By Billy and Akaisha Kaderli, RetireEarlyLifestyle.com

Special to Financial Independence Hub

We’ve written about this for years in our books.

When preparing for retirement, designing your portfolio for income is over-rated. Oh, it feels good bragging about how much money you make each year, but then you also quiver about the taxes you owe each April.

What’s the point?

To make it – then give it back – makes no sense.

With today’s interest rates, people are being forced to look elsewhere.

Our approach 3 decades ago

When we retired 36 years ago, having annual income was not on our minds. Knowing we had decades of life-sans-job ahead of us, we wanted to grow our nest egg to outpace inflation and our spending habits as they changed too. Therefore, we invested fully in the S&P 500 Index.

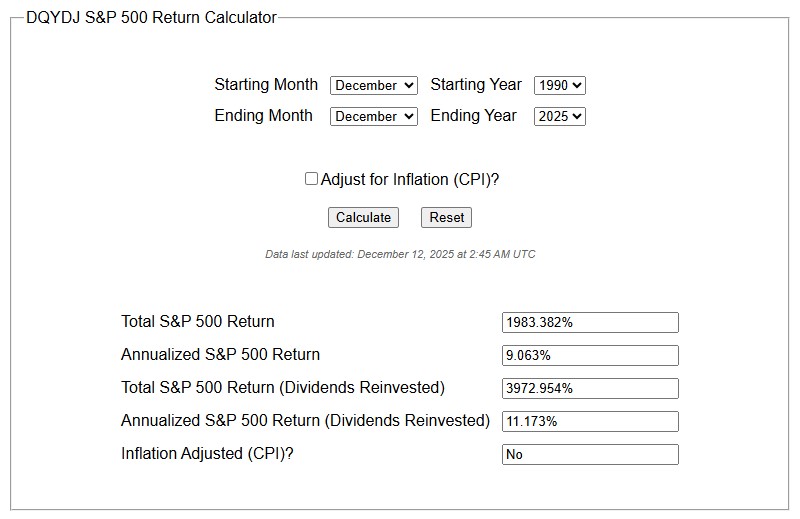

On the day we left the working world the S&P 500 closed at 312.49.

We will get back to this in a minute.

500 solid, well-managed companies

The S&P Index are 500 of the best-managed companies in the United States.

Our financial plan was based on the idea that these solid companies would survive calamities of all sorts and their values would be expressed in higher future stock prices outpacing inflation. After all, these companies are not going to sell their products at losses. Instead they would raise their prices as needed to cover the expenses of both rising resources and wages, thereby producing profits for their shareholders.

How long has Coca-Cola been around? Well over 100 years and the company went public in 1919 when a bottle of Coke cost five cents.

Inflation cannot take credit for all of their stock price growth as they created markets globally and expanded their product line.

This is just one example of the creativity involved in building the American Dream. The people running Coke had a vision and have executed it through the years. Yes, “New Coke” was a flop as well as others, but the point is that they didn’t stop trying to grow because of a setback.

Coca-Cola is just one illustration of thousands of companies adapting to current trends and expanding with a forward vision.

Look at Elon Musk. He has dreams larger than most of us can imagine.

What I want to state here is that when we retired in 1991, the S&P 500 closed at 312.49. Today it is north of 6900 – a 10% annual return.

Sell as needed

Another benefit we have in designing our portfolio in this manner, is that when we sell shares for “income,” they are taxed at a more favorable rate as a long-term capital gain. Dividend output is low, our tax liability is minimal, yet our net worth has grown, out-pacing spending and inflation.

We are in control of our income stream.

Our suggestion is not to base your retirement income on income-producing investments but rather to go for growth. You can always sell a few shares to cover your living expenses. For more on Retirement Topics, click here and here and don’t forget to signup for our free Newsletter.

Billy and Akaisha Kaderli are recognized retirement experts and internationally published authors on topics of finance, medical tourism and world travel. With the wealth of information they share on their award winning website RetireEarlyLifestyle.com, they have been helping people achieve their own retirement dreams since 1991. They wrote the popular books, The Adventurer’s Guide to Early Retirement and Your Retirement Dream IS Possible available on their website bookstore or on Amazon.com. This blog first appeared at RetireEarlyLifestyle.com and is republished on Findependence Hub with their permission.

Billy and Akaisha Kaderli are recognized retirement experts and internationally published authors on topics of finance, medical tourism and world travel. With the wealth of information they share on their award winning website RetireEarlyLifestyle.com, they have been helping people achieve their own retirement dreams since 1991. They wrote the popular books, The Adventurer’s Guide to Early Retirement and Your Retirement Dream IS Possible available on their website bookstore or on Amazon.com. This blog first appeared at RetireEarlyLifestyle.com and is republished on Findependence Hub with their permission.

This article makes sense. Thank you.