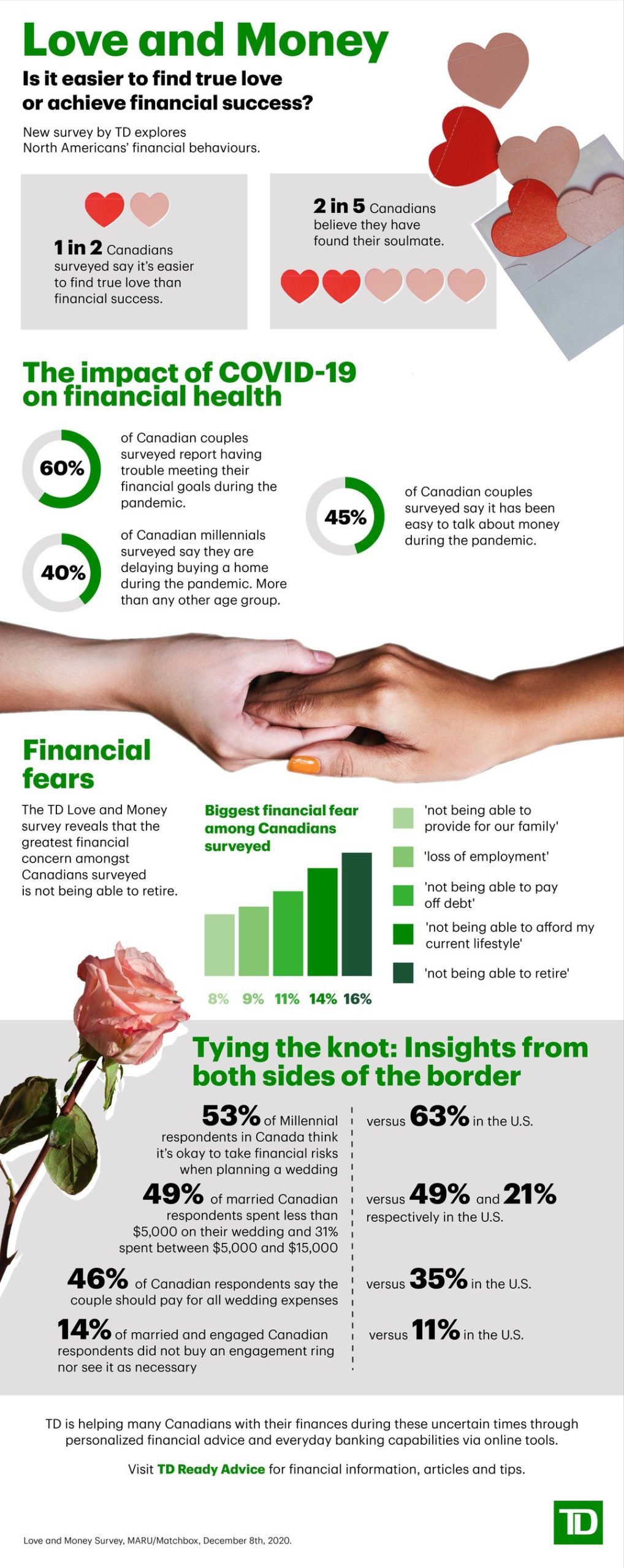

According to Love and Money – a survey from TD exploring the financial behaviours of more than 3,000 married, in-a-relationship or divorced North Americans – half of Canadians surveyed (49%) believe it’s easier to find true love than financial success.

However, that’s not to say those Canadian couples surveyed aren’t feeling cautiously optimistic about their future financial goals.

Despite challenges from the pandemic, nearly nine in ten (88%) respondents are currently saving for something. For those already in committed relationships, the survey also reveals that for most couples (45%) it has been easy to talk about money during COVID-19.

Nearly half (49%) say the pandemic has led to more open and constructive conversations about their finances, including the need to adjust spending habits by reducing spending on non-essential items (62%) and delaying larger purchases (36%).

With Love and Money revealing that six out of ten (60%) couples surveyed are having trouble meeting their financial goals during the COVID pandemic, it’s clear that having conversations about money are critical. In fact, “not talking about money with my partner on a regular basis” is the top financial mistake noted amongst Canadian respondents.

Fortunately:

- 77% of Canadian couples surveyed say they typically open up about their finances within the first year of their relationship: including 56% who get very candid within the first six months.

- Among Canadian married couples and those in a committed relationship, 85% say they talk about money every month.

But even though it seems most Canadians aren’t shying away from the (financial) “talk,” the TD Love and Money survey also shows that some Canadian respondents may be more likely to ask for forgiveness than permission.

- Among the 8% of who admit to keeping financial secrets from their partner, 62% don’t ever plan to disclose them. Canadian couples surveyed admit to hiding a secret bank account (29%) or significant credit-card debt (22%).

- Only 53% of Canadian Millennials say they agree with their partner on what expenses constitute a ‘want’ or a ‘need’.

- 81% of Millennials admit to making unreasonable financial decisions, and one quarter (25%) say excessive and frivolous spending was one of them.

Tying the knot: Insights from both sides of the border

As expected, walking down the aisle looks very different during the pandemic, as many North American couples deal with the impact of lockdowns, gathering restrictions and reduced income. Consequently, Love and Money reveals that of the engaged Canadian couples surveyed whose wedding planning was impacted by the pandemic, more than half (56%) either postponed or downsized their nuptials.

When it comes to the big day, the TD survey also shows:

- 53% of Millennial respondents in Canada think it’s okay to take financial risks when planning a wedding, versus 63% in the U.S.

- 46% of Canadian respondents say the couple should pay for all wedding expenses, versus 35% in the U.S.

- 49% of married Canadian respondents spent less than $5,000 on their wedding and 31% spent between $5,000 and $15,000, versus 49% and 20% respectively in the U.S.

- 14% of married and engaged Canadians and 11% of their U.S. counterparts did not buy an engagement ring nor see it as necessary.

Biggest concern is not being able to retire

In terms of financial worries, the TD Love and Money survey also reveals that the greatest financial concern among Canadians is the fear of not being able to retire. Despite this concern, only one third (32%) of Canadians say they meet with a financial advisor on an annual basis. Continue Reading…