My latest Financial Post column has just been published, both online and on page FP6 of the Friday paper. You can click on the full piece by clicking on the highlighted headline: Everything you need to know about the enhanced CPP — from how much you’ll pay to how much you’ll get.

It summarizes the new enhanced Canada Pension Plan regime, which has (as of this month) started to show itself in slightly higher payroll deductions for both employers and employees.

Won’t fully kick in for 45 years

But as the piece explains, the enhanced CPP won’t fully kick in until 45 years from now, and most Baby Boomers will be retired before feeling any benefits beyond that of the normal practice of delaying CPP till age 70. And as one source explains, even the expanded CPP still isn’t as generous as Social Security is in the United States. Not only do they pay slightly higher payroll premiums to fund Social Security, but they also pay based on a much higher level of income.

U.S. Social Security still more generous

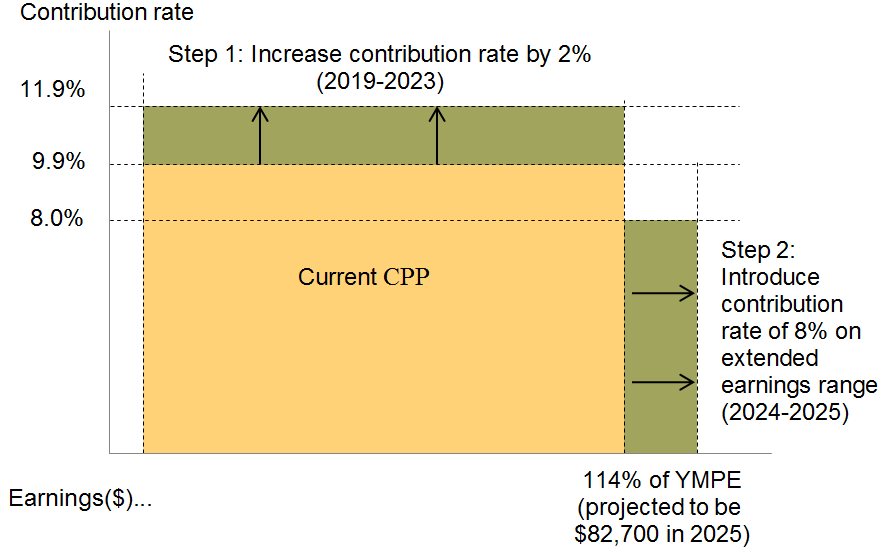

US contributions are up to US$132,900 in income, compared to about half that in Canada: a Year’s Maximum Pensionable Earnings limit (YMPE) of $57,400 in effect in 2019. CPP was originally designed to “replace” about 25% of the average worker’s income but the enhanced CPP will take that up to about 33.3% once it’s fully implemented. Gradually, the limit will rise to $65,400 (rounded down, 2019 dollars.)

While the full payout is 45 years away, benefits start edging up this year. Until now, the maximum CPP benefit at the traditional retirement age of 65 was $1,154.58 assuming earnings at or beyond the YMPE, according to Doug Runchey, of Vancouver Island-based DR Pensions Consulting.

The maximum benefit will be $1,207.83 in 2026, and eventually reach $1,753.78 by 2065. That’s a whopping $21,045 a year!

Too late for the Boomers

Still, Runchey says, “if you’re thinking of applying for your CPP earlier than 2025, the enhanced CPP will be of little value for you.”

As I said at the outset, that’s unlikely to be helpful for Baby Boomers at or on the cusp of retirement. Even so, the combination of an enhanced CPP and the decade-old Tax-free Savings Accounts (TFSAs) is something most Boomers wish they had when they were young!

For more on the enhanced CPP, go to the Government of Canada’s website here.