By Ian Duncan MacDonald

Special to the Financial Independence Hub

Did you ever try to defend investing in the stock market when the risk averse shouted that no one can foretell the future and investing is just a crap shoot?

The Canadian Pension Fund’s purchase of several million more shares of Royal Caribbean Cruises Ltd in the fourth quarter of 2019 is an example of our inability to foretell the future. Due to COVID-19, Royal’s shares dropped a billion dollars in the first quarter of 2020. With assets of $420 billion, our pensions are not in jeopardy, but it may well be years (perhaps decades) before Royal Caribbean share price recovers to its former glory.

“Capital value is going to fluctuate over time,” was the pension fund’s response to the hit. They are right. As long as the pension fund does not sell these depreciated shares, they will technically never take the billion-dollar hit.

Not having to sell is the joy of investing with the public’s money. The next time you lose a few thousand on your stock pick you can tell your spouse, who is questioning your investment skills, “It’s a long-term play. At least it wasn’t a billion dollars like those professionals at the Canadian Pension Fund.”

Until COVID-19, investing in cruise lines looked like the safest of investments. Every year their boats were full of more and more baby boomers with the time and money to splurge on the non-essentials of life.

The $46 billion-dollar cruise industry is dominated by Miami based Carnival Corporation (CCL/NYSE), Royal Caribbean Cruises Ltd (RCL) and Norwegian Cruise Line Holdings (NCLH). In 2019, these three gave boat rides to 80% of the 26 million cruise passengers in the world. Between them they employed 272,000 in 200 ships. These now under utilized assets are tied up at docks with only a hope that some of them might tentatively begin cruising again August 1, 2020.

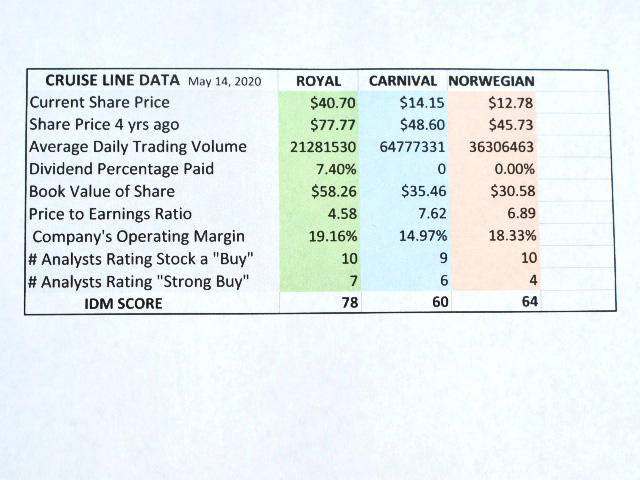

Would cruise shares make a good edition to now add to your portfolio? The following chart gives you an idea of how speculative an investment they might be:

Do you find it interesting that despite the pandemic, analysts are rating all these stocks as buys and strong buys? Based on this limited data, did the pension fund choose the best one to add to their portfolio? Interestingly Royal paid a dividend in April; this appears to be the last dividend they will be paying for the foreseeable future. The other two have not paid dividends this year.

Supply 20 times more than Demand

The book values of these three companies are well ahead of their current share price, which indicates a bargain. Admittedly, “book values” are calculated by accountants and are not the same as the “market values” that might be realized if the company’s assets were liquidated. Currently, the supply for cruise ships is probably 20 times greater than the demand.

The price to earnings ratio is low confirms that the shares are not overpriced. The operating margins for the three reflects their historical sales minus the expense to realize those sales. With little new revenue now coming in, their operating margins will probably be a minus figures when more current financial information is released.

The IDM score at the bottom of the chart is a measuring stick and summary to quickly evaluate stocks. It is based on the data currently available to the public. It does not reflect the dire straights that these businesses are now in. The scores reflect those of the profitable well-run companies that these three once were just a few months ago. Normally any score over 70 indicates a very desirable stock to own. Anything over 50 is normally a safe stock purchase. (You can learn more about the IDM score at informus.ca). Continue Reading…