Hub Blogs contains fresh contributions written by Financial Independence Hub staff or contributors that have not appeared elsewhere first, or have been modified or customized for the Hub by the original blogger. In contrast, Top Blogs shows links to the best external financial blogs around the world.

Investing in companies that sustain and/or increase their dividends through different economic cycles is widely regarded as a prudent investing strategy, as sustainable dividend policies typically serve as a proxy for identifying high-quality businesses.

Companies with a track record of dividend growth often exhibit strong, reliable cash flows, disciplined capital allocation, and a clear commitment to returning value to shareholders. Such an investing approach can provide a steadily rising income stream to help offset inflation and enhance total returns over time.

We are excited to unveil the HAMILTON CHAMPIONS™ ETFs: built for long-term growth from exposure to blue-chip Canadian and U.S. companies with consistent track records of growing dividends (CMVP/SMVP). The suite also includes two Enhanced HAMILTON CHAMPIONS™ ETFs that utilize modest 25% leverage to further enhance long-term growth potential (CWIN/SWIN).

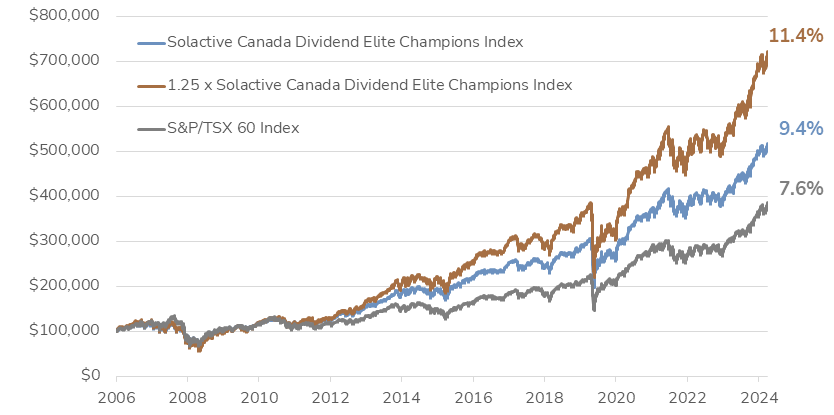

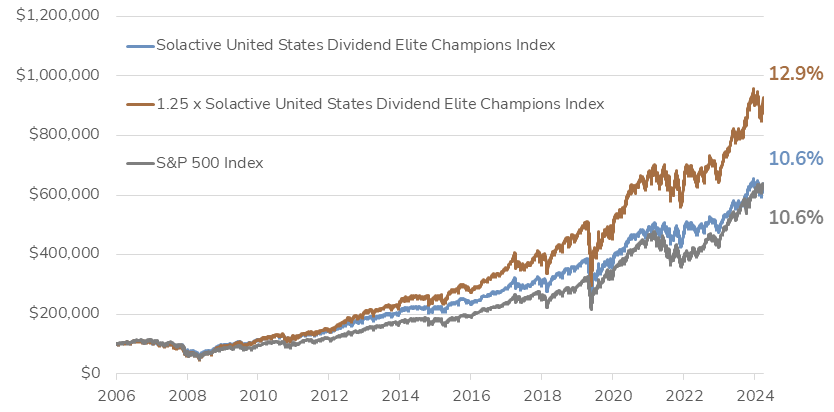

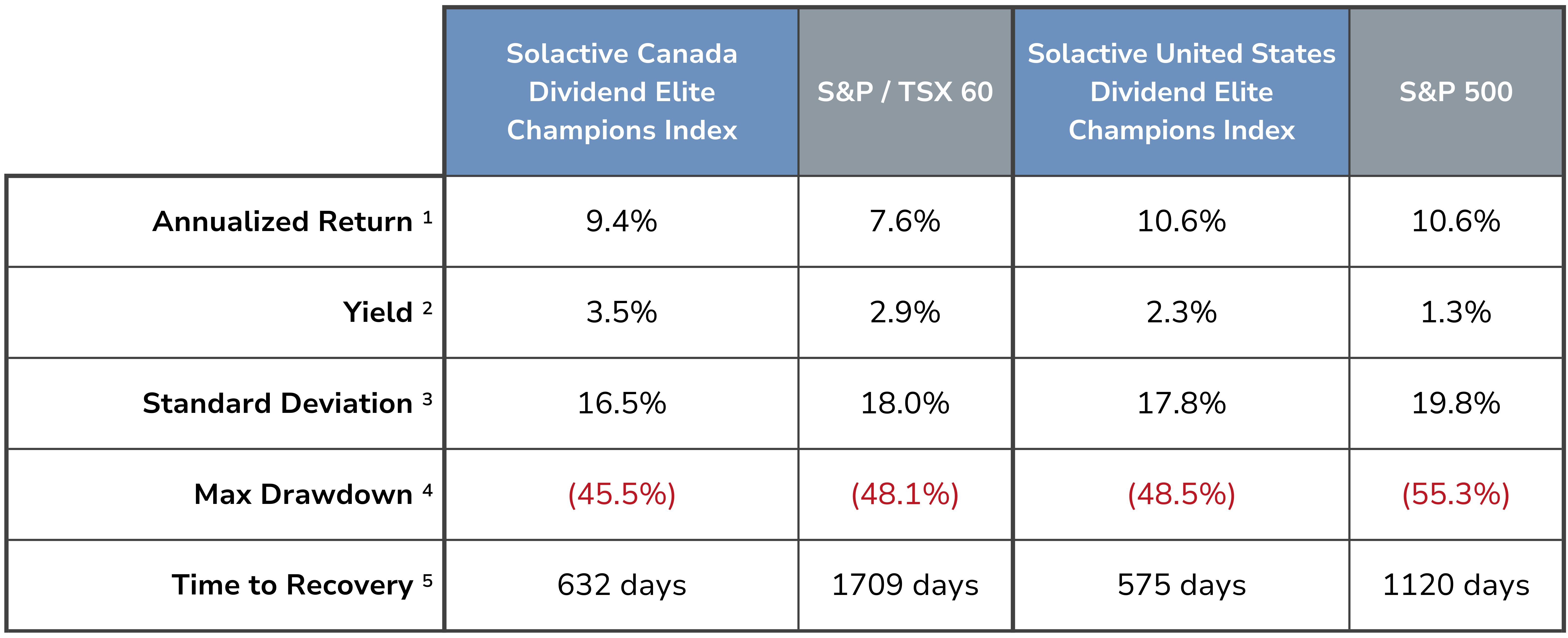

The HAMILTON CHAMPIONS™ ETFs are designed to track the Solactive Dividend Elite Champions Indices[7]. Boththe Canadian and U.S. indices have demonstrated strong performance and low volatility historically relative to the S&P/TSX 60 and the S&P 500, respectively.

Canadian HAMILTON CHAMPIONS™ — Growth of $100K [8],9]

U.S. HAMILTON CHAMPIONS™ — Growth of $100K [8, 10]

The Canada Dividend Champions Index and U.S. Dividend Champions Index are designed to provide equal-weight exposure to blue-chip stocks, listed in their respective countries, with a long history of dividend growth/sustainability. The result is a Canadian and a U.S. index with favourable performance and risk profiles vs. the S&P/TSX 60 and S&P 500, respectively. In addition, both indices have demonstrated (i) lower relative volatility; (ii) lower relative drawdowns; and (iii) faster relative time to recovery.

DISCLAIMER: see footnotes 1-5 below

Proven Winners, Rising Dividends

The Solactive Dividend Elite Champions Indices are focused on delivering diversified portfolios of companies with a long history of increasing dividends. The resulting portfolios have the following important characteristics: Continue Reading…

Discover unconventional paths to Financial Freedom that go beyond traditional advice. This article presents surprising strategies, backed by expert insights, that can transform your approach to wealth-building. From maintaining your lifestyle despite income increases to investing in non-financial assets, these innovative methods offer fresh perspectives on achieving financial success.

Maintain Lifestyle Despite Income Increases

Access High-Value Real Estate Through Syndications

Build Wealth with Niche Websites

Invest in Non-Financial Assets for Growth

Profit from Surplus Business Equipment Sales

Turn Discarded Inventory into Profitable Ventures

Monetize Legal Downtime with Tech Solutions

Transform Teaching into Wealth-Building Opportunity

Generate Passive Income by Renting Unused Space

Leverage Prop Trading Firms for Capital Growth

Maintain Lifestyle despite Income Increases

One unconventional yet effective method I tried to grow wealth and become financially independent is strategically managing lifestyle deflation in alignment with income changes. In simpler words, this means continuing to maintain the same lifestyle and budget even when your income increases, instead of adjusting your expenses alongside it.

I learned to prioritize this in my younger years after seeing people around me struggling to maintain their lifestyles despite rising income. I noticed they were increasing their expenses as their income grew. Most of these expenses were smaller differences that usually go unnoticed but compound to a bigger sum when you see them in total. Examples include subscribing to more services than before, buying more expensive items because they can now afford them, etc. Seeing all this, a thought nagged me often: “What would happen if they saved the raise they got instead of spending it immediately?”

As I learned more about personal finance, budgeting, etc., I started making a conscious effort to maintain the same lifestyle as always even as my salary grew. I funneled the extra sum into various investments instead. Over the years, this habit helped my net worth increase without compromising my quality of life.

Here are some tips I will offer others in this regard:

Automate the transactions into specific accounts: Immediately redirect your extra amount into another savings account for debt repayment and investments. This will help you avoid impulsive spending.

Understand wants vs needs: Take a broader look at your budget, including things you spend on usually. List all the expenses you make and consider which are important and which you can postpone for later since there is no immediate need. Doing this will help you stay focused.

Track net worth monthly: Make sure to track your investments frequently. Seeing your net worth grow will keep you motivated to continue your habit and avoid unnecessary purchases. — Lyle Solomon, Principal Attorney, Oak View Law Group

Access High-value Real Estate through Syndications

One unconventional way I’ve built wealth that surprised me on my journey to Financial Independence is through the strategic use of real estate syndications. While many focus on buying individual properties, I discovered that pooling resources with other investors allowed me to access high-value opportunities I wouldn’t have been able to tackle alone.

This method allows you to invest in larger commercial properties with a group of people, benefiting from economies of scale and shared risks. I first came across this approach through networking with experienced investors and learning about the power of group investment.

My advice to others would be to build a solid understanding of how syndications work and start small with reputable groups. It’s a unique way to scale wealth while minimizing individual risk, and it’s often overlooked compared to traditional property purchases. Collaborating with experienced partners can unlock doors to lucrative projects that wouldn’t be accessible otherwise. — Jonathan Ayala, Licensed Real Estate Salesperson | Founder, Hudson Condos

Build Wealth with Niche Websites

One unconventional way I’ve built wealth that really surprised me was by doubling down on building tiny niche websites. Early in my career, I thought the only path to success was creating huge, authority-style blogs. But after some experimentation, I realized that smaller, hyper-focused sites could generate a steady income without requiring a massive team or overhead.

I stumbled onto this by accident while testing out ideas that didn’t quite fit my main business. A few of these small projects started making a few hundred dollars a month each, and when you scale that up across multiple sites, it becomes something compelling. The magic is in finding a narrow topic where you can be the absolute best resource online, even if it’s something super specific.

For anyone interested, I suggest thinking smaller, not bigger. Find those underserved niches where competition is low, but passion or need is high. Focus on genuinely helpful content, optimize it properly, and be patient. It’s not a get-rich-quick strategy, but it is an incredibly reliable way to build passive income streams.

This approach allowed me to diversify without putting all my eggs in one basket and played a big part in reaching Financial Independence sooner than I expected. — James Parsons, CEO, Content Powered

Invest in Non-Financial Assets for Growth

One unconventional way I built wealth was by keeping a “no-market” year. For twelve months, I chose to remove myself from investing in anything that required speculation, interest, or growth. Instead, I focused on building non-financial assets: time, skill, energy, and relationships. I tracked it like a portfolio: hours of learning, time saved by simplifying routines, days reclaimed from overcommitting, and people I could count on for collaboration. That “quiet compounding” brought in far more than my typical quarterly gains ever did. I walked into the next year with three new paid projects, two solid partners, and almost double the free time.

I discovered it accidentally after turning down a contract that would have pulled me out of integrity. I gave myself permission to step back and see what kind of return I could build without putting money anywhere. I suggest trying this as a 90-day experiment. Track the non-financial gains as seriously as you would your net worth. Value created in learning, trust, and creative space often turns into money later. The catch is, you have to believe it is real before anyone else does. Once you see it, it is hard to go back. — Adam Klein, Certified Integral Coach® and Managing Director, New Ventures West

Profit from Surplus Business Equipment Sales

Purchasing and selling surplus business equipment was much more profitable than previously thought. Initially, it was just a game of turning what companies didn’t want into something useful. But as time went by, I learned what had actual value was an awareness of where the demand was: what buyers were searching for but couldn’t be found easily. That gap became an opportunity.

I became interested in it on a whim when assisting someone with liquidating their lab, and saw its inefficiency. So we built a system around it. My advice? Identify supply chain omissions or inefficiencies in industries that people do not pay much attention to. The more untrendy it sounds, the more opportunities you’ll have if you’re willing to master it inside out. — Joe Reale, CEO, Surplus Solutions

Turn Discarded Inventory into Profitable Ventures

I started buying leftover inventory from failed event suppliers. Half the time they were happy just to offload it for $0.10 on the dollar. I mean, we once picked up $35,000 worth of LED wall panels for $2,800, stacked them in our warehouse, and rented them out per gig for $650 a pop. In under four months, they paid for themselves, and we have since generated over $48,000 in revenue from those same panels. Everyone wants to build wealth from stocks or SaaS. I just bought junk others walked past and turned it into profit. Continue Reading…

The clatter of an engine, the screech of worn brakes, or the ominous glow of a check engine light are often precursors to hefty repair bills that can drain a bank account. Many vehicle owners view car maintenance as an unwelcome expense, yet a proactive approach to servicing your vehicle can be one of the most effective ways to safeguard your finances. By adhering to a regular maintenance schedule, you’re not just ensuring your car runs smoothly and reliably; you’re actively preventing minor issues from escalating into catastrophic failures that can cost thousands of dollars to rectify, ultimately saving you a significant sum in the long run.

Image Adobe Stock, courtesy Logical Position

By Dan Coconate

Special to Financial Independence Hub

Car repairs can suck the cash right out of your wallet if you aren’t careful. But with regular, proactive care, maintaining your car can save you thousands by helping you avoid surprise bills.

This post breaks down how a few simple habits and a bit of attention can help everyday car owners save more over the life of their vehicle.

Why Car Maintenance pays off

Your vehicle is an investment, and treating it appropriately will pay off in the following ways:

Prevents expensive breakdowns: Small problems caught early rarely balloon into wallet-busting repairs. You can save money and avoid the headache (and expense) of having to rent a vehicle. Most importantly, you’ll never be the person stranded with smoke pouring from their engine on a busy freeway.

Extends car lifespan: Well-maintained vehicles last longer, delaying the need for a new (and costly) purchase. Instead, you can trade in or sell your vehicle on your terms and timeline.

Boosts fuel efficiency: Clean filters, fresh oil, and inflated tires mean fewer stops at the pump. Even if you have good fuel efficiency, the less you have to fill up, the more you save.

Higher resale value: Service records and a tidy vehicle earn top dollar if you decide to sell. You can put that money toward your next vehicle, which means you’re ahead of the game.

Key Maintenance Tasks that save Money

Not sure where to start when it comes to maintaining your car to save thousands? Try this checklist:

Oil changes: Stick to your manufacturer’s recommended oil change schedule. Old oil leads to engine wear and potentially catastrophic (read: very expensive) failure.

Brake pads and fluid: Replacing worn pads is much cheaper than replacing your entire brake system.

Air and cabin filters: When clogged, filters make your engine work harder, burning more fuel and costing you more at the pump. Continue Reading…

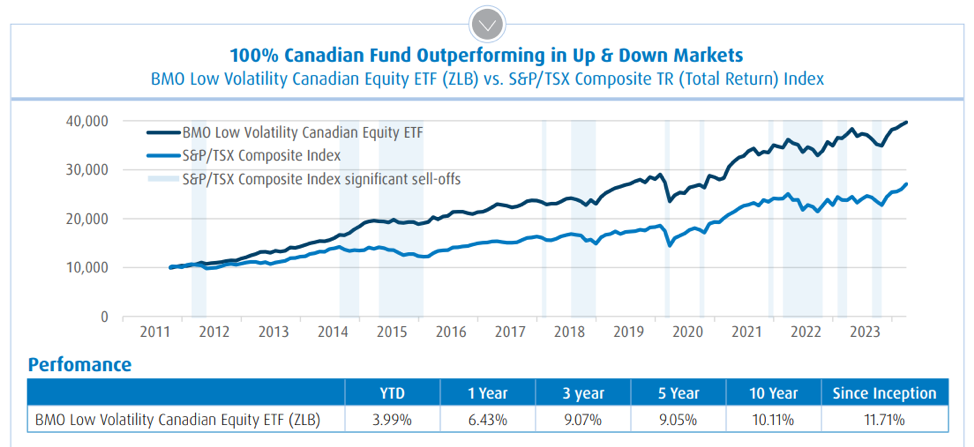

Markets are noisy right now. Between trade talks, shifting rate expectations and recession whispers, there’s no shortage of turbulence. That’s why low-volatility strategies are back in focus: and BMO’s lineup is standing out.

Not all low-vol ETFs are created equal. In fact, BMO’s low-volatility ETFs have been quietly dominating their corner of the market. Here’s what’s working with the approach and the key differentiators of the methodology.

Source: Morningstar as of March 31, 2024 2

Smart, Targeted Methodology

BMO doesn’t just take the market and strip out the riskiest names. Its methodology is precise, practical, and time tested

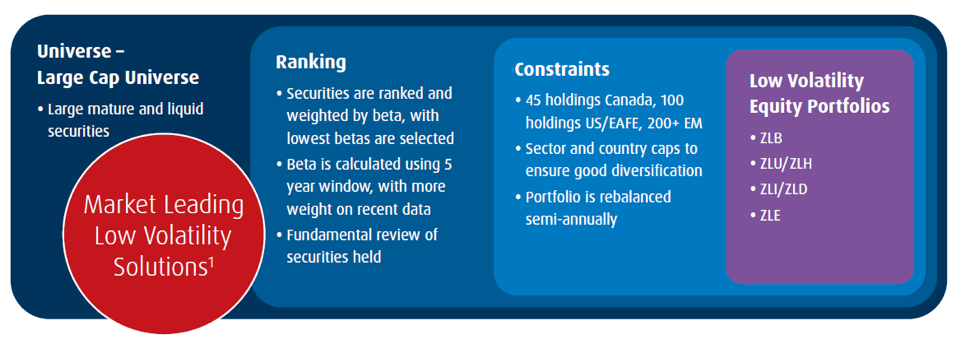

Step 1: The Starting Point

BMO begins with a broad universe of stocks that are the largest and most liquid from a particular region — say, Canada or the U.S. — and then ranks them based on historical return volatility (also known as beta). Lower is better here.

Step 2: Ranking

Next, the securities are ranked and selected based on their beta, with lowest betas carrying the highest weight in the portfolio. Beta is calculated using 5-year window, with more weight on recent data. Then the team engages in a fundamental review of securities held.

Step 3: Sector Constraints

Unlike some low-vol strategies that end up extremely overweight in defensive sectors (hello, utilities and consumer staples), BMO imposes sector caps. Why? To ensure diversification and avoid concentration risk. That means that while there will be a tilt towards defensive sectors, you’re building a balanced, resilient portfolio.

The Burning Question: Why ‘Beta’?

Beta and Standard deviation are two of the most common ways to measure a fund’s volatility. The key difference is that beta measures a stock’s volatility relative to the market as a whole, while standard deviation measures the risk of individual stocks.

This is where BMO ETFs stands apart in their strategy: The BMO ETF Low Volatility Strategy uses beta as the primary investment selection and weighting criteria. By constructing ETFs with lower beta securities, the BMO ETF Low Volatility Strategy gives investors access to portfolios that are designed to provide growth while reducing exposure to market risk. Over the long term, low beta stocks may benefit from smaller declines during market corrections and still increase during advancing markets. Additionally, they tend to be more mature and provide higher dividend yield than the broad market.

Beta is a risk metric that measures an investment’s sensitivity to fluctuations in the broad market (market sensitivity). The broad market is assigned a beta value of 1.00, an investment with a beta less than 1.00 indicates the investment is less risky relative to the broad market.

So why now?

Low volatility has always had its place: particularly for long-term investors looking to stay invested through all market cycles, or those who tend to be more emotional around volatility in their portfolio. But right now, the case is even stronger: Continue Reading…

The U.S. healthcare sector has faced unique challenges in late 2024 and the first half of 2025. Last year, we provided an in-depth look at global healthcare as a long-term opportunity and examined some of the catalysts and innovations that were impacting the sector. Today, the U.S. and global healthcare space continues to evolve while combatting headwinds in some key areas.

The state of U.S. healthcare equities

Healthcare performed relatively well in the early part of 2025, despite broader trade uncertainty and macroeconomic headwinds. The medical technology and tools sub-sector experienced some short-term volatility that was driven by the uncertainty surrounding tariffs. That comes as little surprise, considering companies in the space reliance on oversees manufacturing and revenue generation.

Domestic names, like those in Managed care and select Biopharmaceuticals, remained relatively insulated during this period. This stemmed from an easing in the tariff narrative, which was triggered by a sharp drop in several macroeconomic indicators that included manufacturing activity and consumer confidence. As we progressed further into 2025, a cloud of uncertainty crept into healthcare. That contributed to some recent volatility across several sub-sectors. In this article, we have provided some recent catalysts to help investors make sense of the current situation in healthcare.

Drug pricing in 2025

On May 12, 2025, President Donald Trump signed an Executive Order (EO) titled “Delivering Most-Favored-Nation Prescription Drug Pricing to American Patients.” This EO proclaimed that the Trump administration “will take immediate steps to end global freeloading and, should drug manufacturers fail to offer American consumers, the most-favoured-nation lowest price, my Administration will take additional aggressive action.”

Ultimately, the aim is to align U.S. drug prices more closely with lower prices paid internationally. This EO echoes a summer 2020 Trump-era EO that was blocked in court and failed to be implemented. The current version faces similar hurdles. There is no bipartisan backing for the policy, the legality surrounding it is dubious, and there is opposition among both Democrat and Republican lawmakers.

All of these make the implementation of this EO unlikely. However, we could see pilot programs within the Department of Health and Humans Services (HHS), making attempts to fold the current EO’s proclamations into future IRA negotiations, or more comprehensive legislative proposals.

In addition, there are those who have predicted the policy could reduce the research and development (R&D) budgets further. That could potentially impact innovation and companies that have been propelled due to strong R&D spending. However, the risk may truly lie in the negative sentiment that continues to emerge in the news cycle.

Vaccine market uncertainty

The appointment of Robert F. Kennedy Jr. as the United States Secretary of Health has damaged sentiment for healthcare companies that manufacture vaccines. RFK Jr. is a vocal “vaccine sceptic.” Moreover, the Trump administration has pursued leadership changes at the Food and Drug Administration (FDA), which raises questions about stricter vaccine approval processes going forward.

Merck & Co, the U.S.–based pharmaceutical giant, with its vaccine-related businesses, has felt the pressure. In addition to the political uncertainty, a recent CMS technical document has added to the complexity in the vaccine arena. The report suggested that reformulated drugs may no longer be classified as “new” for Medicare negotiations. This development could impact companies with operations in the “combination therapy” space like Johnson & Johnson’s Darzalex Faspro, or Bristol Myers’ subcutaneous version of Opdivo. That could affect future patent projections as well. Continue Reading…