Commentary by Joseph H. Davis, PhD, Vanguard global chief economist

Republished with permission of Vanguard Canada

There’s only one sure way to identify an asset bubble, and that’s after the bubble has burst. Until then, a fast-appreciating asset may seem overvalued, only for its price to keep rising. Anyone who has tried to breathe one last breath into a balloon and finds it can accommodate two or three more breaths can relate.

Yale University’s William Goetzmann learned just how hard it can be to pinpoint a bubble. He found that assets whose prices more than double over one to three years are twice as likely to double again in the same time frame as they are to lose more than half their value.1

Vanguard believes that a bubble is an instance of prices far exceeding an asset’s fundamental value, to the point that no plausible future income scenario can justify the price, which ultimately corrects. Our view is informed by academic research dating from the start of this century, before the dot-com bubble burst.

Are there asset bubbles out there now? We at Vanguard have great respect for the uncertainty of the future, so the best we can say is “maybe.” Some specific markets, such as U.S. housing and cryptocurrencies, seem particularly frothy. U.S. home prices rose 10.4% year-over-year in December 2020, their biggest jump since recovering from the global financial crisis.2 But pandemic-era supply-and-demand dynamics, rather than speculative excess, are likely driving the rise.

Cryptocurrencies, on the other hand, have soared more than 500% in the last year.3 It’s a curious rise for an asset that is not designed to produce cash flows and whose price trajectory seems like that of large-capitalization growth stocks: the opposite of what one would expect from an asset meant to hedge against inflation and currency depreciation. Rational people can disagree over cryptocurrencies’ inherent value, but such discussions today might have to include talk of bubbles.

What about U.S. stocks? The broad market may be overvalued, though not severely. Yet forthcoming Vanguard research highlights one part of the U.S. equity market that gives us pause: growth stocks. Low-quality growth stocks especially test our “plausible future income” scenario. For some high-profile companies, valuation metrics imply that their worth will exceed the size of their industry’s contribution to U.S. GDP. Conversely, our research will show that U.S. value stocks are similarly undervalued.

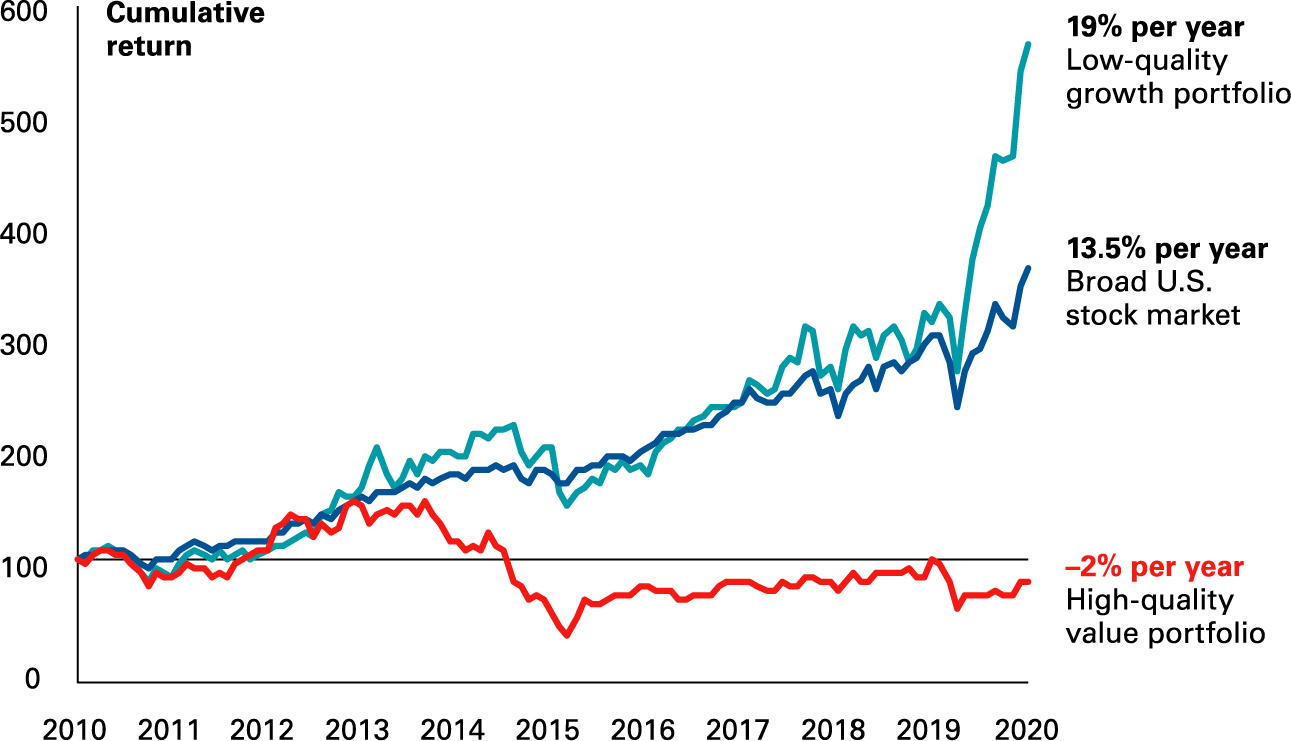

Notes: Data as of December 31, 2020. Portfolios are indexed to 100 as of December 31, 2010. Low-quality growth and high-quality value portfolios are constructed based on data from Kenneth R. French’s website, using New York Stock Exchange-listed companies sorted in quintiles by operating profit and the ratio of book value to market value (B/P). The low-quality growth portfolio is represented by the lowest quintile operating profit (quality) and B/P companies. The high-quality value portfolio is represented by the highest quintile operating profit and B/P companies. The broad U.S. stock market is represented by the Dow Jones U.S. Total Stock Market Index (formerly known as the Dow Jones Wilshire 5000) through April 22, 2005; the MSCI US Broad Market Index through June 2, 2013; and the CRSP US Total Market Index thereafter. Source: Vanguard calculations, based on data from Ken French’s website at Dartmouth College, mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html; MSCI; CRSP; and Dow Jones. Past performance is no guarantee of future returns. The performance of an index is not an exact representation of any particular investment, as you cannot invest directly in an index.

Low-quality growth stocks — companies with little to no operating profits — have outperformed the broad market by 5.5 percentage points per year over the last decade. Of course, there are reasons why growth stocks may be richly valued compared with the broad market. Growth stocks, by definition, are those anticipated to grow more quickly than the overall market. Their appeal is in their potential. But the more that their share prices rise, the less probable that they can justify those higher prices. A small handful of these “low-quality growth” companies may become the Next Big Thing. But many more may fade into obscurity, as occurred after the dot-com bubble.

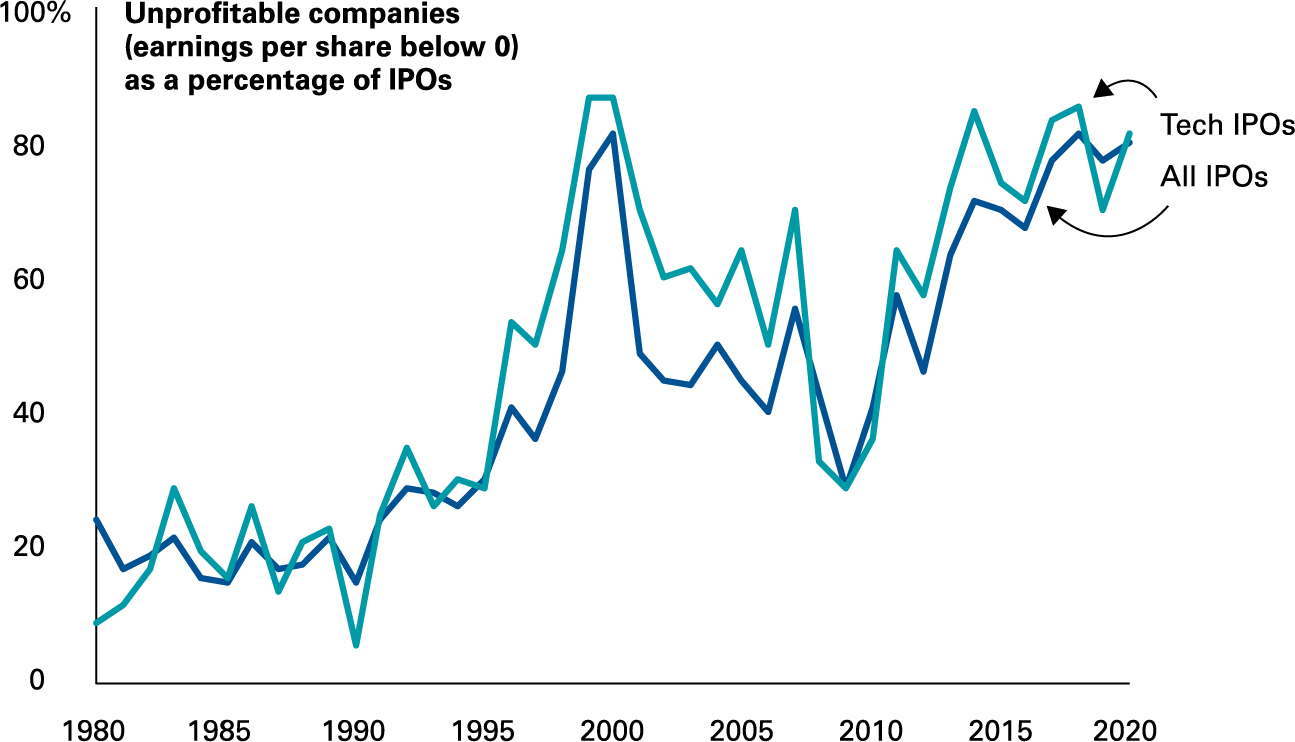

The market for initial public offerings offers some insights (with my thanks to colleagues in Vanguard Quantitative Equity Group). Four out of five companies that offered shares on public markets for the first time in 2020 had earnings per share below zero. The percentage of such unprofitable IPOs has been nearly as high for the last several years, comparable to the numbers seen in the years leading up to the dot-com bubble. Such dynamics could create the catalyst for a hard landing for growth stocks. Of the unprofitable IPOs in 2020, more than 80% were in the technology and biotech sectors.4

Notes: Data as of December 31, 2020. Source: Vanguard calculations, using data from Jay R. Ritter’s website at the University of Florida, site.warrington.ufl.edu/ritter/ipo-data/, excluding American Depositary Receipts, natural-resource limited partnerships and trusts, closed-end funds, real estate investment trusts, special purpose acquisitions companies, banks and savings and loans, unit offers, penny stocks (with an offer price of less than $5 per share), and stocks not listed on the Nasdaq or the New York Stock Exchange for all IPOs.

Value stocks, by contrast, trade at prices below what company fundamentals suggest are reasonable. These steady companies seem to have been around forever and are likely to stay around. High-quality value stocks have underperformed the broad market by 15.5 percentage points per year over the last decade.

We don’t expect the trends that defined the last decade to persist

As we outlined in the Vanguard Economic and Market Outlook for 2021: Approaching the Dawn, we expect equity markets outside the United States to outperform U.S. equities and expect value stocks to outperform growth. Our December 2020 research A Tale of Two Decades for U.S. and Non-U.S. Equity: Past Is Rarely Prologue underscores our beliefs, as does our forthcoming assessment of growth and value stocks.

Performance variation between investing styles and sectors is among the reasons Vanguard believes that investors should hold broadly diversified portfolios, as highlighted in Vanguard’s Principles for Investing Success. Those who do so benefit from a natural rebalancing that occurs over time as market segments outperform and underperform.

However, investors with conviction in their assessment of the markets, the time horizon to be patient, and the discipline to hold firm amid volatility may benefit from an overweight allocation to value stocks commensurate with their risk tolerance. Such a tilt could help offset the lower broad-market returns we expect in the decade ahead compared with the decade past.

We appreciate that fast-rising assets may grow richer still. But, at some point, the markets will be faced with a question related to our definition of asset bubbles: What plausible future income scenario justifies an asset’s price? We expect that valuations eventually will reflect companies’ true probability of profitability, especially in the most-stretched corners of the market.

I’d like to thank Ian Kresnak, CFA, and my colleagues in Vanguard Quantitative Equity Group for their invaluable contributions to this commentary.

1 Goetzmann, William N., 2016. Bubble Investing: Learning from History. Working Paper No. 21693. Cambridge, Mass: National Bureau of Economic Research

2 S&P CoreLogic Case-Shiller 20-City Composite Home Price NSA Index for December 2020. Accessed on January 26, 2021.

3 Based on data from CoinMarketCap as of February 22, 2021.

4 Vanguard calculations using data from the website of Jay Ritter, University of Florida, https://site.warrington.ufl.edu/ritter/ipo-data/ excluding American Depositary Receipts, natural resource limited partnerships and trusts, closed-end funds, real estate investment trusts, special purpose acquisitions companies, banks and savings and loans, unit offers, penny stocks (with an offer price of less than $5 per share), and stocks not listed on the Nasdaq or the New York Stock Exchange for all IPOs.

Important information The views expressed in this material are based on the author's assessment as of the first publication date (March 2021), are subject to change without notice and may not represent the views and/or opinions of Vanguard Investments Canada Inc. The author may not necessarily update or supplement their views and opinions whether as a result of new information, changing circumstances, future events or otherwise. Any "forward-looking" information contained in this material should be construed as general investment or market information and no representation is being made that any investor will, or is likely to achieve, returns similar to those mentioned in this material or anticipated in this material. While this information has been compiled from sources believed to be reliable, Vanguard Investments Canada Inc. does not guarantee the accuracy, completeness, timeliness or reliability of this information or any results from its use. This material is for informational purposes only. This material is not intended to be relied upon as research, investment, or tax advice and is not an implied or express recommendation, offer or solicitation to buy or sell any security or to adopt any particular investment or portfolio strategy. Any views and opinions expressed do not take into account the particular investment objectives, needs, restrictions and circumstances of a specific investor and, thus, should not be used as the basis of any specific investment recommendation. Please consult your financial and/or tax advisor for financial and/or tax information applicable to your specific situation. Information, figures and charts are summarized for illustrative purposes only and are subject to change without notice. In this material, references to "Vanguard" are provided for convenience only and may refer to, where applicable, only The Vanguard Group, Inc.