Hub Blogs contains fresh contributions written by Financial Independence Hub staff or contributors that have not appeared elsewhere first, or have been modified or customized for the Hub by the original blogger. In contrast, Top Blogs shows links to the best external financial blogs around the world.

MoneySense.ca: Photo created by snowing – www.freepik.com

MoneySense magazine has begun to publish a package of three mutual fund articles they commissioned me to write. You can find the first article by clicking on the highlighted headline: DSC mutual funds and the future of investment advice. It ran on January 16th.

The first article looks specifically at the gradual decline of the once-ubiquitous DSC sales structure, or Deferred Sales Charge. It recaps recent regularatory developments surrounding DSC, and addresses the related issue of embedded compensation for financial advisors, or so-called Trailer Commissions. These are gradually being eliminated in various Western nations (notably the UK and Australia/NZ) and they are also being phased out in all Canadian provinces, with the conspicuous exception of Ontario.

The lesser-known “Direct-to-Consumer” mutual fund families

When it’s published, the second article will look at two particular “camps” of mutual fund providers: the big-name Embedded Compensation firms you may have heard from (because they can afford to advertise) and a lesser known camp of Direct-to-Consumer managers whose names may be less familiar because they don’t generally have embedded compensation and whose fees are lower and typically mean they don’t have as much money to throw around on big marketing and advertising budgets. The article focusses on four firms in particular you may not have heard of, except through family referrals and word of mouth: Beutel Goodman, Leith Wheeler, Mawer, Steadyhand.

Space precludes mentioning that in the good old days of mutual fund mania (the 90s) there were several other direct-to-consumer firms that either were acquired or are now a shadow of their former selves: the list includes Altamira, Saxon, Sceptre and a few others. We also look at two deep value firms that are still around but get so much publicity about their performance that they can hardly be dubbed as “firms you’ve never heard of.” They are Irwin Michael’s ABC Funds and Francis Chou’s Chou & Associates. Continue Reading…

By Doug Conick, DUCA Credit Union and Chair of Duca Impact Lab

Special to the Financial Independence Hub

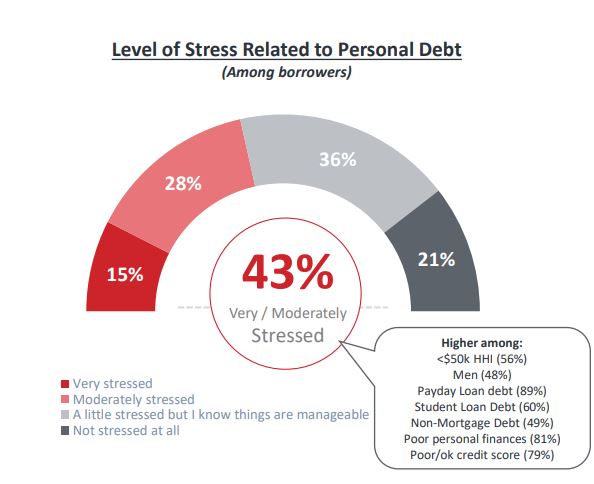

Financial institutions play an important role in Canada’s economic well-being. They support growth in personal wealth, job creation and impact the country’s prosperity overall. It is my firm belief that when it comes to the household debt burden of Canadians, there is an even greater role for financial service providers to play. We have a duty to act in the best interest of our clients and proactively contribute to the financial wellbeing of Canadians.

On Wednesday (Jan 15) DUCA Impact Lab released the results of a first-of-its-kind Canadian study to capture the perceptions of Canadian borrowers and lenders, ultimately shining a light on disparities between the two groups. The research uncovers interesting new details about how Canadian borrower and lenders interact with each other and explains how borrowers are impacted by debt. You can find the full report here.

The mounting stress of debt on Canadians

We talked to over 2,000 Canadian borrowers, nearly half of which reported that personal debt has impacted their ability to save and build wealth. It’s concerning that over one-third of borrowers surveyed report avoiding interactions with their financial advisor, despite recent Statistics Canada research which shows Canadians are spending more money than ever on debt payments.

The household debt-service ratio, which represents the percentage of after-tax income used for debt payments, rose to a record 14.96 per cent in the second quarter of 2019. This underscores the increasing need for better understanding among Canadians on how to manage existing debt. Canadians need help but they simply aren’t asking for it.

Our survey also shows debt affects access to healthcare and quality of life. Those surveyed report anxiety, trouble sleeping and poor lifestyle choices like skipping meals, eating unhealthy foods and spending more time alone.

The gap in perception

A quarter of borrowers surveyed say they don’t trust their financial institution to guide them through their debt issues and 37 per cent report avoiding their financial services representatives due to perceived pressures to manage their finances in a way they do not feel comfortable with or because they are recommended products they do not understand. At the same time, 42 per cent of lenders surveyed report they don’t believe their clients fully understand the products they are purchasing.

This demonstrated lack of trust in financial services professionals and gaps in understanding of financial products can lead to a cycle of debt and a missed opportunity to set or prioritize financial goals. Continue Reading…

Author David Aston, whose book becomes available today

Today is the formal release date for David Aston’s new book, The Sleep-Easy Retirement Guide. Below is a Q&A I conducted with David to mark the occasion. See also my review of the book at MoneySense that appeared in December, as well as the Hub’s throw to that piece.

Jon Chevreau: What inspired you to write the book after so many years of writing about Retirement?

David Aston: I have covered most of the key issues in planning for retirement in stand-alone articles I have written over the years. But I wanted to update that advice for current circumstances and figures, show how all the issues fit together as an interconnected whole, and provide it in a combined reference guide that people could have on their shelf and readily turn to when questions came up.

Q2: What do you think about the FIRE movement?

DA: The Financial Independence Retire Early (FIRE) movement is certainly laudable. It’s an admirable concept that people should try to achieve Financial Independence as early as possible, which frees them up to do work that is most meaningful to them (rather than being obligated to do work that maximizes income). As I understand it, it also includes the concept that people should adopt a modest lifestyle that consumes money carefully and wisely without wasting it, which in turn helps make Financial Independence more achievable at a relatively young age. But from what I’ve read, many of the FIRE scenarios are oriented to extreme examples of people trying to achieve Financial Independence in their 30s. So it sometimes comes up as a concept for millennials who are looking for Financial Independence as a near-time goal rather than one that is achieved after a long career at work. That’s only possible for a tiny minority of people. In my experience, it is far more common for people in their 30s to go through a very difficult financial crunch period where they are struggling to buy a house, then make humungous mortgage payments, and cover the expensive costs of raising kids. FIRE goals are not realistic and achievable in your 30s for the vast majority of people. However, the quality of thriftiness and emphasis on saving can be emulated by everyone. I personally think FIRE makes a fair amount of sense for the far more common case of people of average means who might aspire to achieving Financial Independence in their early 60s or possibly their late 50s, but that may not sound particularly appealing to millennials.

Q3: What’s your take on Semi-Retirement and/or Phased Retirement?

DA: The whole world of work for older workers is opening up. The once accepted norm that people retired from their career job to live a life of leisure close to age 65 has pretty much gone out the window. There are lots of expanding options for people to do post-career work that is different than their career job. Often it involves reduced hours, but it can also be full-time work that is less stressful or more fulfilling, or some combination of these attributes. There are various forms of part-time work, contract work, self-employment, consulting or temp work. Often it means switching employers or being self-employed, but it can also mean gearing down to reduced hours or a less stressful role with the same employer. And these post-career options are often started in your early 60s, but they can also happen earlier or later. So there is a vast array of options out there and it’s really up to people to pursue the opportunities that appeal to them the most.

I should mention that “phased retirement” is a term that is sometimes applied to formal corporate programs that allow older employees to adopt a reduced-work schedule or otherwise gear down with the same company prior to full-retirement from their career job. If you go back about 10 years or so, there was an expectation that these kind of corporate programs would increasingly catch on and be offered by major corporations. However, it never really caught on as formal corporate programs that are broadly offered to all older employees. What I have seen happen is that you get a lot of these kind of arrangements to offer reduced hours or less stressful/more fulfilling job functions negotiated on an informal, individual basis. They aren’t offered to everybody in the company. Whether or not an employee can achieve something like that or not depends on the nature of their job, what their boss is looking for, as well as their individual wants and needs. Continue Reading…

If you’ve been watching the real estate market in British Columbia, you may have noticed that quite a few Nanaimo homes for sale have a large amount of equity. Equity is the difference between the market value of your home and the mortgage balance owed. Another way of thinking about equity is that it’s the profit you make when the time comes to sell.

Building equity is the largest single benefit of owning a home in Nanaimo or anywhere else. Your home equity increases in one of two ways:

Value of your home increases

Amount of debt on your home decreases

Add value to your home

Here are eight great ways to build equity in your home by increasing value and decreasing debt:

You have instant equity in your home when home values appreciate. Three things that make home values rise are:

1.) Real estate market in Nanaimo is moving upward: Appreciation is something that happens without you having to do anything. Home prices are more likely to go up in established, attractive neighborhoods and in growing areas around town.

2.) Improvements and updating: Not all home improvements have the same return on investment. So, before spending money on updating, be sure to choose the ones that will add the most value to your home. Smart home improvements include kitchen and bathroom updating, improving curb appeal with low-maintenance landscaping, and adding square footage to your home.

3.) Upkeep & routine maintenance: Although routine maintenance can be tedious, it’s better to keep everything in your kept up than to face a major repair bill like a leaking roof or broken down furnace. Nanaimo homes for sale that have been maintained poorly are also at the biggest risk of losing equity, even when the real estate market is appreciating.

Decrease debt on your home

Decreasing the debt on your home while adding value can build equity surprisingly fast. Techniques to reduce mortgage debt include: Continue Reading…

Both employees and employers can benefit from keeping track of how much money goes into each paycheck. For employers, it’s important to know for business tax reasons. Employees, while also needing to know how much they make for tax reasons, may also need to provide their pay stubs when signing up for government benefits, when renting an apartment, or for a number of other reasons. However, sometimes it can be hard to keep track of paper pay stubs; that’s where mobile pay stubs come in.

What are Pay Stubs?

Before we get into the benefits of using mobile pay stubs, let’s first discuss what a pay stub actually is. When it comes to people who get paper paychecks, the pay stub will be attached to the paycheck.

For those who get direct deposit paychecks, paystubs can be a little harder to find. The employee may have a website they can check to see their pay stubs. If that is not possible, employees may need to contact the payroll department directly to get printouts or computer files of their paystubs.

What are Pay Stubs used for?

What makes paystubs so important? Why do they need to be kept track of? To put it simply, pay stubs are used as a record of how much an employee makes. As mentioned earlier, it’s important to keep track of pay stubs in order to keep track of income or expenses (based on whether it is the employee or employer looking at pay stubs). Since people usually cash their checks right away, keeping the pay stubs is a great way to keep a record of how much they make.

What information do paystubs have on them? A paycheck only shows the net pay (what a person makes after taxes, insurance, and other items are taken out). However, a pay stub will show an itemized list of earnings and deductions. This includes the gross pay, taxes, insurance, retirement savings, and the net (take-home) pay.

Why use Mobile Pay Stubs?

If paychecks come with a pay stub attached, why should people who get paper checks bother with mobile pay stubs? Unless you’re extremely careful with your pay stubs, they can be easy to lose. Continue Reading…