By Penelope Graham, Zoocasa

By Penelope Graham, Zoocasa

Special to the Financial Independence Hub

The anniversary of the implementation of the Ontario Fair Housing Plan has come and gone, and the playing field is just starting to even in the province’s housing market. Designed to cool demand and price growth in the Greater Golden Horseshoe, the 16-part package of housing regulations has effectively done just that, with sales down double-digit percentages throughout the region, and prices softening for the most expensive housing types.

Housing analysts argue that this result is mainly due to psychological factors, rather than the new regulations – which include a foreign buyer’s tax, and overarching rent controls – themselves.

But what do Ontarians really think about the new regulations? To find out, Zoocasa conducted a survey of 1,400 respondents on their sentiments around the highlights of the plan, and whether they support the government’s intervention in the free housing market.

Following BC’s footsteps

If Ontario’s attempt to tax foreign purchasers of real estate seems familiar, that’s because it closely resembles what occurred in British Columbia; the province initially implemented a 15-per-cent levy on foreign buyers within the Metro Vancouver area in August 2016, before upping the tax to a full 20 per cent, and extending the affected geographical area, in February of this year.

While Ontario’s version, called the Non-Resident Speculation Tax (NRST) still taxes just 15 per cent of a home’s purchase price, it will apply to anyone buying a home within the GGH – including homes for sale in Hamilton, or condos for sale in Mississauga, who is not a Canadian citizen or permanent resident (those who obtain such status, or who are enrolled in a minimum two-year full-time post-secondary program within a year of their home purchase are eligible for a full rebate on the NRST).

At the time of its implementation, former Ontario premier Kathleen Wynne was adamant that the tax was not intended to discourage newcomers to Canada from settling in Ontario.

“The Non-Resident Speculation Tax has nothing to do with new Canadians or people who want to make Ontario their home,” she stated to a media scrum on April 20, 2017. “This is targeting people who are not looking to raise a family, who are just looking for quick profit or a place to park their money.”

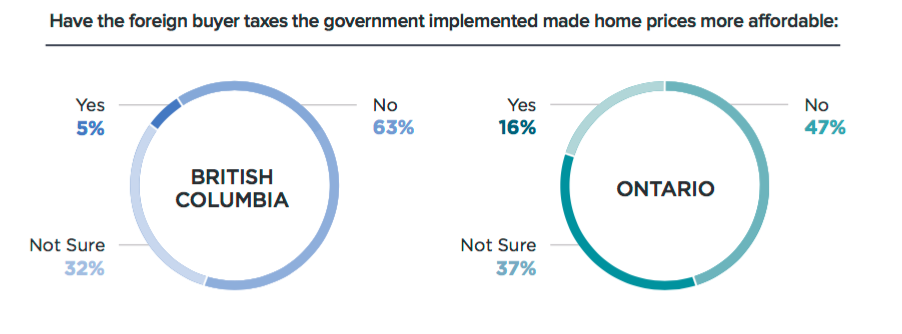

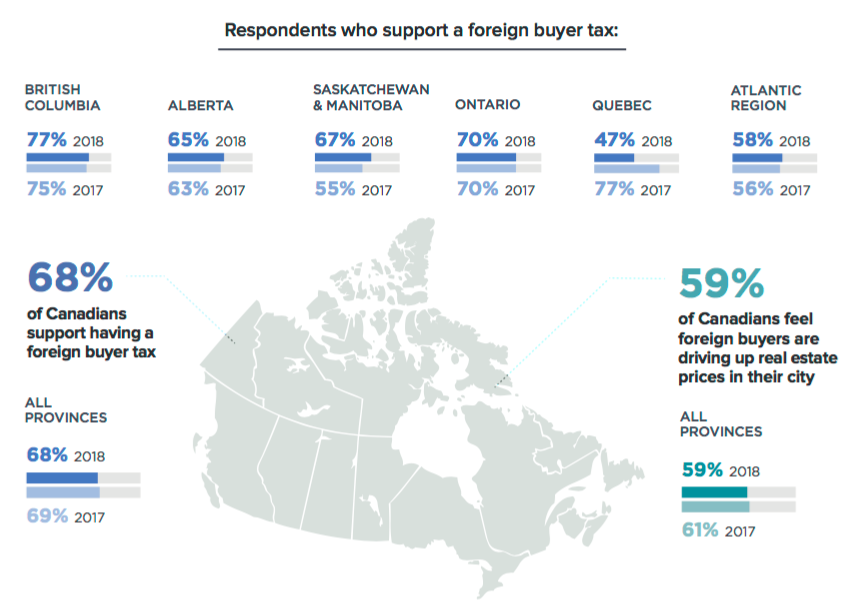

The measure appears to have resonated well with all Canadians; according to survey results, 69 per cent of respondents from all provinces indicated they support the tax, while 61 per cent felt foreign ownership directly impacts prices in the local housing market.

Perhaps not surprisingly, respondents from provinces with the most competitive real estate marketplaces were most likely to support the tax: 77 per cent of British Columbians and 70 per cent of Ontarians indicated they were pro-tax.

Support extends beyond affected Housing markets

Support extends beyond affected Housing markets

However, even respondents from provinces where foreign investment and homeownership is not considered a stressor on the market, indicated support for the tax; 65 per cent of Albertans indicated support, even though only 40 per cent feel out-of-country buyers impact housing prices in their region. Continue Reading…