No doubt about it: at some point we’re neither semi-retired, findependent or fully retired. We’re out there in a retirement community or retirement home, and maybe for a few years near the end of this incarnation, some time to reflect on it all in a nursing home. Our Longevity & Aging category features our own unique blog posts, as well as blog feeds from Mark Venning’s ChangeRangers.com and other experts.

My latest MoneySense Retired Money column looks at a handful of FIRE bloggers who should be familiar to readers of this site, Findependence Hub: notably Mark Seed of myownadvisor and Bob Lai of Tawcan.

As you can see by clicking on the column headline, How are FIRE adherents making out?, Seed recently announced he has reached his Financial Independence in his early 50s. Bob Lai, meanwhile, is still working in his 40s but blogged on how he hopes to reach Findependence before 2030.

The MoneySense column also updates the status of veteran personal finance columnist Rob Carrick, who ended full-time employment at the Globe & Mail last year, the subject of an earlier Retired Money column. And we mention a good blog by The Retirement Manifesto’s Fritz Gilbert about the 12 Good Years between age 60 and 72. As I ironically close the column with, it seems I have just used up my own 12 good years!

The real focus of the MoneySense column is however Mark Seed, just as it was Carrick last summer. In both cases, we exchanged views in Zoom or GoogleMeets over the course of an hour or so.

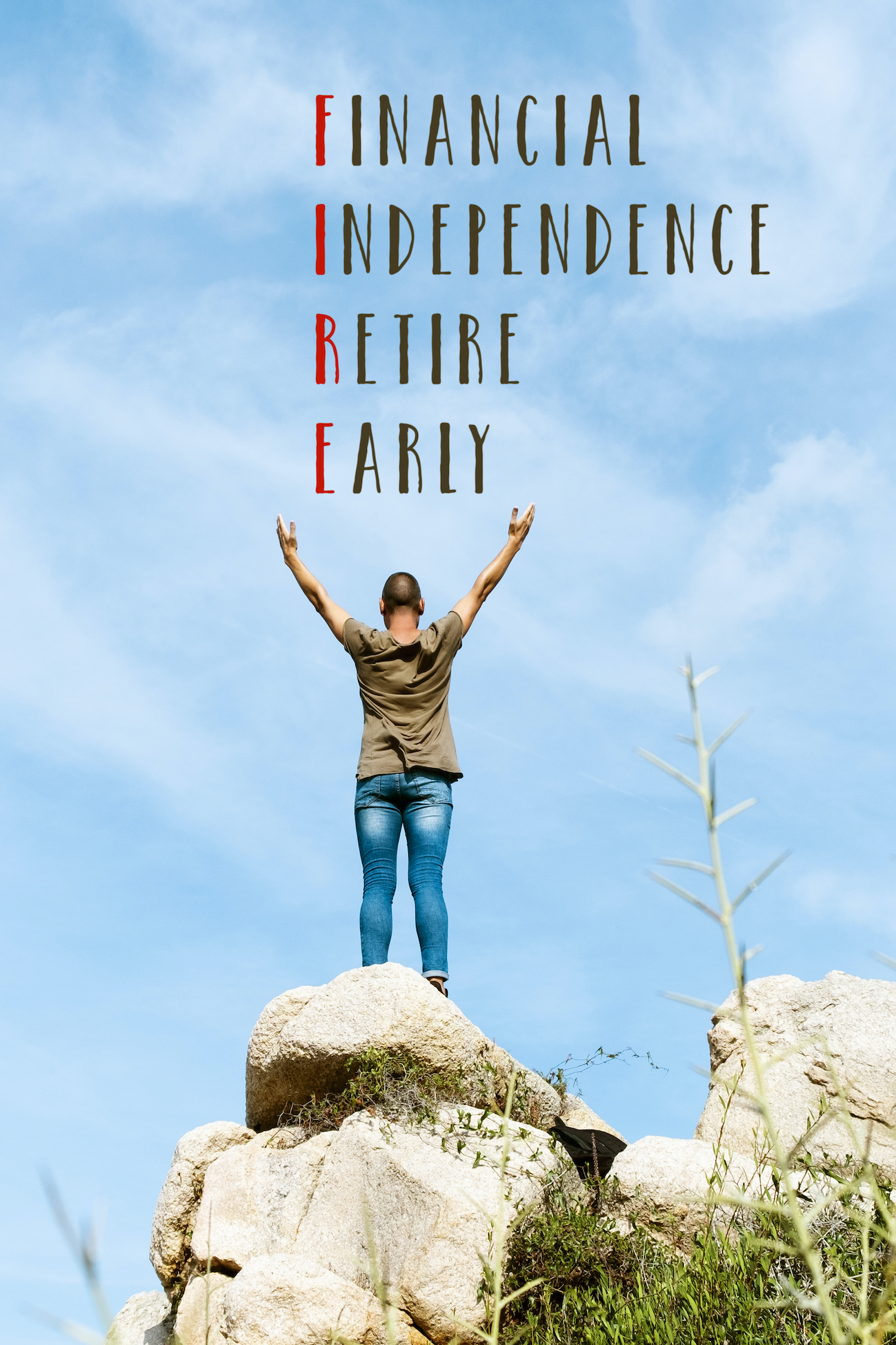

By now, it’s hardly necessary to remind readers that the FIRE acronym stands for Financial Independence Retire Early, as the image above illustrates.

Note that our FIRE subjects in the column span four decades: Lai his 40s, Seed his 50s, Carrick his 60s and I am in my 70s, evidently still running this website and writing for MoneySense, a former employer.

The end of Salaried Employment does not mean no more Working

The observant reader will note that none of the bloggers mentioned here have actually begun the traditional “Full-Stop Retirement.” When FIRE proponents describe Early Retirement, they usually mean leaving the comfort of full-time salaried employment and all that it entails: commuting, bosses, endless meetings, tax deducted at source, annual performance reviews and so on. Continue Reading…

My latest MoneySense Retired Money column expands on a blog written by Devin Partida on my site while we were away in Malta and Italy. In there you can see three photos from our trip, including the one shown here.

For MoneySense, I reached out through Linked In and Featured.com to bounce this idea off various Retirement Experts and Business Owners in North America.

The full Retired Money column can be accessed by clicking this hyperlink: Financial Independence and Travel: Can you have both? The column runs a normal 1200 words or so but the actual responses ran about five times that long, which you can find by clicking on this link also on Findependence Hub. (It ran over the weekend, as did the MoneySense summary of it).

Naturally, I agree with Devin’s original topline conclusion: that “maintaining Financial Independence while traveling is entirely possible with a proper strategy.” As some of the sources indicate, technology and the Internet means most professionals or so-called “Knowledge Workers” can really practice their craft most anywhere in the world that has Web access.

Digital Nomads

The colourful term “Digital Nomad” is often used to describe such globe-trotting workers. Of course, travelling the world by Baby Boomers like myself is relatively straightforward if you spent decades building up pensions and a Retirement nest egg. Ideally at the end of 30 or 40 years of “working for the man (or woman)”, you end up with the lovely combination of relatively endless time and sufficient financial resources to indulge your globe-trotting desires.

Leisure

But the MoneySense column also passes on several tips that can be used by those who are only semi-retired, or even decades from Retirement but who have embraced the so-called FIRE movement: Financial Independence Retire Early. There’s even a term I hadn’t encountered until I researched this piece: Bleisure, which is of course a contraction of the words Business and Pleasure. Continue Reading…

That blog inspired me to reach out to multiple financial experts and business owners, with the assistance of Linked In and Featured.com, which has been supplying this site with quality content for several years.

Here’s how we posed the question:

Can you pursue Financial Independence (or Retirement or Semi-Retirement) without giving up Travel? See this blog for one opinion on this topic:

Malta: where we spent most of February this year. Photo by J. Chevreau

This particular topic attracted 84 comments by the April 20th deadline: this blog presents 25 or so that I selected. It’s long so I’ve summarized the main points with subheadings.

Note also that my latest MoneySense Retired Money column summarizes some of the main points, more succinctly as there is limited space for that column (about 1300 words, compared to the nearly 6,000 words that appear in the particular blog you are now reading).

To ease the reading burden, I’ve added subheads, some of which include:

Geoarbitrage: Live where cost of Living is lower

Renting RVs for Extended Travel Stretches

Make Travel a regular fixed expense you plan on incurring every month

Treat Travel as a budget category, not a luxury to eliminate

Embrace slow travel, house-sitting, points travel hacking and off-season destinations

Buy property in tourist spots to fund Travel

Majority of Professionals can now work remotely

The “goal isn’t to eliminate travel, but rather to make it more intentional.”

“Bleisure”: Let your career fund your transit

As President of Safe Harbors Travel Group, I’ve spent decades helping organizations use strategic logistics and “Bleisure” to explore the world without draining the bottom line. You can reach Financial Independence by letting your career fund your transit; we often help clients integrate vacation days into business trips to eliminate personal airfare and lodging costs.

A key strategy for the budget-conscious traveler is utilizing “humanitarian airfares,” a specialized airline product Safe Harbors provides that offers significant savings for anyone doing charitable, religious, or mission-based work. These fares are a powerful hack for those pursuing a purpose-driven life while keeping their personal travel expenses at a minimum.

By leveraging our elite tech partnerships for data-driven booking, you can ensure “duty of care” and response speed that prevents the costly emergencies often associated with unmanaged travel. This structured approach allows you to focus on wealth building while Safe Harbors handles the complexities of your global footprint. — Jay Ellenby, President, Safe Harbors

Build Travel into the system, not just a later Reward

Yes: you can chase FI or semi-retirement and keep travelling if you build travel into the system instead of treating it like a reward you “earn later.” I’ve run logistics/transportation businesses for years and now my wife and I host 15 furnished units in Detroit/Chicago, so I’m used to designing operations that still run when I’m not physically there.

What made it work for us is shifting travel from “big expensive trips” to “repeatable, planned mobility.” We use our Detroit-focused blog as a planning engine: when we travel, we test neighborhoods, transit (Q-Line/SMART/MoGo), and local routines the same way a guest would: then we bake that learning back into listings and guest guides so travel time also improves the business.

The practical FI move is making your income less dependent on your daily presence. Guest reviews told us people wanted clearer walkthroughs, so we added walkthrough videos to each property page and saw a 15% increase in booking conversions: less back-and-forth, fewer preventable questions, more freedom to be away while keeping standards consistent.

If you want one tactic you can copy: record a 5-8 minute “first night in the unit” walkthrough (lockbox – thermostat – Wi-Fi – parking – trash) and reuse it forever. That single asset cuts support load while you’re on the road, and it’s the difference between “I can travel” and “travel breaks my cashflow.” — Sean Swain, Company Owner, Detroit Furnished Rentals LLC

Geoarbitrage: Live where cost of Living is lower

Geoarbitrage allows you to live in an area with a lower cost of living for your family while allowing your investment portfolio to grow. The combination of using travel rewards on credit cards and traveling during less expensive times reduces your travel costs. This approach to finding money saving ways to see the world makes international exploration a viable way to maintain your lifestyle versus making it a luxury. — Zack Moorin, Founder, Zack Buys Houses

Geoarbitrage and the Second Act Advantage

In The Second Act Advantage, I show how geoarbitrage lets anyone achieve financial independence without sacrificing travel: in fact, it makes travel the strategy. By earning in strong currencies while living and exploring more affordable parts of the world, everyone can enjoy a richer, more adventurous life while actually spending less. The book teaches readers how to design a life where freedom, fulfillment, and financial efficiency all work together. — Jay Samit, Bestselling Author, The Second Act Advantage

Transitioning from Vacationing to Geo-arbitrage

The Travel-First Strategy: Designing FI Without Sacrifice

A common misconception in the FIRE (Financial Independence, Retire Early) community is that travel is a luxury to be deferred until the finish line. However, in my experience advising lifestyle-focused entrepreneurs, pursuing financial independence without giving up travel isn’t just possible it’s often a more sustainable strategy for preventing burnout.

Shifting from Consumer to Global Resident

The key is transitioning from vacationing to Geo-arbitrage. Traditional travel involves paying retail prices for short-term stays, which can cripple a savings rate. A strategic traveler focusing on FI prioritizes medium-term stays in regions where the cost of living is lower than their home base. By spending months in hubs like Portugal, Mexico, or Southeast Asia, you can often live a high-quality lifestyle for 40% less than in major Western cities. In this model, travel actually accelerates your path to financial independence by lowering your monthly burn rate.

Leveraging Credit Strategy as an Asset Class

From a PR and financial positioning standpoint, we should treat travel rewards not as points, but as a shadow asset class. A sophisticated FI seeker uses strategic credit card optimization to ensure that their transportation and lodging line items remain near zero. When flights and hotels are covered by systemic spending, travel stops being a drain on investment capital and becomes a tool for lifestyle maintenance.

The Semi-Retirement Pivot

The all-or-nothing approach to retirement is becoming obsolete. We are seeing a rise in Coast FIRE, where individuals reach a baseline of savings and then transition into remote-first or consulting roles. This allows for perpetual travel while the core nest egg continues to compound undisturbed. By integrating travel into the pursuit of FI rather than viewing it as a reward for the end of it, you create a life you don’t feel the need to escape from. This ensures that when you finally reach full independence, you already possess the global literacy to enjoy it. — James Tech, SEO Marketer, TripFrog

58% of Millennials and GenZ prioritize Travel over Material Accumulation

Financial Independence and travel are not mutually exclusive; in fact, they increasingly reinforce each other when approached strategically. A growing body of research highlights the rise of “geo-arbitrage,” where professionals leverage remote work or location flexibility to reduce living costs while continuing to explore new destinations.

According to a 2024 report by Deloitte, nearly 58% of Gen Z and millennials prioritize experiences like travel over material accumulation, reshaping traditional financial planning models. At the same time, the World Tourism Organization notes a steady increase in long-stay and work-from-anywhere travel patterns, indicating that travel is no longer viewed as a luxury pause but as an integrated lifestyle choice.

From a workforce perspective, continuous upskilling and digital proficiency — particularly in areas like project management, agile practices, and cybersecurity — enable professionals to maintain income streams while remaining location-independent.

Financial independence, therefore, is less about restriction and more about intentional design: aligning income strategies, skill development, and lifestyle priorities in a way that sustains both economic security and personal fulfillment. — Arvind Rongala, CEO, Invensis Learning

Renting RVs for Extended Travel Stretches

Absolutely yes: and I’ll tell you why from an angle most people overlook: your cost of living on the road can actually shrink dramatically while you’re building toward FI.

I run DFW RV Rentals, placing travel trailers for displaced families and insurance claims. What I see constantly is people discovering — often during the worst moments of their lives — that a well-equipped travel trailer is genuinely livable, comfortable, and cheap compared to a mortgage or apartment lease.

Here’s the FI angle nobody talks about: renting an RV for an extended travel stretch eliminates storage fees, maintenance headaches, depreciation, and insurance costs that crush RV owners. I’ve watched people romanticize ownership, buy a unit, and watch it become a financial anchor: whereas someone renting strategically keeps capital free and mobile.

If you’re pursuing FI and want travel woven in, think of RV rental as a variable living expense you control, not a lifestyle luxury. A few months on the road in a rented trailer can cost less than your fixed housing back home: and that gap is real money compounding toward independence. — Jonathan Dies, Owner, DFW RV Rentals

Maintenance-free Retirement communities

As Executive Director of The Village at Mint Spring and Stuarts Draft Retirement Community for over 16 years, I’ve guided hundreds toward maintenance-free retirement living that supports financial goals without homeownership burdens.

Yes, financial independence or semi-retirement pairs perfectly with travel when you eliminate upkeep costs like repairs, lawn care, snow removal, and property taxes: freeing budget and time for trips.

Our residents use the shuttle for local outings while traveling afar, knowing onsite care partners like Visiting Angels handle needs back home.

Fall incentives like up to $3,500 moving allowance make the shift easier, letting you lock in FI sooner and explore without stress. — David Brenneman, Owner, The Village at Mint Spring

Adopt a “Cash Rules Everything” mindset

As an advisor to business owners earning $400K+, I’ve found that financial independence is about aligning your strategy with your personal values rather than following generic industry models. I build plans for my clients that prioritize clarity and lifestyle flexibility, ensuring travel is a core component of the strategy rather than a sacrifice.

When the April 2025 market volatility caused equities to waver due to new tariffs, clients with high-liquidity strategies avoided the “dash for cash” and kept their travel plans intact. I focus on a “cash rules everything” mindset during periods of uncertainty to ensure market jitters don’t interrupt your personal milestones or global adventures.

I use the Altruist platform to give my clients a technology-driven, transparent view of their wealth from any location. This allows entrepreneurs to monitor their progress toward retirement and make confident decisions via mobile tools without being tethered to an office.

True financial guidance starts with understanding your long-term vision so your portfolio serves your life, not the other way around. By creating a practical action plan focused on stability and growth, you can pursue financial freedom while maintaining the lifestyle you have already worked to build. — Daniel Delaney, Owner, Seek & Find Financial

Make Travel a regular fixed expense you plan on incurring every month

Many people misunderstand the idea of being financially independent as a way to have nothing but austerity during their time of independence; however, the reality is that it’s just about allocating your money in a conscious manner. Too often, people will make travel an ‘additional’ expense that must be eliminated in order to achieve their savings goals: this can lead to burn out and a living arrangement that does not continue.

The problem is that travel is often treated as an item that has been paid for with ‘loose change’ after all of the other ‘necessary’ expenses have been paid each month; therefore when budgeting, travel should be included as a regular fixed expense you plan on incurring every month.

To have travel as part of your work-life balance, you will need to establish your savings plan with this in mind. Business places do this as well; you do not build a business just by lowering your cost structure, you have to build a company based on what gives you the highest return on your investment for the long-term. The same should be true for any travel related goal that you desire to achieve. One of the pitfalls that many individuals fall into when comparing their way of saving to the ways that people in the ‘lifestyle’ mode of saving demonstrate is that they fail to establish their own pace and their definition of ‘enough.’

Finding that work-life balance about not simply doing the math correctly, but making certain to build a lifestyle in which you would prefer to ‘Get up and do it!’ every single day. — Abhishek Pareek, Founder & Director, Coders.dev Continue Reading…

Akaisha and Billy playing tennis in Arizona: RetireEarlyLifestyle.com

People often tell us they are going to wait a few more years to retire.

They point out that by waiting, they will have health care provided for life and a pension that will let them afford the same lifestyle to which they’ve become accustomed. They won’t have to scale back on spending or make awkward choices concerning their budgets. Not only will they not need to relocate to a city or state that is more affordable, they will be able to own two houses: one at home with their country club membership, and another on a lake, near a beach, or in a foreign country.

Sounds great

These people have worked their entire lives for this remarkable retirement plan.

They have made personal sacrifices throughout the years such as spending time away from the family, not pursuing their hobbies, and not taking long sabbaticals. They have made these choices because in doing so, their retirement plan will be fully guaranteed.

After investing 35 or 40 years of their working lives, saving their money, raising children, and putting their own personal wants on the back burner, they now look forward to that day when they can relax and finally enjoy the life they deserve.

No tough decision making, no cutting back on their consumer habits.

Or at least, that’s how they think it’ll be.

There are no guarantees

What we have learned in our three decades of financial independence is that the perfect time for retirement simply doesn’t exist. Things change, and sometimes radically.

Perhaps your personal plan for retirement was to take big amounts of equity out of your home. But then the housing market takes a dive or your home or is affected by something out of your control. Oops.

Natural disasters can come up, affecting your lifestyle and investments. Forest fires, floods, hurricanes, earthquakes, drought can all threaten your home whether you have insurance or not. What an upheaval! It’s a financial and emotional storm no one wants to go through.

Financial markets have their earthquakes too. While the market over the years has performed at about a 10% annual return including dividends since we retired in 1991, those of us who are older now and receiving Social Security might not have the time to recover from something drastic.

Health challenges

We have a myriad of friends who, as they worked and aged, have had health problems affect either them or their spouses. One man wanted to travel through Europe, but now has developed claustrophobia (due to an earlier trauma he suffered) and can no longer fly, or take a cruise in a tiny cabin, far from shore.

What if you or your spouse find yourselves with a medical condition that doesn’t allow you the freedom you fought so hard to achieve? What if your grandchild has special needs and requires assistance, time, or your financial help?

Where can you look for comfort in circumstances such as these?

Reap reward from your self-reliance

If you have learned to live below your means, have kept your monthly expenses reasonably low, and have not loaded up with huge amounts of consumer debt, the above scenarios could be an uncomfortable bump in the road, but not a life-defining event.

If you find yourself awash in a financial storm and the days down the road seem dark and menacing or if your retirement dreams seem to be permanently shelved, try some of the following steps to regroup:

Stay calm.

People retire every day, in good times and bad. Like deciding to have a child, it’s never the perfect time. Realize that it’s normal in life for unforeseen events to rattle your confidence level, so try not to let it faze you. Above all, do not make a reflexive emotional decision about the rest of your life by making a bad trade, or an impulsive decision about your home.

Be independent.

Make your own retirement investments independent of your employer’s plan. Don’t rely solely on your employer for your retirement, whether it’s through a traditional pension or with company stock in a 401(k). This way, if your company goes under for reasons you cannot see today, you’ll still be in control of your future.

Know where you stand.

Get support from your past good behaviour. If you have been tracking your spending and living below your means, you know exactly where you are financially. The confidence and discipline of controlling spending should give you great self-assurance that you can weather any storm. And you will know exactly where to make spending changes if need be. Look for buying opportunities.

It’s always a good time to review your portfolio to see whether you have been over-concentrated in one stock or in one particular sector. We recommend no more than 4% in any one particular stock, and that includes the companies you worked for. A balanced portfolio with roughly 60% equities to 40% cash/bonds and equivalents for those in or nearing retirement is a good approach.

Invest in no-load ETFs (Exchange Traded Index Funds) such as VTI, Vanguard Total Market Fund or SPY, S&P 500 Index, that you can buy or sell in real time, instead of the market price at the day’s end and use weakness in the market to add to your positions.

If the idea of fully retiring frightens you, consider working part time, cutting back the hours at your current job, doing consulting work, or starting a second career. You’ll still earn income, but you may not have the same work demands that your current job makes of you.

Get creative.

Consider other alternatives for the expression of your retirement life. Perhaps you now have the incentive to think about relocating to a smaller home, a more affordable city, or to own one vehicle instead of two. You don’t need to shelve your future plans entirely. Find other ways of scaling down pressure and moving toward fun, relaxation, and new ways of self-expression.

You are not alone. If you find yourself in a financial or health challenge, there are others who are facing something similar. They may have an answer for you, share some tips or point you in the right direction to receive the help you are looking for.

No matter what your circumstances, there are always opportunities, there are always options. Be open to them and make the most of where you are!

Billy and Akaisha Kaderli are recognized retirement experts and internationally published authors on topics of finance, medical tourism and world travel. With the wealth of information they share on their award winning website RetireEarlyLifestyle.com, they have been helping people achieve their own retirement dreams since 1991. They wrote the popular books, The Adventurer’s Guide to Early Retirement and Your Retirement Dream IS Possible available on their website bookstore or on Amazon.com. This blog first appeared at RetireEarlyLifestyle.com and is republished on Findependence Hub with their permission.

By Dale Roberts, Retirement Club/Cutthecrapinvesting

Special to Financial Independence Hub

The Globe & Mail offers ongoing real-life retirement funding (cash flow plan) scenarios. They also invite a financial planner to offer their opinion. They call the series Financial Facelift. A recent article caught my eye. I thought I would give it a go using a popular free use retirement software that allows DIY retirees and near retirees to run their own plans.

The following is a cash flow review from the Globe. I was curious, so I started to enter the details at MayRetire: a very intuitive, easy-to-use (free use) retirement cash flow calculator.

And I’ll show you how: you can join Dale for a …

How to use MayRetire Intro Zoom Call Session

You can join a 12 pm or 7 pm EST session this Thursday, April 16th.

Ennis and Kara are planning to retire soon, leaving behind joint family income of more than $340,000 a year. Ennis is 61 years old and earns $220,000 a year in senior management. His wife, Kara, is 54 and earns $120,000 in research.

Both have defined-benefit pensions. Ennis’s will be $27,960 a year, while Kara’s will pay $9,000 a year. Both pensions are only partly indexed to inflation, his 50 per cent, hers 60 per cent.

“We’ve received no shortage of advice on how to prepare for this transition, but are interested in getting an experienced, objective view on whether we can retire on our timeline or are being overly optimistic,” Ennis writes in an e-mail.

Both anticipate receiving inheritances at some point.

Their goals are to travel and help their three young adult children buy first homes when the family cottage is sold. Their share will be about $150,000.

The couple’s home in an Ontario city is valued at $1.1-million, and has a $300,000 mortgage. Their retirement spending goal is $135,000 a year after tax.

The G&M asked Ian Calvert, a certified financial planner and head of wealth planning at HighView Financial in Oakville, Ont., to look at Ennis’s and Kara’s situation.

What the expert says

Ennis and Kara have a net worth of about $2.18-million, Mr. Calvert says.

“They have a healthy asset base, and their pensions are a strong component of their retirement plan,” he notes. “However, without any non-registered assets or tax-free savings accounts (TFSAs), all of their withdrawals in retirement will be treated as taxable income, with the exception of their cash savings.”

To fund their cash flow requirements, they will need to withdraw about $129,000 a year from their combined RRSPs and locked-in retirement accounts, or LIRAs, the planner says.

“Before they start consistent withdrawals from these accounts, they should consider converting their RRSPs to registered retirement income funds (RRIFs) and unlock 50 per cent of their LIRAs,” Mr. Calvert says.

Unlocking 50% of the LIRAs

The unlocking of retirement assets adds more flexibility: They are moving assets out of LIRAs, which have annual withdrawal maximums, into RRSPs, which do not.

Moving assets from RRSPs to RRIFs makes sense because they are entering their withdrawal phase and need consistent income from these accounts.

“It’s important to remember that the 50 per cent unlocking is a one-time option that should be completed at age 55 or older when you are completing the transfer from a LIRA to a life income fund (LIF) and starting to withdraw.”

The couple’s $129,000 withdrawal, plus combined pension income of $37,000 a year, will give them a total family income of $166,000 a year, less $31,000 in income taxes. This will meet their after-tax spending target of $135,000.

“The required annual withdrawals from their retirement savings represent about 10 per cent of their portfolio,” the planner notes. “It would be challenging to maintain their capital at this withdrawal rate, and they should expect a decline in capital over time.”

Fortunately, they have two items that will reduce the withdrawal rate. “First, they are expecting a combined inheritance of about $1.3-million in the next few years,” Mr. Calvert says. “Second, they will both be getting Canada Pension Plan and Old Age Security benefits.”

When their inheritance comes through, they should use part of it to fund their TFSAs to the maximum available limit at the time, Mr. Calvert says. Currently, the lifetime maximum TFSA contribution is $109,000 each, increasing by $7,000 each year.

This will leave a substantial amount to be invested in their non-registered portfolio.

“Investing the remaining non-registered funds to generate steady and reliable income would be beneficial for a couple of reasons,” the planner says. With $1-million or so to invest, “they should build a portfolio structure that not only will participate in growth, but will generate a consistent dividend yield of about 3.5 per cent, or $35,000 a year.”

Relying on inheritance

The inheritance money will give them much more flexibility, the planner says. They will have funds they can access without adding to their taxable income. However, the new investment income from the funds they can’t shelter in their TFSAs will be reported and taxed every year.

“Once their inheritance is received, they could withdraw $35,000 per year from the non-registered portfolio and reduce the withdrawals from their RRSPs and LIRAs to about $89,000 a year. This, combined with their pension income of about $38,000 (with inflation), would bring their total income to about $162,000 year while reducing their taxes to $27,000 per year, he says.

When to take CPP and OAS will depend on the timing and amount of their expected inheritance, the planner says. Without the inheritance, starting their benefits at age 65 would help reduce the annual withdrawals from their portfolio, the planner says.

Because of the seven-year difference in their ages, Ennis and Kara have time to think about when to take benefits. “They could take a hybrid approach,” the planner says. “For instance, if no inheritance was received by 2029 when Ennis turns 65, they could start his CPP and OAS payments to reduce the withdrawals from their savings,” he says. “They would still have lots of time to make the decision for Kara because she won’t turn 65 until 2037.”

They also ask about helping their children. “The challenge in their current position is they don’t have the after-tax capital to do it today,” Mr. Calvert says. “Large withdrawals from their RRSPs would not be tax-efficient and would further hasten the decline in their capital,” he says. “Their only other option is to pull equity from their house, which would come with additional debt servicing.”

The situation

The people: Ennis, 61, Kara, 54, and their three children, 20, 24 and 26.

The problem: Can they afford to retire soon and still meet their retirement spending goal?

The plan: A lot depends on the anticipated inheritance. They’d be drawing heavily on their registered savings in the early years. Ennis could start his government benefits at 65 to keep the withdrawals to a minimum. Continue Reading…