By Penelope Graham, Zoocasa

By Penelope Graham, Zoocasa

Special to the Financial Independence Hub

When the federal government announced in March that it would be wading into the shared equity mortgage market in efforts to improve home buyer affordability, it stirred up some controversy.

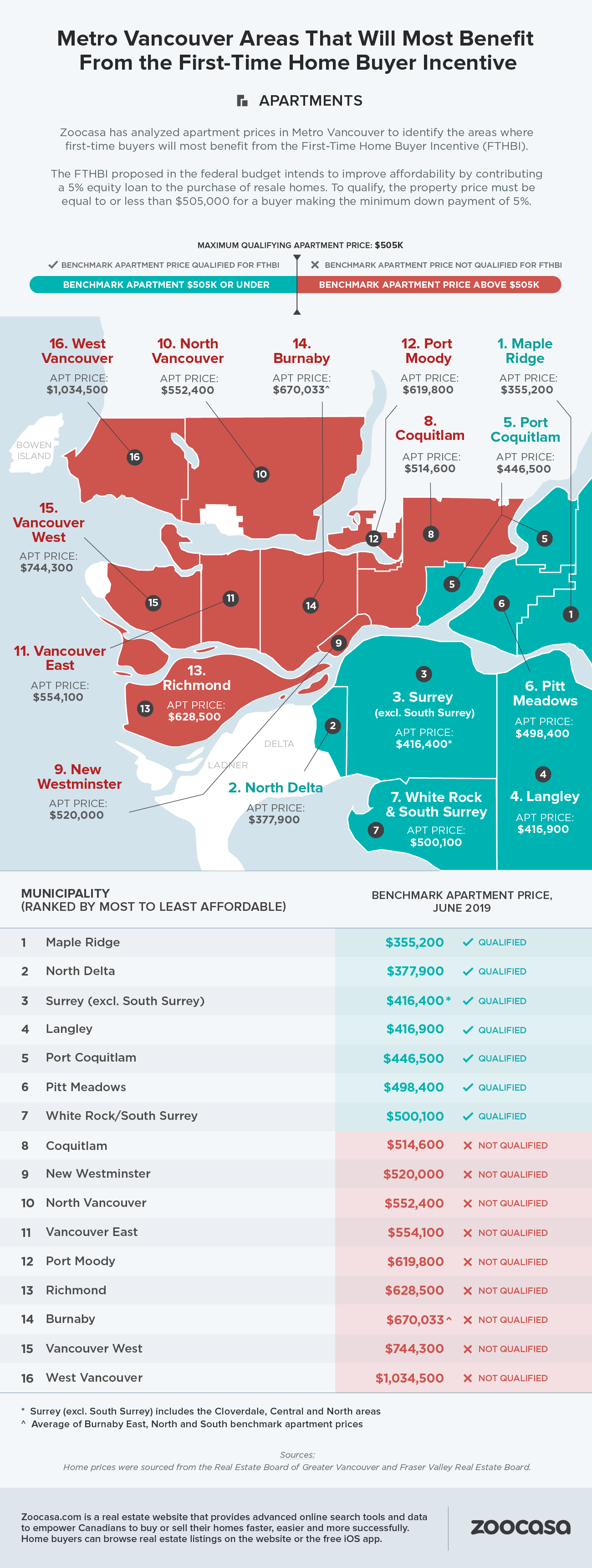

The program, called the First-Time Home Buyer Incentive (FTHBI), was teased in the budget as a ground-breaking approach to helping buyers get into the market by providing interest-free down payment loans of 5% for resale homes, and up to 10% on brand-new builds.

In exchange for the upfront funds, which are designed to reduce the overall size of the mortgage and monthly payments, the Canada Mortgage and Housing Corporation (CMHC) will take an equity percentage the homes’ value, which must be paid off when either the mortgage matures, or the home is sold.

This paid-back amount fluctuates along with appreciation and depreciation in the market. For example, let’s say the CMHC provides a 5% loan of $25,000 for a home purchase of $500,000. The homeowner sells the home several years later, and its value has increased to $550,000. The homeowner would then need to pay the CMHC back $27,500 to reflect 5% of the increased value of the home.

Critics say FTHBI too restrictive to be effective

Mortgage analysts have called the effectiveness of this equity sharing program into question, as the total amount owed to the government could be significantly more than what was loaned in the first place, especially in a market that experiences rapid price growth.

However, the most contested features of the FTHBI are its mortgage and purchase price restrictions, which critics say render the program useless in markets like Toronto and Vancouver where home buyers arguably need the most help. Continue Reading…