Hub Blogs contains fresh contributions written by Financial Independence Hub staff or contributors that have not appeared elsewhere first, or have been modified or customized for the Hub by the original blogger. In contrast, Top Blogs shows links to the best external financial blogs around the world.

Are electric scooters the future of urban transport?

Only time will tell, but at this point, the buzz is huge about these cool vehicles gaining mileage around city streets and sidewalks across the United States and as far away as China.

Bird, Skip, Scoot, Lime and Spin are some of the popular electric scooter rental services giving cars, SUVs and trucks a run for their money, and talk about the economic advantages.

It’s simple, fast and done from your cell phone app. For instance, the Bird company will charge $1 to start each ride and 15 cents per minute after that. The dockless scooters are activated and unlocked via your smartphone, and you get billed by credit card.

Dockless bike and electric scooter rental businesses seem like no-fail methods for big companies and investors to make an easy buck, lots of them. However, oversaturation could become a problem for these modern, eco-friendly modes of urban transportation, and China is one example.

Oversaturation in China?

According to an item in the BBC, in the country that launched the dockless bike phenomenon it has possibly become too much of a good thing. Two of China’s leading bike-sharing companies have yet to turn a profit there, and mountains of abandoned bicycles piled along city sidewalks show that maybe the fad is wearing off.

Some in sunny San Diego, CA, are not worried though and see the investment in scooter and bike share programs as an excellent approach to creating more accessible and livable cities.

LimeBike, based in San Mateo, is being funded by Silicon Valley’s leading VC firm Andreessen Horowitz. The brand is also branching out to Europe and deploying electric scooters, electric-assist bikes and the standard pedal bike. LimeBike is currently available in 46 markets. Continue Reading…

Despite Tuesday’s 3% plunge in US stock markets, Franklin Templeton money managers are optimistic most major asset classes will deliver positive if muted returns in 2019.

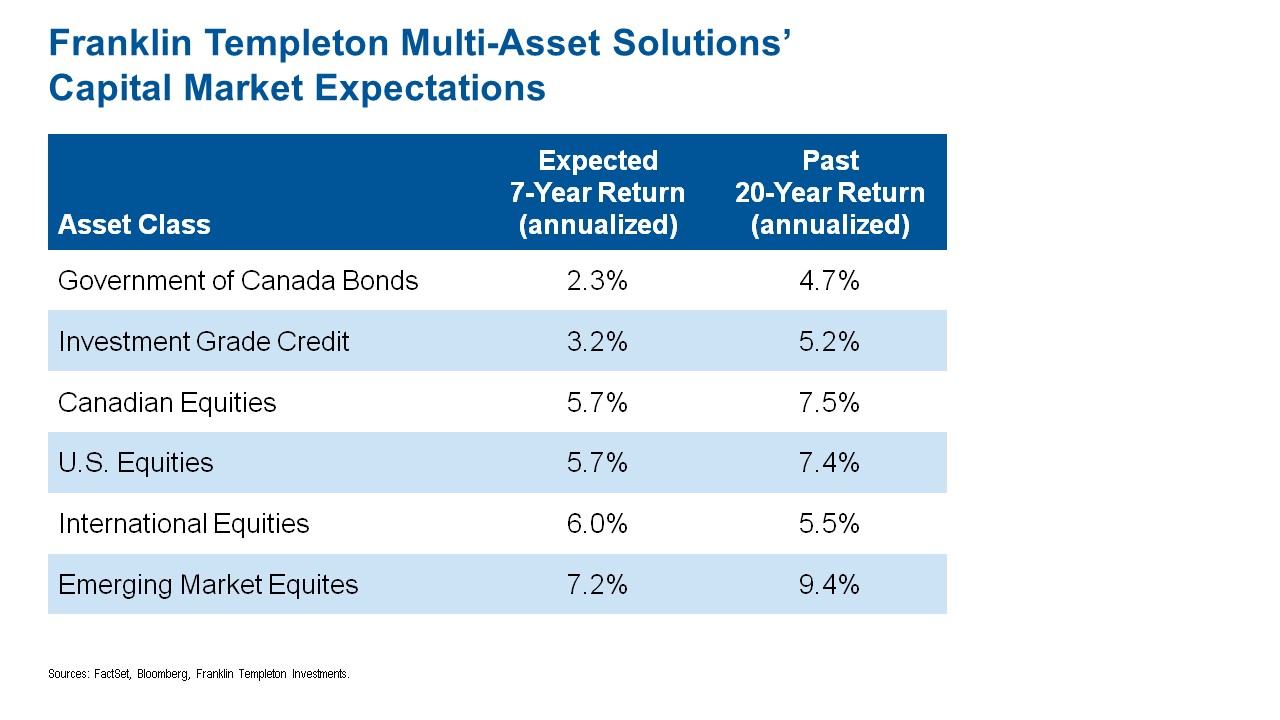

At the 2019 Global Market Outlook event in Toronto, William Yun, New York-based executive vice president for Franklin Templeton Multi-Asset Solutions, projected 7-year annualized returns for Canadian equities of 5.7%, compared to a 7.5% average the last 20 years [as shown in above chart]; 5.7% for U.S. equities (versus 7.4% historically), 6% for international equities (versus 5.5%), and 7.2 versus 9.4% for Emerging Markets. On the fixed income side, he is projecting 2.3% annualized 7-year returns for Government of Canada bonds (versus 4.7% historically the last 20 years), and 3.2% for investment grade corporate bonds (versus 5.2%).

All this is in an environment of continued desyncronized global growth (of 3%) and moderate inflation expectations. Long term, Yun is particularly optimistic about the long term growth of Emerging Markets equities, which at 5% is two-and-a-half times the 2% growth expectation for developed market equities. This optimism is based on positive population growth and labor productivity in Emerging Markets. Globally, inflation “remains muted” and “we don’t see many excesses in the global economy generally.” There are however, some excesses in the U.S. labor market.

More normalized interest rate environment

William Yun, Franklin Templeton Multi-Asset Solutions

Capital spending growth patterns are supportive and trending upwards since the 2016 US election, with the transition from very low interest rates post the financial crisis to a “more normalized interest rate environment.” The opportunity is to reinvest capital to more productive assets, as opposed to allocating to corporate share buybacks.

With respect to central bank balance sheets, markets are normalizing around the world, transitioning from excessive Quantitative Easing to Quantitative Tightening and shrinking balance sheets. Assets quadrupled at the Fed between US$1 trillion in 2008 to $4 trillion today as the Fed committed to buying bonds, with liquidity tapering off. He has similar expectations for the ECB, which has announced the ending of its QE programs, and it’s the same with Japan and China. “Central bankers are pulling back on Quantitative Easing.” There is a “restart of normalization in interest rate policy.”

Rising volatility

Even as the Dow Jones Industrial Average was in the process of tanking almost 800 points Tuesday, Yun predicted rising volatility after a period of relative calm. In that environment, “investing passively [in index products] has been the way to go but we anticipate volatility returning.” With higher interest rates and more volatility, it may be a time for active management, Yun said, acknowledging his own firm’s expertise in active security management.

Emerging Markets gross domestic product (GDP) continues to rise relative to the rest of the world, from 40% in 1990 to 60% in 2017, and Yun expects that percentage to move higher still. The trend is driven by rising consumption growth for the middle class, which benefits industries like consumer staples and consumer discretionary stocks, technology and even investment management.

Emerging Markets are showing reduced reliance on developed markets, which are slowing. Whereas in 2007 eight of the top trade markets were with the United States, in 2017-2018 China has supplanted the US, with 8 of the top 14 destinations.

In short, Yun sees a supportive global market for risk assets but lower returns: positive growth and moderate inflation, with increased volatility.

Ian Riach, Fiduciary Trust Canada

Ian Riach, Chief Investment Officer for Fiduciary Trust Canada and a senior vice president of Franklin Templeton Multi-Asset Solutions, says it makes sense in this environment to make some “dynamic” (i.e. tactical) shifts to long-term Strategic Asset Allocation. Currently, the firm is underweight Canadian equities and Canadian bonds, because the loonie has been getting weaker and Canada is facing a number of challenges ranging from trade to energy to a shrinking manufacturing base, all of which “affects growth going forward.” In the short term, Riach expects short-term interest rates in the United States will be higher than in Canada, “given that they are growing more quickly than us.”

Flat yield curve

Even after the recent rate back-up, “we think Government of Canada bonds are expensive, Continue Reading…

My latest MoneySense Retired Money column looks at a financial planning software platform called Viviplan. You can find the full article by clicking on the highlighted text: What I learned by putting Viviplan to the test.

Viviplan is the third retirement planning package I’ve tested this year, perhaps — as the MoneySense article reveals — the topic is getting all too real for me now that my wife, Ruth, has told her employer she plans to retire when she turns 65 next summer. I’m a year older and have been somewhere between self-employed and semi-retired for most of my 60s.

All these packages deserve consideration and work in more or less similar fashion. To do the job justice, you need to have handy — or at least summary information — such documents as your latest tax returns, brokerage statements, Service Canada CPP and/or OAS projections, as well as having a good grasp of your regular and occasional monthly expenses.

Having most recently performed this exercise with Viviplan — and as one of the users we interviewed for MoneySense relates — it can be a bit scary to see in black and white just how expensive daily living can be. The package won’t let you forget any tiny expense, from pet food to boarding your pet when you’re on vacation (or arranging to hire a neighbour’s teenager, which is what we do if we go away and must leave our cat behind.)

Viviplan calls itself a Robo Planner

Viviplan — which has been dubbed “Canada’s Robo Planner” — is the brainchild of financial planner Rona Birenbaum. Birenbaum also runs a separate fee-for-service financial planning firm called Caring for Clients. I have consulted her for various pieces in the past, particularly about annuities.

Indeed, when I was putting Viviplan through its paces, one of the big questions I had was whether there was a need for us to partly annuitize, seeing as Ruth has no employer-provided Defined Benefit pension at all (just a hefty RRSP), and I have only two modest DB pensions that are not inflation-indexed.

Viviplan’s Morgan Ulmer

Our main question was whether to make up for this lack of employer pensions by at least partially annuitizing, or what Moshe Milevsky and Alexandra McQueen call in the title of their book Pensionize Your Nest Egg. Another author, Fred Vettese in Retirement Income for Life, was in a similar situation when he reached 65 (the same month as I did) and had suggested annuitizing 30% of his nest egg at 65 and doing another 30% at age 75 (assuming CPP at 70). Our question for Viviplan was whether this would make sense for us too, or just for Ruth.

We went back and forth with Calgary-based certified financial planner and product manager Morgan Ulmer (pictured to the right). As she relates in the MoneySense piece, “it’s certainly not necessary,” since at today’s interest rates, Viviplan told her that for us a pure GIC portfolio could get us to where we want to go, with the virtue of more financial flexibility and higher final estate value. Like the other programs, Viviplan recommends delaying CPP till 70 and OAS too if possible.

Annuitize? No wrong decisions and no rush

Partial annuitization for Ruth along the lines of what Vettese suggests would result in a slightly lower estate for our daughter. “With annuities, you are making a choice between legacy and flexibility versus security and longevity protection,” Ulmer said in the plan’s written recommendations, “There are no wrong decisions here, and there is also no rush.” Continue Reading…

It’s no secret that purchasing a home is the largest financial investment for many households, and having a realistic budget is key to maximizing affordability. However, despite the years of careful saving and planning most prospective buyers undertake, there’s one closing cost that can present considerable sticker shock: land transfer tax.

Charged by the provincial government (as well as at the municipal level in the City of Toronto), this levy is calculated based on the total purchase price of the home. It must be paid in cash before the transaction can be completed, and cannot be covered by a home loan or rolled into a mortgage.

Because LTT is based on home price, this means buyers in Ontario’s priciest markets shell out much more for it than others. In fact, according to a recent cost analysis by Zoocasa, a buyer in Toronto would be taxed $27,521 for a home priced at the September average of $864,275. That’s an additional 3.2% of the total purchase price.

In Sault Ste. Marie, however, where the average home price clocks in at a relatively more affordable $164,853, said buyer would pay only $1,374 in tax, representing just 0.8% of the total home price.

However, buyers in the majority of Ontario’s more moderately-priced markets can expect to pay between $5,000 and $7,000 in LTT; someone perusing Kitchener homes for sale, which come at the average price of $479,904, would pay $6,073 in LTT. A buyer of Hamilton real estate would be taxed $6,482 on the average home price of $500,365.

Check out the infographic to the left to see how LTT can vary in housing markets across Ontario:

LTT rebates available for first-time home buyers

Fortunately for those climbing onto the property ladder for the first time, there is some relief from land transfer tax in the form of rebates: The Ontario government will refund $4,000, while the City of Toronto offers $4,475. As well, first-time home buyers paying less than $368,360 on their home – the provincial threshold for LTT – will avoid paying it altogether, a reality in markets such as Saut Se. Marie, Thunder Bay, North Bay, Sudbury, Windsor-Essex, and Kingston.

Top 5 Ontario cities where you’ll pay the most Land Transfer Tax

Just because you retire, your money doesn’t have to.

In the words of Gordon Gecko from the 1987 movie Wall Street, “money never sleeps.” And your money definitely won’t once you leave your job.

Many people are shocked to learn that since we left the conventional work force almost thirty years ago our net worth has actually increased, significantly out-pacing inflation and spending. Reading financial articles about what if retirees run out of money, I get the impression that the authors do not understand that once retired, your money can – and should – continue to work for you.

Working smart, not hard

Once you clock out or walk out of the office for the last time, that doesn’t mean your investments are frozen at that point. The stock market is still functioning and now your “job” is to become your own personal financial manager. Actually, you should have been doing this all along, but if not, start now.

You need to get control of your expenses by tracking your spending daily, as well as annually. This is so easy — only taking minutes a day — and this will open your eyes as to where your money is going. Not only that, but it will give you great confidence to manage your financial future. Every business tracks expenses and you need to do the same. You are the Chief Financial Officer of your retirement.

Income is important, but …

Many people structure their investments for income knowing they need $3,000 or more per month to cover their lifestyle. Which is fine, but inflation will be eating away at those numbers and most likely taxes will do the same. Over time your expenses will rise and your purchasing power will drop. You need protection to cover the increases.

Stocks provide that protection and there is an added bonus; when you sell, capital gains are taxed at a lower rate than ordinary income. Therefore, tilting your investments for growth as compared to income will help protect yourself against future inflation. Plus, it will minimize your tax liability.

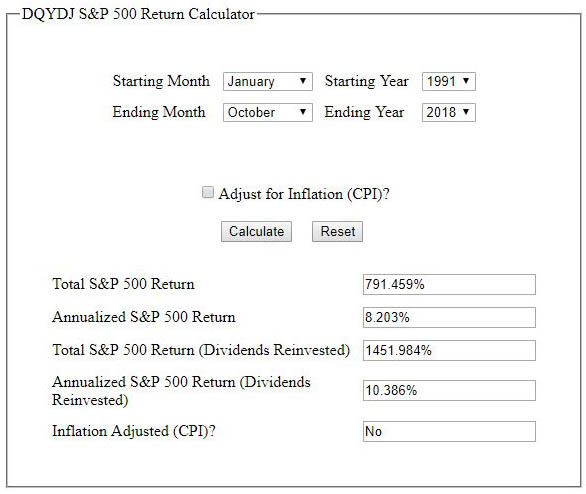

The day we retired the S&P 500 index closed at 312.49. Today, this equates to a better than 10% annual return including dividends.

That’s pretty good for sitting on the beach working on my tan.

Making 10% on our portfolio annually while spending less than 4% of our net worth has allowed our finances to grow out-pacing inflation, while we continue to run around the globe searching for unique and unusual places.

The key is to start as young as you can with as much as you can and let the markets work in your favor. Time is the greatest asset with investing and younger people can utilize this to their advantage.

By Aaron Burdick

By Aaron Burdick