Alain Guillot in Cascais, Portugal, a rich neighborhood.

By Alain Guillot

Special to Financial Independence Hub

Learning how you can turn a little bit of money into a lot of money is a great way to get your finances on the right track. After all, this can help with everything from paying off debt and credit card bills to growing your savings.

With that in mind, here are some top tips that you can use to do exactly that!

Add money to your savings immediately after getting paid

Don’t wait until the end of the month (i.e., when you have spent all your money) to think about transferring cash into your savings account. Instead, transfer a pre-designated amount of money into your savings account each payday. This way, you are reducing the chances of spending money you’d originally wanted to save!

By regularly adding to your savings account, you put yourself in the best possible position to improve your finances in the long term. When setting up a savings account, make sure you choose one with a great interest rate!

Start investing

Whether you’re going to buy and sell Cyrpto currency or going down a more traditional investment pathway, investing money is a great way to turn a little cash into a lot of cash. This can also be a great way to earn passive income, as a lot of the work is out of your hands once you’ve made the initial investment.

Of course, you should make sure to do plenty of research ahead of time so that you are protecting your best interests as much as possible. Remember, while no investments are risk-free, some are more stable than others, and you should not invest money you cannot afford to lose.

Turn your hobby into a side-hustle

Turning your hobby into a side hustle can also help you to turn your finances around, and could even become a real money-maker over time. While it may not seem that way to begin with, you can monetise just about every hobby. Whether you’re a painter or a writer, you simply need to be willing to put the work in to refine your craft and get your name out there. Continue Reading…

If you’ve ever felt nervous about the stock market ups and downs, you’re not alone. Most investors want their money to grow steadily without the wild swings: especially if you’re thinking about retirement. Lately, worries about an AI bubble and changing interest rates have shown just how quickly things can get unpredictable.

That’s why building the right portfolio is important to help you stay calm and stay invested, even when markets get a little rocky.

Low-volatility investing, and specifically using funds such as BMO Low Volatility Canadian Equity ETF (ZLB) and BMO Low Volatility US Equity ETF (ZLU), are designed to give you a smoother experience. These strategies help you stay invested with confidence no matter what the markets are doing.

What does Low Volatility mean for your Investments?

Imagine low-volatility investing as playing it smart in baseball: not trying for risky home runs, but focusing on steady singles and doubles. This way, you keep making progress, scoring runs over time, and avoiding big losses. It’s all about reliable growth, not wild swings that could set you back.

ZLB and ZLU are designed to help your investments stay on track, even when markets get unpredictable. They pick companies that don’t jump around as much as the overall market: think of them as the steady players on the team. By steering clear of those big ups and downs, your money can grow more smoothly, and you can benefit from compounding over time.

Building a Smoother Ride with Low volatility

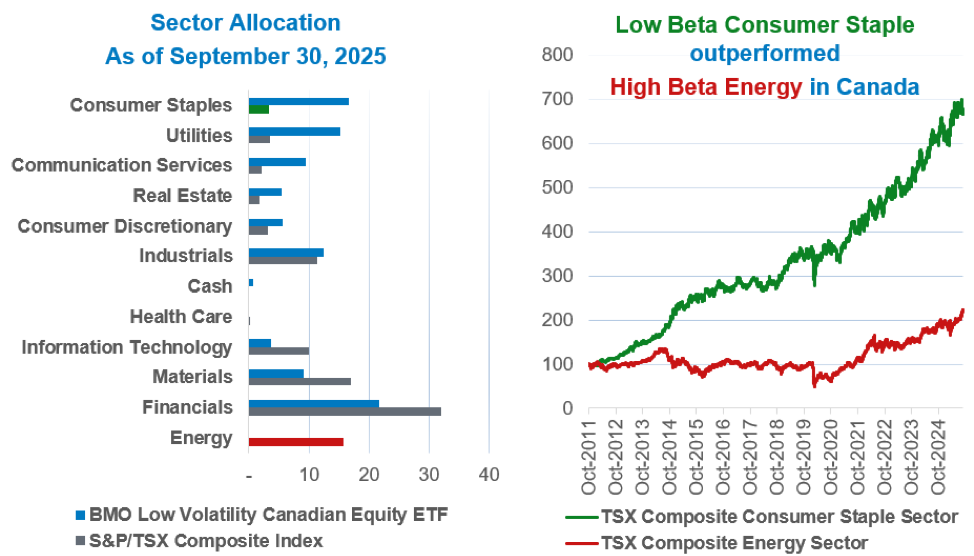

ZLB and ZLU focus on defensive sectors like utilities, consumer staples, and healthcare. These ETFs can act as financial shock absorbers, reducing risk from market swings and limiting exposure to more volatile sectors like technology. Position and sector caps further protect against over-concentration, while the selection of low-beta1 companies means the portfolio is designed to cushion losses during downturns.

The disciplined construction of ZLB and ZLU helps you stay on course regardless of market conditions. This approach isn’t about chasing the latest trends but about building steady, long-term growth through stability and diversification, letting compounding work its magic over time.

Low volatility cushioned the blow with stability

Chart 1

Note: Data as of September 30, 2025. Source: BMO AM Inc. Bloomberg Sector allocation subject to change without notice. Chart compares sector allocations of BMO Low Volatility Canadian Equity ETF and S&P/TSX Composite Index as of September 30, 2025, and shows Consumer Staples outperforming Energy in Canada from 2011 to 2024.

Common Myth: Low-Volatility ETFs reduce Return

Low volatility doesn’t mean you have to settle for lower returns. In fact, Canadian low-volatility investments have consistently outpaced the S&P/TSX Capped Composite Index since inception, offering strong returns while helping to reduce risk.

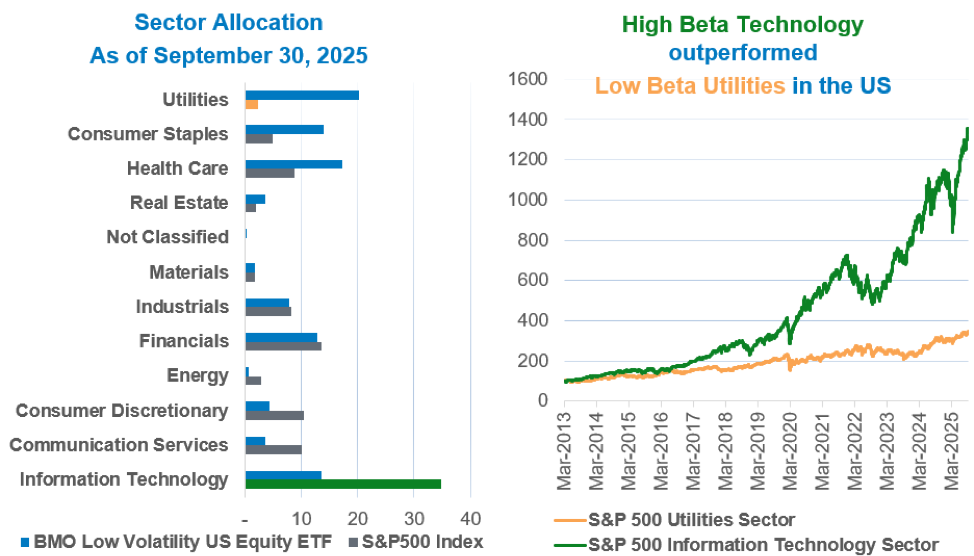

Chart 2

Note: Data as of September 30, 2025. Source: BMO AM Inc. Bloomberg Sector allocation subject to change without notice. Chart compares sector allocations of BMO Low Volatility US Equity ETF and S&P 500 Index as of September 30, 2025, and shows Technology outperforming Utilities from 2013 to 2025.

The U.S. market is highly concentrated in the Magnificent 72 and generally information. Because ZLU invests more in stable sectors like utilities and healthcare, it provides steady, long-term returns, though it might not keep up with the S&P 500 when the market is booming, as it has more recently with the growth dominated in the Tech sector. Even with this more cautious approach, ZLU still delivers strong annual returns for investors by emphasizing stability and value rather than jumping into the latest tech trends.

Balanced Growth, Less Stress: Blending ETFs for Smoother Returns

If you want steady growth for your portfolio without taking on too much risk, you may not have to choose between safety and strong returns. By combining BMO Low Volatility US Equity ETF (ZLU) with BMO NASDAQ 100 Equity Index ETF (ZNQ), you can get the best of both worlds: reliable stability and exciting growth. This mix has delivered higher returns and lower risk than simply investing in BMO S&P 500 Index ETF ( ZSP) as shown in Chart 3. Continue Reading…

Canada is about to experience an unprecedented transfer of wealth across generations that will transform household balance sheets, life plans, and the role of financial advisors. Experts estimate that roughly $1 trillion will transfer between generations over the next decade, and this shift is discussed weekly.

As someone who advises families across multiple generations, I see three key implications. First, the amount of capital shifting hands is significant, but equally important are the who and the how: younger recipients seek different things than their parents. Second, the timing and structure of transfers (gifts made during life versus testamentary bequests) are driven by family dynamics as much as tax considerations. Third, the industry itself must modernize to stay relevant: advice now goes beyond portfolio selection to include income architecture, behavioral coaching, private-market access, values alignment, and digital delivery. The landscape is changing more quickly than I have experienced in the past 25 years.

Understanding what each generation needs and why they want it is the foundation for giving meaningful advice.

Baby Boomers: stewardship, income, and legacy

Baby Boomers still hold a disproportionate share of wealth in Canada, and their priorities have shifted from accumulation to preservation, predictable income, and legacy planning. The questions they ask are practical and existential: Will I outlive my money? How do I leave a legacy without causing family conflicts? How do taxes and health-care risks affect my plan? In practice, this means structuring retirement income to address longevity risk, incorporating tax-efficient solutions, and creating estate plans that minimize friction at death.

At Trans Canada Wealth, an advisory group of Harbourfront Wealth’s independent platform, we integrate investment strategies with our in-house CPA tax specialist and estate planning expertise so clients can see the full chain of outcomes, cash flow, taxes, and transfer, rather than isolated portfolio returns. This comprehensive approach is what gives Boomers the peace of mind they value most. We walk clients through our “Atlas” system to ensure they have peace of mind that no stone has been left unturned and that they have a structure and plan that works for their unique situation.

Gen X: the bridge generation demanding clarity

Generation X is in the middle, often financially squeezed, supporting aging parents while raising children, yet they are likely to be the most active people in managing wealth transfers. Many Gen X clients will inherit significant wealth but usually don’t plan for it; instead, they seek control, transparency, and practical plans that address debt today, catch up on retirement savings, and fund education. Unlike parents of previous generations, they have a stronger desire to help their children buy their first home and ensure they start their financial journey on solid footing.

An important role for advisors is facilitation: helping families have clear conversations about intentions and timing. We frequently counsel Boomers on the merits of lifetime gifts versus estate transfers because earlier transfers can increase intergenerational utility and allow parents to witness the benefits. Equally, Gen X wants straightforward, independent advice that filters noise, ensuring one poor decision doesn’t derail a 20- or 30-year plan.

Millennials: aligning performance with purpose

Millennials prioritize differently when they invest. While performance remains important, purpose and fees are now key factors. Studies and industry reports reveal that younger investors are highly interested in sustainable and impact strategies; they seek access to alternative investments and ESG-informed allocations as part of a diversified portfolio.

For advisors, this means providing institutional-grade access and clear discussions about costs alongside values-based solutions. Millennials are well-informed but have limited time; they expect advisors to add value by curating investment opportunities, conducting thorough due diligence, and explaining trade-offs: such as how an ESG focus might affect risk/return, liquidity, and fees. When advisors excel at this, they not only retain inherited capital but also build lifelong relationships.

Gen Z: digital-first, early adopters and learners

Gen Z approaches wealth conversations with a different relationship to money. They are digital natives, comfortable transacting and learning online, and many start their investing journey earlier than previous generations. Research shows a significant rise in early retail investing and financial literacy among Gen Z, and their expectations for digital access, education, and transparency are high. Continue Reading…

It’s that time of year again. Holiday shoppers know the secret: start with a meaningful primary gift that makes an impression. Add smaller delights for a personal touch. Asset allocators can do the same: anchor portfolios with a broad emerging market (EM) core and use dynamic tilts1 for the perfect stocking stuffers.

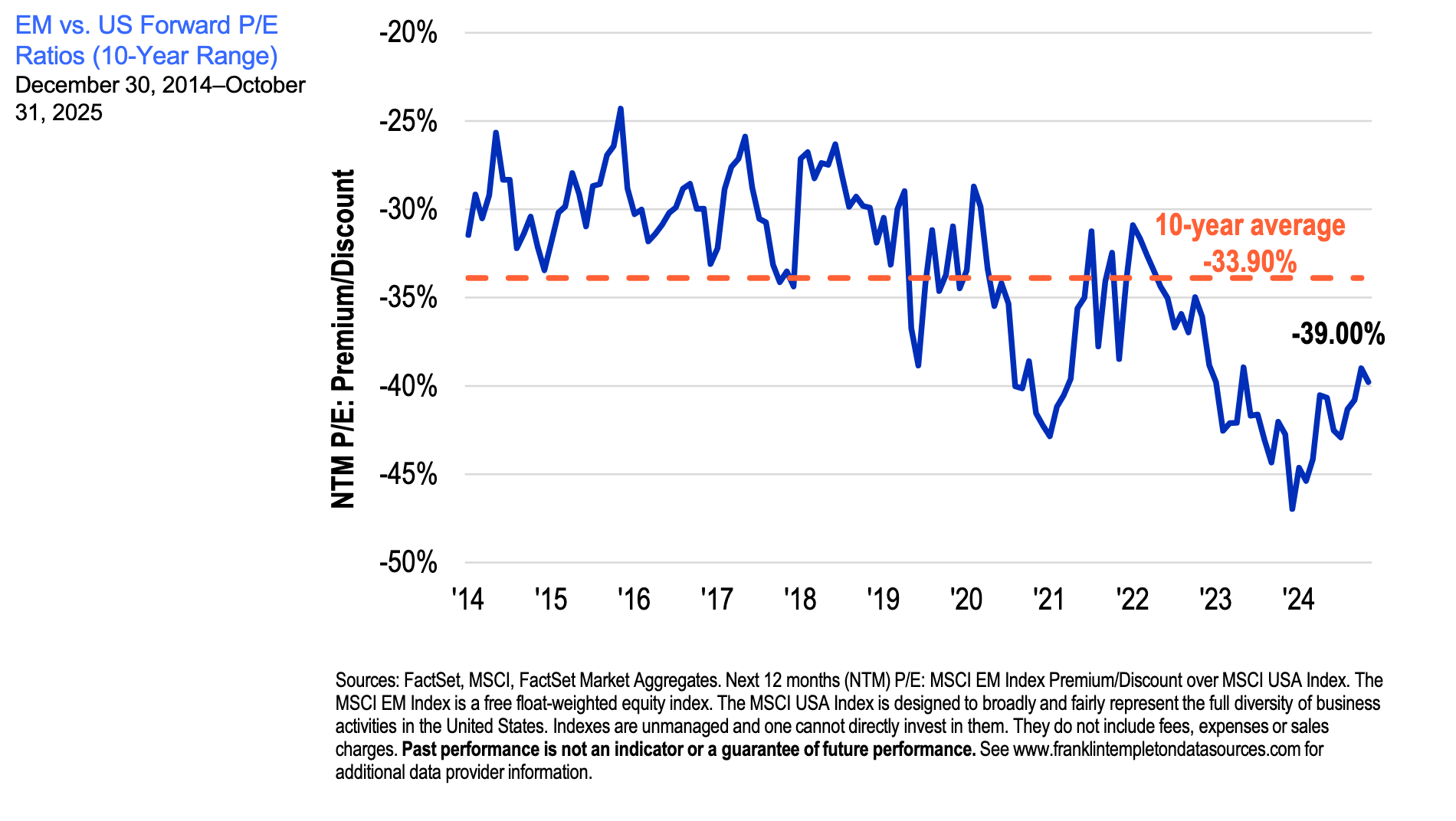

The broad EM equity rally has now entered a more structurally supportive phase rather than a pure sentiment bounce. EM equities have advanced for 10 straight months, now up more than 30% year to date, outpacing U.S. large caps, which returned slightly less than half that over the same period.2 We believe this outperformance is likely to continue through year‑end amid a weaker US dollar, improving earnings and growing demand for geographic diversification.

Valuation gaps remain wide: EM equities recently traded at nearly a 40% discount versus US peers: one of their lowest forward price-to-earnings (P/E) differentials in over a decade. Meanwhile, early macro indicators suggest modest expansion among EM manufacturing sectors.

Adding to this tailwind, the recent decline in the US dollar is easing financial conditions across EMs. The weaker greenback makes it cheaper for EM borrowers to service dollar-denominated debt, while the Federal Reserve’s pivot toward interest-rate cuts is fueling renewed demand for local-currency bonds that still offer attractive real yields. Meanwhile, deepening trade and manufacturing linkages between the United States and Mexico underscore how supply-chain rerouting is boosting multiple EM hubs — not just one market — reinforcing the case for a broad EM core. These forces of less dollar pressure, falling US rates and stronger regional trade flows are creating what we see as a more favorable backdrop for EMs.

In terms of portfolio construction, a diversified EM allocation anchors exposure to global easing, demographic growth and digital transformation, while selective country tilts reflect conviction-driven opportunities. Such an approach helps investors look beyond short-term noise and stay invested through the macro cycle. With valuations still moderate, we believe the risk-reward for EMs broadly remains compelling.

Why broad core + dynamic tilts works now

Global supply-chain remapping triggered by tariffs has created more stark standouts and laggards across the EM universe and we believe a broad EM core can help capture the multiplicity of growth vectors, while dynamic tilts allow investors to capture standout growth pockets when dispersion widens. South Korea’s equity market, for example, has emerged as a clear leader this year, up nearly 70% year-to-date: the strongest returns for any major market globally.3 Continue Reading…

As you know, I have frequently expressed concerns about high valuations for stocks. The concern has been expressed vehemently, yet so far, no serious risk has presented itself in terms of market drawdowns.

The narrative of U.S. public markets being risky has not proven to be accurate over the past few years. That said, what was once a minority view is becoming increasingly mainstream, as valuations remain stretched. The adage of ‘markets can remain irrational for longer than you can remain solvent’ has proven to be prescient and problematic for those who raised their cash positions. It has also caused certain commentators (including myself) to feel like Chicken Little. Despite our breathless admonitions, the sky has not fallen: yet.

Reallocate to more reasonably priced Asset Classes

Some people chose to exit public securities, but not capital markets. Private assets where there are likely to be pockets of more realistic valuation, as well as traditional inflation hedges like infrastructure and gold, have all performed relatively well in 2025. Rather than engage in market timing, this approach is more akin to an active reallocation toward being fully invested in asset classes that are more reasonably priced.