My latest MoneySense Retired Money column takes a look at how a new Government program can be used by young people to save up tax-effectively for a first home: including the children of retirees and the almost-retired. For the full column, click on the highlighted text: How retired parents can use the FHSA to help their adult children.

The new First Home Savings Accounts [FHSA] should be operational by April 1, 2023. At least two regular bloggers who often appear here on the Hub have weighed in with summaries of the program. Dale Roberts’ take appeared on his cuthecrapinvesting blog on March 1st. Mark Seed’s myownadvisor blog ran a summary of the key points on March 4th.

For MoneySense and Retired Money, I took a bit of a different take, seeing as the column’s focus technically is on Retirees and near-retirees. These days, that category consists primarily of aging baby boomers like myself, but of course many of us have adult children who may have been slow to jump into the real estate market with home prices in places like Vancouver and the GTA soaring in recent years during the long spell of almost-free money. That era has of course ended with the Bank of Canada gradually raising rates over the past year, which has also helped to push home prices down to slightly more reasonable levels.

Whether they become even more reasonable remains to be seen but of course the positive of slightly lower prices is offset by higher mortgage rates so it’s a bit of a Hobson’s choice. You can wait and hope for the proverbial “blood in the streets” to hit home prices and make the plunge into ownership then, but there’s no guarantee that will happen.

Either way, if Ottawa is providing another tax-optimized way to save up a down payment, why not take advantage of it? We already have the RRSP home-buying program [HBP] and there’s no reason why TFSAs can’t also be used for the same purpose. What’s nice about the new FHSA is that not only does it tax-shelter investment income but it also provides a tax refund on contributions, similar to how RRSPs do so. (as the above blogs note, there are differences however.)

The Home Savings plan we all dreamt of

As quoted in the MoneySense column, CFP and RFP Matthew Ardrey, Wealth Advisor & Portfolio Manager with Toronto-based TriDelta Financial provides the following enthusiastic thumbs up for the new program: “The FHSA is the home savings plan we were all dreaming of when we first got the HBP. Combining the best aspects of the RRSP, tax deductions for contributions, and the TFSA, tax-free qualifying withdrawals, this can be a game changer for the next generation of homebuyers in Canada.” Continue Reading…

Yes, it’s March, also dubbed Fraud Prevention Month. To mark it, a TD survey has been released that finds fraudsters are getting more persistent as the cost of living keeps soaring.

While 62% of Canadians agree they are being targeted now more than ever, a whopping 46% haven’t taken any measures to educate themselves or take protective measures in the past year.

Among the findings:

47% believe the rising cost of living and other financial hardships will expose them to more scams

78% don’t have much confidence in their ability to identify fraud or scams

54% feel stressed or anxious about financial fraud

31% are too embarrassed to tell anyone if they were the victim of a fraud or scam

66% of Gen Z and 44% of Millennials admit they wouldn’t tell someone if they were swindled

“As Canadians report being targeted by a record number of financial fraud attempts, many can benefit from using the tools and resources available to protect themselves and their loved ones,” says Mohamed Manji, Vice President of Canadian Fraud Management at TD in the release, “It’s very important to exercise caution, especially at a time when fraudsters may take advantage of the economic challenges many Canadians are currently facing. In addition to the robust security measures TD has in place for its customers, the best defence against financial fraud is being aware and knowing how to spot it.”

Both TD and the Canadian Anti-Fraud Centre offer a comprehensive library of articles discussing the latest trends in scams and measures Canadians can take to enhance their awareness and avoid falling victim to fraudsters.

Targeting mostly via e-mail or telephone

The survey found 72% of Canadians reported being targeted by email/text message fraud, up 14 percentage points from last year, while 66% were targeted over the phone. Oddly, the poll finds Fraudsters seem to be pivoting away from social media, with only 26% targeted this way, 10 percentage points less than 2022.

Those polled were most concerned about identity theft (52%), title fraud (23%) and fake emergencies (20%).

Factors likely to increase vulnerability to fraud include age (43%), loneliness or isolation (35%), moving recently to Canada (34%) and financial hardship or job loss (32%).

“We’re seeing more fraudsters preying on customers through the ‘grandparent’ or ’emergency’ scam,” adds Manji. “This cruel crime is often successful because it exploits someone’s desire to care for their loved ones. If you get a call from somebody claiming to be a family member or friend in immediate need of funds, hang up the phone and call them back using a number you have for them.”

TD says that with 31% saying they’d be too embarrassed to tell anyone if they were a fraud or scam victim, it’s clear there’s some stigma in talking about this type of crime. If someone believes they’ve fallen victim to a scam, they should immediately report it to their financial institution, local police department, credit bureaus (Equifax and TransUnion) and the Canadian Anti-Fraud Centre.

Both look at the widely publicized BMO poll that found Canadians now need $1.7 million to retire on average. The figure used to be $1.4 million but inflation has made it a bit tougher. Here’s the CNW newswire release from Feb. 7th.

As I mention in the MoneySense column, the Hub version was written off the top of my head and published as part of the initial news cycle. With an extra week to go to expert sources, the updated column is more nuanced and has more accurate returns projections and calculations where the first version consisted of guesstimates.

Of course, generalizations are always dangerous and that goes double for retirement planning, especially over the kind of 40-hour time horizon involved. It’s one thing to be a Millennial investor just starting out on the retirement journey and quite another to be a boomer like myself, looking back at portfolios begun three or four decades earlier. As the original Hub version commented, $1 million isn’t what it used to be. Even so, even maxing out your RRSP contributions each year will take some doing: as I wrote after my quick guesstimate, if you divide $1.7 million by 40 you get $42,400 a year that needs to be contributed each and every year, or almost twice the maximum RRSP contribution permitted even if you’re a top earner.

If you’re fortunate enough to be one half of a couple, $850,000 per spouse seems a lot more achievable. And if you have a Defined Benefit pension plan, you may not need anything else, whether from an RRSP, TFSA or non-registered savings. If you hang in to a gold-plated DB pension plan for 40 long years, odds are it alone will be the equivalent of $1 million, and possibly backstopped by taxpayers and indexed to inflation to boot.

But if you begin investing early, you won’t need to save anywhere close to $1.7 million because of investment returns that are tax-deferred inside an RRSP. Because of the time value of money, even the modest 4% compounded annual investment returns will over the course of 40 years get you to the promised land.

The Hub blog assumed investment returns of 4% per annum either from fixed income (4- or 5-year GICs) or from high-yielding dividend-paying stocks, like Canada’s bank stocks, utilities or telecom majors. In the MoneySense column, wealth advisor Matthew Ardrey of TriDelta Financial assumes a more hopeful 5% return across those asset classes.

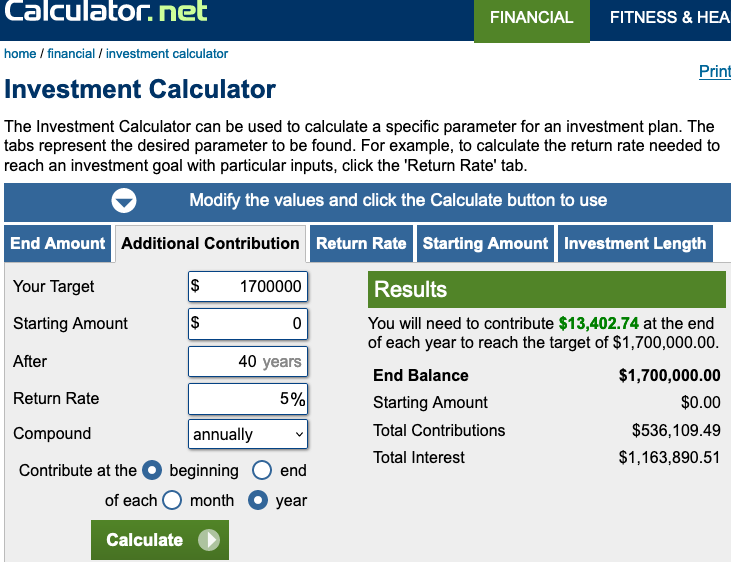

Using the retirement calculator Calculator.net, used by BMO (www.calculator.net), if you can earn a conservative 4% a year, you’d need to contribute only $17,202 (rounded) at the end of each year to reach $1.7 million after 40 years. That breaks down to $688,074 in total contributions and another $1,011,926 in interest payments.

And if you can do better than 4%, you could contribute even less and make up the difference in investment returns: at 5% a year, you’d need to contribute only $13,403 (rounded) at the end of each year to reach $1.7 million after 40 years. That breaks down to $536,110 in contributions and $1,163,891 in interest.

P.S. MyOwnAdvisor doesn’t think most need to save $1.7 million

As a postscript, I note that on his Weekend Reads feature, MyOwnAdvisor also tackled this question of $1.7 million, which ran after I had already submitted my MoneySense column on the same topic. You can find Mark’s take here, but here’s his bottom line:

Front page of Wednesday’s Financial Post print edition.

Plenty of press this week over a BMO survey that found Canadians now believe they’ll need $1.7 million to retire, compared to just $1.4 million two years ago (C$). The main reason for the higher nest-egg target is of course inflation.

As you’d expect, the headline of the story alone attracted plenty of media attention. I heard about it on the car radio listening to 102.1 FM [The Edge]: there, a female broadcaster who was clearly of Millennial vintage deemed the $1.7 million ludicrously out of reach, personalizing it with her own candid confession that she herself hasn’t even begun to save for Retirement. Nor did she seem greatly fussed about it.

Here’s the Financial Poststory which ran in Wednesday’s paper: a pick-up of a Canadian Press feed; a portion is shown to the left. The writer, Amanda Stephenson, quoted BMO Financial Group’s head of wealth distribution and advisory services Caroline Dabu to the effect the $1.7 million number says more about the country’s economic mood than about real-life retirement necessities.

BMO’s own client experience finds that “many overestimate the number that they need to retire,” she told CP, “It really does have to be taken at an individual level, because circumstances are very different … But $1.7 million, I would say, is high.”

Here’s my own take and back-of-the-envelope calculations. Keep in mind most of the figures below are just guesstimates: those who have financial advisors or access to retirement calculators can get more precise numbers and estimates by using those resources. I may update this blog with input from any advisors or retirement experts reading this who care to fill in the blanks by emailing me.

A million isn’t what is used to be

Image via Tenor.com

Back in the old days, a million dollars was considered a lot of money, even if that amount today likely won’t get you a starter home in Toronto or Vancouver. This was highlighted in one of those Austin Powers movies, in which Mike Myers (Dr. Evil) rubs his hands in glee but dates himself by threatening to destroy everything unless he’s given a “MILLL-ion dollars,” as if it were an inconceivably humungous amount.

The quick-and-dirty calculation of how much $1 million would generate in Retirement depends of course on your estimated rate of return. When interest rates were near zero, this resulted in a depressing conclusion: 1% of $1 million is $10,000 a year, or less than $1,000 a month pre-tax. When my generation started working in the late 70s, a typical entry-level job paid around $12,000 a year so you could figure that $1 million plus the usual government pensions would get you over the top in retirement.

Inflation has put paid to that outcome but consider two rays of hope, as I explained in a recent MoneySense Retired Money column. To fight inflation, Ottawa and most central banks around the world have hiked interest rates to more reasonable levels. Right now you can get a GIC paying somewhere between 4% and 5%. Conservatively, 4% of $1 million works out to $40,000 a year. 4% of $1.7 million is $68,000 a year. That certainly seems to be a liveable amount. More so if you have a paid-for home: as I say in my financial novel Findependence Day, “the foundation of Financial Independence is a paid-for home.”

Couples have it easier

If you’re one half of a couple, presumably two nest eggs of $850,000 would generate the same amount: for simplicity we’ll assume a 4% return, whether in the form of interest income or high-yielding dividend stocks paid out by Canadian banks, telecom companies or utilities. I’d guess most average Canadians would use their RRSPs to come up with this money.

This calculation doesn’t even take into consideration CPP and OAS, the two guaranteed (and inflation-indexed) government-provided pensions. CPP can be taken as early as age 60 and OAS at 65, although both pay much more the longer you wait, ideally until age 70. Again, couples have it easier, as two sets of CPP/OAS should add another $20,000 to $40,000 a year to the $68,000, depending how early or late one begins receiving benefits.

This also assumes no employer-pension, generally a good assumption given that private-sector Defined Benefit pensions are becoming rarer than hen’s teeth. I sometimes say to young people in jest that they should try and land a job in either the federal or provincial governments the moment they graduate from college, then hang on for 40 years. Most if not all governments (and many union members) offer lucrative DB pensions that are guaranteed for life with taxpayers as the ultimate backstop, and indexed to inflation. Figure one of these would be worth around $1 million, and certainly $1.7 million if you’re half of a couple who are in such circumstances.

Private-sector workers need to start RRSPs ASAP

But what if you’re bouncing from job to job in the private sector, which I presume will be the fate of our young broadcaster at the Edge? Then we’re back to what our flippant commentator alluded to: if she doesn’t start to take saving for Retirement seriously, then it’s unlikely she’ll ever come up with $1.7 million. In that case, her salvation may have to come either from inheritance, marrying money or winning a lottery.

For those who prefer to have more control over their financial future, recall the old saw that the journey of a thousand miles begins with a single step. In Canada, that step is to maximize your RRSP contributions every year, ideally from the moment you begin your first salaried job. Divide $1.7 million by 40 and you get $42,400 a year that needs to be contributed. OK, I admit I’m shocked by that myself but bear with me. The truth is that no one even is allowed to contribute that much money every year into an RRSP. Normally, the limit is 18% of earned income and the 2023 maximum RRSP contribution limit is $30,780 (and $31,560 for the 2024 taxation year.) Continue Reading…

My latest MoneySense Retired Money column has just been published and can be accessed by clicking the highlighted headline: Inflation and investments: Heads up if you’re retired or retiring soon.

It looks at the anxiety of would-be retirement savers in the light of soaring inflation and in particular, a recent Leger Questrade poll that looked at how inflation is affecting Canadians’ intentions to contribute to TFSAs and RRSPs. My Hub blog on this includes 4 charts on the topic.

Not surprisingly, inflation is a particular concern for retirees and those hoping to retire soon. The 2023 RRSP Omni report found that while 87% of Canadians are worried about rising prices, it also found 73% of RRSP owners still plan to contribute again this year, and so do 79% of TFSA holders. That’s despite the fact 69% fret that inflation will impact their RRSPs’ value and 64% worry about their TFSAs’ value. Seven in ten with RRSPs and 64% with TFSAs are concerned about inflation and a possible recession: 25% “very” concerned.

A Silver Lining

The MoneySense column also summarizes some of the compensating factors that Ottawa builds into the retirement saving system: as inflation rises, so too do Tax brackets, the Basic Personal Amount (BPA: the tax-free zone for the first $15,000 or so of annual earnings), and of course TFSA contribution limits (now $6500 in 2023 because of inflation adjustments). This was nicely summarized late in 2022 by Jamie Golombek in the FP, and reprised in this Hub blog early in the new year.

Because tax brackets and contribution levels are linked to inflation, savers benefit from a little more tax-sheltered (or tax deferred) contribution room this year. The RRSP dollar limit for 2023 is $30,790, up from $29,210 in 2022, for those who earn enough to qualify for the maximum. And TFSA room is now $6,500 this year, up from $6,000, because of an inflation adjustment. As Golombek noted, the cumulative TFSA limit is now $88,000 for someone who has never contributed to one.

Golombek, managing director, Tax & Estate planning for CIBC Private Wealth, wrote that in November 2022, the Canada Revenue Agency said the inflation rate for indexing 2023 tax brackets and amounts would be 6.3%: “The new federal brackets are: zero to $53,359 (15%); more than $53,359 to $106,717 (20.5%); more than $106,717 to $165,430 (26%); more than $165,430 to $235,675 (29%); and anything above that is taxed at 33%.”

Another break is that the yearly “tax-free zone” for all who earn income is rising. The Basic Personal Amount (BPA) —the annual amount of income that can be earned free of any federal tax — rises to $15,000 in 2023, as legislated in 2019.

CPP and OAS inflation boosts in late January

On top of that, retirees collecting CPP and/or OAS can expect significant increases when the first payments go out on or around Jan. 27, 2023. (I include our own family in this). There’s more information here. Continue Reading…