Hub Blogs contains fresh contributions written by Financial Independence Hub staff or contributors that have not appeared elsewhere first, or have been modified or customized for the Hub by the original blogger. In contrast, Top Blogs shows links to the best external financial blogs around the world.

Deciding whether or not to get into the real estate market? While budget, location, and home type will be among your top considerations, there’s another metric that can help inform your move: the buyers’ conditions in your desired neighbourhood.

Understanding whether you’ll be dealing with a sellers’, buyers’, or balanced market is key to crafting your offer or listing strategy. Those trying to buy a home amid tight sellers’ conditions will need to be ready to participate in bidding wars, for example, make aggressive bids, and be prepared to drop offer conditions to be competitive. Entering a buyers’ market indicates more real estate inventory and choice for buyers, and often the room to negotiate.

Sellers are also wise to take these conditions into account as listing during a relaxed market may mean adjusting pricing expectations; it could be a better idea to wait for the market to firm up before trying to sell your home.

What is a Sellers’ Market?

But what actually classifies a market as buyers’, sellers’, or balanced? A common misconception is price. However, while prolonged conditions will eventually influence home values, a buyers’ market doesn’t also indicate better affordability, and vice versa. Rather, these conditions are determined by a metric called the sales-to-new-listings ratio (SNLR).

The SNLR is calculated by dividing the number of sales by the number of new listings within a specific housing market over a period of time. It reveals how many of the homes listed for sale are selling within that time frame, and sheds insight into how competitive the market is for buyers and sellers. According to the Canadian Real Estate Association (CREA), an SNLR between 40 to 60% is considered a balanced market, with below and above that threshold indicating buyers’ and sellers’ conditions, respectively.

Getting the Bigger Picture

A great thing about looking at SNLR is you can get as local as you need to with your market assessment; a buyer or seller can understand what’s happening at the neighbourhood level, whether they’re looking for condos for sale in downtown Toronto, or Etobicoke homes for sale.

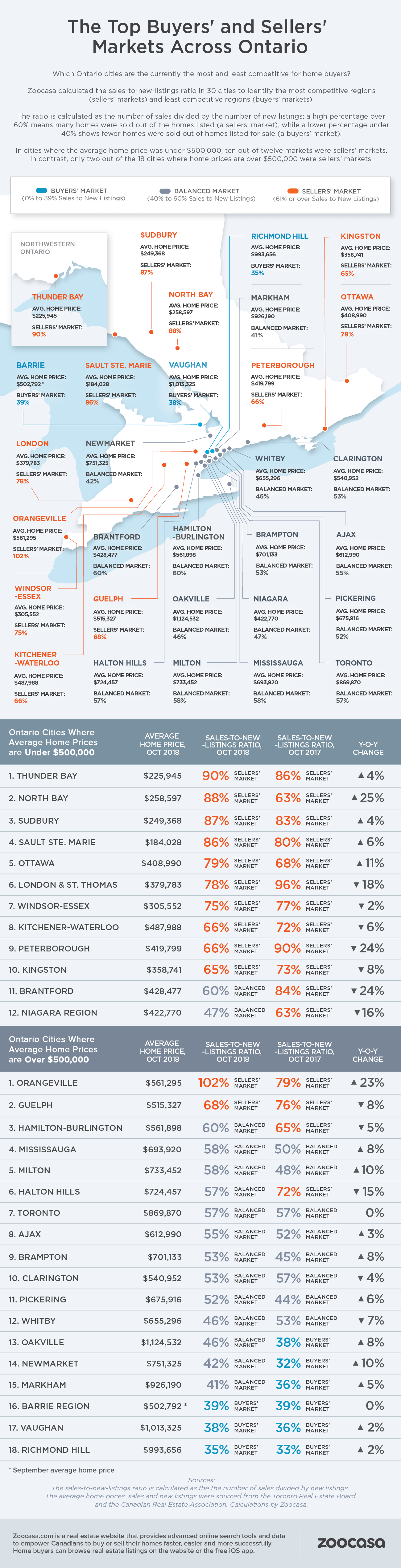

The SNLR can also be used to measure activity over larger geographic areas. At a provincial level, Ontario’s housing market remains in balanced territory, with an SNLR of 56%. However, this ranges quite widely throughout the province with some surprising results, according to recent data compiled by Zoocasa; a look at October sales and new listings numbers reveals Ontario’s most affordable markets are actually among the tightest in terms of sellers’ conditions.

Sellers’ conditions in Ontario’s most affordable markets

In markets where homes sell for less than $500,000, 10 of 12 municipalities could be considered sellers’ markets. Continue Reading…

Does the “global trade war,” quotation marks intentional, spell doom? It depends on your silo.

The 2009 American Recovery and Reinvestment Act poured some C$1.03 trillion of stimulus into the system, while China’s coincident crisis-era package dumped a C$768 billion package on top.1Central banks added trillions in bond purchases for the trifecta.

But some people may have missed the boat. Who? Those who couldn’t get past their ideological differences with the last U.S. president, who made some of them think the global financial crisis would lead to a perpetual depression. Distorted reality costs money, and what happened with Obama’s detractors is now happening in the Trump administration. Some proportion of the public, including many on Wall and Bay Streets, are letting their political views with respect to President Trump get in the way of arithmetic.

That can create opportunity for the sober observer.

What is one mistake investors are making? Prognosticating “global trade war” doom.

Global Trade War?

2018 has witnessed nothing but improvement in relations between China and Japan, nothing but improvement in relations between Japan and Europe and, arguably, nothing but improvement in relations between the U.S. and both Mexico and Canada, at least compared to this past summer.

Some global trade war this is, with major foreign leaders jumping over each other to prove their free market bona fides.

“We must promote trade and investment, liberalization and facilitation through opening up—and say no to protectionism.”— Chinese President Xi Jinping, 2017

“It is also quite vital that we keep on raising high the flag of free trade.” — Japanese Prime Minister Shinzo Abe, 2017

“We believe multilateral cooperation can add value for everyone, and that’s why we’re advocating global trade that is as free as possible and which is based on common rules. ”— German Chancellor Angela Merkel, 2018

The truth is that Trump is calculating that Americans have finally hit a wall on the status quo with respect to China. Regular people on the street may not know the specific trade numbers, but they know where the knock-off purses come from, they know now about wanton intellectual property theft and, most disconcertingly, cyberwarfare.

In reframing the argument about global trade, does anyone care that Japan, China and South Korea are sitting at the table with one another for trilateral trade talks?2How about the big August trade deal between Japan and the EU? Talk about large economies.

While market angst is focused on the Trump administration’s “global trade war,” most of the planet is actively making deals, in direct contrast to the meme of global internecine tariff warfare.

And China’s Scythe on Taxes

While markets react to headlines, China’s fiscal stimulus continues apace. Some investors appear to be missing the good in hoping for Trump to prove an economic failure. One such “good” is the total revolution happening in China’s personal income tax code, shockingly ignored by so many. Figure 1 shows the C$565 tax cut that the average white-collar Chinese worker, earning C$17,689 a year, is set to witness. There’s more too if we count mortgage, student loan and child deductions (figure 1).3

Figure 1: Proposed China Personal Income Tax Example, Average White-Collar Worker

That comes on the heels of this spring’s 1% cut in value-added tax (VAT) rates. Combined with income tax relief, we count C$135 billion in cuts this fiscal year alone (figure 2).4

Figure 2: VAT + Personal Income Tax Cuts, 2018 Amount

Granted, there are offsets. For example, Beijing is also vaguely promising reductions in social insurance premiums, but that may be more than offset by the tax authority’s ratcheting up of collections efforts this year. The result could be a net tax hike on this front.

Nevertheless, figure 3 shows the decade-long effect of Chinese President Xi Jinping’s tax cuts on the VAT and personal income fronts. At slow-to-fast growth rates, the cumulative 10-year estimate is C$1.35 trillion to C$2.66 trillion, straddling both sides of Trump’s C$1.97tn package that sent stocks higher in 2017.

Figure 3: Cumulative 10-Year Total, Xi Tax Cuts (Using WisdomTree’s C$135bn Calculation for 2018)

Meanwhile, we present figure 4; China’s exports to the U.S. have been shooting higher in a largely uninterrupted fashion for most of this century.

Figure 4: Annual USD Chinese Exports to the U.S.

The Play

Our TSX-listed dedicated China strategy is the WisdomTree ICBCCS S&P China 500 Index ETF (CHNA.B). It hits broad China with a 9+% earnings yield and tracks China’s S&P 500.5Because it is so broad, it can be used as a single line item for a portfolio’s entire Chinese equity exposure.

While the mass of investors focus on “global trade wars,” few observers are noting Chinese fiscal expansion or, for that matter, big trade deals being signed right now. There’s your edge, contrarian reader.

1Sources: Congressional Budget Office, Publication 49958, Estimated Impact of the American Recovery and Reinvestment Act on Employment and Economic Output in 2014. Chinese stimulus data by The Economist, China Seeks Stimulation, 11/10/08.2Source: Laura Zhou, “China, Japan and South Korea Aim to Speed Up Talks on Free-Trade Agreement to Counter U.S. Tariffs,” South China Morning Post, 9/22/18. 3Average white-collar worker income calculated by Zhaopin Ltd., a career platform similar to Monster.com, as of end-2017. Tax cut calculations by WisdomTree, using the PBoC’s tax proposal that is likely to become law in October. 4See source data beneath Figure 1. 5Sources: Bloomberg, WisdomTree, as of 10/24/18.

Jeff Weniger, CFA serves as Asset Allocation Strategist at WisdomTree. Jeff has a background in fundamental, economic and behavioral analysis for strategic and tactical asset allocation. Prior to joining WisdomTree, he was Director, Senior Strategist with BMO from 2006 to 2017, serving on the Asset Allocation Committee and co-managing the firm’s ETF model portfolios. Jeff has a B.S. in Finance from the University of Florida and an MBA from Notre Dame. He is a CFA charter holder and an active member of the CFA Society of Chicago and the CFA Institute since 2006. He has appeared in various financial publications such as Barron’s and the Wall Street Journal and makes regular appearances on Canada’s Business News Network (BNN) and Wharton Business Radio.

Important Risks Related to this Article

There are risks associated with investing, including possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. The Fund focuses its investments in China, including A-shares, which include risk of the RQFII regime and Stock Connect program, thereby increasing the impact of events and developments associated with the region, which can adversely affect performance. Investments in emerging or offshore markets are generally less liquid and less efficient than investments in developed markets and are subject to additional risks, such as risks of adverse governmental regulation and intervention or political developments. The Fund’s exposure to certain sectors may increases its vulnerability to any single economic or regulatory development related to such sector. As this Fund can have a high concentration in some issuers, the Fund can be adversely impacted by changes affecting those issuers. The Fund will be required to include cash as part of its redemption proceeds which introduces additional risks, particularly due to the potential volatility in the Chinese market and market closures. The Fund invests in the securities included in, or representative of, its index regardless of their investment merit and the Fund does not attempt to outperform its index or take defensive positions in declining markets. Due to the investment strategy of this Fund, it may make higher capital gain distributions than other ETFs. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Is your job failing to provide you with money to spend on the things that you always wanted to have for yourself? Since you most likely have free time other than the typical eight hours of sleep per day, you should use it to earn additional income.

If you need further convincing as to why you should seek to build a source of income aside from the one that your current job provides, you should consider talking to a financial advisor or planner like those from Capstone who can walk you through the nitty-gritty of how to plan out your finances going forward. But if you already want to get straight to it, here’s how you can create a supplementary source of income:

Build an online store

Shopping online has become a common activity for some, especially those with tons of money to spend but don’t want the inconvenience of driving into town. However, instead of settling at becoming an online shopper yourself, why not try selling products via the Internet?

You might want to consider registering a seller account first at an e-commerce platform such as Amazon or eBay. You can set up shop in your chosen e-commerce platform in only a matter of minutes, thus allowing you to focus more on spreading the word about your online store and targeting potential buyers.

Once you’ve established yourself as an online seller, you can then consider creating a dedicated website for your onlinestore where you can have fuller control of all the profit generated by your side business. Just remember to retain your day job for the time being until you can already live comfortably using the earnings that your online store receives.

Work as a Freelance Writer

You may have a knack for writing about anything under the sun, but your current job might find you doing anything but that. However, since you don’t spend your entire day working at your job, you can use your free time in an income-generating way by rekindling your passion for writing and finding work as a freelance writer.

Website owners and bloggers who find very little time to write content – especially if they have a hectic schedule – often hire freelance writers and pay them to create articles and posts. Once you become a freelance writer for a website owner or blogger, your research skills will be put to the test, thus making you learn more about specific topics in a more active way compared to when you stumble upon a random article on the Internet and read it in your spare time. Best of all, you can work anytime you want as a freelance writer. Continue Reading…

The big Canadian banks, and by extension the entire Canadian financial industry, occupy a position of paternalistic authority that too many individual investors respect unquestioningly, and even appreciate to some extent. The industry brilliantly capitalizes on a combination of poor understanding of fees, deep loyalty, and misplaced trust by charging Canadians the highest mutual fund fees in the world. This leaves most Canadian retirement investors with 100% of the market risk but only about 50% of market returns.

The impact of these high (and often unseen) investment fees on Canadian retirement accounts is more than a consumer issue, it is a major social issue of our time.

Government pensions will not be nearly enough to provide a satisfactory retirement lifestyle for most Canadians, and guaranteed employer pensions are rapidly becoming a thing of the past. In order to live well in retirement, you now likely need to build significant savings and make those savings grow through investment. So,while previous generations of Canadians with guaranteed pensions could casually observe the markets from the sidelines, most of us today must participate directly in the markets to secure a comfortable retirement.

In other words, you, and only you, have the burden of responsibility to get investing right. But the structure and practices of the investment industry continue to conspire against the ability of the average investor to succeed, to maximize that retirement nest egg. This compromises not only the financial well-being of individual Canadians, but also the health of our retirement system and of our society as a whole.

But there is good news. There are a growing number of very efficient, low-cost investment products such as index ETFs and services such as online discount brokers and “robo-advisors” that enable Canadians to keep a much larger share of their investment returns where they belong … in their retirement accounts. And these lower-cost products and services are offered by the big banks as well as several independent institutions. But you need to know the basics in order to take advantage of these opportunities and build bigger nest eggs. Continue Reading…

It’s no secret that many Canadians think about escaping the cold winter months for some place warmer. While some may like to spend their vacation days relaxing beside the beach or pool, boomers are increasingly seeking out unforgettable travel experiences.

While embracing bucket list travel might mean trying new things off the beaten path, like driving a Ferrari in Italy, hiking the Inca Trail or helping build clean water wells in Africa, there’s always a risk that adventure could turn into misadventure. A recent TD Insurance survey revealed more than a third of Canadian boomers who travel annually say they or someone they’ve travelled with has had a travel emergency, such as an injury that required a trip to the doctor.

The survey also revealed many boomer travellers report they don’t purchase travel insurance because they’re already covered under their work benefits or credit card. Although existing travel insurance plans may cover certain travel emergencies, it’s important to take the time to review them for any gaps in coverage, especially if you’re planning activities you haven’t tried before, and purchase supplementary coverage if needed.

For Boomer travellers setting out to check off their travel bucket list items, here are a few more pre-travel tips, so your epic adventure can be exactly that:

1.) Follow your interests

What’s on your travel bucket list is very personal and will vary widely depending on your interests. Do you want to test your physical limits by hiking along the Great Wall of China? Do you dream of seeing the annual migration on the Serengeti Plains? Bucket list travel are trips of a lifetime, so take the time to not only decide what you want to see or do, but also properly prepare in advance of your travels.

2.) Pre-departure prep

Proper preparation is key to making your bucket list trip terrific. Prepay or set up autopayments for bills that will be due while you are away. Verify whether you need any vaccinations for where you’re travelling to. Ensure you have enough prescriptions to last the trip. There’s lots to be done ahead of time so that your bucket travel is as dreamy as imagined. Check out TD Insurance’s Travel Checklist for more tips. Continue Reading…

By Penelope Graham, Zoocasa

By Penelope Graham, Zoocasa