Can you trust your retirement to a robot? Illustration by Chloe Cushman/National Post files

With the annual RRSP season coming to a close next week (the RRSP contribution deadline is March 1st), there’s plenty of media coverage to remind investors of this fact. Two this week came from my pen (or electronic equivalent).

By robot, we are referring of course to so-called Robo-Advisers or automated online investment “solutions” that generally package up various Exchange-traded Funds (ETFs) and handle the purchase, asset allocation and rebalancing at an annual fee that’s generally is far less than what a mutual fund or two might deliver. (that is, usually 0.5% plus underlying ETF MERs, compared to 2% or more for most retail mutual funds sold in Canada.)

The piece begins with a fond nod to a topic I used to write about periodically in the FP in the 1990s, at the height of so-called Mutual Fund Mania. It was then that I would write about a set-it-and-forget it approach we dubbed the Rip Van Winkle portfolio, which was simply two mutual funds (Trimark Income Growth, a balanced fund) and a global equity fund (Templeton Growth) that in effect did (and still do, I suppose) everything the modern robo advisers do. The difference is that because of ETFs, the robo services are about a quarter of the price of the old “Rip” portfolio.

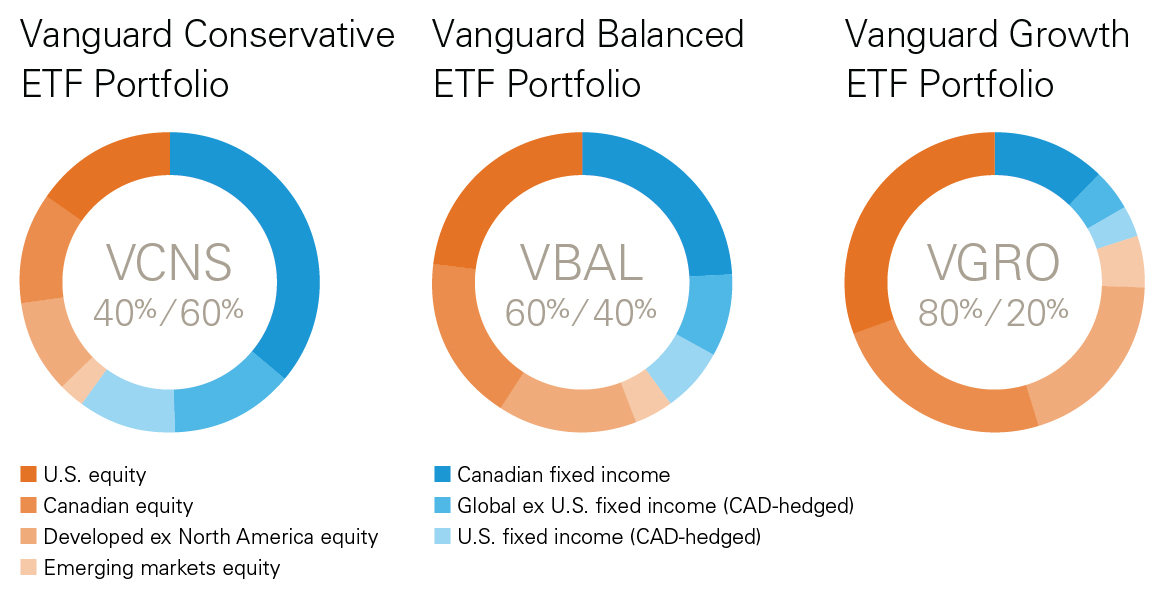

But speaking of undercutting, and as the piece also notes, both “Rip” and the robo services have been undercut by the three new Vanguard asset allocation ETFs that were announced on February 1st, more of which you can find in the Hub blog I wrote at the time: Gamechanger? As I noted there, the Vanguard ETFs seem to be ideal for TFSAs (especially VGRO, the 80% equities offering) but of course they are also ideally suited for a “Rip” like RRSP core offering: VBAL (60% equities) for the typical balanced investor, VCNS (40% equities) for very conservative investors and perhaps those now in the RRIF stage who are required to make forced annual (and taxable) withdrawals.

Motley Fool Canada: 11 myths equals 11 lame excuses for not maxing your RRSP

Meanwhile, Motley Fool Canada has just released a special report I wrote titled The 11 Most Common RRSP myths. The report builds on several RRSP myths that CIBC’s Jamie Golombek published earlier this year, which you can find here, and my FP commentary on them here. The report adds several new myths submitted from veteran advisers like Warren Baldwin.

You can also view this promotional email on the RRSP report by Motley Fool Canada Chief Investment Officer Iain Butler.

Once they move from the wealth accumulation phase to “decumulation” retirees and near-retirees start to focus on how to boost Retirement Income.

The latest instalment of myMoneySense Retired Money column looks at five “enhancements” to do this, all contained in Fred Vettese’s about-to-be-published book, Retirement Income for Life, subtitled Getting More Without Saving More. You can find the full column by clicking on this highlighted headline: A Guide to Having Retirement Income for Life.

You’ll be seeing various reviews of this book as it becomes available online late in February and likely in bookstores by early March. I predict it will be a bestseller since it taps the huge market of baby boomers turning 65 (1,100 every day!): including author Fred Vettese and even Yours Truly in a few months time.

That’s because a lot of people need help in generating a pension-like income from savings, typically RRSPs, group RRSPs and Defined Contribution plans, TFSAs, non-registered investments and the like. In other words, anybody who doesn’t enjoy a guaranteed-for-life Defined Benefit pension plan, of the type that are still common in the public sector but becoming rare in the private sector.

The core of the book are the five “enhancements” Vettese has identified that help to ensure that those seeking to pensionize their nest eggs (to paraphrase the title of Moshe Milevsky’s book that covers some of this ground) don’t outlive their money. Vettese says many of these concepts are current in the academic literature but have been slow to migrate to the mainstream, in part because few of these “enhancements” will be welcomed by the typical commission-compensated financial advisor. That in itself will make this book controversial.

Each of these “enhancements” get a whole chapter but in a nutshell they are:

1.) Enhancement 1: Reducing Fees

By moving from high-fee mutual funds or similar vehicles to low-cost ETFs (exchange-traded funds), Vettese explains how investment fees can be cut from 1.5 to 3% to as little as 0.5% a year, all of which goes directly to boosting retirement income flows. One of his takeaways is that “Tangible evidence of added value from active management is hard to find.”

2.) Enhancement 2: Deferring CPP Pension

We’ve covered the topic of deferring CPP to age 70 frequently in various articles, some of which can be found here on the Hub’s search engine. Even so, very few Canadians opt to wait till age 70 to collect the Canada Pension Plan. Because CPP is a valuable inflation-indexed guaranteed for life instrument — in effect, an annuity that you can never outlive — Vettese argues for deferral, although he (like me) is fine with taking Old Age Security as soon as it’s available at age 65. He argues that for someone who contributed to CPP until age 65, they can boost their CPP income by almost 50% by waiting till 70 to collect. “You are essentially transferring some of your investment risk and longevity risk back to the government, and you are doing so at zero cost.” Continue Reading…

My latest Financial Post column looks at a CIBC survey released Thursday that finds on average individual Canadians believe they’ll need $756,000 in order to retire.

Of course, most fall woefully short because they haven’t even crafted a financial plan to get there. And you know the old sayings, “Failing to plan is planning to fail,” or “If you don’t know where you’re going you’ll probably end up somewhere else.”

Considering that on average Canadians hope to retire by age 63, the fact that almost one in five haven’t even begun to even think about retirement suggests a bit of a disconnect. And women are consistently more behind in their retirement planning preparations than men. That’s a problem, considering that women have longer life expectancies and their money will therefore have to last longer.

Depending on aspirations, the “Number” can range from Zero to $2 million

\While the CIBC study looks at individuals rather than couples, the column quotes regular Hub guest blogger Marie Engen, who described three levels of retirement — basic, average and deluxe — in this 2016 blog: How much do you REALLY need to retire? (The original blog ran on the Boomer & Echo site late in 2015.) Some with modest needs can save nothing and subsist on the $38,000 senior couples can get from CPP and OAS. Continue Reading…

Doug Dahmer, CEO and founder of www.RetirementNavigator.ca has been a regular guest contributor to the Hub since its inception in November 2014. His focus is on Canada Pension Plan optimization, avoidance of retirement tax traps, and the creation of drawdown strategies during the decumulation side of financial planning. Some of these ideas have been used (with proper attribution) in various columns I’ve written in other media outlets, generally summarized here at the Hub.

However, Dahmer has been noticeably quiet lately. This blog explains why.

As the headline says and the adjacent image suggests, Doug is about to turn financial planning on its head. How? By democratizing access to financial planning, in the same way that Robo-Advisors democratized investing. This disruption of the planning industry is built upon a new planning platform called Better Money Choices.

Asked what motivated him to launch this venture Dahmer said more than 70% of Canadians say their greatest worries in life are centred around their financial futures. “Yet at the same time it is estimated that fewer than 15% of Canadians have a formal financial plan in place.”

As he talked to clients about this disconnect — why they resisted the idea of financial planning as an Rx to their financial stress — he discovered most people have no idea what true financial planning looks like.

Doug Dahmer, creator of BetterMoneyChoices.com

“The financial services industry has twisted the planning process into a tedious, time-consuming, onerous task that’s heavily biased toward the sale of financial products. What they hated most about planning, is that, more often than not, the conclusion to the process was always the same: spend less, save more, work longer, work harder. These recommendations were made while providing little in the way of understanding of the specific rewards these sacrifices would deliver.”

In short, Planning did not relieve their level of stress, it actually increased it!

Money doesn’t buy stuff, it buys choices

True planning was never meant to promote the sale of financial products. It’s supposed to be a process that allows you to explore the lifestyle choices you are thinking about, so you can discover their future financial implications before you need to commit to them. “Armed with this insight, you can then decide whether you’re willing to make the necessary sacrifices to bring them to fruition.”

Your most valuable asset isn’t money. It’s Time — and how you choose to spend it

Dahmer’s financial planning philosophy is based on the belief our lives are defined by the choices we make: the more good choices we make, the better our lives will be. His new site, BetterMoneyChoices.com, lets people quickly, easily and securely explore their lifestyle choices so they can better determine what outcomes they should focus on.

Everyone’s personal resources – time, money, energy, relationships and talents – are limited in some way. That forces each of us to make choices to accept less of one thing in order to obtain more of the things that are most important to us. However, seldom is “more money” what we are seeking.

It’s time the financial planning sector evolved with the times

Dahmer says technology has given us many low cost/no-cost, self-serve tools that make almost all aspects of our lives easier, but not yet financial planning. “My mission is to change this. By putting the focus on how you want to live your life instead of how much money you can accumulate, and making it easy for you to determine which set of choices will bring you closer to what you value most, the technology behind the Better Money Choices process will revolutionize planning.”

His goal is to make it a quick, easy and engaging process to determine the trajectory our lives are tracking. “I want to convert the misnomers that planning is an event that translates into an exact science to the reality that planning is an ongoing, never ending process of making a set of best guesses – projecting those best guesses into the future – then re-engaging with life to learn more.”

Such a process requires frequently returning to our ever-living planning platform to check our progress and improve upon our guesses. “Once people understand what true planning looks like and the huge benefits that can accrue by adopting this approach for directing them to better choices, their disdain for planning will finally disappear and they will rely on their planning tools with the same natural inclination they reach for their google maps when it comes time to choose how best to arrive at their desired destination.”

Exact pricing has yet to be determined, but Dahmer’s goal is to have a monthly subscription that is comparable to Netflix or Spotify.

Beta Testing

Dahmer is currently running a beta test to get user feedback, prior to it being released publicly (currently scheduled for April 1st, 2018, coincidentally a week before I myself turn 65).

Doug has asked me to participate as one of the early beta testers and I have agreed to do so. In the past week, I have been “playing” with the software with our own personal data and I can tell you already it’s an eye opener. Over the next few weeks on the Hub, I’ll report back to you on my experiences with the software and the impact this novel approach to planning has had on my own plans for the second half of my life.

After all, I’m hardly unique in turning 65 this year: some 1,100 other Canadians now do so each day. (Incidentally, I’ll be collecting my first Old Age Security cheque late in May but, as per the guidance of Doug and his new software, I’ve elected to wait until age 70 to collect the Canada Pension Plan. This too has been reported in my columns in the country’s two major daily newspapers or MoneySense.ca )

If you’d like to be one of the first to know when the site officially launches, you can sign up at www.BetterMoneyChoices.com.

Vanguard Investments Canada Inc. has announced the listing of three new low-cost Asset Allocation ETFs that give investors one-stop shopping to the firm’s globally diversified strategies. They began trading on the TSX today (February 1, 2018.)

Both investors and advisors are asking for “simple yet sophisticated single-ticket investment solutions that provide well-diversified global equity and bond exposure within a low-cost ETF structure,” says Atul Tiwari, managing director for Vanguard Canada. The new ETFs offer investors three different risk profiles and regular rebalancing.

In effect, each ETF is a fund of funds although Vanguard describes them as having an “ETF of ETFs structure.” Each holds seven existing core Vanguard index ETFs (which I list in the postscript below). Each new ETF of ETFs has a management Fee of 0.22%. Vanguard says that when one of its ETFs invests in underlying Vanguard funds, “there shall be no duplication of management fees.” Spokesman Matthew Gierasimczuk said “There are no duplicate fees beyond the 0.22 management fee, other than a basis point or two for operating expense and the trading fee for buying or selling the ETF.”

The three asset allocation ETFs cover the normal range from Conservative to Balanced to Growth, as reflected in the product names. Equity weights range from 40% for the Conservative offering, to 60% for the Balanced and 80% for the Growth.

Here are the 3 ETFs and their ticker symbols on the TSX:

Vanguard Conservative ETF Portfolio (VCNS) seeks to provide a combination of income and moderate long-term capital growth by investing in equity and fixed income securities with a strategic allocation of 40% equities and 60% fixed income.

Vanguard Balanced ETF Portfolio (VBAL) will provide long-term capital growth with a moderate level of income split 60% equities to 40% fixed income.

Vanguard Growth ETF Portfolio (VGRO) provides long-term capital growth by investing in equity and fixed income securities with 80% equities and 20% fixed income.

In a press release, Vanguard Canada head of product Tim Huver said the ETFs offer “a simplified and scalable solution for financial advisors, and a one-stop globally-diversified and transparent option for investors … Investors can rely on Vanguard’s global investment experts to continuously assess their portfolio’s exposure and rebalance it back to its intended risk level.”

With the three new ETFs, Vanguard Canada now offers 36 ETFs, with C$14 billion in assets under management. Vanguard Investments Canada Inc. is a wholly owned indirect subsidiary of The Vanguard Group, Inc.