By Robb Engen, Boomer & Echo

Special to the Financial Independence Hub

I know it’s tough to save money. It’s even more difficult to up the ante and increase your savings year-after-year. But saving is necessary to meet both our short- and-long-term financial goals. Without any savings, and living paycheque-to-paycheque every month, you’ll either work until you die or else retire in extreme poverty.

So what will it take for you to save more this year? Some people start off small, saving two or three per cent of their salary, and that’s fine – every little bit counts. But many of us short-change our retirement by not finding ways to increase that amount every year. Here are four easy ways to save more in 2015:

- Take up a challenge

All the rage in 2014 – the 52-week money saving challenge was pinned, posted, and shared across social networks and blogs to help inspire people to save. Ordinary Canadians, who’d typically only post about their vacation and dining experiences, were taking up the challenge and talking about money. Fantastic!

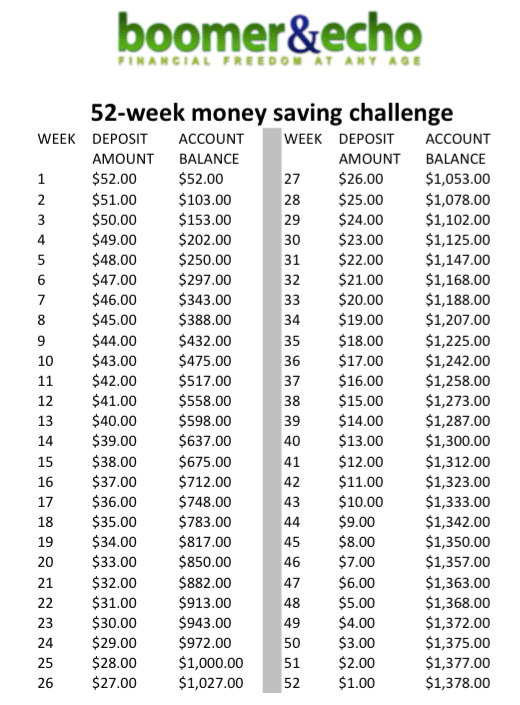

The 52-week money saving challenge is simple: Save $1 in week one, $2 in week two, $3 in week three, and so on until you have about $1,400 saved by the end of the year. Or, increase the degree of difficulty and try to put away $10 in week one, $20 in week two, $30 in week three, and so on until you’ve saved nearly $14,000.

The best variation I’ve found is the reverse challenge where savers put aside $52 in week one, $51 in week two, $50 in week three, and so on. The reverse order works well because the bulk of the saving happens at the start of the year while you’re still motivated.

Let’s be honest – who’s going to remain excited after saving a measly $10 in January? But with the reverse challenge, come December, when money is tighter, the amount you need to save goes down as your spending is likely to increase. You’ll also get compound interest working for you earlier, and the habit of saving more early on just might stick with you for the entire year.

- Find your match

Many employers offer a contribution-matching savings program. But according to industry experts, Canadians are leaving as much as $3-billion on the table by not taking advantage of these programs. Employers are only paying out between 40 to 50 per cent of available matching funds.

Some employers will kick in 50 cents for every dollar you contribute, while others will match you dollar-for-dollar. One could argue that skipping out on an employer-matching program is a worse financial move than carrying a credit-card balance for a year. That’s because you’d give up a guaranteed return of between 50 and 100 per cent in order to pay down credit-card debt at 19 per cent.

I get it, most of these plans are voluntary and that portion of your salary feels better in your bank account than in some group plan that you can’t touch until retirement. But if your employer offers you free money, free money that doubles your retirement contribution, you take it!

The same goes for government matching programs like the Canada Education Savings Grant, which provides grants to RESP contributors – 20 per cent on every dollar of the first $2,500 you save inside an RESP each year. That’s up to $500 in free money for your child’s education.

- Bank your raise

One sure-fire way to boost your savings is to bank your annual raise. Okay, salary increases are few and far between in this economic climate. I know – last summer I got my first raise in nearly five years. But if you are managing to get an annual increase, even if it’s just cost of living, here’s an example of how to make it work for you:

Most retirement calculators assume that you save a fixed amount every year and that number doesn’t grow with inflation.

John is 25 and earns $50,000 per year. He can afford to save $250 per month ($3,000 per year) toward his retirement.

The conventional “pay-yourself-first” approach doesn’t assume any increase in that amount over time, and so after 40 years of saving $3,000 per year John will have $480,000 saved for retirement. Not bad.

But how much would John have if he simply increased his savings rate along with his two per cent annual raise? It doesn’t sound like much, but it would mean an additional $145,000 at retirement – or $625,000.

- Build on what’s already working

Most of us have already have some sort of automated savings plan in place, whether it’s a percentage of income that gets funnelled into our RRSP or TFSA, or monthly contributions to our child’s RESP. Even your mortgage payment is a forced automated savings plan.

Build on the good things that you already have in place. Increase your monthly mortgage payments by $50 or $100. You’ll easily take a few years off the life of your mortgage – especially if you make a habit of increasing your payments annually.

Keep bumping up the contributions to your RRSP, TFSA, and RESP until you start maxing out the annual limits. Once you get there – see if you can catch up on unused contribution room to further bolster your savings.

Final thoughts

There’s always room to improve our finances each year, but often we get complacent with our savings plans and fall victim to financial inertia.

Find a way to grow your savings every year, whether through a fun challenge, by taking advantage of employer and government matching programs, banking your raise, or by simply building on what’s already working for you.

This blog originally appeared on January 4th here at the Boomer & Echo site. In addition to running the site, Robb and Marie Engen are fee-only financial planners. You can also find them listed at the Hub’s Getting Help section.

How are you supposed to compound with money when you don’t have the money to do it with at the end of the month