Hub Blogs contains fresh contributions written by Financial Independence Hub staff or contributors that have not appeared elsewhere first, or have been modified or customized for the Hub by the original blogger. In contrast, Top Blogs shows links to the best external financial blogs around the world.

Thinking about boosting your productivity in your home office? Decluttering your office space and creating a tidy working environment might just do the trick. Let’s take a look at some of the benefits of cleaning up your home office.

You won’t get distracted

Working in a clean office means you are less likely to be distracted by different items cluttering up your workspace. It’s quite easy to get distracted by unnecessary objects lying around your desk, so why not remove everything that is not needed and that may distract you from being productive? The truth is that clean offices also make people less stressed simply because mess and clutter can have a bad influence on your focus and make your stress levels jump up to the roof. By making your desks sparklingly clean and moving all the unnecessary stuff to another room, you will definitely see the difference between an organized space and a cluttered work office.

The new trade deal with our neighbours to the south will have wide-reaching effects across all areas of our economy, and housing is no exception. While the agreement is said to be good for our economy overall, it’s not necessarily good news for your ability to afford a home.

What is the USMCA?

Canada recently reached an agreement with the United States and Mexico to replace NAFTA, the decades-old trade agreement that has stood since it was signed by Brian Mulroney, Bill Clinton and Carlos Salinas de Gortari.

The new agreement looks much like the old one, with some changes. Key differences include changes to the way the three countries approach auto manufacturing, fewer restrictions on trade of dairy products, and stronger measures against counterfeiting and media piracy. Like NAFTA, the USMCA makes it possible for the three countries to exchange goods without barriers.

For now, the US, Mexico and Canada will continue trading under the rules of NAFTA. The USMCA will come into effect once it’s ratified by its members, a process that could take months. In the United States, congress won’t vote on ratification until some time next year due to that county’s mid-term elections. Here in Canada, the looming Federal election means that if the USMCA isn’t made official by June, it could be delayed until 2020.

How does this affect Canadian housing?

If you’re wondering how having access to American milk at your local Superstore can possibly affect how much mortgage you can afford, you’re not alone. The implications for home affordability are driven by the market’s reaction to the uncertainty of the negotiation period, the removal of uncertainty brought by a signed agreement, and the actual economic growth that’s expected to occur because of the USMCA once it’s in force.

When the Trump administration demanded to renegotiate “the worst trade deal” ever, the market got spooked. As the trade war intensified, the US threatened to (and did) impose significant tariffs on imports from Canada. With repeated threats from our largest trading partner, there was a real chance that the Canadian economy could be jeopardized. Even though our economy was growing during that time, the Bank of Canada (BoC) was reluctant to raise interest rates, which it would normally do in that situation. Continue Reading…

Investors should avoid making major portfolio changes in advance of the US midterm elections, says former advisor Dale Roberts

By Dale Roberts

Special to the Financial Independence Hub

When I was an advisor at Tangerine Investments I would have many more-than-interesting conversations with clients about short-term economic and political events; especially over Donald Trump. For those of you who do not live under a rock, Donald Trump is the more than controversial President of The United States. Mr. Trump went from real estate magnate and reality TV show host to the most important chair in the world. Many will write and say that the President who resides over the world’s largest and most influential economy and the world’s most powerful armed forces (by many times over) is the most ‘powerful person’ in the world.

So as investors, and for those who manage money, we should pay attention to what the most powerful person on earth does and says, right?

Nope.

As investors, we don’t invest in Presidents or Prime Ministers, we invest in economies and the companies that help drive those economies. With respect to investing in the U.S. the world’s greatest investor, Warren Buffett, often writes …

Never bet against America.

And heading into the Presidential elections of 2016 Mr. Buffett (a vocal Democrat and Hillary Clinton supporter) offered in a Nasdaq interview …

“America works … I’ve said this before, it’ll work wonderfully under Hillary Clinton, and I think it’ll work fine under Donald Trump … For 240 years it’s been a terrible mistake to bet against America, and now is no time to start.”

Ahhh, and there’s the very powerful and destructive key phrase tucked into that sentience; the two words “bet against.” If you make a short-term move, make a guess on a short term event, you’ve just turned investing into betting/gambling. You’ve turned investing into trading. As the saying goes, on the list of the world’s most successful investors you won’t find any traders.

Successful investors have a long-term outlook and a long-term holding period. Boring works. Excitement is for the casino. When asked what is his favourite holding period for a stock or investment Mr. Buffett will reply “forever.”

So don’t listen to me, but you might listen to the word’s greatest investor: who often states that he has never invested based on a short-term economic event or economic prediction or political event or political commentary.

An investor with a well-balanced portfolio will likely invest in US and International markets. When we invest in America we often own market-leading companies such as Apple, Microsoft, Johnson & Johnson, Walmart, Home Depot, McDonald’s, Coke and Pepsico, Costco, Amazon, Google, Netflix, AT &T, Exxon Mobil, Clorox, Facebook, Colgate-Palmolive, Goldman Sachs, and even Mr. Buffett’s conglomerate Berkshire Hathaway.

You’re not investing in Donald Trump, you’re investing in McDonald’s.

Investors can ignore the midterm elections

If you now understand that you don’t need to pay attention to the current President of the United States, you also do not need to pay attention to the next President of the United States, nor do you need to pay attention to the next group of Congresswomen and Congressmen and Senators who will fill the seats of The House of Representatives. You can ignore the midterm elections on Tuesday November 6th, 2018. You can ignore the Presidential election that will follow two years later. Continue Reading…

Questrade’s TV commercials put pressure on fees, as do its new Questwealth Portfolios

As my latest MoneySense Retired Money column explained when it was published early Saturday morning, Questrade Inc., the leading independent Canadian online brokerage, is laying down the gauntlet on fees. You can find the full story by clicking on the highlighted headline here: Questrade’s new robo advisor service showcases rockbottom fees.

For consumers, it’s good news that the new iteration of Questrade’s Portfolio IQ robo adviser service — rebranded Questwealth Portfolios — pushes fees down to around the level of the new Vanguard Asset Allocation ETFs.

That’s somewhere between 0.20% and 0.25%, which is roughly half of what most other robo services charge, and about a tenth of what most retail mutual funds charge.

Questrade Wealth Management was one of three early entrants to the Canadian robo advisor space in 2014 (along with NestWealth.com and Wealthsimple). Until now, its robo service was called Portfolio IQ (PIQ henceforth) but the latter has been rebranded, relaunched and indeed replaced as of Saturday under the new trademarked name Questwealth Portfolios. Questwealth replaces PIQ accounts, according to a press release issued on Nov. 3.

The management fee is 0.25% for Questwealth Portfolios between $1,000 and $99,999, dropping to a very competitive 0.20% for $100,000 or more. These fees are significantly lower than for PIQ, which charged 0.7% under $100,000, 0.6% between $100,000 and $249,000, 0.5% up to $500,000, 0.4% up to $1 million and 0.35% for accounts of a million dollars or more. The average asset-weighted PIQ fee was 0.62%, versus 0.23% for Questwealth Portfolios, lower by a whopping 63%.

For consumers it’s good news that Questrade is slashing its own fees and putting more pressure on the rest of the industry, which is evident from its edgy TV commercials. (With the launch it is releasing a new batch of these often-humorous ads. The screen shot at the top of this blog is from the earlier ads.

How Questwealth Portfolios compare to other Robo services

As I note in the MoneySense column it’s not hard to show how ETFs and robe-based portfolios of ETFs can undercut the notoriously high MERs of Canada’s mutual funds, so the real contest is how the Questwealth Portfolios stack up against the rest of the robo advisors (or indeed, against DIY ETF portfolios held at discount brokers like Questrade itself or any of its (mostly) bank-owned online brokerage arms. Continue Reading…

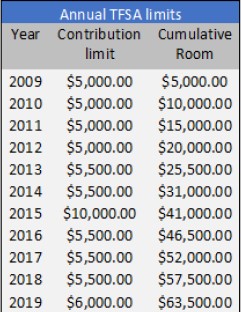

2019 TFSA limits will likely see an increase to $6,000 for 2019, up $500 from $5,500 in 2018. But is taking advantage of the TFSA the right choice for you?

The big story

Most Canadians still don’t understand the TFSA or know if it’s the right type of account for them. More room is great but according to the CRA in 2015, only 10% of Canadians are currently maximizing their TFSA limits1. Also, the CRA has looked to collect over $75 million in past audit penalties over improper use of the TFSA2.

The history

Starting in January 2019, annual TFSA room of $6,000 will be provided to each Canadian resident over the age of 18. Since 2009, Canadian residents have been able to contribute a small portion of their after-tax savings into this tax-free account. If you still are paying taxes on interest, dividends or capital gains on your investments in a non-registered account, it’s time to review the TFSA. If no contributions had been previously made, your TFSA room accumulates over time and a full $63,500 contribution could be made January 1, 2019.

The contribution you make today can grow without any tax implications in the future. If you over contribute, the CRA will penalize you 1% per month on any amount over the approved threshold. A best practice is to check first with the CRA to determine your personal TFSA limit for the calendar year.

Improper use

If you accidently, or purposefully, over-contribute to your TFSA, the CRA will impose a 1% per month penalty on the overage. This may be overstating the obvious, but over-contributing is a bad idea. You would have to reasonably expect your investments to grow higher than 12%/year (assuming simple math with a January 1stcontribution) to break even. Having TFSAs at two or more institutions may be a way you lose track of your contribution room. Ensure you check with the CRA to understand your annual TFSA contribution limit.

Another example of improper use could be frequently trading stocks within the TFSA, aka ‘day trading.’This may be considered a ‘business activity,’ as perceived by the CRA and you could be taxed personally on all the income, dividends and capital gains.

Spousal successor

An important but often overlooked benefit to utilizing a TFSA is as an estate planning feature: the spousal successor declaration. Continue Reading…

By Melanie Saunders

By Melanie Saunders