The following is a question-and-answer session conducted via email with advisor John De Goey following his recent talk at the MoneyShow in Toronto, which we reported here. Some of the questions and answers also appeared in my recent MoneySense Retired Money column here.

Jon Chevreau, Findependence Hub: How defensive do you think low-volatility ETFs (i.e., BMO’s, iShares, Harvest) are?

John De Goey: Let’s say the market pulls back by 25%. If you can handle that, then you don’t need a low-volatility ETF. In short, low-volatility products are more defensive than market (cap)-weighted products, but it all depends on how investors react and behave when things go south.

Chevreau Q2.) Most of those are overweight utilities, consumer staples and healthcare stocks. Do you advocate that investors do this themselves with sector ETFs?

De Goey – I generally don’t recommend buying utilities as a stand-alone product/strategy. That said, if you already own cap-weighted products and want to be more conservative, it would likely be more tax effective to simply add utilities rather than sell cap-weighted products in order to buy low-vol products. Same net result, but less tax on the way.

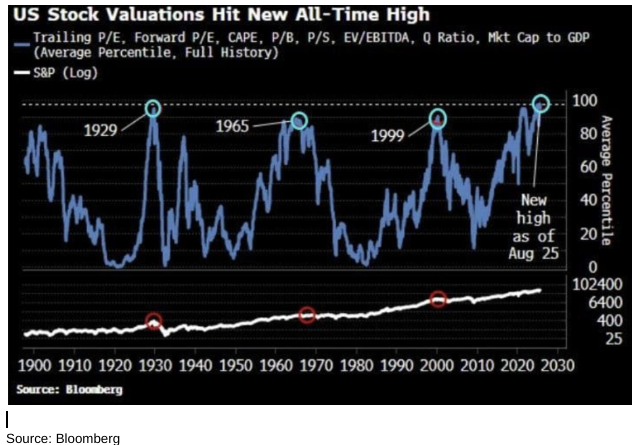

Chevreau Q3.) If U.S. stocks are so richly priced, do you advocate owning a Value U.S. ETF to compensate, or simply sell down some U.S. or and add more International/Canada? Or other factor funds?

De Goey – I recommend getting out of the U.S. entirely. If you cannot do that then, at the very least, I’m worried that there’s an AI bubble much like what we saw with .com a quarter-century ago.

Chevreau Q4.) What range of asset allocation do you recommend for retirees, especially those who are middle-of-the-road and risk-averse?

De Goey: I think all portfolios should have alternatives. Pension plans like CPP, OMERS and HOOP all have over 33% in alternatives. But for MOR retail investors, I’d opt for something like 20% alternatives, 30% income, and 50% equity.

Chevreau Q5.) Can investors and especially retirees rely on global Asset Allocation ETFs to keep them out of too many over-valued U.S. stocks?

De Goey: I wouldn’t use the word ‘rely.’ Such products will soften the blow, but right now the U.S. represents almost 2/3 of global stock market capitalization. So, if all your stocks were in a single global ETF or mutual fund with a cap-weighted mandate, you’d have massive exposure to a massively over-valued market.

Chevreau Q6.) What about annuitizing a portion of an RRSP/RRIF? Continue Reading…