By Tyler Mordy, Forstrong Global Asset Management

By Tyler Mordy, Forstrong Global Asset Management

Special to the Financial Independence Hub

An old Japanese proverb states “many a false step was made by standing still.”

So it is with currency exposures in investor portfolios. Consider the recent experience of Brazilian, Russian and even Canadian investors — to name a few countries with steeply depreciating exchange rates. By electing to remain invested in their domestic currency, they have all experienced a steep “loss” in their own global purchasing power (even if nominal values held up). An ostensibly conservative position has cost them dearly.

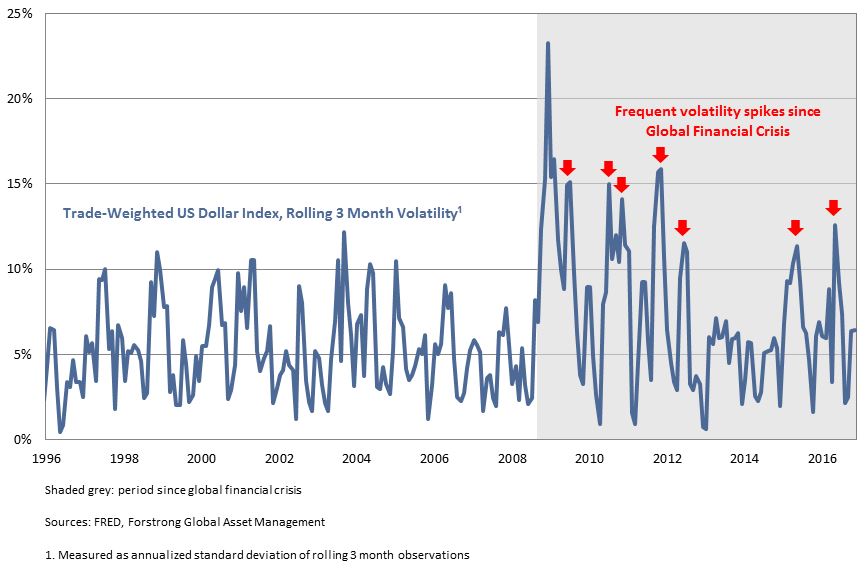

Welcome to the new, hyper-globalized world. Since the financial crisis, unorthodox policies — with central banks trying to outdo the effects of one another by plunging into a subterranean universe of quantitative easing and negative interest rates — have driven currency volatility much higher. Now, capital has a way of swiftly seeking out safe harbours and penalizing others who are not safeguarding their national currencies. Who would have thought the once-august Swiss franc would lose its safe haven status?

Indeed, currency exposures are having an outsized impact on portfolio returns. Currency-focused ETF vehicles could not have arrived at a better time, introducing yet another evolution in the portfolio management process. Today, gaining global currency exposures is as easy as buying stocks.

Beyond the academic view