Unretirement is a concept not unlike Findependence or Financial Independence; it’s also the title of a recently published book by Chris Farrell, Bloomberg Businessweek columnist and senior economics contributor for American Public Media’s syndicated radio show, Marketplace.

I’ve also seen the term Unretirement used by Sun Life Financial in Canada but that seems to be more a marketing term the company uses to promote its surveys on traditional retirement. That survey has been going for six years now, which certainly predates the publication of Farrell’s UnretirementContinue Reading…

One of the strongest arguments made by investment industry groups against banning embedded commissions – or the trailer fees paid to advisors when you purchase mutual funds – is that investors don’t want to pay up-front for financial advice.

Advocis, which represents financial advisors across Canada, as well as the Mutual Fund Dealers Association, believe things are fine just the way they are, claiming, “investors prefer to pay for financial advice through fees that are part of their mutual funds.”

These arguments are used to convince regulators that a ban on trailer fees would only hurt investors, with potentially “devastating consequences” for those who are just starting out and don’t have the means to pay directly for advice.

I’ve tried to debunk this argument in a recent post, stating that it’s up to the investment industry to adapt and deliver new service (and cost) models to meet the needs of consumers.

But a recent study by Morningstar India shed further light on the gap between investor expectations and what advisors perceived to be investors’ expectations.

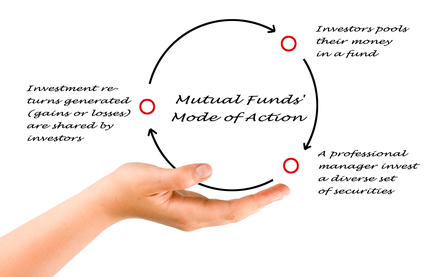

Hub Extra for Newcomers: Primer on how mutual funds work

A third of investors don’t seek professional advice

The study found that over one-third of investors do not seek out professional advice when it comes to their finances, instead relying on their own knowledge or help from family, friends or colleagues.

Here’s my latest MoneySense blog, which is a followup to Robb Engen’s article here at the Hub about his conversion from stock-picking to 100% “pure” indexing.

After Robb revealed his “conversion” and I appealed for other readers with similar stories, readers started to come out of the woodwork. In one of the cases, the “confession” appeared first at MoneySense and now The Hub.

In addition to the two readers profiled in the MoneySense blog, I’ve already started to receive more emails from other “pure” readers. Please let me know by emailing me at jonathan@findependence.com. Hopefully, we’ll discover that there are a lot more than the half dozen I’m so far aware of.

I’ve republished the original version of the blog below and included photographs of the two readers that were not included in the MoneySense version:

Pure indexers step forward

Boomer & Echo’s Robb Engen

Early in January, popular blogger and fee-only financial planner Robb Engen announced on Twitter and his Boomer & Echo site that he had finally bitten the bullet – he’d liquidated his portfolio of individual dividend-paying stocks in order to become a 100% “pure” indexer. Continue Reading…

Once you hit the Decumulation years, a common option new retirees consider is Downsizing from a large urban home. Friends of ours on our street are about to put their home up for sale in order to move to a small town an hour away. The difference in the home values will constitute a major nest egg to supplement meagre government pensions and part-time work.

The small-town appeal is a huge factor for retirees because it can allow them to sell their house in a large city and extract the equity, which they can then live off for their remaining years.

Imagine dad dies. The widow and children miss him terribly, but he made good money and they’ll be taken care of financially. What they don’t realize is that dad left them “black money.” He kept most of his money in a secret offshore bank account — black money —unreported to Canada Revenue Agency (CRA). He also left his heirs a big problem.

Governments and tax collectors around the world have come down hard on the banks that harbour secret accounts. The crackdown came after the terrorist attacks of September 11, 2001, as terrorist cells need financing and want to remain under the radar. That got the ball rolling worldwide. As well, governments began cracking down on money laundering from the proceeds of crime (drugs, guns, human trafficking, exotic animal parts smuggling, and so on).

A True Story

This is a true story, with the details changed a bit to protect the heirs from embarrassment. The widow called my firm, distraught and I was able to provide some comfort. It’s good news that the money is not lost forever. But it will take a while to get it back to Canada, and the family will have a Canada Revenue Agency tax bill to pay.

The best news is mom and the kids have no fear of going to jail for tax evasion. They can sleep at night.

At my firm, 2015 started with a call from a Canadian businessman who spends part of his time outside Canada. He was given bad advice years ago by his Canadian stock broker to set up an offshore account. Now the offshore broker is getting out of business, has sold the portfolio and wired funds back to the businessman. But the offshore portfolio was never reported to CRA. The businessman recognizes his obligations, and we are doing voluntary disclosure to bring him onside, once again ending fear of criminal charges. Continue Reading…

By Jonathan Chevreau

By Jonathan Chevreau