By Noah Solomon

Special to the Financial Independence Hub

Cycles are inevitable. They have persisted since markets have existed and will endure for as long as humans engage in the pursuit of profit. In prolonged up cycles, people are euphoric, bid up prices to unsustainable levels, and sow the seeds for subsequent misery. Similarly, severe price declines result in unsustainably pessimistic sentiment, pushing prices down to bargain levels, thereby sowing the seeds of the next up cycle.

Neither bull nor bear markets continue indefinitely. Despite this incontrovertible truth, every time an up or down cycle persists for an extended period and/or to a great extreme, the “this time it’s different” crowd becomes increasingly pervasive, citing changes in geopolitics, institutions, technology, and behavior that render the old rules obsolete. But then it turns out that the old rules do apply, and the cycle resumes.

The persistence of cycles is in large part the result of the inability of investors to remember the past. According to legendary economist John Kenneth Galbraith:

“Extreme brevity of financial memory…. When the same or closely similar circumstances occur again, sometime in only a few years, they are hailed by a new, often youthful, and always supremely self-confident generation as a brilliantly innovative discovery in the financial and larger economic world. There can be few fields of human endeavor in which history counts for so little as in the world of finance. Past experience, to the extent that it is part of memory at all, is dismissed as the primitive refuge of those who do not have the insight to appreciate the incredible wonders of the present.”

Will the True Driver of Market Cycles Please Stand Up?

Without a doubt, macroeconomic factors such as interest rates, inflation, fiscal policy, GDP growth, unemployment, etc. exert a significant influence on the ebb and flow of markets. However, in our view, fluctuations in psychology have the greatest impact on cycles. More than any other factor, changes in sentiment are what cause shifts between hospitable to treacherous markets, and therefore between gains and losses.

In market cycles, most excesses on the upside and the inevitable reactions to the downside (which also tend to overshoot) are the result of exaggerated swings of the pendulum of psychology. Even the father of value investing and Buffett mentor, Benjamin Graham, acknowledged the tremendous influence of psychology in his allegory about “Mr. Market.” Depending on his volatile mood swings, Mr. Market will buy assets at unrealistically high levels or sell them at bargain basement prices.

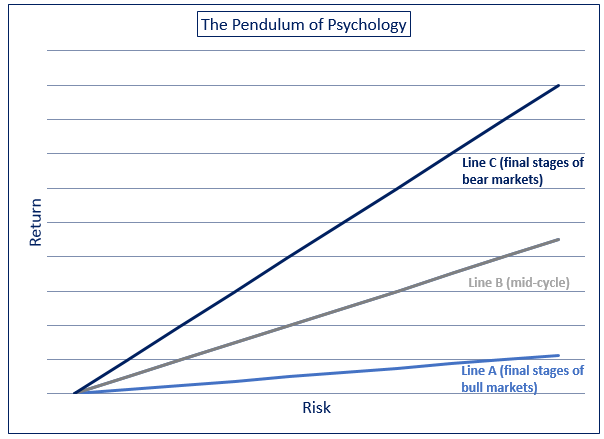

The following graph offers a succinct and accurate portrayal of investor psychology at different parts of the cycle.

In bear markets, the dominant psychology in the markets is represented by line C, where investors demand generous risk premiums to compensate them for taking risk. In these environments, valuations are undemanding, prospective returns from bearing risk are high, and chances are good you that will be rewarded for taking risk.

As the cycle progresses and markets begin to rise, the dominant psychology shifts to line B, which represents the “happy medium” where investors are neither overly pessimistic nor blindly optimistic. In such environments, people require adequate compensation for taking risk, valuations are neither depressed nor excessive, and you can expect returns that approximate the long-term historical average.

Lastly, during the latter stages of bull markets when prices have risen significantly over a period of several years, the general mindset of the investing public shifts to line A, where investors become euphoric and adopt a lopsided desire for return with little regard for risk. In such environments, people require scant compensation for bearing risk, valuations become unrealistic, and losses become more likely than gains.

In essence, the pendulum of investor psychology is heavily influenced by the recency bias of what has happened over the past several years, swinging between collecting gold bars in front of a wisp during the bad times (line C) and picking up pennies in front of a steamroller at market tops (line A).

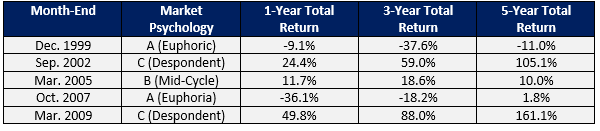

S&P 500 Index: Investor Psychology and Subsequent Returns

The table above demonstrates that the mood shifts of investors can have a dramatic impact on returns. With respect to the current environment, we are more confident about where we are not than where we are. It’s difficult to make the case that market participants are despondent and are demanding huge risk premiums for investing. In our view, market psychology is currently somewhere between lines A and B.

Except for the short lived Covid-induced swoon of early 2020, governments and central banks have been successful in maintaining the bull market that began in March 2009 after the global financial crisis. This has increased confidence in the Fed put and emboldened investors. Although nobody can know for certain whether it is possible to engineer a perpetual party by plying its attendees with ever-increasing stimulus, we wouldn’t bet the farm on it!

The Elusive Happy Medium: Average Doesn’t Mean Normal

In the real world, things generally fluctuate between “pretty good” and “not so hot.” But in the world of investing, investor psychology seems to spend much more time at the extremes (lines A and C) than it does at a “happy medium” (line B). At any given point in time, markets are more likely driven by greed or fear rather than greed and fear. Either “Risk is my friend. I need to buy before I miss out” or “I just don’t want to lose any more. Sell before it goes to zero” are far more likely to dominate markets than equanimity. Continue Reading…

By Andrew Gillies

By Andrew Gillies