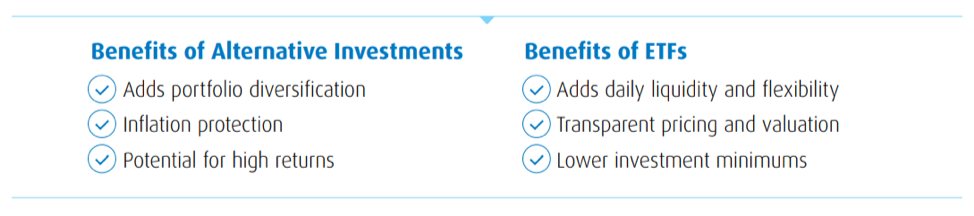

At a time when market volatility, rising rates and high inflation are a common denominator, investors are looking for alternative solutions that can boost returns, while diversifying their asset mix away from traditional assets and fixed income.

In 1991, an investor with a portfolio of only Canadian bonds could have earned an annualized return of ~11% over 5 years. [1] Investors have increasingly had to look to alternative assets to add diversification, for growth and income generation, and enhanced returns with more challenging market environments

Alternative investments include non-traditional assets, like real estate and infrastructure. Investors can access these types of investment through ETFs that invest in public securities to give exposure to alternative investments offering greater diversification to a portfolio.

Infrastructure defined

When focusing on infrastructure as an alternative investment, it is important to first define what infrastructure actually is. One way to think of it is that infrastructure is the essential underpinning of modern industrial societies: all the core physical structures that allow us to function and enjoy modern life. Examples of such modern physical structures are transportation (roads, bridges, railroads etc.), energy infrastructure (energy transmission lines and pipelines), telecom infrastructure (cell phone towers) etc.: the things that allow all commerce to occur across the globe.

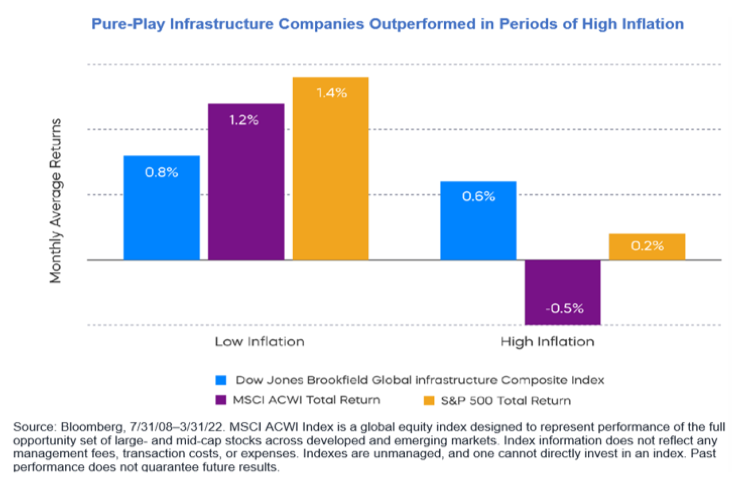

These core assets to modern life are staples for society and you don’t see demand vary much with the economic cycle. This lends to a few key attractive characteristics that makes infrastructure good to look at from an investment perspective.

So why Infrastructure?

One of the aspects that makes Infrastructure a good hedge or offset to the cost of inflation is the nature of the underlying business. These businesses are often supported by long-term contracts with governments, municipalities, or cities. This could lead to relatively steady cash flow with a potential yield component. Another important aspect to consider is that the high barrier to entry in the marketplace which does not encourage competition to emerge easily (mostly monopolistic businesses).

In a lot of the cases, contracts are linked to inflation or the operators have the ability to pass on the inflation to the end consumers. Because of the nature of the services being provided, people aren’t going stop paying the costs associated with services and products. You can rely on income being generated. So essentially, there is baked-in inflation protection.

According to a recent report from CNBC, Ethereum has just completed its “final dress rehearsal” for the so-called Merge, which will shift the second-largest cryptocurrency by market value from a “proof of work” validation protocol to “proof of stake.” As CNBC notes, this upgrade has been years in the making and is considered “one of the most important events in the history of crypto.”

The reason is simple: efficiency. Moving to “proof of stake” will reduce Ethereum’s carbon footprint over 99.5% per its internal estimates, and also significantly lower its “gas” prices, i.e. the cost of transactions. Carbon emissions and the cost of converting crypto to fiat currencies (or other crypto currencies) are the two major criticisms of Ethereum, in particular, and crypto, in general.

Network will be more secure and less prone to manipulation

The Merge is not only important to the investing public, however; it’s a critical upgrade for the crypto community. The Ethereum network will now be more secure and less prone to manipulation. For example, anyone who wants to take over 51% of the network will now need to hold half of the total staked amount in ETH, rather than 51% of the mining hash power, as was the case previously. What this means is that the platform is guaranteed to be controlled by those who have a long-term interest in its success, ergo the term “proof of stake.”

But it’s the lower “gas fees” that will probably attract the most attention: and have the most profound effect on adoption. As the cost to process any transaction on the Ethereum blockchain goes down, more adoption will occur, meaning more people will be more open to participate in Ethereum blockchain projects. Think of how stock trading took off in the 1980s after US markets were deregulated and the world’s first discount stockbroker, Charles Schwab, opened for business. More recently, Robinhood spurred another surge in trading by reducing the cost of stock transactions to zero. This is commonly referred to as the “democratization” of investing. With the Merge, a similar revolution is coming to crypto. Continue Reading…

Many people feel you need to save a bundle for retirement, and that can be true, depending how much you intend to spend. So, can you retire with a $500,000 RRSP? Can you retire without any company pension plan?

Read on to learn more, including how in our latest case study we tell you it’s absolutely possible to retire with no company pension while relying on your personal savings.

Financial independence facts to remember

You may recall from previous case studies on our site while achieving financial independence (FI) is desired by many it may not be possible for most to achieve.

Realizing FI takes a plan, some multi-year discipline, and ideally one or both of the following:

For every additional dollar you save, you can invest that money so it can grow your wealth faster, and/or,

You can realize financial independence by consuming less.

Here at Cashflows & Portfolios, we suggest you optimize both options above: if you can.

Check out these previous, detailed case studies, to see if you fall into any of these retirement dreams:

Check out how Michelle, a 20-something software engineer, plans to retire by age 40, including how much she’ll need to save to accomplish that goal.

Members of our site have already learned the powerful math behind any retirement plan:

The more you save, the faster you are likely to achieve your goal.

However, life is not a straight line. Everyone has a unique path to retirement. Twists and turns abound. Depending on the path you took in life, including what decisions you made, your retirement planning work could be vastly different than anyone else’s.

Can you retire with a $500,000 RRSP?

Not every person has a high savings rate. In fact, most don’t.

Not every person has a company pension plan to rely on either. In fact, increasingly, many don’t!

Our case study participant today was unable to have a high, sustained savings rate and he didn’t have any company pension plan to buy into either. Is he doomed for retirement? Will $500,000 saved inside his RRSPs in his 60s be enough (in addition to $100,000 in his TFSA)?

Let’s look at his case study.

In our profile today, is Tom.

Tom is aged 63 and wonders if he can retire with $500,000 invested inside his RRSP and $100,000 in his TFSA. Here are some snippets from his email to us:

Hi there,

I was hoping you can help since I know you perform some financial projections for clients … I was just wondering if you have any articles or would you know the answer to this question. I’m a single guy with a simple life. Let’s say I have only my RRSP (for the most part) to rely on for retirement beyond government benefits. I have almost $500,000 invested there. I have no non-registered account although my TFSA is maxed and now worth $100,0000. (I don’t want to use my TFSA for retirement spending right now, I consider it a big safety net as I get older so maybe you can help me run some math?) Anyhow, I am wondering if I could start taking money from my RRSP, and retire soon. Any money I don’t need for retirement, I would move in-kind into my TFSA. (I know from reading your site I cannot make a direct transfer from my RRSP to TFSA – thanks guys but I will take any excess cash I don’t spend and likely move it there. We’ll see.) I have very modest spending needs. I have no debt. I own my home in rural, small town Ontario.

What do you think?

I make decent money now, definitely not $100,000 per year but “enough” to meet my needs and to continue to invest inside my RRSP and TFSA for the next couple of years.

Do I have enough to retire and spend about $3,000 per month well into my 80s and 90s?

Thanks very much!

Thank you Tom!

To help Tom out in the future, we shared some low-cost investment ideas for his TFSA and RRSP:

Like many Canadians, early in my investing career, I was investing in high fee mutual funds and the high fees were eating into my returns. I started dabbling in DIY investing but I didn’t get very serious about it until around 2010.

When it comes to DIY investing, I would group DIY investors into two categories. Investors in the first category are people that rely completely on low cost index ETFs. They purchase ETFs on their own and re-balance them regularly. In the past few years, the emergence of all-in-one ETFs like VGRO and XGRO and all-equity ETFs like VEQT and XEQT have significantly simplified the investing process for these investors.

DIY investors in the second category are people that invest in individual stocks and possibly index ETFs as well. These investors study and research individual stocks and make the requisite buying and selling decisions.

As you’d expect, we fall in the second category. We manage our own portfolio and invest in both index ETFs and individual stocks. We have adopted this approach because we want to be more involved with our money and have more control over it. I also enjoy learning about investment-related topics and how to analyze stocks.

I will admit that I have made A LOT of investment mistakes throughout the years. However, investing mistakes are inevitable. The important thing is that we learn from them. That is the absolutely crucial thing as we all make mistakes; it is the learning from those mistakes that distinguishes the good/great investor from the mediocre/poor one.

So, I thought I’d share my learning from my investment mistakes and hopefully help readers to avoid the same mistakes.

Here are some investment mistakes I have made since I started managing our investment portfolio. They are not specific to only dividend growth stock investing.

Note: These mistakes aren’t in any particular order.

Mistake #1: Not doing proper research

When we first started with dividend investing, I knew very little about how to analyze dividend growth stocks. Like many new dividend investors, I was very much focused on only one metric – high yield. I was not paying any attention to other key metrics like payout ratio, dividend streak, or dividend growth rate. I certainly wasn’t keeping a dividend scorecard.

I stumbled onto a high yield dividend stock called Liquor Store in 2012. At first, I was overjoyed to find a dividend stock in the alcohol industry. Without doing my own research, I assumed that Liquor Store owned and operated all the liquor stores in Canada. I bought $1,500 worth of Liquor Store thinking I had hit the jackpot.

The first couple of years, I was really happy collecting dividends but the share price stayed flat. Upon further research, I learned that I was deeply mistaken. Unlike what I initially assumed, Liquor Store operated privately owned stores. The company operated 230 retail liquor stores in Canada and the US. In other words, the company was competing against Crown-owned liquor stores.

The business certainly wasn’t as rosy as I originally anticipated. The stock price then took a beating when BC introduced legislation to allow licensed grocery stores to sell BC wine.

Due to the deteriorating business environment, Liquor Store cut its dividend in 2016 and we exited this position shortly after, taking around 50% loss, not counting dividends collected.

Although I was deploying the be an owner strategy, I didn’t do my due diligence and learn more about the company. I failed to understand that the company was operating privately owned stores. I also failed to realize the Liquor Store only had a small fraction of the market share and was competing against Crown-owned liquor stores in Canadian provinces.

The biggest mistake? I foolishly assumed that since people would regularly buy alcohol, therefore the company would always be highly profitable, and the dividends would be safe.

I was simply too naive.

What did I learn from this mistake? I learned to always do research about the company regardless of whether I know the company very well or not. Never assume that I know something and never let my ego take over. At a minimum, learn about the company by going over investor presentations that most companies have under their investor relations. It is also important to go over quarterly and annual reports or consult websites such as Morningstar, Yahoo Finance, Marketbeat, Digrin, Seeking Alpha, Simply Wall St, etc.

In case you’re wondering, Liquor Store eventually was de-listed. It is now part of Alcanna (CLIQ.TO).

Mistake #2: Being greedy, not following my own rules

When I graduated in 2006 and entered the workforce, my company’s stock was trading around $15 per share. After my three-month probation period, I enrolled myself in the share purchase program and purchased company stocks with a portion of my pay-cheque every two weeks (the company matched 15% of my contribution).

The stock price went up to $22 in 2007 but I decided to keep my shares instead of selling them.

Then the financial crisis happened and the company stock went down the drain. My company stopped the share purchase program and I owned a few hundred shares at a cost basis in the low teens.

Early in 2009, the company stock went all the way down to just below $4 a share. It sat around that price for a few months. Being young and with some money saved up, I decided to purchase 300 shares at $3.93. I then purchased a few hundred shares more as the stock price climbed its way up to around $10.

Altogether, I owned less than 2,000 of my company shares. Knowing that the company was not profitable at the time and that I could be easily replaced in a blink of an eye, I decided that it was not a good idea to put all my money in one basket, so I invested my money elsewhere (i.e. high fee mutual funds).

My company turned itself around in 2012 and the stock price started climbing. At one point, I told myself that I’d sell everything when the stock hit $20.

Throughout 2013, the stock price kept climbing, reaching a high of $25. The company was firing on all cylinders – we had won many multi-million deals with key customers and we were gaining market shares. I sold a few hundred shares to take in some profit. But I was not satisfied. I believed that the stock price would keep climbing.

I was being greedy and wanted to make more money.

So I kept most of my shares.

The stock price continued to climb. First, it was $30 per share. I told myself I’d wait for a little bit longer and sell when the price hit $35.

The stock price hit $35. Once again, I told myself I’d wait for $40.

Then the stock price hit $40 and I told myself I’d wait for $45 before selling everything.

The stock price went higher and higher. It was exhilarating. Everyone in the company was excited and happy about the stock price.

In early 2015, the stock price hit a high of just below $55. I thought about selling all my shares at the time but decided to reset my selling target to $60.

I was crunching numbers and imagining how much money I’d profit if I sold all my shares at $60.

But the stock price never got anywhere close to $60. In about three months’ time, the share price quickly tumbled from a high of around $55 to just below $20.

I was kicking myself for not selling my shares at higher prices. A year later the stock price eventually climbed back up. Seeing that I missed the boat the first time and didn’t want to miss my chance again, I sold a few hundred shares at a time as the stock price climbed its way up to $35.

What lesson did I learn? First of all, I was being too greedy and wanted to sell things at a high point. But I couldn’t have predicted where the top was so I completely missed it. Although it’s fine to increase my selling target incrementally, what I should have done was to sell some shares along the way and take in profits while the stock price was going up, instead of just holding onto all the shares and keeping increasing my selling target price.

Investing has a lot to do with being patient, setting and executing strategies as flawlessly as possible, and not letting your ego get in the way. In this instance, I totally got my ego in the way. I needed to learn to have an exit plan and execute this exit plan according to it, rather than continuously deviating from it.

Mistake #3: Not thinking long term

I purchased a number of Google shares in October 2012, a few days after Google announced a terrible quarterly result and the stock price went for a slide. At around $340 a share, I thought the per-share price was high but when I looked at the PE ratio and how much cash Google had, I thought I purchased Google shares at a discount (remember, you can’t just look at the stock price alone and claim it’s expensive).

I’ve always wanted to own Google shares, ever since I started using Google for internet searches in the late 1990s. I was amazed at how good and efficient Google was compared to other search engines like Yahoo, Altavista, and Excite (remember them?). As a teenager, I was convinced that Google would be extremely profitable. In the early 2000s, on several occasions, I told my dad to invest in Google if the company was to go public. Continue Reading…

Is it just me, or do investors have a knack for overcomplicating things?

Take the argument about active versus passive investing. We’ve known for more than 30 years that, after costs, the return on the average passively managed dollar must beat the return on the average actively managed dollar. Nobel laureate William Sharpe demonstrated this for us in his 1991 article, “The Arithmetic of Active Management,” and nothing has changed since then.

Despite that scary word, “arithmetic,” you don’t need to be a math major to accept Sharpe’s conclusions and invest accordingly. Still, you may want to see for yourself what he’s talking about. In the first episode of our Index and Chill video/blog series, we’ll show you why active investors (as a group) are destined to underperform passive investors.

Dividing and Conquering the Canadian Stock Market

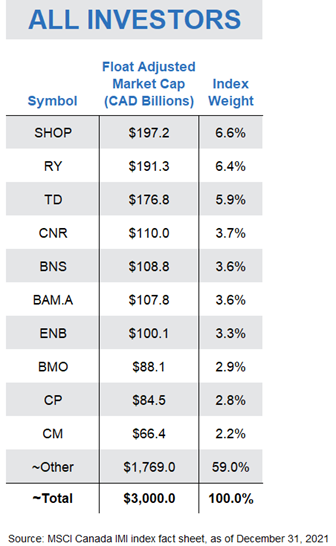

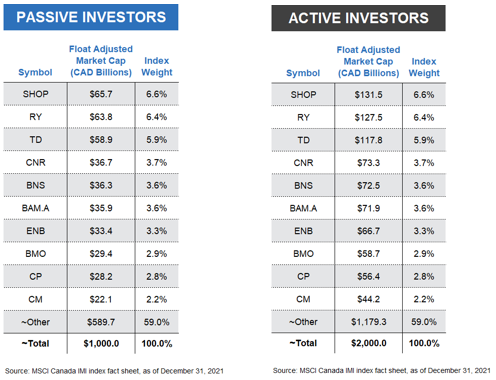

To demonstrate how Sharpe’s theory plays out in action, let’s illustrate his work using the Canadian stock market as our example. The Canadian stock market is made up of hundreds of companies, with a total value of around 3 trillion dollars. If we sort these 300 or so companies from largest to smallest based on the value of their shares available to regular investors, we find familiar names at the top of our list, including Shopify, Enbridge, and the Big Five banks.

Dividing each company’s value by the total value of the Canadian stock market provides us with a percentage weight for each, otherwise known as its “index weight.” For example, at the end of 2021, Shopify had the largest index weight, at around 6.6%, followed by RBC and TD, which made up 6.4% and 5.9% of the Canadian stock market, respectively. These weights guide index fund managers on how much to allocate to each company in their funds.

So, here’s where Sharpe’s work applies: At any point in time, investors as a group must hold all available shares of these companies. So, it stands to reason that, as a group, investors also collectively receive the total return of the Canadian stock market. In other words, if the Canadian stock market returns 10% this year, or around 300 billion dollars, everyone invested in the market will receive 300 billion dollars to divvy up amongst themselves.

Zero-Sum Games

Of course, some market participants will receive a higher return. But for each winner, there must be one or more losers.

This is the concept behind zero-sum game theory. The holdings of all investors in a particular market combine to form that market. So, if one investor’s dollars outperform the market over a particular period, another investor’s dollars must underperform, ensuring that the dollar-weighted return of all investors equals the return of the market.

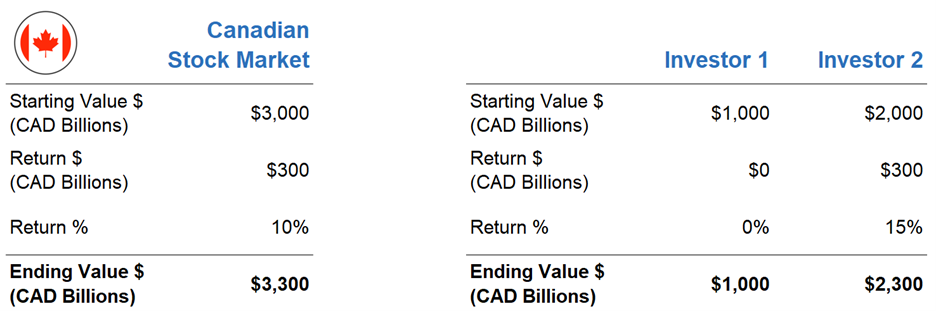

Let’s use a super-simplified example to illustrate this point. Sticking with our $3 trillion-dollar Canadian stock market, let’s assume there are only two investors in the entire market. Investor 1’s portfolio is worth 1 trillion dollars and Investor 2’s portfolio is worth 2 trillion dollars. Combined, they are the Canadian stock market.

Of course, Investor 1 and Investor 2 wouldn’t be much fun if they didn’t have different opinions about which stocks were going to outperform over the next year. Based on their preferences, they trade with each other until they are both relatively happy with their portfolio.

Over the next year, let’s say the Canadian stock market returns 10%, providing a total dollar return of 300 billion to our two investors. But Investor 1’s stock picks end up returning 0%, while Investor 2’s portfolio earns an impressive 15%, or 300 billion dollars. Investor 2 was able to earn an additional 100 billion dollars by “winning” this amount from unlucky Investor 1. But again, as a group, there was no way the pair could earn more than 300 billion dollars. In a zero-sum game, the winner’s gain comes at the expense of the loser’s loss, with zero “extra” money floating around unaccounted for.

Setting the Stage: Active vs. Passive Participation

Now, let’s look at how this zero-sum game stuff applies to active versus passive investing.

To illustrate, we’ll return to our $3 trillion Canadian stock market, and each company’s weighting within the total market.

But instead of imagining Canada’s total market is divided between two active investors, let’s establish a slightly more realistic model. We’ll assume passive investors as a group hold one-third, or $1 trillion of all Canadian company shares, and active investors as a group hold the remaining two-thirds, or $2 trillion. We’ll once again assume the overall Canadian stock market returns 10% this year, but with one critical caveat. That 10% is before costs. As we know, extra investment costs can add up quickly from management fees, bid-ask spreads, commissions, and other tricks of the trade.

I want to also point out that the particular split between passive vs. active makes no difference to our exercise. Since these passive and active investors as a group are the total Canadian stock market, and since the passive group’s holdings have the same percentage weights as the overall market, the active group’s holdings must also have the exact same percentage weights. In other words, however you slice it up, the pie is the pie, with the same ratio of ingredients in the mix.

Passive Pursuits

Let’s now look at how our passive investors would have fared with their $1 trillion market share. With these assumptions, if the market returned 10%, the passive investor group would be expected to earn $100 billion, before costs.

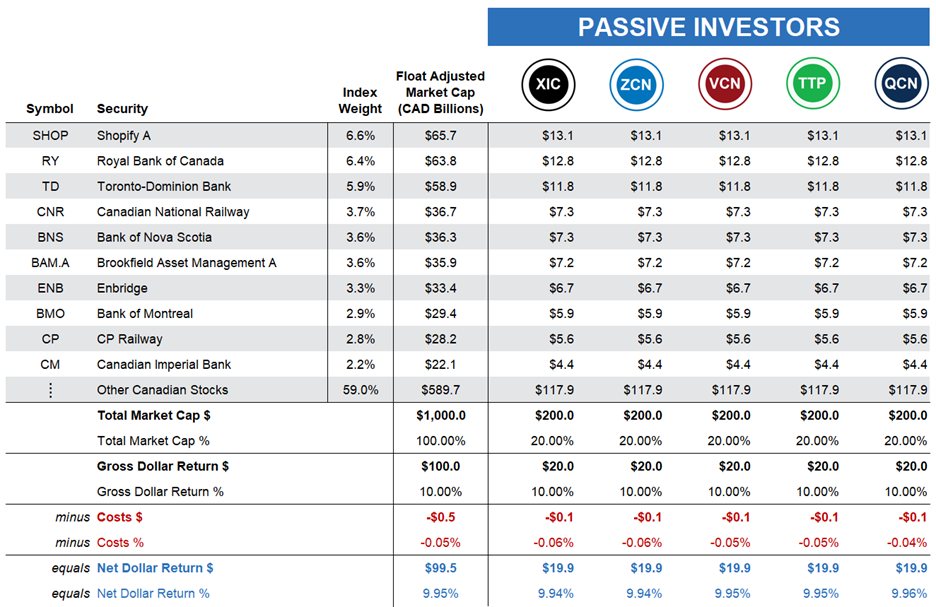

Now, suppose you are one of five passive investors in the Canadian market, with about $200 billion to invest — or one-fifth of the passive investors’ $1 trillion market share.

You don’t have a fancy business degree, and you’ve never even glanced at a company’s financial statements. You’d rather just buy and hold a low-cost index fund or ETF that tracks the broad Canadian stock market, so you invest your $200 billion in the iShares Core S&P/TSX Capped Composite Index ETF (XIC). XIC’s fund managers would use your money to purchase hundreds of Canadian stocks on your behalf, each according to its weight in the index. For example, they would purchase $12.8 billion of Royal Bank stock, or 6.4% of your $200 billion … and so on.

A year goes by, and in our illustration, you receive the stock market return of 10%, before costs. That’s $20 billion on your $200 billion investment. And because passive investing costs are low, your after-fee return will be around 9.94%, or just slightly less than the market return.

Your four fellow passive investors choose comparable broad-market Canadian equity ETFs that deliver similar after-cost returns. So, on average, the passive group earns around 9.95% after costs.

Active Adventures

Next, let’s turn to our active investors, who continue to hope or believe they can beat the market, even after costs. We’ll again assume there are only five investors in our active management group, and they all have the same $400 billion each to invest.

However, unlike our passive camp, our active investors do not all share a similar approach to investing; each will pursue a different tactic.

Our first active investor selects a portfolio of funds recommended by their favorite banker who is a so-called “closet indexer.” This banker is afraid of losing their job if their recommendations stray too far from the popular benchmarks, so their preferred funds closely follow a passive approach … but with a catch. Their fund management fees are a hefty 2.5%. As a result, our closet indexer earns the market return of 10% before fees, but their net, after-cost return shrinks to 7.5%. Continue Reading…