My latest MoneySense Retired Money column looks at one unexpected upside of inflation; the government’s indexing to inflation of tax brackets, retirement savings limits and OAS thresholds. You can find the full column by clicking on the link here: Inflation a scourge for retirees? Ottawa’s silver lining(s)

TFSA room rises to $7,000

Fans of the popular Tax-free Savings Account (TFSA) will experience this as early as Jan. 1, 2024, when the annual maximum contribution room rises to $7,000, up from $6,500 in 2023. As of January 2024, someone who has never before contributed to a TFSA now has cumulative contribution room of $95,000.

In November Kyle Prevost’s weekly Making Sense of the Markets column included an item titled Make inflation work for you. “We shouldn’t ignore or discount the more advantageous aspects of inflation, such as increased government benefits and more contribution room in our RRSPs and TFSAs.”

Prevost linked to a spreadsheet posted on X (formerly Twitter) by financial advisor Aaron Hector, posted late in October, after the CPI announcement that Ottawa’s official inflation indexing rate for 2024 would be a sizeable 4.7%. While below 2023’s 6.3% indexation rate, it’s well above 2022’s 2.4% and 2021’s 1%.

Also quoted in the MoneySense column is Matthew Ardrey, wealth advisor with Toronto-based TriDelta Financial. “One of the main benefits is paying less taxes.” Income tax brackets increase with inflation each year. For example, in 2021 the lowest tax bracket in Ontario ended at $45,142 of income. “Starting in 2024, this lowest tax bracket now ends at $51,446. This is a 14% increase over just a few years.” Continue Reading…

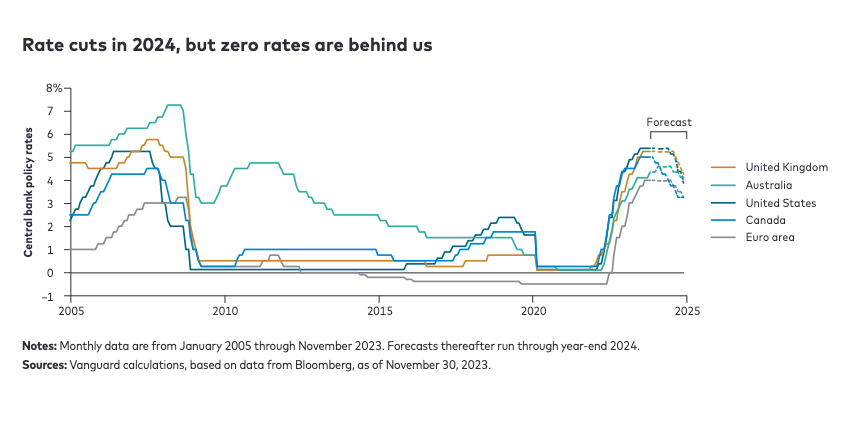

Higher interest rates are here to stay, according to the Vanguard Economic and Market Outlook for 2024, delivered online on Tuesday, Dec. 12. The following is an advance document viewed under embargo and it has been edited down from a Global Summary prepared by Vanguard Global Chief Economist Joseph Davis and the Vanguard global economics team. Anything below in quotes is directly lifted from that document. Otherwise, I have used ellipses and/or paraphrased to make this fit the Hub’s normal blog format. Subheadings are also by Vanguard. At the end of this blog, we have also added a chart about Canada in particular, and projected investment returns in Canada and the rest of the world, supplied by Vanguard Canada.

The main paper begins:

Joseph Davis, Ph.D., Global Chief Economist for Vanguard Group Inc.

“Higher interest rates are here to stay. Even after policy rates recede from their cyclical peaks, in the decade ahead rates will settle at a higher level than we’ve grown accustomed to since the 2008 global financial crisis (GFC). This development ushers in a return to sound money, and the implications for the global economy and financial markets will be profound. Borrowing and savings behavior will reset, capital will be allocated more judiciously, and asset class return expectations will be recalibrated. Vanguard believes that a higher interest rate environment will serve investors well in achieving their long-term financial goals, but the transition may be bumpy.”

Monetary policy will bare its teeth in 2024

“The global economy has proven more resilient than we expected in 2023. This is partly because monetary policy has not been as restrictive as initially thought. Fundamental changes to the global economy have pushed up the neutral rate of interest — the rate at which policy is neither expansionary nor contractionary. Various other factors have blunted the normal channels of monetary policy transmission, including the U.S. fiscal impulse from debt-financed pandemic support and industrial policies, improved household and corporate balance sheets, and tight labor markets that have resulted in real wage growth.

In the U.S., our analysis suggests that these offsets almost entirely counteracted the impact of higher policy interest rates. Outside the U.S., this dynamic is less pronounced. Europe’s predominantly bank-based economy is already flirting with recession, and China’s rebound from the end of COVID-19-related shutdowns has been weaker than expected.

The U.S. exceptionalism is set to fade in 2024. We expect monetary policy to become increasingly restrictive as inflation falls and offsetting forces wane. The economy will experience a mild downturn as a result. This is necessary to finish the job of returning inflation to target. However, there are risks to this view. A “soft landing,” in which inflation returns to target without recession, remains possible, as does a recession that is further delayed.

In Europe, we expect anemic growth as restrictive monetary and fiscal policy lingers, while in China, we expect additional policy stimulus to sustain economic recovery amid increasing external and structural headwinds.”

Zero rates are yesterday’s news

“Barring an immediate 1990s-style productivity boom, a recession is likely a necessary condition to bring down the rate of inflation, through weakening demand for labor and slower wage growth. As central banks feel more confident in inflation’s path toward targets, we expect they will start to cut policy rates in the second half of 2024.

That said, we expect policy rates to settle at a higher level compared with after the GFC and during the COVID-19 pandemic. Vanguard research has found that the equilibrium level of the real interest rate, also known as r-star or r*, has increased, driven primarily by demographics, long-term productivity growth, and higher structural fiscal deficits. This higher interest rate environment will last not months, but years. It is a structural shift that will endure beyond the next business cycle and, in our view, is the single most important financial development since the GFC.”

A return to sound money

“For households and businesses, higher interest rates will limit borrowing, increase the cost of

capital, and encourage saving. For governments, higher rates will force a reassessment of fiscal

outlooks sooner rather than later. The vicious circle of rising deficits and higher interest rates

will accelerate concerns about fiscal sustainability.

Vanguard’s research suggests the window for governments to act on this is closing fast — it is

an issue that must be tackled by this generation, not the next.

For well-diversified investors, the permanence of higher real interest rates is a welcome

development. It provides a solid foundation for long-term risk-adjusted returns. However, as the

transition to higher rates is not yet complete, near-term financial market volatility is likely to

remain elevated.

Bonds are back!

Global bond markets have repriced significantly over the last two years because of the transition

to the new era of higher rates. In our view, bond valuations are now close to fair, with higher

long-term rates more aligned with secularly higher neutral rates. Meanwhile, term premia

have increased as well, driven by elevated inflation and fiscal and monetary outlook

uncertainty.

Despite the potential for near-term volatility, we believe this rise in interest rates is the single

best economic and financial development in 20 years for long-term investors. Our bond

return expectations have increased substantially. Continue Reading…

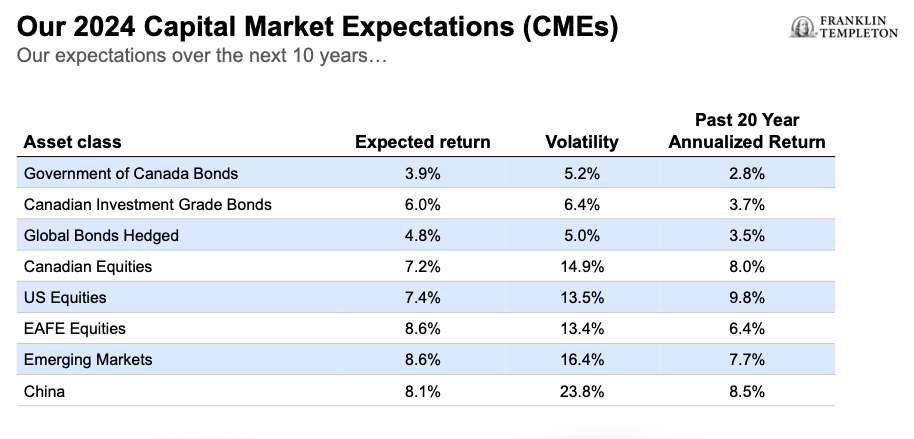

Investors can expect strong positive single-digit returns for the ten years between 2024 and 2034, portfolio managers for Franklin Templeton Investments told advisors on Thursday.

Ian Riach

Speaking at the 2024 Global Investment Outlook in Toronto, portfolio manager Ian Riach said Canadian equities will have expected returns in C$ of 7.2%, a tad below the 7.4% of U.S. equities and 8.6% for both EAFE and Emerging Markets and 8.1% for China. Riach is Senior Vice President and Portfolio Manager for Franklin Templeton Investment Solutions and CIO of Fiduciary Trust Canada.

Fixed-income returns are expected to be in the low single digits: 3.9% for Government of Canada bonds, 6% for investment-grade Canadian bonds and 4.8% for hedged global bonds, again all in C$. See above chart for the Volatility of each of these asset classes, as well as the past 20-year annualized returns for each. From my read of the chart, expected returns of North American equities the next decade are slightly below past 20-year annualized returns but EAFE and Emerging Markets expected returns are slightly higher, with the exception of China.

Fixed-income investors who were dismayed by bond returns in 2022 will no doubt be relieved to see expected future returns of Canadian bonds and global bonds are higher than in the past 20 years. “Expected returns for fixed income have become more attractive; recent volatility [is] expected to subside,” Riach said in the presentation provided to attendees.

Capital markets expectations (CME) are used to set Strategic Asset Allocation, which forms the basis of Franklin Templeton’s long-term strategic mix for portfolios and funds, the document explains: “Portfolio managers then tactically adjust.”

“This year CMEs are generally higher than last year. Primarily due to higher cash and bond yields as a starting point,” the document says.

Global equity returns are expected to revert to longer- term averages and outperform bonds, EAFE equities “look attractive,” and Emerging market equities are expected to outperform developed market equities, albeit with more volatility.

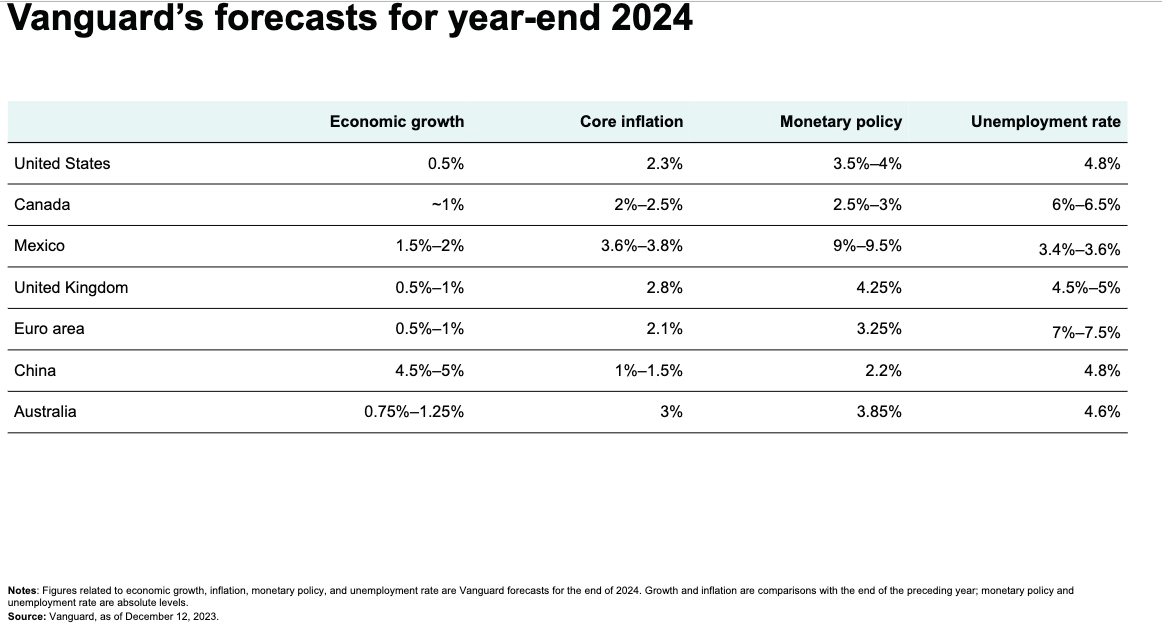

Central banks may have to tolerate higher inflation, but are determined to at least get it closer to target in the short-run. The Bank of Canada does have some room to tolerate a higher rate as its target is more flexible at 1%-3%. This compares to the Fed’s hard-wired 2%. Thus, rates in the US may stay higher for longer to bring inflation down to target

Risks of Recession

Riach described three major broad portfolio themes. The first is that Recession risks are moderating but “reasons for caution remain.” The second is that on interest rates, central banks have reached “Peak policy, but expect higher rates for longer.” The third is that “Among the risks, opportunities exist.” Addressing the narrow market of the top ten stocks in the S&P500 (the Magnificent 7 Big Tech stocks plus United Health, Berkshire Hathaway and ExxonMobi), market breadth should broaden to the rest of the market.

For portfolio positioning, Riach suggested selectively adding to Equities, overweighting U.S. and Emerging markets equities, underweighting Canada and Europe equities, and for Fixed Income,”trimming duration and prefer higher quality corporates.” In short, “a diversified and dynamic approach [is] the most likely path to stable returns.”

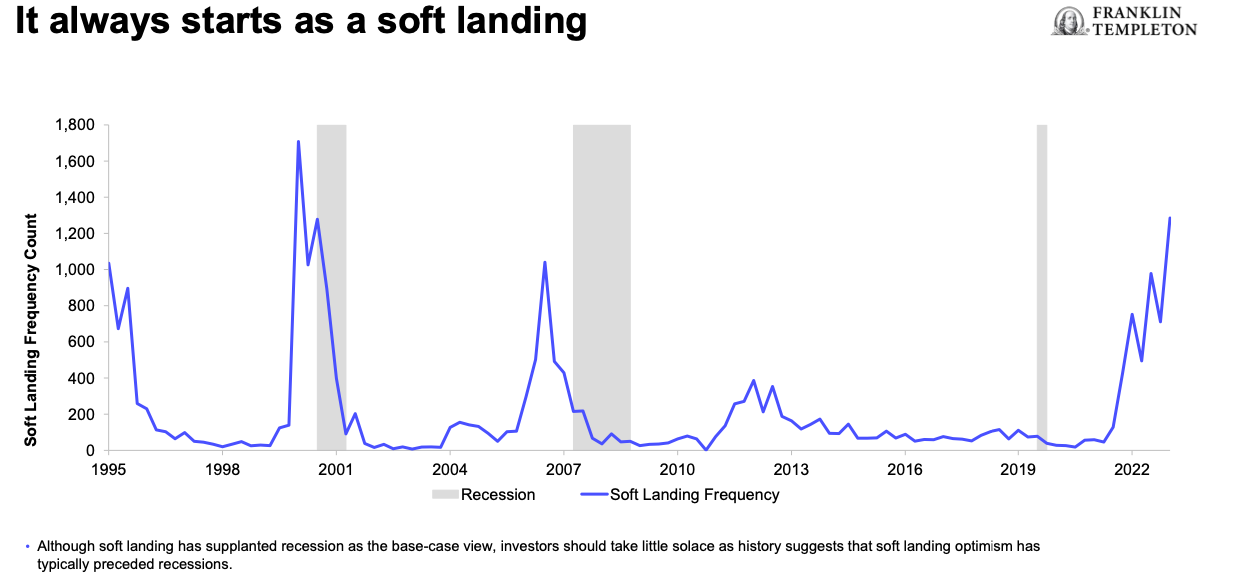

Jeff Schulze, Head of Economic and Market Strategy, ClearBridge Investments (part of Franklin Templeton) gave a presentation titled “Anatomy of a Recession.” A recession always starts as a “soft landing,” as the slide below illustrates. “We’re not out of danger. Leading indicators point to Recession,” he said, “The base case is Recession.” While the S&P500 consensus is for earnings growth, the U.S. GDP is expected to worsen.

He described himself not as a permabear but a permabull, at least until a year ago. If as he expects there’s a “soft landing” with stocks possibly correcting by 15 to 20% in 2024 Schulze would view that as an opportunity to add to U.S. equities in preparation for the next secular bull market.

One of the catalysts will be A.I., not just for the Magnificent 7 but also for the S&P500 laggards. As the chart below illustrates, economic growth often holds up well leading into a recession, with a rapid decline coming only just before the onset of a recession. Continue Reading…

A majority of nearly retired Canadian households — 55 per cent — will have to make lifestyle changes to avoid running out of money in their old age, says a Deloitte Canada report released on Wednesday.

Worse, that percentage jumps to almost three quarters (73%) if you factor in unexpected costs like health care, long-term care costs and occasional one-off expenses. You can find the full release here from Canada Newswire.

Some 4,000 retired and near-retired Canadian households were surveyed, all between ages 55 and 64.

Only 14% of 3 million soon-to-retire households can retire with confidence and be able to absorb unexpected costs without much stress. This fortunate group tends to have at least $900,000 in financial assets and likely have a paid-for home.

31% of near-retirees will require support in the form of the government’s public pension system: nearly a million households are expected to rely mainly on the Canada Pension Plan in retirement.

Only 24% of private-sector workers participate in employer-sponsored pension plans

40% of retirees have not purchased health insurance, of which 44% cite expensive premiums as the primary reason for not doing so

73% of near-retiree households will be at risk of financial hardships in later stages of life if they require long-term care

58% of near-retiree and retiree households do not have a formal or detailed retirement plan in place

44% of working Canadians were dipping into their retirement savings to pay for non-retirement-related expenses

“By employing a host of radical and innovative solutions, Canada can help to protect those vulnerable both near and in-retirement, and set a global standard for how it tackles retirement on the world stage,” says Hwan Kim, Partner, Financial Services Innovation and Open Banking at Deloitte Canada in the press release, “Given roughly 40 per cent of retirement wealth inequality is due to a lack of financial knowledge, the financial services ecosystem must collaborate with the health care system and public sector to equip Canadians with accessible retirement advice, holistic near-retirement offerings, updated pension planning, quality health care, and new resources to retire confidently.”

The report concedes the saving for Retirement has always been “a daunting challenge for working Canadians,” things have gotten worse the last few years. The shift from employer-provided guaranteed Defined Benefit pensions to group RRSPs and Defined Contribution pensions that fluctuate with financial markets is a major hurdle. The report also cites the rising costs of retirement, a lack of high-quality, near-retirement planning resources, and unexpected expenses during late-stage retirement.

According to the report, 55 per cent of near-retiree households will need to make lifestyle changes to avoid outliving their financial savings – a number that is expected to jump to 73% when factoring in unexpected expenses such as healthcare, long-term care costs, and one-off expenditures.

A Bank of Montreal survey released early in 2023 found Canadians believe they need $1.7 million to retire. My blog on this in February asked whether this was doable or not.

Financial services silos must collaborate

The Deloitte report says the Canadian financial services “ecosystem must collaborate across banking, wealth management, insurance, and the public sector.” This ecosystem needs to focus on three main categories of commercially viable solutions: improve the quality and accessibility of near-retirement advice and products, help retirees manage rising retirement costs, and help Canadians build healthy saving habits early on. Continue Reading…

Joe Biden this week carrying a copy of Democracy Awakening, via Threads.

While the Hub’s focus is primarily on investing, personal finance and Retirement, Findependence has given me sufficient leisure time to absorb a lot of content on politics and the ongoing battle to preserve democracy and in particular American democracy. What’s the point of achieving Financial Independence for oneself and one’s family, if you find yourself suddenly living in a fascist autocracy?

To that end, I have recently read two excellent books that summarize where we are, where we have come from and where we likely may be going. These books came to my attention from two relatively new social media sites I joined in the past year.

For those who care, I am still on Twitter (now X) but restrict most of my posts there to the financial matters on which this blog focuses. I post there as @JonChevreau, which is the same handle I have on Mastodon (since Nov 6, 2022) and Threads, which I joined a week after its early July launch this summer. Threads is now almost the polar opposite of X politically, a veritable Blue haven: just last week Joe & Jill Biden both signed on as @potus and @flotus respectively, as well as under their real names. So did vice president Kamala Harris (posting as @VP and @kamalaharris).

Amazon.ca

But back to the books. The first must read is Prequel, by the brilliant U.S. broadcaster Rachel Maddow [cover image shown on the left]. Tellingly, it’s subtitled An American Fight Against Fascism.

The second is Democracy Awakening, by Heather Cox Richardson [cover shown below]. Both are available as ebooks on the Libby app, through (hopefully) your local library. I couldn’t find either book on Scribd (now called Everand) but they do have ebook Summaries of both.

An American Hitler?

Given that the 2024 U.S. election is now about 12 months away, there is a certain urgency to these books. The Maddow book I’d read first since it’s a brilliant historical recap of the rise of German Fascism in the 1930s and — the shocking bit! — how close Germany came to installing fascists in America. It’s literally about Germany’s search for an American Hitler it hoped to install. It’s full of sinister characters you’ve probably not heard about before, like the assassinated Huey Long.

Maddow credits the reader with enough intelligence to extrapolate from that period into the current dangerous environment. One is left to infer how she feels about the parallels to the modern GOP and its fascist leader and would-be dictator: she never says their names although she is usually more explicit in her MSNBC and podcast commentaries.

Modern readers could easily substitute Putin’s Russia for Hitler’s Germany and draw their own conclusions about the parallels to collusion with foreign powers. There are also similarities between protracted attempts by the U.S. government to try the perpetrators in court and the protracted Delay tactics of the Defence — including many U.S. senators of the 1930s and early 1940s. And as is currently the case, these tactics largely seemed to work, since the Allies won World War II before most of the collaborators were brought to justice. Frustrating indeed, as many of today’s Americans bristled at the ultimate futility of the Mueller Report around 2019 and other protracted legal proceedings that may not be resolved before the 2024 election.

Maddow of course hints at this right at the end, quoting one frustrated prosecutor (O. John Rogge) from the 1940s:

“The study of how one totalitarian government attempted to penetrate our country may help us with another totalitarian country attempting to do the same thing …the American people should be told about the fascist threat to democracy.”