By Dale Roberts, CutTheCrap Investing

Special to the Financial Independence Hub

Data shows that Canadians continue to embrace low-cost ETFs. That said, more monies continue to flow into high-fee mutual funds. As you likely know, Canadians pay the highest mutual fund fees in the developed world. Of course, those high fees are wealth destroyers and can eat up 50% of your investment returns over the decades.

But here’s the good news: more Canadians are moving more monies to low-cost ETF portfolios by the way of self-directing or through Canadian Robo Advisors or by way of those One Ticket Asset Allocation Portfolios.

Here’s a look at the flow comparisons for Mutual Funds and ETFs courtesy of the IFIC site:

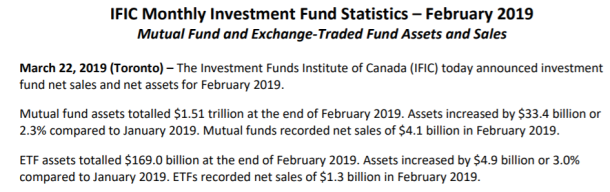

Here’s the sales figures for mutual funds in what we would typically call the usually robust RRSP season, January and February:

And here’s the sales figures for the ETF industry for RRSP season:

And here’s the sales figures for the ETF industry for RRSP season:

If we want to be optimists, that is more than promising. While 2019 was a soft RRSP season for money flows into mutual funds and ETFs (compared to 2018 figures) there was an acceleration of flows to ETFs compared to mutual funds, year over year.

- In 2019 35% of new monies went to ETFs.

- In 2018 27% of new monies went to ETFs

That is certainly something to celebrate. While the total mutual fund industry is almost 10 times the size of the ETF industry, they did not even double the size of inflows for January and February of 2019. That aligns with the findings of Nest Wealth, which conducted a poll in RRSP season. Respondents suggested one third of all new account openings would be by way of one of the Canadian Robo Advisors: also known as digital wealth managers. For more on that please have a read of There will be a tipping point for ‘Robo Advisors’ suggests Randy Cass of Nest Wealth. Keep in mind the poll was reading account openings, not the move of assets or amounts of assets.

Here’s another way to frame that more than ‘good news’.

- In 2019 $1.8 billion more went to mutual funds compared to ETFs

- In 2018 $7.74 billion more went to mutual funds compared to ETFs

In what year will more monies go to ETFs over mutual funds?

I don’t even want to guess. I don’t mind being wrong (which I would be), but I also don’t want to get my hopes up. The simple projections based on current trends might suggest several years. But if we get more acceptance and awareness we might get a nice surprise and see more monies flow into ETFs within 5 years or so. And in the self-serving attempt to not get left behind, many of the bigger banks might make the move to providing lower cost options that includes ETFs and ETF One Ticket Solutions and perhaps more low-cost index-based funds. We’ve seen RBC team up with iShares, the world’s largest ETF provider by assets under management. And of course the number 2 ETF provider in Canada is BMO. RBC is a profit monster and many in the industry will suggest that RBC is Canada’s best-run bank. They might be the smartest bankers in the room. They know that ‘something is up.’ The high-fee cat is out of the bag.

What will cause the tipping point?

Put it this way, the big banks and mutual fund companies did not get out in front and do what’s right for investors. They will have it thrust upon them. When more monies starts to flow to ETFs it’s likely all over but the crying. Canadian investors, en masse, will likely wake up to the new reality that there is a better way to invest. RBC likely knows that if you’re not already in the game in a meaningful way, the train will leave without you. There are some banks and well-known wealth managers who are about to get left behind.

TD might have to pull their e-series funds out of the closet, ha. But that will be too little, too late. Many of the high-fee dinosaurs are scrambling already.

For Globe and Mail subscribers, here’s a link to that surprising article and take on mutual fund industry trends and the attempt to adapt to the new realities.

And keep in mind that not all mutual fund providers are bad (just most). I am a big fan of index-based portfolios are mutual funds. I am a big fan of Steadyhand, Mawer Investments, Leith Wheeler and of course, Tangerine Investments ’index-based portfolios are mutual funds.

Dale Roberts is the Chief Disruptor at cutthecrapinvesting.com. A former ad guy and investment advisor, Dale now helps Canadians say goodbye to paying some of the highest investment fees in the world. This blog originally appeared on Dale’s site on April 2, 2019 and is republished on the Hub with his permission.

Dale Roberts is the Chief Disruptor at cutthecrapinvesting.com. A former ad guy and investment advisor, Dale now helps Canadians say goodbye to paying some of the highest investment fees in the world. This blog originally appeared on Dale’s site on April 2, 2019 and is republished on the Hub with his permission.

I retired last year and turned my retirement funds over to RBC. They have put the money into their managed fund series of funds which are funds of funds. The prospectus booklet indicated that the MER of these funds is maximum 0.2%. However they have tacked on another almost full percentage point for overall fee of 1.17%. Do you think this is excessive for portfolio of >$1,000,000. When I asked for reduction of fees they said no.