Happy New Year!

Below we canvas 11 retirement experts and financial planners in Canada and the United States about how they and their clients can use new Longevity insurance products above and beyond traditional life annuities.

These experts were gathered by Featured.com, which has been supplying Findependence Hub with quality content for several years. It recently changed its procedure so editors like myself can request input on particular topics we think will interest our readership. The sources are all on LinkedIn, as you can see by clicking on their profiles below.

Here’s what we asked for this instalment:

“In addition to Annuities, what is one new Longevity product or fund that you believe in enough to recommend to clients approaching or already in Retirement? Examples in Canada are Purpose Longevity Fund and Guardian’s Longevity Funds. Are there similar new products in the U.S. (or Canada) of which you are aware?”

Here is what these 11 thought leaders had to say:

In addition to traditional annuities, one of the emerging longevity products in the U.S. that I have come to recommend to clients approaching or already in retirement is the LifeX Longevity Income ETF, particularly the LFAI fund.

In addition to traditional annuities, one of the emerging longevity products in the U.S. that I have come to recommend to clients approaching or already in retirement is the LifeX Longevity Income ETF, particularly the LFAI fund.

While it is not a classic insurance product, it is designed to provide predictable monthly distributions over a long horizon, effectively hedging against the risk of outliving one’s assets. The fund invests primarily in U.S. Treasuries and money-market instruments, and its structure is built around the concept of a target cohort’s 100th birthday, which allows for a systematic income stream without relying on a life insurance company guarantee.

For many clients, especially those who purchased assets during low-interest periods or are seeking reliable cash flow without tying up their entire portfolio in an annuity, this product offers a compelling complement to their existing retirement income strategy. What I find particularly valuable is the transparency it provides. Unlike certain annuities, clients can clearly see the underlying investments, understand how distributions are generated, and retain the flexibility to adjust allocations as their personal circumstances or market conditions evolve.

It also fits naturally into a broader retirement strategy where a portion of assets remains growth-oriented, some is allocated to defensive income-generating investments, and a dedicated longevity-income segment addresses the specific risk of living decades beyond retirement.

Of course, it is not without considerations; while the fund aims to provide stable income, it is sensitive to interest-rate changes, inflation, and the assumptions built into its cohort-based design. Clients need to assess the fit carefully, ensuring the time horizon and income targets align with their health, lifestyle, and other holdings. For those who understand these dynamics, however, it offers a sophisticated and innovative approach to longevity planning, bridging the gap between traditional annuities and fully self-managed income portfolios, and giving retirees confidence that they can sustain their lifestyle even as they live longer than expected.

Andrew Izrailo, Senior Corporate and Fiduciary Manager, Astra Trust

If you’re getting close to retirement, you might want to check out the BlackRock LifePath Paycheck fund. I’ve been following it. It works like those Canadian longevity funds, designed to give you regular monthly checks. The biggest risk is outliving your savings, and this fund has professionals handle the withdrawals so you don’t run out of money. It seems to offer more flexibility than a traditional annuity, which is worth a look.

JP Moses, President & Director of Content Awesomely, Awesomely

——————————————-

The Vanguard Target Retirement Income Fund is not an entirely new “longevity” product in the mold of Canada’s Purpose and Guardian funds, but it fulfills a similar role for retirees. It is intended to deliver a steady flow of income while protecting against the effects of inflation by investing in a diversified blend of stocks, bonds and cash. The Fidelity Strategic Advisers (r) Core Income Fund is also designed to provide income for retirees with a diversified approach. The two funds both provide some level of stability for those who want to keep a lid on risk and market vomit in retirement.

Evan Tunis, President, Florida Healthcare Insurance

——————————————-

I’ve often been asked about newer longevity products beyond traditional annuities, especially by clients preparing for retirement who want flexibility without giving up stability. What I have observed while working with financially cautious founders and executives is that people want income structures that feel modern, transparent, and liquid, and one option in the U.S. that I genuinely find promising is the Stone Ridge LifeX Longevity Income ETFs. I first came across them while helping a client map out a long term retirement strategy, and what stood out was how these funds provide monthly distributions while still allowing investors to keep full liquidity. I remember reviewing the structure and appreciating how it focuses on Treasuries and a long horizon rather than tying someone into an insurance contract. It felt refreshing. many retirees dislike the idea of locking up money permanently, and this approach allowed them to protect their cash while still receiving consistent income. The experience reminded me of moments with founders who want efficiency without losing control, and pattern is similar

In my opinion, the biggest advantage of these longevity ETFs is the balance between predictability and freedom, since investors receive monthly payouts but can still adjust their strategy if life takes an unexpected turn. The main drawback is that there is no lifetime guarantee, so someone who ends up living much longer than expected might outlive the structure if they rely on it too heavily. I often explain that longevity planning still requires layering different tools rather than expecting one product to solve everything. Another point that came up during discussions with retirees is the sensitivity to interest rate changes, which can affect the value of the ETF itself, and it is important not to overlook that risk. Still, for clients who want something more adaptable than an annuity, this has become a strong option to consider. I also pay attention to emerging pooled longevity concepts, similar to modern tontine ideas, which share risk across participants and create higher payouts for those who live longer. Even though these structures are not mainstream in the U.S. yet, the logic is compelling for retirees who expect longer than average lifespans. Whenever I see innovation like this, I feel the same excitement I do when a founder shows us a new model at spectup because it signals that the industry is shifting toward more transparent, flexible solutions.

Niclas Schlopsna, Managing Partner, spectup

——————————————-

When I think about longevity-focused options beyond traditional annuities, one U.S. product I genuinely find compelling is the Stone Ridge LifeX Longevity Income ETFs. What draws me to LifeX is that it tries to solve the same problem that Canadian funds like Purpose Longevity and Guardian Longevity address — steady income over an unknown lifespan — but without locking someone into an irreversible insurance contract.

Instead of handing over capital permanently, retirees stay invested and receive structured monthly distributions, which feels more flexible and respectful of changing needs. I’ve always liked the idea of having income that mimics an annuity while still keeping the door open if health, family, or market circumstances shift.

I’ve come to see LifeX as especially appealing for clients who want predictable cash flow but aren’t comfortable giving up control of their assets. Because the funds are built largely on U.S. Treasuries, the income stream feels relatively stable, and the target-date structure helps align payouts with the later stages of retirement, when longevity risk becomes more real. The liquidity alone makes it feel like a meaningful evolution in retirement planning: it’s easier to sleep at night knowing the money isn’t trapped.

Of course, I’m also realistic about its limitations. There’s no lifetime guarantee the way a true annuity offers, and the income still depends on market and interest-rate dynamics. It’s not a perfect replacement for insurance-based products. But as a complement — or even a middle ground between full guarantees and full market exposure — it’s one of the few newer U.S. longevity products I’d feel confident putting on the table for someone approaching or entering retirement.

Sovic Chakrabarti, Director, Icy Tales

——————————————- Continue Reading…

By Ariel Liang, BMO Global Asset Management

(Sponsor Blog)

If you’ve ever felt nervous about the stock market ups and downs, you’re not alone. Most investors want their money to grow steadily without the wild swings: especially if you’re thinking about retirement. Lately, worries about an AI bubble and changing interest rates have shown just how quickly things can get unpredictable.

That’s why building the right portfolio is important to help you stay calm and stay invested, even when markets get a little rocky.

Low-volatility investing, and specifically using funds such as BMO Low Volatility Canadian Equity ETF (ZLB) and BMO Low Volatility US Equity ETF (ZLU), are designed to give you a smoother experience. These strategies help you stay invested with confidence no matter what the markets are doing.

What does Low Volatility mean for your Investments?

Imagine low-volatility investing as playing it smart in baseball: not trying for risky home runs, but focusing on steady singles and doubles. This way, you keep making progress, scoring runs over time, and avoiding big losses. It’s all about reliable growth, not wild swings that could set you back.

ZLB and ZLU are designed to help your investments stay on track, even when markets get unpredictable. They pick companies that don’t jump around as much as the overall market: think of them as the steady players on the team. By steering clear of those big ups and downs, your money can grow more smoothly, and you can benefit from compounding over time.

Building a Smoother Ride with Low volatility

ZLB and ZLU focus on defensive sectors like utilities, consumer staples, and healthcare. These ETFs can act as financial shock absorbers, reducing risk from market swings and limiting exposure to more volatile sectors like technology. Position and sector caps further protect against over-concentration, while the selection of low-beta1 companies means the portfolio is designed to cushion losses during downturns.

The disciplined construction of ZLB and ZLU helps you stay on course regardless of market conditions. This approach isn’t about chasing the latest trends but about building steady, long-term growth through stability and diversification, letting compounding work its magic over time.

Low volatility cushioned the blow with stability

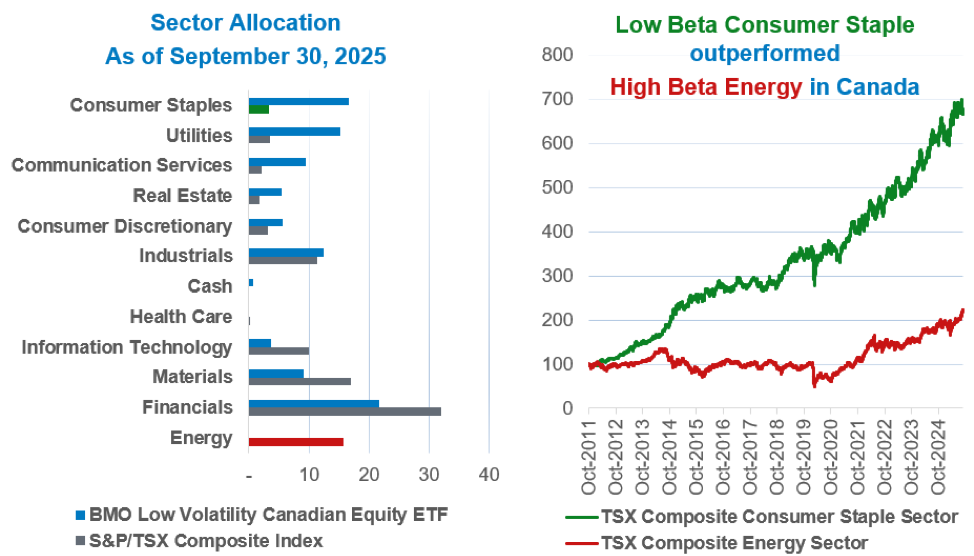

Chart 1

Note: Data as of September 30, 2025. Source: BMO AM Inc. Bloomberg Sector allocation subject to change without notice. Chart compares sector allocations of BMO Low Volatility Canadian Equity ETF and S&P/TSX Composite Index as of September 30, 2025, and shows Consumer Staples outperforming Energy in Canada from 2011 to 2024.

Common Myth: Low-Volatility ETFs reduce Return

Low volatility doesn’t mean you have to settle for lower returns. In fact, Canadian low-volatility investments have consistently outpaced the S&P/TSX Capped Composite Index since inception, offering strong returns while helping to reduce risk.

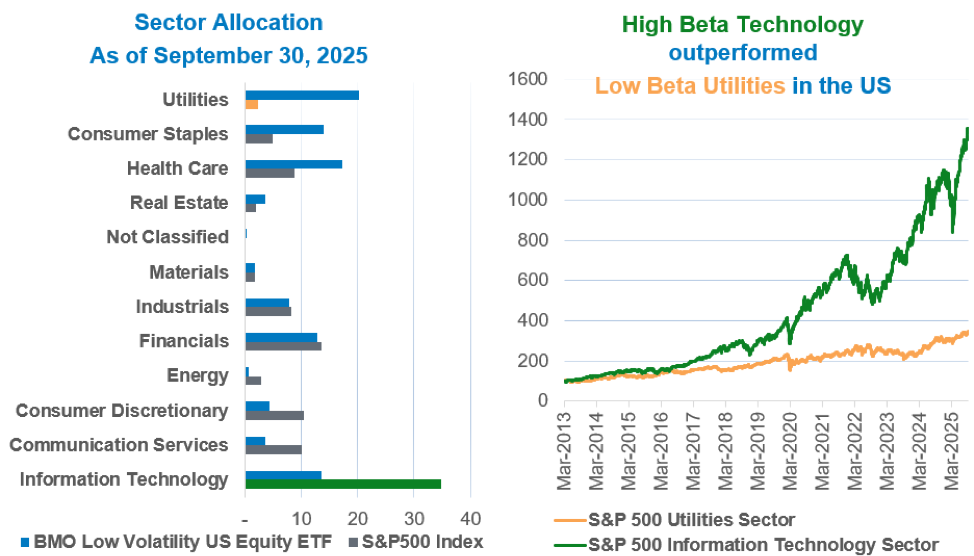

Chart 2

Note: Data as of September 30, 2025. Source: BMO AM Inc. Bloomberg Sector allocation subject to change without notice. Chart compares sector allocations of BMO Low Volatility US Equity ETF and S&P 500 Index as of September 30, 2025, and shows Technology outperforming Utilities from 2013 to 2025.

The U.S. market is highly concentrated in the Magnificent 72 and generally information. Because ZLU invests more in stable sectors like utilities and healthcare, it provides steady, long-term returns, though it might not keep up with the S&P 500 when the market is booming, as it has more recently with the growth dominated in the Tech sector. Even with this more cautious approach, ZLU still delivers strong annual returns for investors by emphasizing stability and value rather than jumping into the latest tech trends.

Balanced Growth, Less Stress: Blending ETFs for Smoother Returns

If you want steady growth for your portfolio without taking on too much risk, you may not have to choose between safety and strong returns. By combining BMO Low Volatility US Equity ETF (ZLU) with BMO NASDAQ 100 Equity Index ETF (ZNQ), you can get the best of both worlds: reliable stability and exciting growth. This mix has delivered higher returns and lower risk than simply investing in BMO S&P 500 Index ETF ( ZSP) as shown in Chart 3. Continue Reading…

By Kevin Anseeuw, CFP

Special to Financial Independence Hub

Canada is about to experience an unprecedented transfer of wealth across generations that will transform household balance sheets, life plans, and the role of financial advisors. Experts estimate that roughly $1 trillion will transfer between generations over the next decade, and this shift is discussed weekly.

As someone who advises families across multiple generations, I see three key implications. First, the amount of capital shifting hands is significant, but equally important are the who and the how: younger recipients seek different things than their parents. Second, the timing and structure of transfers (gifts made during life versus testamentary bequests) are driven by family dynamics as much as tax considerations. Third, the industry itself must modernize to stay relevant: advice now goes beyond portfolio selection to include income architecture, behavioral coaching, private-market access, values alignment, and digital delivery. The landscape is changing more quickly than I have experienced in the past 25 years.

Understanding what each generation needs and why they want it is the foundation for giving meaningful advice.

Baby Boomers: stewardship, income, and legacy

Baby Boomers still hold a disproportionate share of wealth in Canada, and their priorities have shifted from accumulation to preservation, predictable income, and legacy planning. The questions they ask are practical and existential: Will I outlive my money? How do I leave a legacy without causing family conflicts? How do taxes and health-care risks affect my plan? In practice, this means structuring retirement income to address longevity risk, incorporating tax-efficient solutions, and creating estate plans that minimize friction at death.

At Trans Canada Wealth, an advisory group of Harbourfront Wealth’s independent platform, we integrate investment strategies with our in-house CPA tax specialist and estate planning expertise so clients can see the full chain of outcomes, cash flow, taxes, and transfer, rather than isolated portfolio returns. This comprehensive approach is what gives Boomers the peace of mind they value most. We walk clients through our “Atlas” system to ensure they have peace of mind that no stone has been left unturned and that they have a structure and plan that works for their unique situation.

Gen X: the bridge generation demanding clarity

Generation X is in the middle, often financially squeezed, supporting aging parents while raising children, yet they are likely to be the most active people in managing wealth transfers. Many Gen X clients will inherit significant wealth but usually don’t plan for it; instead, they seek control, transparency, and practical plans that address debt today, catch up on retirement savings, and fund education. Unlike parents of previous generations, they have a stronger desire to help their children buy their first home and ensure they start their financial journey on solid footing.

An important role for advisors is facilitation: helping families have clear conversations about intentions and timing. We frequently counsel Boomers on the merits of lifetime gifts versus estate transfers because earlier transfers can increase intergenerational utility and allow parents to witness the benefits. Equally, Gen X wants straightforward, independent advice that filters noise, ensuring one poor decision doesn’t derail a 20- or 30-year plan.

Millennials: aligning performance with purpose

Millennials prioritize differently when they invest. While performance remains important, purpose and fees are now key factors. Studies and industry reports reveal that younger investors are highly interested in sustainable and impact strategies; they seek access to alternative investments and ESG-informed allocations as part of a diversified portfolio.

For advisors, this means providing institutional-grade access and clear discussions about costs alongside values-based solutions. Millennials are well-informed but have limited time; they expect advisors to add value by curating investment opportunities, conducting thorough due diligence, and explaining trade-offs: such as how an ESG focus might affect risk/return, liquidity, and fees. When advisors excel at this, they not only retain inherited capital but also build lifelong relationships.

Gen Z: digital-first, early adopters and learners

Gen Z approaches wealth conversations with a different relationship to money. They are digital natives, comfortable transacting and learning online, and many start their investing journey earlier than previous generations. Research shows a significant rise in early retail investing and financial literacy among Gen Z, and their expectations for digital access, education, and transparency are high. Continue Reading…