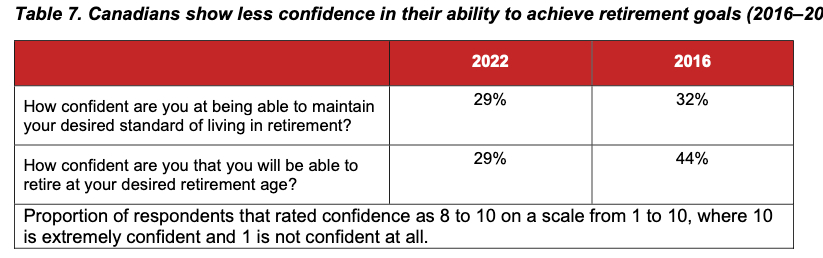

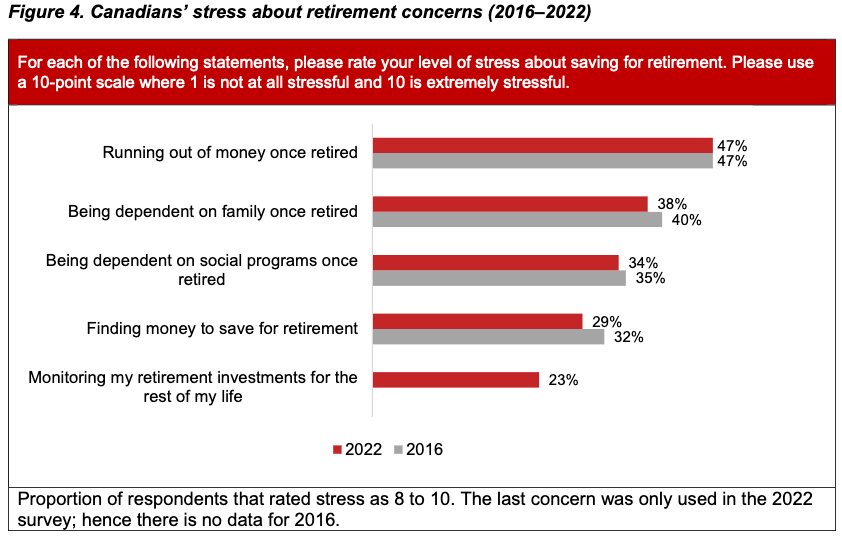

Canadians have lost confidence in their ability to retire on time and debt-free, according to a new report by the Canadian Public Pension Leadership Council (CPPLC). As a result, almost half of those polled by Pollara Strategic Insights are stressed about the prospect of running out of money in Retirement, as the graphic from the report illustrates below:

Canadians have lost confidence in their ability to retire on time and debt-free, according to a new report by the Canadian Public Pension Leadership Council (CPPLC). As a result, almost half of those polled by Pollara Strategic Insights are stressed about the prospect of running out of money in Retirement, as the graphic from the report illustrates below:

You can find the full report, which runs roughly 40 pages, by clicking on its highlighted title here: The Pensions Canadians Want: Perceptions of Retirement (2016–2022).

A press release issued Monday says the report comes from a Canada-wide survey conducted in 2022 similar to an earlier survey by the CPPLC on retirement perceptions prepared in 2016.

An introduction recaps the three major pillars of the Canadian retirement income system: government-sponsored CPP/OAS/GIS; Workplace Retirement Plans and Personal Savings (primarily RRSPs/TFSAs/non-registered savings).

However, a minority of Canadians currently have access to the workplace pension plans of Pillar 2: only 39.7% as of 2021, according to Statistics Canada. Worse, Pillar 3 savings are not making up for that gap: the report cites a Bank of Montreal finding that the average RRSP account balance is $144,613. That is not enough to fund an average yearly spending level of $64,000 (2019 average) over a retirement that may last 20 or 30 years. It also finds that not everyone is using TFSAs: those who do tend to older and married, with higher incomes and education.

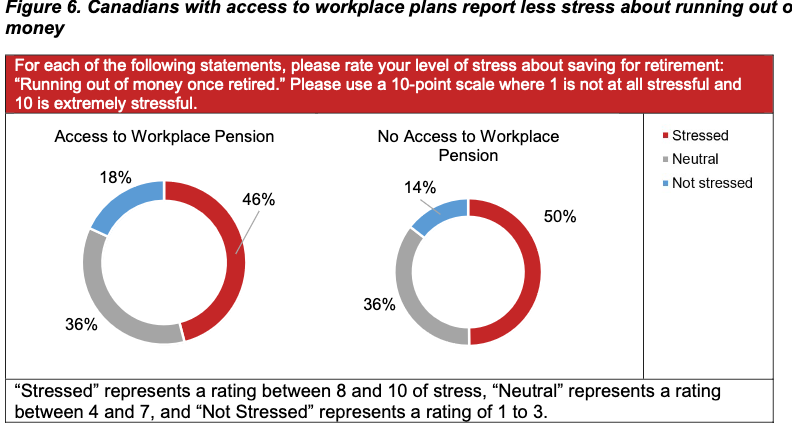

As you can see from the graphic on the right, those with Employer Pensions (especially classic Defined Benefit plans) experience somewhat less stress than those who do not. (Actually, I’m surprised the gap isn’t wider!).

As you can see from the graphic on the right, those with Employer Pensions (especially classic Defined Benefit plans) experience somewhat less stress than those who do not. (Actually, I’m surprised the gap isn’t wider!).

As you might expect, given that they tend to live longer, women are more stressed than men about running out of money: a majority (53%) are stressed about running out of money once retired, compared to 41% of men.

Women also report more uncertainty about managing retirement savings themselves. And they rate the importance of maintaining standard of living higher than men, as shown in the graphic below:

Four key Observations

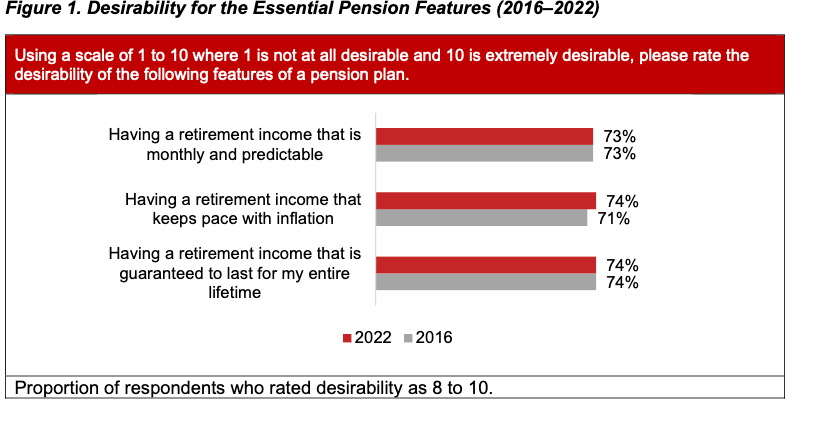

1.) Canadians consistently show preferences for predictable, inflation-adjusted, and lifetime

guaranteed retirement income

2.) Canadians continue to place importance on maintaining their standard of living in retirement

3.) Fewer Canadians are confident about managing their savings or that they will reach their

objectives and retire when they want

4.) Canadians are less confident they will be debt free in retirement and continue to report low

knowledge of retirement income sources

Three major recommendations

1.) Increase access to collective plans: leverage homegrown expertise to increase participation in

workplace pension plans by encouraging the growth of sector- and broader-based public sector

plans.

2.) Make it easier to provide pension plans for every Canadian: Apply lessons learned from other

countries to improve participation in workplace pension plans, promote existing Canadian

products, and ensure they cover those without traditional employment relationships.

3.) Empower innovation to improve access to lifetime income: support the implementation of new

products that will provide Canadians with simple and cost-effective options for turning

accumulated savings into a lifetime income stream.