In a nutshell, once again pundits are fretting that interest rates have been so low for so long, that they inevitably must soon begin to rise. And if and when they do, because of the inverse relationship between bond prices and interest rates, any rise in rates may result in capital losses in the value of the underlying bonds.

In practice, this means choosing (or switching) to bond ETFs with shorter maturities: the risk rises with funds with a lot of bonds maturing five years or more into the future, although of course as long as rates stay as they are or fall, that can be a good thing.

As the column shows, typical aggregate bond ETFs (like ETF All-Star VAB) and equivalents from iShares have suffered losses in the first quarter of 2021. Shorter-term bond ETFs that hold mostly bonds maturing in under five years have been hit less hard. This is one reason why in the US Vanguard Group just unveiled a new Ultra Short Bond ETF that focuses on bonds maturing mostly in two years or less.

The short-term actively managed bond ETF is called the Vanguard Ultra Short Bond ETF. It sports the ticker symbol VUSB, and invests primarily in bonds maturing in zero to two years. It’s considered low-risk, with an MER of 0.10%.

Of course, if you do that (and bear the currency risk involved, at least until Vanguard Canada unveils a C$ version), you may find it less stressful to keep your short-term cash reserves in actual cash, or daily interest savings account, or 1-year or 2-year GICs. None of these pay much but at least they don’t generate red ink, at least in nominal terms. Continue Reading…

My latest MoneySense Retired Money column has just been published: it looks at how much real estate should make up of an investment portfolio, either through direct ownership in physical real estate, or through more diversified REITs or REIT ETFs. Click on the highlighted headline for the full column: How much real estate should you have in a balanced portfolio?

How much should real estate comprise in a balanced portfolio? While a principal residence certainly will be a big part of most people’s net worth, personally I don’t “count” it as part of my investment portfolio, even though it can ultimately serve as a retirement asset of last resort, via Home Equity Line of Credits (HELOCs), reverse mortgages or simply an outright sale when it’s time to enter a retirement or nursing home.

If you take that approach, and many of my advisor sources do, then the question becomes how much real estate should you have in your investment portfolio, above and beyond the roof over your head?

Certainly, if you are happy being a landlord and handy about home maintenance, direct ownership of rental apartments, duplexes or triplexes and the like is a time-honored route to building wealth. That’s the focus of organizations like the Real Estate Investment Network (REIN).

However, if you don’t want the hassle of being a landlord, you may want to try Real Estate Investment Trusts (REITs), which are far more diversified both geographically and by housing type. Some REITs focus on baskets in particular real estate sectors, such as residential apartments or retirement homes.

A still more diversified approach is to buy ETFs providing exposure to multiple major REIT categories, whether Canadian, US or international.

Adrian Mastracci, portfolio manager with Vancouver-based Lycos Wealth Management, says the REIT idea “makes sense” but suggests they should not make up more than 5 or 10% of an investor’s total wealth or not more than 7% of an equity portfolio. “I consider it part of the equity bucket. Publicly traded REITS trade more like equities than real estate.” He advises buying top-quality REITs (or ETFs holding them), diversified across Canada but avoids foreign ETFs because “you want the dividends taxed as Canadian dividends.”

Most of the major ETF suppliers with a Canadian presence have broad-based passively managed REITs although there is at least one actively managed one.

Major passive and active Canadian REIT ETFs

The Vanguard FTSE Canadian Capped REIT Index ETF (ticker VRE/TSX) was launched in 2012 and has a modest MER of 0.39%. As the name implies, any one holding is capped at 25% of the total portfolio [typically this is RioCan.] Its mix is 22% retail REITs, 19.8% office REITs, 18.5% real estate services, 18.5% residential REITs, 8.5% industrial REITs, 8.1% diversified REITs and 4.6% real estate holding and development.

An alternative is XRE, the iShares S&P/TSX Capped REIT Index ETF, trading on the launched in 2020, which holds roughly 16 Canadian REITs, with weightings almost identical to VRE. The iShares product (from BlackRock Canada) has a slightly higher MER of 0.61%. Continue Reading…

A report by LendEDU finds Bitcoin is making a lot of headway with investors over Gold. 56% said Bitcoin is a better investment to maximize profits, versus just 33% for gold. However, they still see gold as a better store of value against inflation, with 50% answering gold (including 67% over the age of 54), and 39% saying bitcoin.

On behalf of New Jersey-based LendEDU, research firm Pollfish surveyed 1,000 Americans on April 21st to see how they would deploy an initial US$50,000 to build a retirement nest egg, and found gold only had a slight edge: 45% versus 42% for bitcoin. However, if the goal of the $50,000 investment is strictly to maximize profits, 49% specified bitcoin, versus just 37% for gold.

LendEDU Director of Communications Mike Brown says Bitcoin is up roughly 68,189,500% since its start in 2009, while gold is up 105% over the same period.

“Gold is proven as a reliable investment and safe haven against market volatility and inflation, which is especially relevant in 2021. Bitcoin is becoming a competitor for just the same thing, although its wild price fluctuations are not for the faint-hearted and attract a younger, more aggressive investor … We found gold is still trusted for more cautious investing, especially amongst older Americans, but bitcoin is closing that gap and is preferred for speculative investing, especially with the younger crowd.”

LendEDU’s Mike Brown

Brown says the survey results were “none too surprising; bitcoin has periods of monumental gain that make it a salivating buy for aggressive investors trying to make a profit. But it also has periods of monumental loss and faces constant regulatory and institutional scrutiny that make it a questionable buy if your first investment priority is protecting the money you already have.”

Gold, on the other hand, doesn’t have eye-popping surges like bitcoin but is safe and has historically delivered steady profits to the patient investor looking for a financial safe haven.

The survey reveals a younger bias towards bitcoin and an older population favoring gold. Thus, 56% of those between the ages of 18 and 24 thought bitcoin was the better speculative asset, while 29% thought gold was. The percentages were 29% and 55%, respectively, for poll participants over 54.

Similarly, 42% of the 18 – 24 cohort thought bitcoin was a better store of value to protect against inflation, while 44% said gold. For the over 54 cohort, those percentages were 16% and 67%, respectively.

Brown found the 35-44 age group surprising as they were quite bullish on bitcoin in all four questions and broke with the normal trend that had older respondents favoring gold and younger ones opting for bitcoin. “This could be due to this demographic getting in on bitcoin in the extremely early stages, around 2010 when they were in their mid-twenties or early-thirties.”

When asked if they have invested in bitcoin or gold recently amid concerns about inflation, 15% had invested in gold, 31% in bitcoin, 15% in both, and 36% in neither.

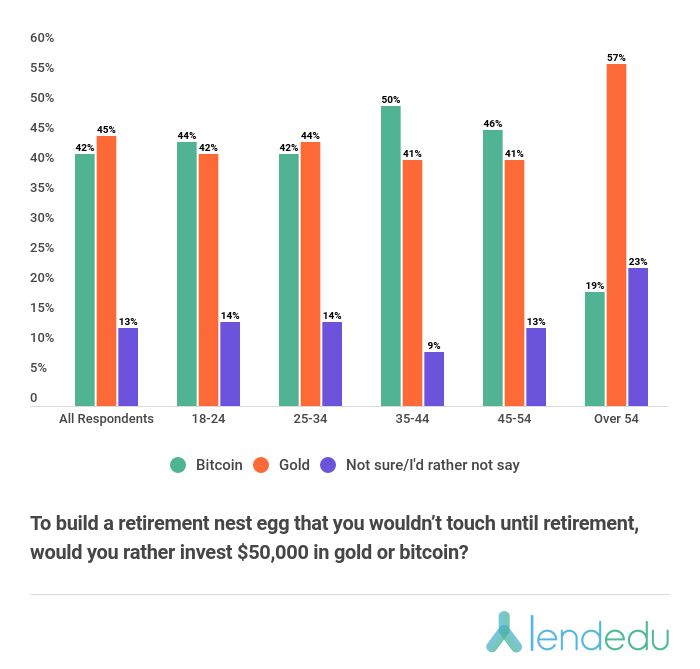

For retirement investing, gold still holds a dwindling edge

In another part of the survey, poll participants were given four increasing monetary values and asked if they would rather invest each value in either bitcoin or gold to build a retirement nest egg that they couldn’t touch until retirement. In nearly every scenario, gold was the preferred retirement investment choice over bitcoin. Only when $1,000 was the starting amount did more respondents (47%) want to invest in bitcoin over gold (43%).

But as the starting amount went up, so too did the risk, which is likely why respondents switched over to the less-risky, less-volatile gold to start building their retirement nest eggs as the questions progressed. As Brown notes, “Retirement accounts should be stable, and you’ll lose a lot less sleep investing $50,000 in gold instead of $50,000 in bitcoin.”

Even so, no matter the initial investment amount, most age groups preferred building their retirement nest egg through bitcoin rather than gold. For example, 46% of the 45-54 cohort wanted to invest $50,000 in bitcoin compared to 41% who said gold. Continue Reading…

The first Federal Budget in more than two years was unveiled shortly after 4 pm Monday. You can get the official documents [all 724 pages of it, with the heft of a big-city telephone book] from the Department of Finance here.

It sports the title A Recovery Plan for Jobs, Growth, and Resilience.

The last federal budget [“Investing in the Middle Class”] came down on March 19, 2019.

You can find the latest Budget tweets and post-announcement reaction under the hashtag #Budget2021, and on my Twitter feed @JonChevreau, which also scrolls on the right of this site. Minister of Finance Chrystia Freeland tweets as @cafreeland. Earlier Monday she tweeted that “we will finish the fight against COVID-19 and invest in job creation and a resilient economy.”

Federal Minister of Finance and Deputy Prime Minister Chrystia Freeland. (Twitter.com)

Billed as a post-pandemic Budget, it lived up to the prerelease leaks of a spending marathon the past week. In short it is Justin Trudeau’s pre-election Spendapalooza 2021. More than $100 billion in spending over 3 years was unleashed, including $30 billion over 5 years and $8.3 billion a year thereafter for the centrepiece of it all: a National Childcare and Early Learning Program.

No real help to cool Housing Bubble and other measures that didn’t happen

As interesting as what was announced is what many feared might be announced and didn’t happen. As far as I can see at this point, there was no move to end the tax-free gains of a principal residence, nor did I see any changes in capital gains tax inclusion rates on investments in general. As Watson quipped about taxes, “Overthreaten and underdeliver.”

Also in the category of things we’re glad not to see is, as Global News summarized, no hike to the GST and no imposition of a Universal Basic Income, no broad-brush Wealth Tax [but new taxes on expensive cars, boats and planes] and no increases in Health Transfers to the provinces. There wasn’t even significant help to cool runaway housing markets, apart from a tax on vacant or underused residential property owned by non-residents: as reported by Robyn Urback in the G&M.

Nor was there much about Pharmacare, to the dismay of the NDP.

Apart from that there was billions for everybody. As Andrew Coyne wrote in the G&M, the budget had to be the longest in history because “this budget is about everything.” He notes that the word “support” appears almost 1,000 times, and benefit/s more than 1,300 times.

OAS sweetener for 3.3 million seniors

A $500 one-time Old Age Security payment for seniors 75 or older [as of June 2022] is coming in August, followed by a 10% rise in regular OAS benefits in July 2022. Continue Reading…

Purpose Investments Inc. says it has been cleared by Canadian securities regulators to launch the Purpose Ether ETF, which would be the first direct-custody Ether [Ethereum] ETF in the world.

While there already exist Ethereum-owning closed-end funds trading both on US and Canadian exchanges, Purpose said in a press release Friday that its new Ether ETF is designed to provide investors with exposure to the popular Ether cryptocurrency by investing directly in physically settled Ether tokens. The ticker symbol will be ETHH, available in three classes of units: Canadian dollar currency hedged units (ETHH); Canadian dollar non-currency hedged units (ETHH.B) and US dollar units (ETHH.U).

“While Bitcoin tends to get a lot of attention as it was the first major cryptocurrency, what Ether and the Ethereum ecosystem represent is one of the most exciting new technology visions today in society,” said Purpose founder and CEO Som Seif, “By launching the first ETF in the world that directly owns and provides exposure to Ether, we are enabling every investor to have access to this unique opportunity and ecosystem.”

Invests directly in physically settled Ether

The ETF will be the first in the world to invest directly in physically settled Ether. The ETF provides investors easy access to the emerging asset class of cryptocurrency without the associated risk of self-custody within a digital wallet. Similar to the Purpose Bitcoin ETF and other physically backed gold or silver products, the ETF will always be backed directly by physically settled Ether holdings, the company says.

Purpose will act as manager of the ETF while Ether Capital Corporation — a company with long-established expertise in digital assets — will act as a special consultant to Purpose.

“Our role in Purpose Ether ETF is to help make sure the more complex aspects of cryptocurrency ownership and transactions fit together,” said Brian Mosoff, CEO of Ether Capital. “We focused on addressing key issues relating to Ether custody, transactions and liquidity. Ether is the cryptocurrency we believe has the most potential for the future and is where our expertise really lies.”

Ether holdings will be kept in “cold storage” — the most secure custody solution in the market. As it did with Purpose Bitcoin ETF, Purpose Investments is working with Gemini Trust Company, LLC as sub-custodian and CIBC Mellon Global Securities Services Company as fund administrator.

The ETF’s daily NAV will be priced based on the daily spot price of the TradeBlock ETX Index.

Purpose Bitcoin ETF, which launched February 18, 2021, has attracted more than C$1.4 billion in assets since its launch, which it says makes it “one of the most successful ETF launches in history.”