not sure whether to blame HGTV and the homeshopping shows or what it is, but there is no doubt that most of us look at properties completely differently whether we are renting or buying. Keeping up with the Joneses becomes so much more important (is this what “being a real adult” is truly all about?) when you’re buying and furnishing a house.

One thing that we have learned from moving overseas is that we can be 98% as satisfied in a two-bedroom apartment as we were in our large bungalow. Now, I hear you that things might be different if you have a young family. I’m sure this equation changes substantially when adding children to the picture, but when you look at the smaller average house size that the larger families of yesteryear were raised in, it raises some interesting questions about how much room we all need to be happy.

5) “Drive until you Qualify” = Too Much Driving

I have consistently found that we underestimate the cost of driving: in both lifestyle and dollars!

There have been many studies done on how spending time in the car can really impact your physical health in a myriad of ways. It doesn’t take a genius to figure out that the more time you spend sitting by yourself (often stuck in frustrating traffic) the less healthy and happy you are likely to be.

Maybe this work-from-home thing is going to reduce these financial and physical costs … but I have my doubts as to how many people this will actually affect a few months from now.

When calculating how much your commute will cost you, one needs to factor in depreciation and repairs, in addition to the price of gasoline (or perhaps electricity) and possibly parking. The government of Canada believes it costs about $0.73 per km to drive, while CAA posts similar estimates (and that’s prices from before the recent surge in Canadian gas prices).

At 260 work days per calendar year, every km you move further from your workplace will cost you about $380 per year! If you have two working adults that are both commuting in your household, it doesn’t take long for those numbers to really add up.

6) My House is Definitely NOT the Best Investment I’ve ever Made

If the real estate boosters didn’t try to burn down this website after reading the rent vs own comparison earlier in this article, they will surely reconsider after reading this.

If I’ve heard it once, I’ve heard it two hundred times: “My house is the best investment I’ve ever made.”

While I have written extensively on this topic (and had to explain the point to many parents in the course of teaching personal finance over the years) there is simply no debating the following considerations about owning your home from an investment perspective. Note: We’re not talking about owning a rental property here: that’s a much different conversation.

There are many reasons why the Holy Grail of investment advice is Thou Shalt Diversify. Tying up all of your cash (and then borrowing huge amounts of money that tie up all future earnings) is NOT diversification. Having your entire net worth determined by one building in one location is not a smart risk management decision.

Why is it that when people borrow money to invest in the stock market (known as leverage) it’s considered inherently risky, but when people borrow 9x their downpayment on a house it’s considered “common sense”?

When we think about how much money we’ve “made” on our home, we often forget to include all of the non-recoverable costs involved such as taxes, maintenance and repair costs, transaction fees to buy & sell, renovations that cost way more than they added resale value, etc.

The Case-Shiller Housing Index has stated that between 1928 and 2013, the average annualized rate of return for American housing was 3.7%. The average annual rate of return for American stocks was 9.5% during that time period. Canadian housing and stocks track much the same path.

The National Association of Home Builders in the USA has stated that the average home in 1950 was 983 square feet, and by 2015 it had nearly tripled in size to 2,740 square feet! When you adjust for this fact, the actual increase in value per-square-foot of house is much smaller than the 3-4% number that is commonly tossed around in both Canada and the USA. Likely more in the 1.5-2% territory.

If you think that the last few decades have been the “golden age of Canadian real estate” then you might be surprised to find out that since 1982, Canada’s house prices have only gone up an average of 1.7% per year (vs an average inflation rate of 2.46%).

House values do NOT always go up : no matter what your friend in Toronto says. Go back and ask a Floridian in 2008 or a Calgarian in 2014.

Remember, these considerations are looking backwards at record return decades for Canadian real estate. We are now likely close to the top of that mountain (if not at the peak), so going forward …

Alternative investments to Canadian real estate: View our guide about Canada’s best dividend stocks if you want to learn more about beginner-friendly ways of investing your money into safe non-real-estate assets.

7) Freedom to Travel … Forever

Ok, so this one is likely somewhat unique to us.

I get that not everyone wants to spend years travelling without a fixed address.

That said, I think most Canadians would be amazed at how cheap it is to travel months on end if they don’t have to pay a mortgage back home, and don’t have to fly during the peak weeks of the year. I know that my wife and I were astounded when we went down the digital rabbit hole and found out just how many people were “slow travelling” 12-months per year for under $25,000 CAD.

I don’t think we’re quite as frugal as many of these veteran travellers, but after some pretty extensive research and many conversations with people actually living the “digital nomad” or “FIRE” lifestyle, we think we could pretty easily mix 6 months in relatively expensive countries like Canada, the USA, Western Europe, etc, with 6 months in cheaper countries centred on Eastern Europe and SE Asia, for $40,000 CAD.

2025 Update: My wife and I actually did this last year. We spent 3 months at our family cabin in rural Ontario, then went to Portugal for three months, Thailand for two months, Bali for a month and Japan for a month.

All-in, the price tag came in around $45,000. That includes many flights, an excellent cheap ticket on a Japanese cruise sale, several 3-to-5-day stays at luxury resorts, and several months in good-to-great Airbnbs. Financially, it was a success. It was a bit lonelier than we anticipated at times: but that’s not the math’s fault!

Beyond the obvious fun of seeing more of the world, we love the idea that we will get to spend more time with friends and family that don’t live close to where our 9-to-5 jobs were in rural Manitoba.

AirBnb and competing rental platforms have really changed the game when it comes to attempting to live this “no fixed address” lifestyle. With monthly discounts and competition keeping prices low, finding a place to live for 1-3 months has never been so convenient or affordable. If you want to be responsible for someone’s pets, there are even more affordable travel opportunities available!

Canadian Housing Prices in 2026 (How Expensive is Canada Really?)

After we wrote about gas prices in Canada a couple of weeks ago, I thought it might be useful to take a look at housing affordability in Canada for 2026.

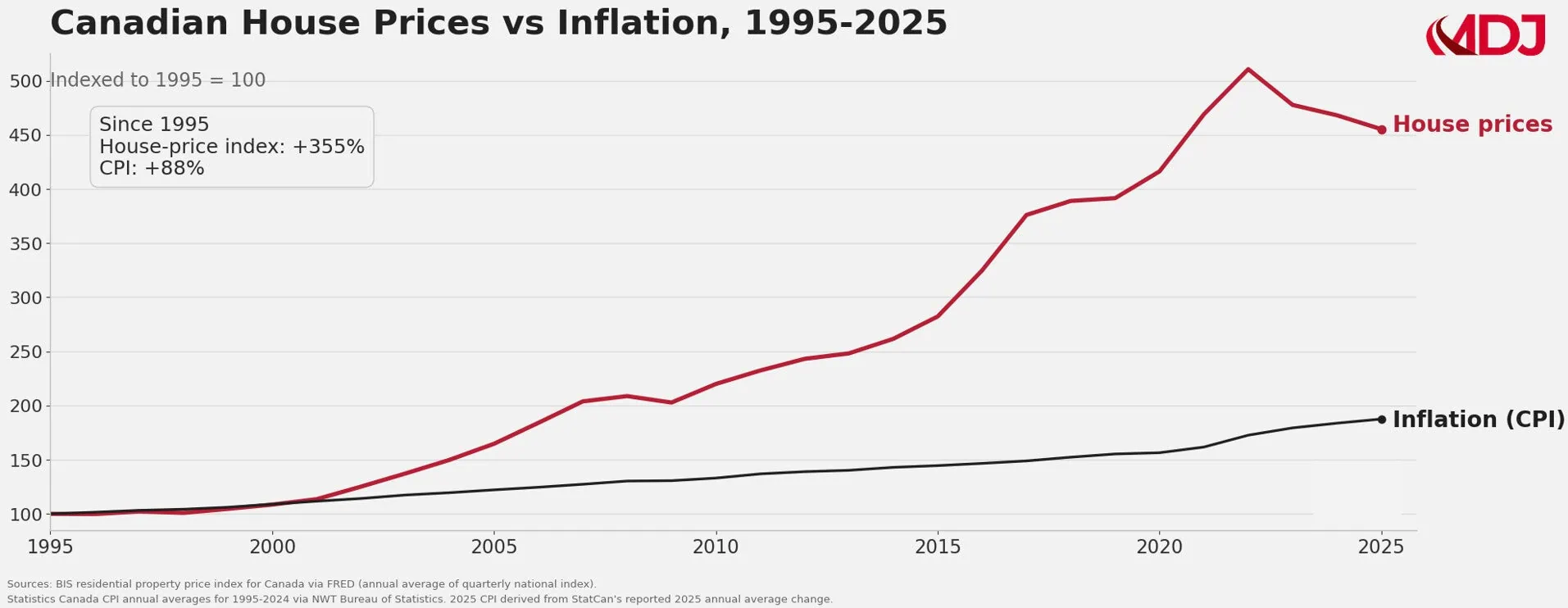

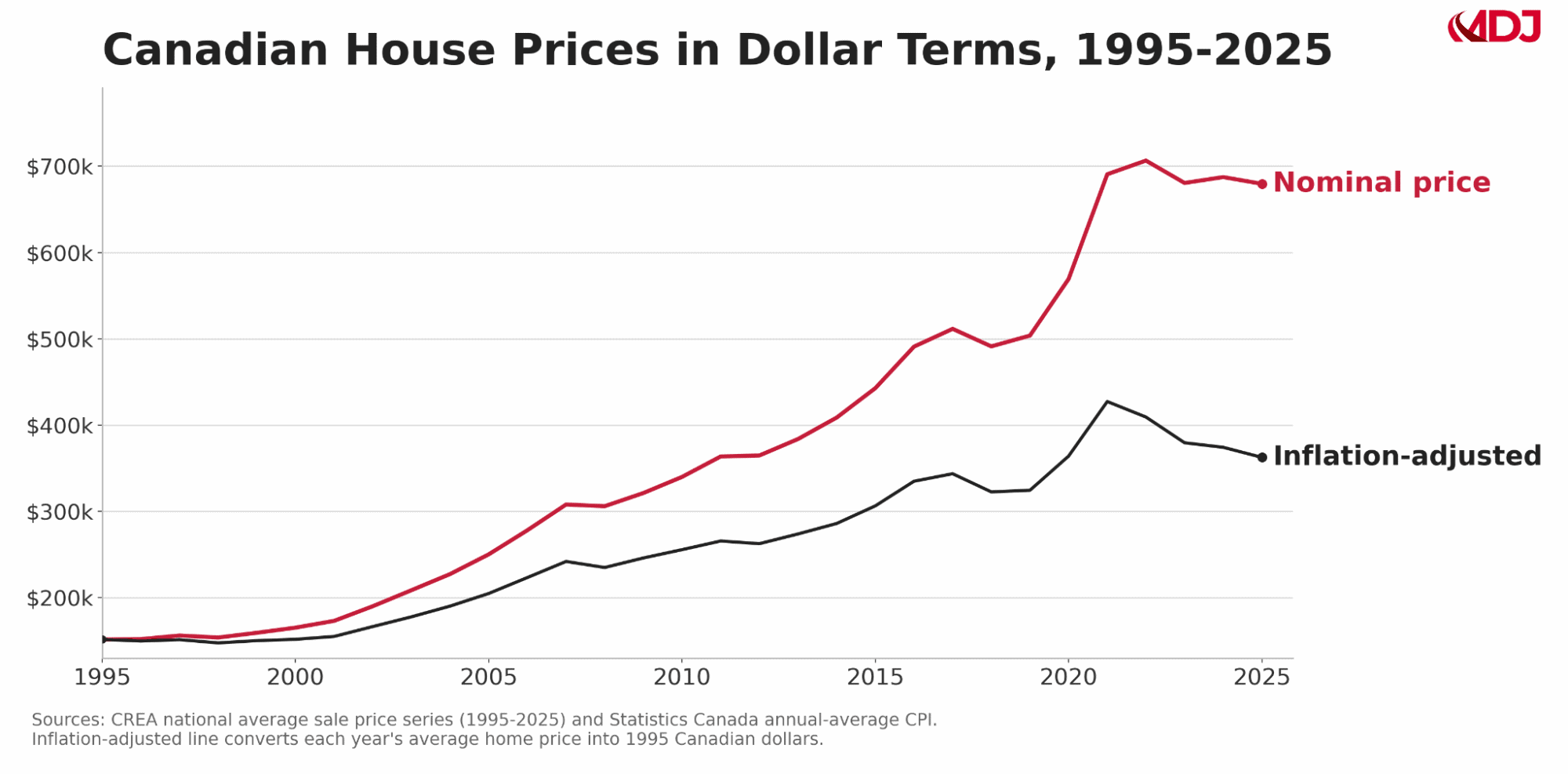

If you’re wondering just how expensive housing has gotten in Canada over time, you can take a look at the inflation-adjusted Canadian house prices charts below. The first one I put together to show just how much faster Canadian housing has went up relative to the average overall inflation (and don’t forget that housing is actually a pretty big part of the overall CPI basket as well, so that means that the gap between housing and “everything else” is actually larger than what you can see here.

Then, I wanted folks to be able to see in real dollar terms just how expensive housing has gotten in Canada and why some folks call it a housing affordability crisis.

It’s pretty clear to see that the cost of living in the Canadian housing category has went up significantly in the last 20 years.

It’s also interesting to note that while Canadian real estate gurus like to say, “Oh the market is just taking a bit of a breather until it goes up again: it has hardly gone down at all.”

… That’s not exactly true in real-life.

Because inflation has been somewhat high the last few years, we see that in inflation-adjusted terms, Canadian housing has actually lost a substantial amount of value. When you compare that to the massive stock market returns of the last five years, I’d say my 2021 housing sentiment holds up pretty well!

The good news is that housing affordability in Canada has improved slightly in the last few years. The bad news is that the overall cost of living for the housing category is still way higher than it was even 20 years ago.

Canada Cost of Living: Housing Costs

I still think a lot of Canadians underestimate where their total housing costs come from. I have yet to meet a homeowner of more than a few years (who didn’t buy new) who thinks they only spend 1% in maintenance. I also think that we look at our mortgage payment and we don’t totally mentally calculate how much of that is interest.

Let’s take a quick look at a plausible home ownership case. Helen the Homeowner decides that she’s ready to take the plunge and buys a $700k house in a small Ontario city.

She has diligently saved up the 70K that she needs (making good use of her FHSA and RRSP). With 10% Helen is going to need a mortgage for nearly $650k because as a high-ratio insured mortgage, she is going to owe some extra. Here’s a rough idea of what her total housing cost of living will be over the next 25 years if she averages a 4.3% mortgage interest rate (pretty generous by historical standards). I’m keeping everything in 2026 dollars here for ease of comparison.

Down payment: $70,000

Home principal repaid: $630,000

Mortgage interest: $407,403

CMHC insurance premium: $19,530

Ontario tax on CMHC premium: $1,562

Property tax: $131,250

Home insurance: $37,500

Maintenance: $262,500

Ontario land transfer tax: $10,475

Total 25-year out-of-pocket cost: about $1,570,220

So for the first 25 years of home ownership, that works out to the following breakdown:

Home principal repaid: 40.1%

Mortgage interest: 26.0%

Maintenance: 16.7%

Property tax: 8.4%

Down payment: 4.5%

Home insurance: 2.4%

CMHC premium: 1.2%

Land transfer tax: 0.7%

Tax on CMHC premium: 0.1%

It’s interesting to note that the actual price of the home is significantly less than half of the total housing cost of living.

It’s OK to Own a Home – and It’s OK NOT to Own one Too!

It’s odd to say, but that makes it no less true: Owning your home in Canada is an emotional decision heavily tied to middle-class identity.

Because the decision is so important, no one likes to think that they chose the “wrong” path. Consequently, there are very few rational conversations to be had when it comes to home ownership. Like most issues that cut to the core of our identity, we usually choose our side, and then selectively look for arguments or data to support the decision we made.

I’ve been on both sides of the home ownership debate and the only thing that I can decisively say is that for some people owning a home makes sense: but for many others it simply does not.

Hey, if you are 80%+ sure that you’re going to be rooted in the same area for 10+ years, and you derive a lot of enjoyment out of handyperson fixes/renos, then the benefits of home ownership might make it the perfect choice for you.

That said, judging by all the “buy at all costs” talk I continue to hear from coast-to-coast, I think we really need to examine the bigger picture when it comes to home ownership.

2026 Update: Very little has changed since 2021 that has led me to change my thinking on rent vs buy. You can see in the comments below that it hit a major pain point for a lot of folks (as I predicted it would). While rent and housing prices remain fairly stagnant in most markets since 2021 (and have actually decreased relative to general inflation).

At the end of 2020, the S&P 500 was at USD$3,756 and the TSX 60 was at CAD$1,034. As of writing this update they are at $7,126 and $1,996 respectively. Good for a stock market gain of 90% and 93% respectively. Once you factor in that the S&P 500 would have spun off a dividend of a little less than 2%, and the TSX 60 would have rewarded you with 3%, the case for stocks gets even stronger.

Now, who knows, the next five years could look much different, but I’m going to take a victory lap on this controversial article for the time being!

Kyle Prevost is a financial educator, author and speaker. When he’s not on a basketball court or in a boxing ring trying to recapture his youth, you can find him helping Canadians with their finances over at MillionDollarJourney.com, and the Canadian Financial Summit.The newly updated version of this blog appeared on MillionDollarJourney on April 24, 2026. It has been slightly edited and is republished on Findependence Hub with permission.

My latest MoneySense Retired Money column expands on a blog written by Devin Partida on my site while we were away in Malta and Italy. In there you can see three photos from our trip, including the one shown here.

For MoneySense, I reached out through Linked In and Featured.com to bounce this idea off various Retirement Experts and Business Owners in North America.

The full Retired Money column can be accessed by clicking this hyperlink: Financial Independence and Travel: Can you have both? The column runs a normal 1200 words or so but the actual responses ran about five times that long, which you can find by clicking on this link also on Findependence Hub. (It ran over the weekend, as did the MoneySense summary of it).

Naturally, I agree with Devin’s original topline conclusion: that “maintaining Financial Independence while traveling is entirely possible with a proper strategy.” As some of the sources indicate, technology and the Internet means most professionals or so-called “Knowledge Workers” can really practice their craft most anywhere in the world that has Web access.

Digital Nomads

The colourful term “Digital Nomad” is often used to describe such globe-trotting workers. Of course, travelling the world by Baby Boomers like myself is relatively straightforward if you spent decades building up pensions and a Retirement nest egg. Ideally at the end of 30 or 40 years of “working for the man (or woman)”, you end up with the lovely combination of relatively endless time and sufficient financial resources to indulge your globe-trotting desires.

Leisure

But the MoneySense column also passes on several tips that can be used by those who are only semi-retired, or even decades from Retirement but who have embraced the so-called FIRE movement: Financial Independence Retire Early. There’s even a term I hadn’t encountered until I researched this piece: Bleisure, which is of course a contraction of the words Business and Pleasure. Continue Reading…

That blog inspired me to reach out to multiple financial experts and business owners, with the assistance of Linked In and Featured.com, which has been supplying this site with quality content for several years.

Here’s how we posed the question:

Can you pursue Financial Independence (or Retirement or Semi-Retirement) without giving up Travel? See this blog for one opinion on this topic:

Malta: where we spent most of February this year. Photo by J. Chevreau

This particular topic attracted 84 comments by the April 20th deadline: this blog presents 25 or so that I selected. It’s long so I’ve summarized the main points with subheadings.

Note also that my latest MoneySense Retired Money column summarizes some of the main points, more succinctly as there is limited space for that column (about 1300 words, compared to the nearly 6,000 words that appear in the particular blog you are now reading).

To ease the reading burden, I’ve added subheads, some of which include:

Geoarbitrage: Live where cost of Living is lower

Renting RVs for Extended Travel Stretches

Make Travel a regular fixed expense you plan on incurring every month

Treat Travel as a budget category, not a luxury to eliminate

Embrace slow travel, house-sitting, points travel hacking and off-season destinations

Buy property in tourist spots to fund Travel

Majority of Professionals can now work remotely

The “goal isn’t to eliminate travel, but rather to make it more intentional.”

“Bleisure”: Let your career fund your transit

As President of Safe Harbors Travel Group, I’ve spent decades helping organizations use strategic logistics and “Bleisure” to explore the world without draining the bottom line. You can reach Financial Independence by letting your career fund your transit; we often help clients integrate vacation days into business trips to eliminate personal airfare and lodging costs.

A key strategy for the budget-conscious traveler is utilizing “humanitarian airfares,” a specialized airline product Safe Harbors provides that offers significant savings for anyone doing charitable, religious, or mission-based work. These fares are a powerful hack for those pursuing a purpose-driven life while keeping their personal travel expenses at a minimum.

By leveraging our elite tech partnerships for data-driven booking, you can ensure “duty of care” and response speed that prevents the costly emergencies often associated with unmanaged travel. This structured approach allows you to focus on wealth building while Safe Harbors handles the complexities of your global footprint. — Jay Ellenby, President, Safe Harbors

Build Travel into the system, not just a later Reward

Yes: you can chase FI or semi-retirement and keep travelling if you build travel into the system instead of treating it like a reward you “earn later.” I’ve run logistics/transportation businesses for years and now my wife and I host 15 furnished units in Detroit/Chicago, so I’m used to designing operations that still run when I’m not physically there.

What made it work for us is shifting travel from “big expensive trips” to “repeatable, planned mobility.” We use our Detroit-focused blog as a planning engine: when we travel, we test neighborhoods, transit (Q-Line/SMART/MoGo), and local routines the same way a guest would: then we bake that learning back into listings and guest guides so travel time also improves the business.

The practical FI move is making your income less dependent on your daily presence. Guest reviews told us people wanted clearer walkthroughs, so we added walkthrough videos to each property page and saw a 15% increase in booking conversions: less back-and-forth, fewer preventable questions, more freedom to be away while keeping standards consistent.

If you want one tactic you can copy: record a 5-8 minute “first night in the unit” walkthrough (lockbox – thermostat – Wi-Fi – parking – trash) and reuse it forever. That single asset cuts support load while you’re on the road, and it’s the difference between “I can travel” and “travel breaks my cashflow.” — Sean Swain, Company Owner, Detroit Furnished Rentals LLC

Geoarbitrage: Live where cost of Living is lower

Geoarbitrage allows you to live in an area with a lower cost of living for your family while allowing your investment portfolio to grow. The combination of using travel rewards on credit cards and traveling during less expensive times reduces your travel costs. This approach to finding money saving ways to see the world makes international exploration a viable way to maintain your lifestyle versus making it a luxury. — Zack Moorin, Founder, Zack Buys Houses

Geoarbitrage and the Second Act Advantage

In The Second Act Advantage, I show how geoarbitrage lets anyone achieve financial independence without sacrificing travel: in fact, it makes travel the strategy. By earning in strong currencies while living and exploring more affordable parts of the world, everyone can enjoy a richer, more adventurous life while actually spending less. The book teaches readers how to design a life where freedom, fulfillment, and financial efficiency all work together. — Jay Samit, Bestselling Author, The Second Act Advantage

Transitioning from Vacationing to Geo-arbitrage

The Travel-First Strategy: Designing FI Without Sacrifice

A common misconception in the FIRE (Financial Independence, Retire Early) community is that travel is a luxury to be deferred until the finish line. However, in my experience advising lifestyle-focused entrepreneurs, pursuing financial independence without giving up travel isn’t just possible it’s often a more sustainable strategy for preventing burnout.

Shifting from Consumer to Global Resident

The key is transitioning from vacationing to Geo-arbitrage. Traditional travel involves paying retail prices for short-term stays, which can cripple a savings rate. A strategic traveler focusing on FI prioritizes medium-term stays in regions where the cost of living is lower than their home base. By spending months in hubs like Portugal, Mexico, or Southeast Asia, you can often live a high-quality lifestyle for 40% less than in major Western cities. In this model, travel actually accelerates your path to financial independence by lowering your monthly burn rate.

Leveraging Credit Strategy as an Asset Class

From a PR and financial positioning standpoint, we should treat travel rewards not as points, but as a shadow asset class. A sophisticated FI seeker uses strategic credit card optimization to ensure that their transportation and lodging line items remain near zero. When flights and hotels are covered by systemic spending, travel stops being a drain on investment capital and becomes a tool for lifestyle maintenance.

The Semi-Retirement Pivot

The all-or-nothing approach to retirement is becoming obsolete. We are seeing a rise in Coast FIRE, where individuals reach a baseline of savings and then transition into remote-first or consulting roles. This allows for perpetual travel while the core nest egg continues to compound undisturbed. By integrating travel into the pursuit of FI rather than viewing it as a reward for the end of it, you create a life you don’t feel the need to escape from. This ensures that when you finally reach full independence, you already possess the global literacy to enjoy it. — James Tech, SEO Marketer, TripFrog

58% of Millennials and GenZ prioritize Travel over Material Accumulation

Financial Independence and travel are not mutually exclusive; in fact, they increasingly reinforce each other when approached strategically. A growing body of research highlights the rise of “geo-arbitrage,” where professionals leverage remote work or location flexibility to reduce living costs while continuing to explore new destinations.

According to a 2024 report by Deloitte, nearly 58% of Gen Z and millennials prioritize experiences like travel over material accumulation, reshaping traditional financial planning models. At the same time, the World Tourism Organization notes a steady increase in long-stay and work-from-anywhere travel patterns, indicating that travel is no longer viewed as a luxury pause but as an integrated lifestyle choice.

From a workforce perspective, continuous upskilling and digital proficiency — particularly in areas like project management, agile practices, and cybersecurity — enable professionals to maintain income streams while remaining location-independent.

Financial independence, therefore, is less about restriction and more about intentional design: aligning income strategies, skill development, and lifestyle priorities in a way that sustains both economic security and personal fulfillment. — Arvind Rongala, CEO, Invensis Learning

Renting RVs for Extended Travel Stretches

Absolutely yes: and I’ll tell you why from an angle most people overlook: your cost of living on the road can actually shrink dramatically while you’re building toward FI.

I run DFW RV Rentals, placing travel trailers for displaced families and insurance claims. What I see constantly is people discovering — often during the worst moments of their lives — that a well-equipped travel trailer is genuinely livable, comfortable, and cheap compared to a mortgage or apartment lease.

Here’s the FI angle nobody talks about: renting an RV for an extended travel stretch eliminates storage fees, maintenance headaches, depreciation, and insurance costs that crush RV owners. I’ve watched people romanticize ownership, buy a unit, and watch it become a financial anchor: whereas someone renting strategically keeps capital free and mobile.

If you’re pursuing FI and want travel woven in, think of RV rental as a variable living expense you control, not a lifestyle luxury. A few months on the road in a rented trailer can cost less than your fixed housing back home: and that gap is real money compounding toward independence. — Jonathan Dies, Owner, DFW RV Rentals

Maintenance-free Retirement communities

As Executive Director of The Village at Mint Spring and Stuarts Draft Retirement Community for over 16 years, I’ve guided hundreds toward maintenance-free retirement living that supports financial goals without homeownership burdens.

Yes, financial independence or semi-retirement pairs perfectly with travel when you eliminate upkeep costs like repairs, lawn care, snow removal, and property taxes: freeing budget and time for trips.

Our residents use the shuttle for local outings while traveling afar, knowing onsite care partners like Visiting Angels handle needs back home.

Fall incentives like up to $3,500 moving allowance make the shift easier, letting you lock in FI sooner and explore without stress. — David Brenneman, Owner, The Village at Mint Spring

Adopt a “Cash Rules Everything” mindset

As an advisor to business owners earning $400K+, I’ve found that financial independence is about aligning your strategy with your personal values rather than following generic industry models. I build plans for my clients that prioritize clarity and lifestyle flexibility, ensuring travel is a core component of the strategy rather than a sacrifice.

When the April 2025 market volatility caused equities to waver due to new tariffs, clients with high-liquidity strategies avoided the “dash for cash” and kept their travel plans intact. I focus on a “cash rules everything” mindset during periods of uncertainty to ensure market jitters don’t interrupt your personal milestones or global adventures.

I use the Altruist platform to give my clients a technology-driven, transparent view of their wealth from any location. This allows entrepreneurs to monitor their progress toward retirement and make confident decisions via mobile tools without being tethered to an office.

True financial guidance starts with understanding your long-term vision so your portfolio serves your life, not the other way around. By creating a practical action plan focused on stability and growth, you can pursue financial freedom while maintaining the lifestyle you have already worked to build. — Daniel Delaney, Owner, Seek & Find Financial

Make Travel a regular fixed expense you plan on incurring every month

Many people misunderstand the idea of being financially independent as a way to have nothing but austerity during their time of independence; however, the reality is that it’s just about allocating your money in a conscious manner. Too often, people will make travel an ‘additional’ expense that must be eliminated in order to achieve their savings goals: this can lead to burn out and a living arrangement that does not continue.

The problem is that travel is often treated as an item that has been paid for with ‘loose change’ after all of the other ‘necessary’ expenses have been paid each month; therefore when budgeting, travel should be included as a regular fixed expense you plan on incurring every month.

To have travel as part of your work-life balance, you will need to establish your savings plan with this in mind. Business places do this as well; you do not build a business just by lowering your cost structure, you have to build a company based on what gives you the highest return on your investment for the long-term. The same should be true for any travel related goal that you desire to achieve. One of the pitfalls that many individuals fall into when comparing their way of saving to the ways that people in the ‘lifestyle’ mode of saving demonstrate is that they fail to establish their own pace and their definition of ‘enough.’

Finding that work-life balance about not simply doing the math correctly, but making certain to build a lifestyle in which you would prefer to ‘Get up and do it!’ every single day. — Abhishek Pareek, Founder & Director, Coders.dev Continue Reading…

If you are Canadian and you buy or sell U.S. stocks, you need to remember that arbitrage in the stock market is your friend, all the more so when it has an assist from AI, or Artificial Intelligence.

If you are Canadian and you buy or sell U.S. stocks, you need to remember that arbitrage in the stock market is your friend, all the more so when it has an assist from AI, or Artificial Intelligence.