An Interac survey being released today finds that more than two thirds (69%) of Canada’s Gen Z generation [defined as Canadians aged 18 to 27] have embraced the mobile wallet, while almost as many (63%) would rather leave their old-fashioned physical wallets at home for short trips. Gen Z’s Interac contactless mobile purchases also rose 27% in the first half of 2024, compared to the same period a year earlier.

Gen Z appears to be more enthusiastic than their counterparts in older cohorts: 60% of Millennials [aged 28-43] embraced mobile wallets, compared to 44% of Gen Xers [aged 44-59] and just 27% of Baby Boomers [aged 60-78.] Only 10% of the older Silent Generation [age 79 or older] did so.

A whopping 63% of Gen Z mobile wallet users have loaded their Interac debit card on their smartphones, and 31% plan to set debit as their default method of payment. For 63% of them, the reason is perceived faster payment times compared to physical card payments.

“Choosing your default payment method may feel like a small step, but it can play a big role in shaping Canadians’ ongoing spending habits,” said Glenn Wolff, Group Head and Chief Client Officer, Interac in a press release. “When consumers tap to pay with their phones, the decision to select a card from the digital wallet is easy to miss. Canadians could end up unintentionally using a default payment method that prompts them to take on more debt. This differs from traditional physical wallets where the consumer had to select the card they wanted to use each time.”

Majority want to be smarter with money

62% of Gen Z want to be “more mindful when spending” with 57% saying they want the option to use debit when paying in store or online; 79% of them say the cost of living is too expensive and 59% feel the need to be smarter with their money.

Interact says this generation’s desire to control overspending is heightened by back-to-school season: last year, family clothing stores saw almost twice as many Interac Debit mobile purchases in September and October compared to earlier that year in January and February. 54% of Gen Zs see the need to develop new habits to stay in control over their finances, while 56% are setting a timeline for this September to introduce new habits. Continue Reading…

Darren Coleman (left) and Kim Moody (right, with glasses).

The following is an edited transcript of an interview conducted by financial advisor Darren Coleman’s of the Two Way Traffic podcast with tax expert Kim Moody, of Moody Private Client. It appeared on August 8th: click here for full link.

Moody recently wrote an article in the Financial Post about the government flirting with the idea of a home equity tax, even on principal residences. Such a tax could result in an annual levy of about $10,000 for a home worth $1 million. He described that, along with the increase in the capital gains inclusion rate that has already passed into law, “really bad tax planning” based on ideology, not economics.

In the podcast Moody and Coleman also discussed …

The disparity between U.S. and Canadian tax rates, beginning with how the state of Florida compares with Ontario, a difference of 17%.

The tax model established in Estonia lets you reinvest in your company without paying corporate tax while personal income is taxed at a flat rate of 20%. They say such a system would work in Canada, and celebrate success and entrepreneurship.

What organizations like the Fraser Institute and mainstream economists think about Canada’s economic performance.

Below we publish an edited transcript of the start of the interview, focusing on the capital gains inclusion rate and trial balloon about taxing home equity.

Darren Coleman, Raymond James

Darren Coleman: I’m Darren Coleman, Senior Portfolio Manager with Raymond James in Toronto. I’m delighted to be joined by Kim Moody of Moody’s tax and Moody’s private client. You’re also a law firm based in Calgary, Alberta, and probably one of Canada’s best known tax and estate planning advisors. You may have heard our last conversation with Trevor Perry about some of the issues we might be seeing in terms of taxation of the principal residence in Canada.

I think because governments have spent so much money that we’re going to see tremendous innovation in taxation. Do you want to set the table for the article you wrote in the Financial Post, where you talked about where this is coming from, and why Canadians might be on alert for what might be coming to tax the equity in their homes.

Kim Moody: The point of the piece was mainly just to put Canadians on notice that you had the Prime Minister and the finance minister sitting down with what I call a pretty radical

think tank. I consider them an ideological bastion of radical thought but that issue aside,

they call them call themselves a think tank, and this particular one, led by Paul Kershaw of

Generation Squeeze, has stuff on their website that pretty much attacks older Canadians:

basically saying they’ve gotten rich by going to sleep and watching TV. Unbelievable. Whoever approved that, it’s just so offensive. But that issue aside, the whole connotation of the messaging is that, hey, these people are rich. We’ve got these poor young Canadians who are not rich and they can’t afford houses because you’re rich and …

Darren Coleman Someone should do something about it, right? That’s the trick.

Kim Moody

Kim Moody: Someone should do something about it. And their solution is to introduce a so-called Home Equity tax on any equity of a million dollars or more. And they call it a modest surtax of 1% per year. So it’s like another, effectively property tax … It’s just so nonsensical and so offensive on a whole bunch of different levels. Like you think about grandma and grandpa, yeah, they’ve got equity in their homes, but they don’t have a lot of cash. They’ve been working hard their entire lives to pay off their houses. And yes, they want to transfer down to their kids at some point, but right now, they’re living again, and they’re making ends meet by living off their pensions that they worked hard, and you’re expecting them to shell out more money for that, and I find that offensive.

…. Back to the original premise of why I wrote the article: to let Canadians know that our leaders are entertaining stuff like this. It doesn’t mean they’re going to implement it, but they’re actually entertaining radical organizations like this and secondly, just to put Canadians on

notice that this is just the beginning. If this regime continues with out-of-control spending and no

adherence to basic economics, then we could expect a whole bevy of new taxes.

Darren Coleman

Indeed, they’ve already done some of this, right? So you know that this idea about we’re going to tax home equity, either through some kind of annual surtax on equity over a certain amount, or we’re going to put a capital gain on principal residences. And I would argue that for years now, Canadians have had to report the sale of the principal residence on their tax returns, which is a non-taxable event, yet you now have to tell them, and if you don’t, there’s a penalty. Continue Reading…

I start with Die with Zero because it most directly deals with the topic of money as we age. In fact, as most retirees know, one of the biggest fears behind the whole retirement saving concept is running out of money before you run out of life.

But it appears that many of us have become so fixated with saving for retirement, we may end up wasting much of our precious life energy, and being the proverbial richest inhabitant of the cemetery. For you super savers out there, this book may be an eye opener, as is the other book, 4,000 Weeks.

As I note in the column, this genre of personal finance started with Die Broke, by Stephen Pollan and Mark Levine, which I read shortly after it was first published in 1998. That’s where I encountered the amusing quip that “The last check you write should be to your undertaker … and it should bounce.”

The premise is similar in both books: there are trade-offs between time, money and health. Indeed, as you can see from the cover shot above, its subtitle is Getting all you can from your money and your life. As with another influential book, Your Money or Your Life, we exchange our time and life energy for money, which can therefore be viewed as a form of stored life energy. So if you die with lots of money, you’ve in effect “wasted” some of your precious life energy. Similarly, if you encounter mobility issues or other afflictions in your 70s or 80s, you may not be able to travel and engage in many activities that you may have thought you had been “saving up” for.

A treatise on Life’s Brevity and appreciating the moment

Amazon.com

The companion book is Four Thousand Weeks : Time Management for Mortals, by Oliver Burkeman. If you haven’t already guessed, 4,000 weeks is roughly the number of weeks someone will live if they reach age 77 [77 years multiplied by 52 equals 4,004.] Even the oldest person on record, Jeanne Calment, lived only 6,400 weeks, having died at age 122.

I actually enjoyed this book more than Die with Zero. It’s more philosophical and amusing in spots. Some of the more intriguing chapters are “Becoming a better procrastinator” and “Cosmic Insignificance Therapy.” I underlined way too many passages to flag here but here’s a sample from the former chapter: “The core challenge of managing our limited time isn’t about how to get everything done – that’s never going to happen – but how to decide most wisely what not to do … we need to learn to get better at procrastinating.”

Added Note on July 4, 2024, America’s Independence Day

American stock markets are closed today for Independence Day. I wish all Americans a happy holiday.

This blog originally ran in February but in light of the momentous events of the past week, we’re republishing and updating it. In fact, emotions have been so raw the last week that some corners of the web fret that July 4, 2024 may turn out to be the last Independence Day.

I doubt that but the events since last Thursday certainly have grabbed the world’s attention, as well as Canada’s: as ever, when the elephant south of the border sneezes, we in the great white north catch a cold.

Those new developments are of course President Biden’s disastrous debate last Thursday, June 27th, and then this week’s equally dismaying Supreme Court ruling (on July 1) to grant the Former Guy immunity for any official acts while he was president.

If Democracy seemed on shaky footing back in February, it seems doubly so today, roughly four months from the November election. But that’s still enough time to read the four books highlighted in this blog, and perhaps act on them.

Back to the original text in the blog, which has also been revised and updated where appropriate:

While Findependence Hub’s focus is primarily on investing, personal finance and Retirement, Findependence has given me sufficient leisure time to absorb a lot of content on politics and the ongoing battle to preserve democracy and in particular American democracy. What’s the point of achieving Financial Independence for oneself and one’s family, if you find yourself suddenly living in a fascist autocracy?

To that end, I have recently read four excellent books that summarize where we are, where we have come from and where we likely may be going. (Note, this blog is an update of what I wrote in late November, but with two books added.)

In contrast to two of the books mentioned below, Heather Cox Richardson’s Democracy Awakening is disturbingly current and explicitly names names. There is an extensive recap of The Former Guy’s attempt to highjack the 2020 election and the subsequent event of January 6th and everything that has occurred since.

Yes, I’m sick of reading about him too, which is why I don’t even name him here (even on social media accounts I prefer to use 45). But after his deranged Thanksgiving rant and an equally insane Christmas greeting on the soon-to-be defunct Truth Social (aka Pravda Social), his behaviour has become nothing short of alarming.

On other words, what may have seemed alarmist warnings in these books six months ago now seem scarily more relevant and likely to pass. So what do these books actually say about past dictatorships of history and the possibility of another one coming to pass in the not-too-distant future?

Reclaiming America

Richardson is a history professor at Boston College. For Canadians in particular the book is a valuable primer on the founding of America, the Declaration of Independence, the civil war, the Constitution and its many amendments, the creation of the Democratic and Republican parties, and the politics of the last few centuries. I assume most well-read American readers are taught this in grade school (although maybe not, judging by the millions of deluded MAGA zealots.)

The book itself is divided into three main parts: Undermining Democracy, The Authoritarian Experiment, and Reclaiming America.

Richardson make frequent references to Adolf Hitler and the Nazis. As she writes in the foreword:

“Hitler’s rise to absolute power began with his consolidation of political influence to win 36.8 percent of the vote in 1932, which he parlayed into a deal to become German chancellor. The absolute dictatorship came afterward. Democracies die more often through the ballot box than at gunpoint.”

She goes on to write that a small group of people “have made war on American democracy,” leading the country “toward authoritarianism by creating a disaffected population and promising to re-create an imagined past where those people could feel important again.” In other words, MAGA.

I’ll skip to the ending but again urge readers to get a copy and read everything between these snippets:

“Once again, we are at a time of testing. How it comes out rests, as it always has, in our own hands.”

Amazon.ca

Hitler: Ascent 1889-1939

Even since I wrote the original version of this blog in November, the press has been full of alarming reports of 45’s Hitler-like rhetoric early in 2024: famously his references to vermin and to immigrants poisoning the blood of the American people, both from the original Hitler playbook. And who can forget his “dictator only on the first day,” an alarming recent example of many a truth said in jest?

A two-book series by Volker Ullrich looks first at Hitler’s political rise and then to his decline and defeat in the second World War that he created.The second book is titled Hitler: Downfall: 1939-1945.

While most of us may think we know this history going back to high-school history classes, not to mention numerous histories, novels and films about World War II, Hitler: Ascent is nevertheless a bracing refresher course.

Ullrich charts Hitler’s improbable rise from failed artist to political rabble rouser, to his failed beerhall putsch in the 1920s, his writing of Mein Kampf after a too-short prison sentence and ultimately his stunning January 1933 manoeuvre to become the Chancellor of Germany, which he soon consolidated as combined chancellor/president and ultimately the dictator he is now known to be.

The book also makes clear his goals for creating a Greater Germany at the expense of most of his European neighbours (famously Poland and France), and his plans for impossibly grandiose architectural structures to be implemented by Albert Speer, with Berlin (to be renamed Germania) the centre of what he hoped would be a global dictatorship.

The second Ullrich book — Hitler: Downfall, 1939-1945 — is also well worth reading. The final sentences are particularly relevant to today’s environment:

If Hitler’s “life and career teaches us anything, it is how quickly democracy can be prised from its hinges when political institutions fail and civilizing forces in society are too weak to combat the lure of authoritarianism; how thin the mantle separating civilization and barbarism actually is; and what human beings are capable of when the rule of law and ethical norms are suspended and some people are granted unlimited power over the lives of others.”

Of course, for most of us, reading yet another book (or two) about Adolf Hitler doesn’t usually create undue anxiety, since it all seems to be comfortably in the faraway past. Ancient history, as they say. Continue Reading…

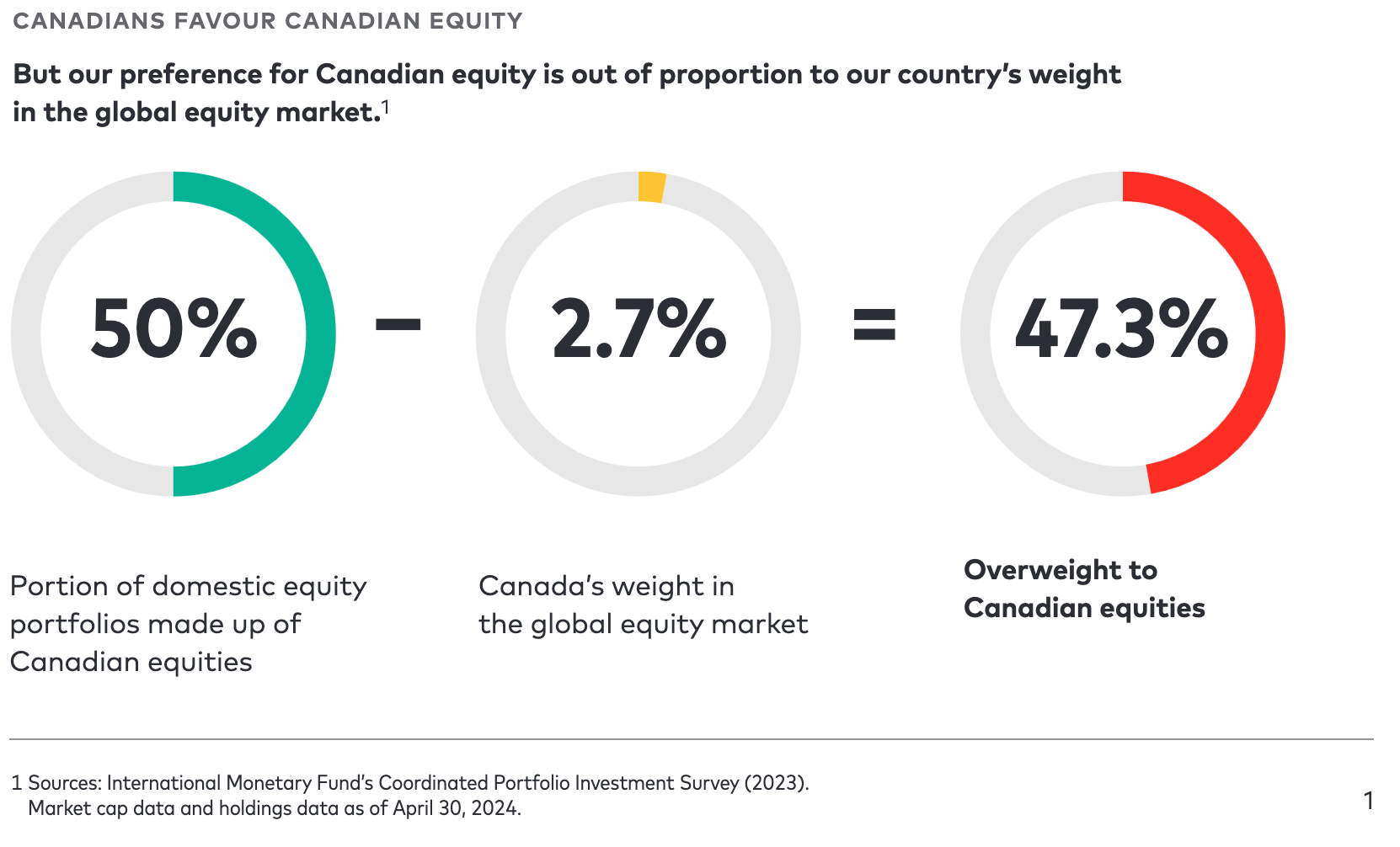

A just-released study from Vanguard Canada on Home Country Bias shows that Canadians have about 50% of their portfolios allocated to Canadian equities: well beyond what is recommended for a country that makes up less than 3% of the global stock market.

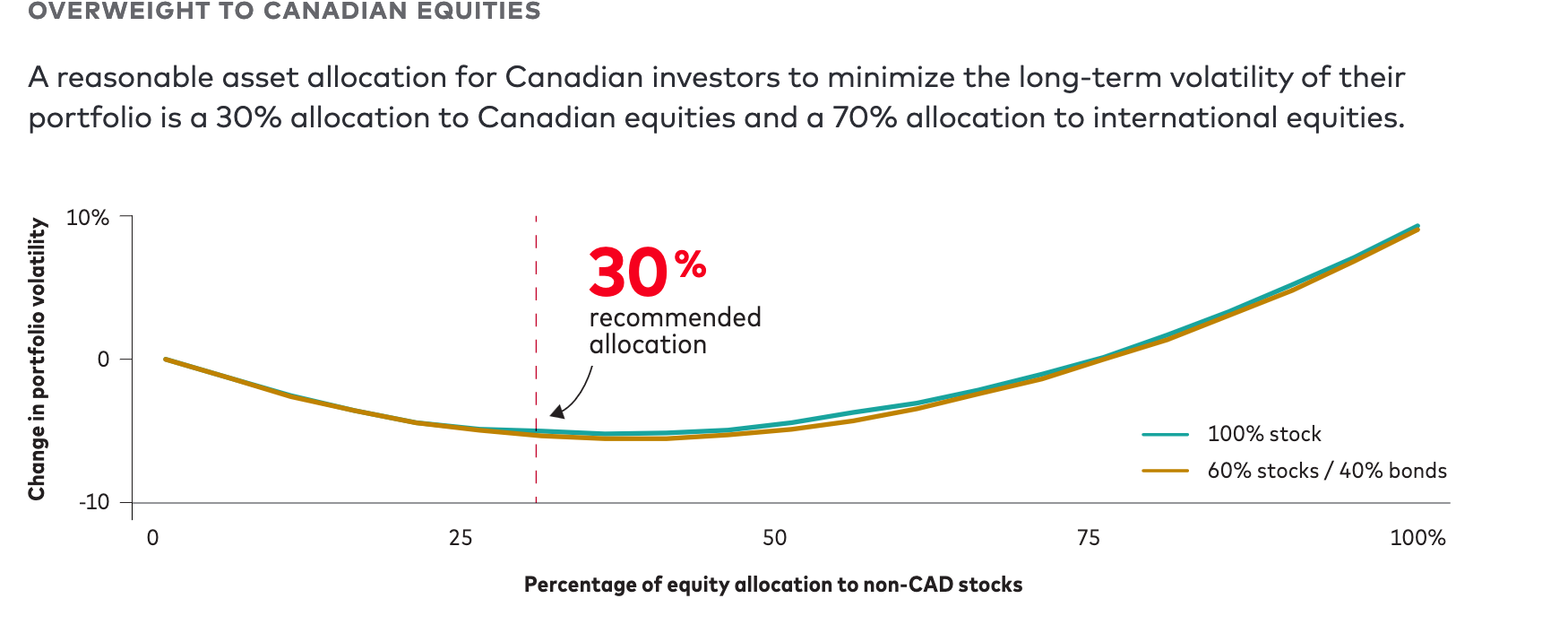

As the chart below shows, Vanguard recommends just 30% in Canadian stocks but notes that the domestic overweight is slowly decreasing as investors move to global and U.S. equities.

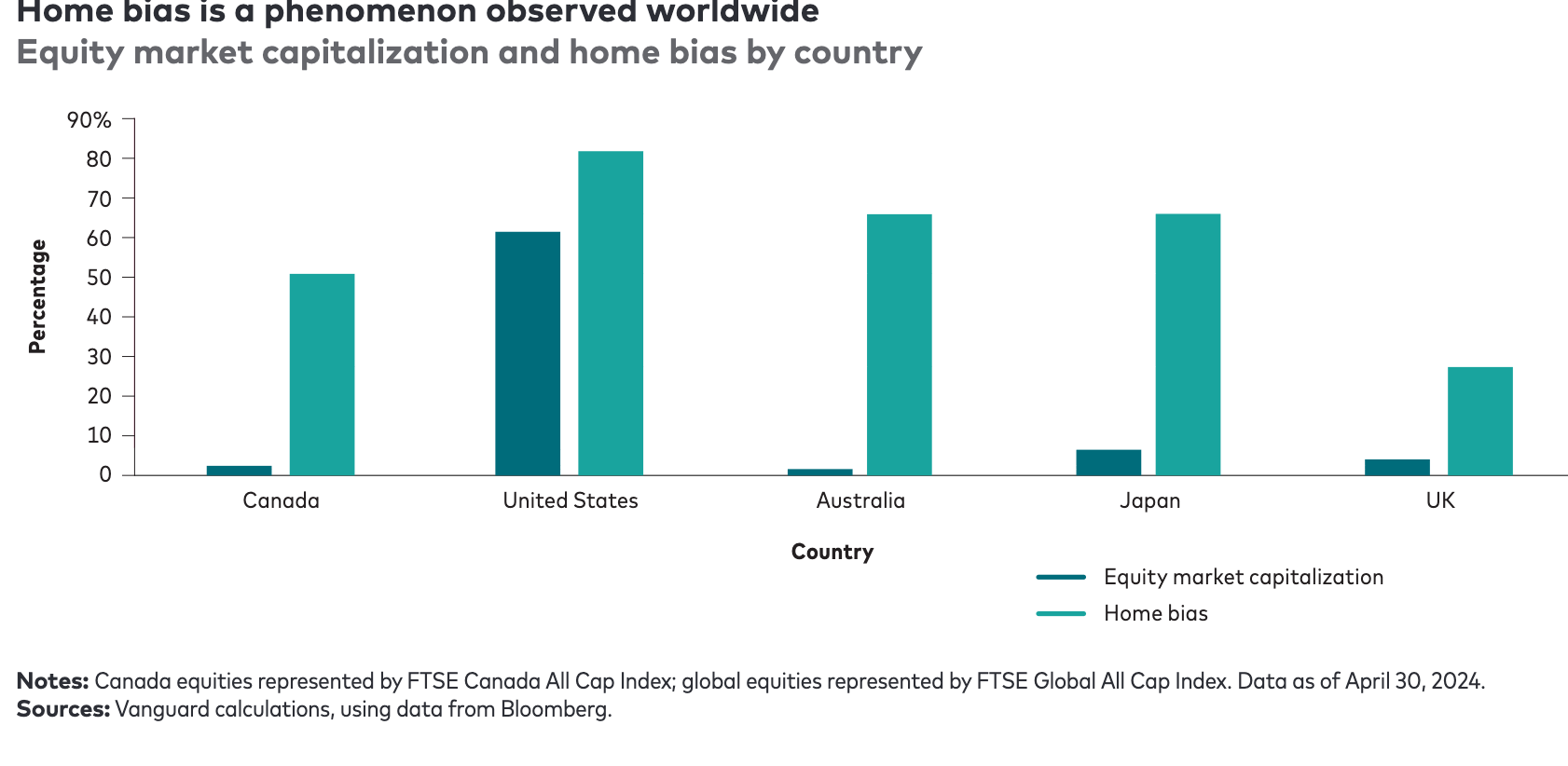

Vanguard says home country bias is not unique to Canada: Americans behave similarly with respect to the U.S. stock market. But as you can see from the chart below, because the U.S. makes up more than half of the global stock market by market capitalization, the gap between its relative overweighting is far less dramatic than in Canada. Canada’s home country bias is almost as pronounced as in Australia (a similar market to Canada in terms of resources and financial stocks), and Japan is not far behind.

However,Vanguard adds, “overall, Canadians and investors in other developed countries are trending towards a greater appetite for diversification through global equities.”

Too much Canada can be volatile

So what’s wrong with having too much Canadian content (both stocks and bonds)? Vanguard says portfolios overweight Canadian equity can be volatile because the domestic market is too concentrated in just a few economic sectors. “Relative to the global market, Canada’s market is concentrated within a few large names. It is also significantly overweight in the energy, financials and materials sectors, and significantly underweight in others.” Continue Reading…