Hub Blogs contains fresh contributions written by Financial Independence Hub staff or contributors that have not appeared elsewhere first, or have been modified or customized for the Hub by the original blogger. In contrast, Top Blogs shows links to the best external financial blogs around the world.

Money management is essential to help your savings thrive and benefit your [U.S.] retirement accounts. Discover movements to minimize taxable income.

By Dan Coconate

Special to Financial Independence Hub

Navigating the path to a financially secure retirement can often seem like navigating a labyrinth with no exit. With so many potential strategies and considerations, it’s easy to feel overwhelmed. However, efficient tax management is key to unlocking a financially comfortable retirement.

By adeptly managing your taxable income, particularly through individual retirement accounts (IRAs) [or in Canada, RRSPs], you can pave a clear path through the complexities of retirement planning, positioning yourself for a secure, worry-free future. Understanding the necessary movements to minimize taxable income in a retirement account will help you optimize and maximize your retirement savings.

Contribute to a Traditional IRA

Investing in a traditional IRA can be a smart move to effectively reduce your taxable income. Your contributions may be tax deductible, depending on your income and whether your work’s retirement plan also covers your spouse.

The more you contribute to your traditional IRA within the IRS contribution limits, the more you can reduce your taxable income for the year.

Consider a Roth IRA Conversion

A Roth IRA conversion is a strategic financial decision that can secure tax-free income during retirement. When you convert from a traditional IRA to a Roth IRA, you pay taxes on the converted amount in the year of conversion. [Roth IRAs are the U.S. equivalent of Canada’s Tax-Free Savings Accounts or TFSAs] Continue Reading…

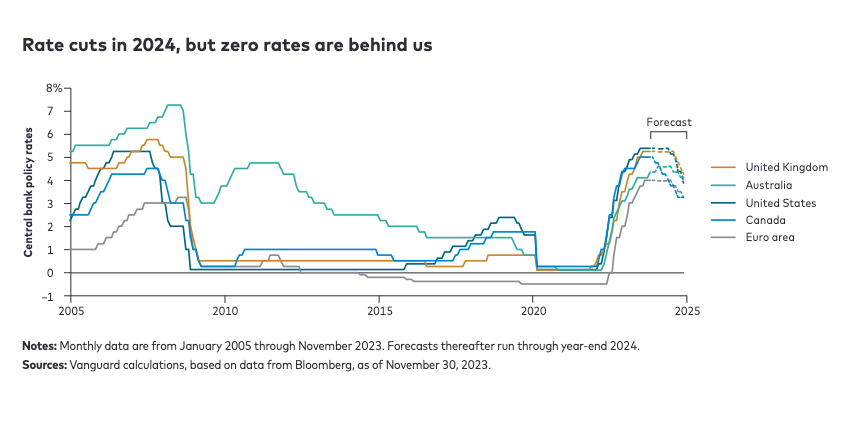

There seems to be some confusion around what to expect for monetary policy in 2024. There’s a strong consensus that cuts are coming, but what is far less certain is how many – and why they are implemented.

Let’s assume that all cuts are of the traditional 25 basis point variety. Since the bank rate is adjusted every six weeks, there will be eight or nine opportunities to adjust it in 2024 in both Canada and the United States.

There are as many as three narratives making the rounds about what might be in store. Each narrative has a combination of rate cuts for monetary policy and corresponding outcomes for the broader economy. I attended a luncheon last week hosted by Franklin Templeton, where senior representatives outlined three possible scenarios with three different narratives accompanying them. A similar perspective was offered earlier this week by the Vanguard Group.

The three narratives are as follows:

#1 We have a soft landing.

The soft landing involves the economy remaining relatively robust, employment remaining strong, delinquency is modest, and rates are normalizing at a level close to but somewhat lower than where they are right now. Most people would suggest that scenario involves no more than two cuts in 2024.

#2 We have a routine recession.

To be more precise, the second narrative involves a garden-variety recession that lasts perhaps a couple of quarters that involves only modest reductions in economic activity over that time frame. Nonetheless, this scenario includes five or six rate cuts to stimulate the economy to the point where things can become stable going forward.

#3 We have a severe recession.

The final narrative involves massive cuts that are made out of desperation to keep the economy from plunging into an abyss. This scenario is not only the most drastic, but also seems to be the least likely. Nonetheless, if things get really ugly, seven, eight or nine rate cuts might be needed to stanch the bleeding. One or more of those cuts might even be for 50 basis points or more.

While I accept the logic associated with all three scenarios, I cannot help but notice that much of the financial services industry is conflating those scenarios in a way that strikes me as being intellectually inconsistent. The financial services industry has long been overly optimistic in the way it portrays outlooks and forecasts. It routinely engages in something I call bullshift, which is the tendency to shift your attention to make you feel bullish about the future.

There can be little doubt that stimulative cuts are positive developments for capital markets. What the industry seems disinclined to acknowledge is that cuts are often made out of desperation. People need to look no further then what happened throughout the entire industrialized world in the first quarter of 2020. Central banks in all major economies cut rates to essentially zero by the end of March of 2020 in the aftermath of the COVID pandemic. At the time it was seen as being both necessary and reasonable, given the severity and breadth of the challenge.

Reining in Inflation

As we all know, inflation became the primary public policy challenge by the beginning of 2022. Central banks needed to take what looked like draconian measures to rein in inflation, which had risen to generational highs and needed to be brought under control lest a sustained period of inflation like what was experienced in the 1970s were to recur. By the end of 2023, inflation is still higher than the high end of the range that is deemed to be acceptable for most central banks.

There is still work to be done, yet many pundits seem eager to take a victory lap, as if a reduction in inflation is somehow akin to bringing inflation under control. Much has been done over the past 20 months, but more work is needed. The admonition that rates will have to stay higher for longer is a very real constraint on economic activity and long-term growth prospects. We head into the new year on the horns of a dilemma. Bond market watchers are now suggesting that rate cuts will come no later than Q2 2024, whereas central bankers are insisting that those cuts will be modest and will only begin in Q3 of 2024 at any rate. They cannot both be right.

It gets worse. Most commentators have taken to suggesting that we will have both a soft landing and five or six rate cuts in the New Year. That strikes me as being fantastic – not to mention intellectually inconsistent. If we have a soft landing, it will likely entail the economy being remarkably resilient as it has been throughout 2023. There is absolutely no reason to have a parade of rate cuts in such an environment.

Stated differently, the financial services industry needs to pick a lane. If it believes we will have a soft landing in 2024, it should also be anticipating a very small number of very modest cuts in the second half of the year. Conversely, if it believes a recession is on the horizon, it should be forecasting multiple cuts only after it is clear a recession is underway. These would likely be needed to stimulate the economy in an environment where inflation will likely be modest as a direct result of economic weakness.

To hear the industry tell it, the economy will remain strong, but we’ll get multiple rate cuts anyway. You can’t have it both ways. I call Bullshift.

John De Goey is a Portfolio Manager with Designed Securities Ltd. (DSL). DSL does not guarantee the accuracy or completeness of the information contained herein, nor does DSL assume any liability for any loss that may result from the reliance by any person upon any such information or opinions.

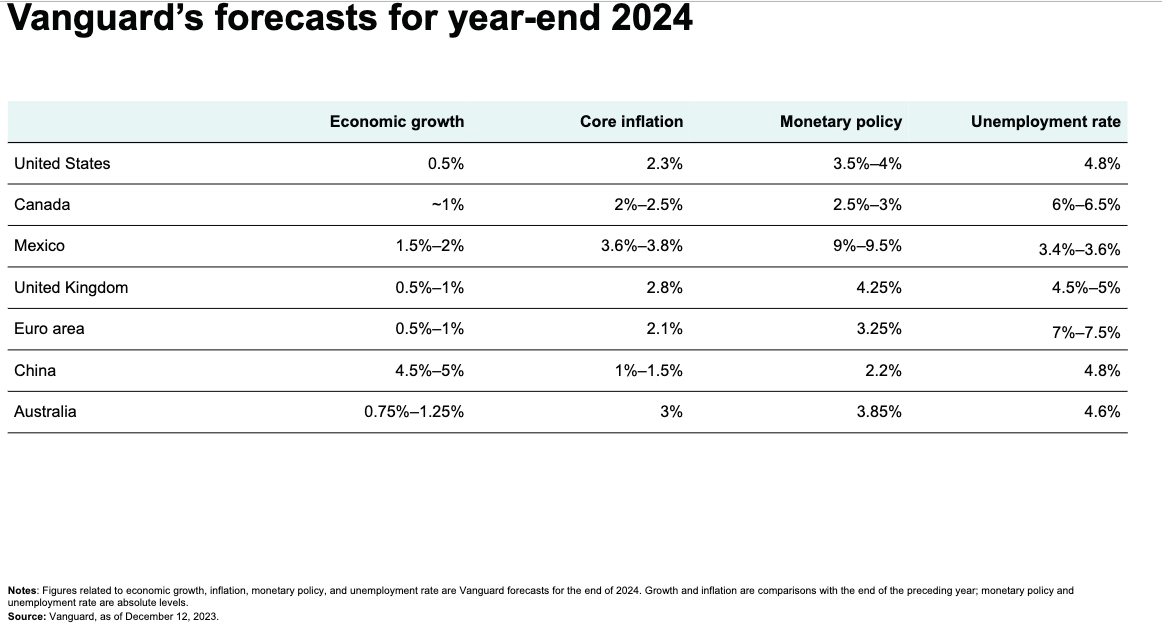

Higher interest rates are here to stay, according to the Vanguard Economic and Market Outlook for 2024, delivered online on Tuesday, Dec. 12. The following is an advance document viewed under embargo and it has been edited down from a Global Summary prepared by Vanguard Global Chief Economist Joseph Davis and the Vanguard global economics team. Anything below in quotes is directly lifted from that document. Otherwise, I have used ellipses and/or paraphrased to make this fit the Hub’s normal blog format. Subheadings are also by Vanguard. At the end of this blog, we have also added a chart about Canada in particular, and projected investment returns in Canada and the rest of the world, supplied by Vanguard Canada.

The main paper begins:

Joseph Davis, Ph.D., Global Chief Economist for Vanguard Group Inc.

“Higher interest rates are here to stay. Even after policy rates recede from their cyclical peaks, in the decade ahead rates will settle at a higher level than we’ve grown accustomed to since the 2008 global financial crisis (GFC). This development ushers in a return to sound money, and the implications for the global economy and financial markets will be profound. Borrowing and savings behavior will reset, capital will be allocated more judiciously, and asset class return expectations will be recalibrated. Vanguard believes that a higher interest rate environment will serve investors well in achieving their long-term financial goals, but the transition may be bumpy.”

Monetary policy will bare its teeth in 2024

“The global economy has proven more resilient than we expected in 2023. This is partly because monetary policy has not been as restrictive as initially thought. Fundamental changes to the global economy have pushed up the neutral rate of interest — the rate at which policy is neither expansionary nor contractionary. Various other factors have blunted the normal channels of monetary policy transmission, including the U.S. fiscal impulse from debt-financed pandemic support and industrial policies, improved household and corporate balance sheets, and tight labor markets that have resulted in real wage growth.

In the U.S., our analysis suggests that these offsets almost entirely counteracted the impact of higher policy interest rates. Outside the U.S., this dynamic is less pronounced. Europe’s predominantly bank-based economy is already flirting with recession, and China’s rebound from the end of COVID-19-related shutdowns has been weaker than expected.

The U.S. exceptionalism is set to fade in 2024. We expect monetary policy to become increasingly restrictive as inflation falls and offsetting forces wane. The economy will experience a mild downturn as a result. This is necessary to finish the job of returning inflation to target. However, there are risks to this view. A “soft landing,” in which inflation returns to target without recession, remains possible, as does a recession that is further delayed.

In Europe, we expect anemic growth as restrictive monetary and fiscal policy lingers, while in China, we expect additional policy stimulus to sustain economic recovery amid increasing external and structural headwinds.”

Zero rates are yesterday’s news

“Barring an immediate 1990s-style productivity boom, a recession is likely a necessary condition to bring down the rate of inflation, through weakening demand for labor and slower wage growth. As central banks feel more confident in inflation’s path toward targets, we expect they will start to cut policy rates in the second half of 2024.

That said, we expect policy rates to settle at a higher level compared with after the GFC and during the COVID-19 pandemic. Vanguard research has found that the equilibrium level of the real interest rate, also known as r-star or r*, has increased, driven primarily by demographics, long-term productivity growth, and higher structural fiscal deficits. This higher interest rate environment will last not months, but years. It is a structural shift that will endure beyond the next business cycle and, in our view, is the single most important financial development since the GFC.”

A return to sound money

“For households and businesses, higher interest rates will limit borrowing, increase the cost of

capital, and encourage saving. For governments, higher rates will force a reassessment of fiscal

outlooks sooner rather than later. The vicious circle of rising deficits and higher interest rates

will accelerate concerns about fiscal sustainability.

Vanguard’s research suggests the window for governments to act on this is closing fast — it is

an issue that must be tackled by this generation, not the next.

For well-diversified investors, the permanence of higher real interest rates is a welcome

development. It provides a solid foundation for long-term risk-adjusted returns. However, as the

transition to higher rates is not yet complete, near-term financial market volatility is likely to

remain elevated.

Bonds are back!

Global bond markets have repriced significantly over the last two years because of the transition

to the new era of higher rates. In our view, bond valuations are now close to fair, with higher

long-term rates more aligned with secularly higher neutral rates. Meanwhile, term premia

have increased as well, driven by elevated inflation and fiscal and monetary outlook

uncertainty.

Despite the potential for near-term volatility, we believe this rise in interest rates is the single

best economic and financial development in 20 years for long-term investors. Our bond

return expectations have increased substantially. Continue Reading…

Jon Chevreau and Canada Podcasts’ Philip Bliss: https://canadaspodcast.com/findependencehub/

By Philip Bliss

Special to Financial Independence Hub

In an age where knowledge is easily accessible, podcasts have emerged as one of the most potent tools for personal development.

Findependence [aka Financial Independence] is a goal many aspire to, but achieving it often requires a solid understanding of money management, investments, and entrepreneurship. This is where podcasts shine, providing a wealth of knowledge and inspiration that can be instrumental in your journey towards financial freedom.

This new tool is particularly valuable in the fast-paced world of entrepreneurship, where the quest for knowledge and inspiration is ceaseless. In this digital age, Canada’s Podcast has emerged as a game-changer, becoming a cornerstone for Canadian entrepreneurial development and a key to enabling Findependence. Let’s explore why these audio/video gems are so critical to the journey of every aspiring entrepreneur.

1.) Education at your Fingertips

Podcasts offer a wide array of financial knowledge, from personal finance basics to advanced investment strategies. By tuning into podcasts, you can learn about budgeting, saving, and investing while going about your daily routine. Whether you’re commuting, exercising, or doing household chores, these audio programs allow you to convert idle time into a valuable learning opportunity.

Some popular finance podcasts like “The Dave Ramsey Show” and “BiggerPockets Money” offer practical advice on budgeting, getting out of debt, and achieving financial freedom. These shows are like having a personal finance mentor guiding you through the intricacies of money management.

2.) Diverse Perspectives and Ideas

Findependence is not a one-size-fits-all goal. Everyone’s journey is unique, and podcasts reflect this diversity. Podcast hosts often bring their personal experiences and perspectives to the table, offering a rich tapestry of ideas and approaches to achieving financial success.

You can listen to real-life stories of people who have achieved findependence, learning from their triumphs and pitfalls. This diversity of experiences can help you tailor your approach to fit your own circumstances and goals.

3.) Investing Insights

For those looking to grow their wealth through investments, podcasts can be a treasure trove of valuable insights. Whether you’re interested in stocks, real estate, cryptocurrencies, or other investment avenues, there’s likely a podcast that caters to your interests.

Podcasts like “Invest Like the Best” and “The Motley Fool” provide deep dives into various investment strategies, market analysis, and expert interviews. By regularly listening to such shows, you can stay updated on market trends and make informed investment decisions.

4.) Motivation and Inspiration

Findependence can be a long and challenging journey. At times, you may find yourself discouraged or unsure about your financial decisions. Podcasts can serve as a source of motivation and inspiration, reminding you of the benefits of findependence and keeping your goals in focus.

Many findependence podcasts share stories of people who have achieved their financial goals against all odds. These tales of perseverance and success can fuel your determination and keep you on track, even when the path seems daunting.

5.) Building a Supportive Community

Podcasts often come with dedicated communities. These communities provide a space to discuss financial topics, share experiences, and seek advice from like-minded individuals. Engaging with these communities can be a valuable source of support as you work towards findependence. Continue Reading…

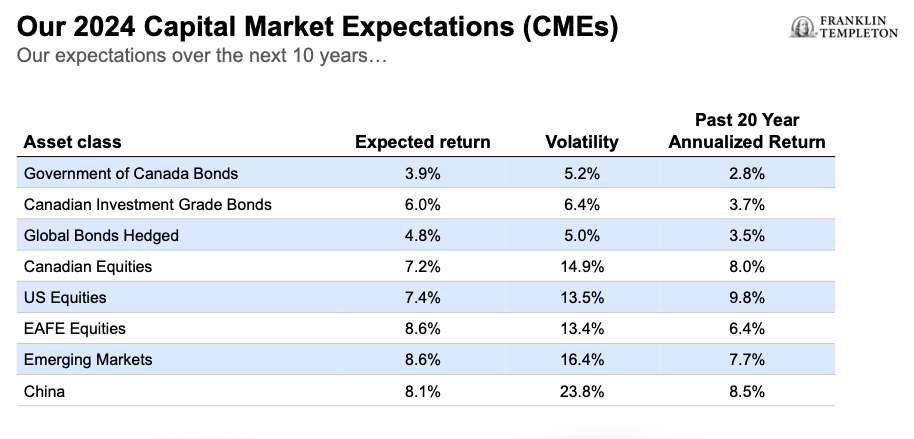

Investors can expect strong positive single-digit returns for the ten years between 2024 and 2034, portfolio managers for Franklin Templeton Investments told advisors on Thursday.

Ian Riach

Speaking at the 2024 Global Investment Outlook in Toronto, portfolio manager Ian Riach said Canadian equities will have expected returns in C$ of 7.2%, a tad below the 7.4% of U.S. equities and 8.6% for both EAFE and Emerging Markets and 8.1% for China. Riach is Senior Vice President and Portfolio Manager for Franklin Templeton Investment Solutions and CIO of Fiduciary Trust Canada.

Fixed-income returns are expected to be in the low single digits: 3.9% for Government of Canada bonds, 6% for investment-grade Canadian bonds and 4.8% for hedged global bonds, again all in C$. See above chart for the Volatility of each of these asset classes, as well as the past 20-year annualized returns for each. From my read of the chart, expected returns of North American equities the next decade are slightly below past 20-year annualized returns but EAFE and Emerging Markets expected returns are slightly higher, with the exception of China.

Fixed-income investors who were dismayed by bond returns in 2022 will no doubt be relieved to see expected future returns of Canadian bonds and global bonds are higher than in the past 20 years. “Expected returns for fixed income have become more attractive; recent volatility [is] expected to subside,” Riach said in the presentation provided to attendees.

Capital markets expectations (CME) are used to set Strategic Asset Allocation, which forms the basis of Franklin Templeton’s long-term strategic mix for portfolios and funds, the document explains: “Portfolio managers then tactically adjust.”

“This year CMEs are generally higher than last year. Primarily due to higher cash and bond yields as a starting point,” the document says.

Global equity returns are expected to revert to longer- term averages and outperform bonds, EAFE equities “look attractive,” and Emerging market equities are expected to outperform developed market equities, albeit with more volatility.

Central banks may have to tolerate higher inflation, but are determined to at least get it closer to target in the short-run. The Bank of Canada does have some room to tolerate a higher rate as its target is more flexible at 1%-3%. This compares to the Fed’s hard-wired 2%. Thus, rates in the US may stay higher for longer to bring inflation down to target

Risks of Recession

Riach described three major broad portfolio themes. The first is that Recession risks are moderating but “reasons for caution remain.” The second is that on interest rates, central banks have reached “Peak policy, but expect higher rates for longer.” The third is that “Among the risks, opportunities exist.” Addressing the narrow market of the top ten stocks in the S&P500 (the Magnificent 7 Big Tech stocks plus United Health, Berkshire Hathaway and ExxonMobi), market breadth should broaden to the rest of the market.

For portfolio positioning, Riach suggested selectively adding to Equities, overweighting U.S. and Emerging markets equities, underweighting Canada and Europe equities, and for Fixed Income,”trimming duration and prefer higher quality corporates.” In short, “a diversified and dynamic approach [is] the most likely path to stable returns.”

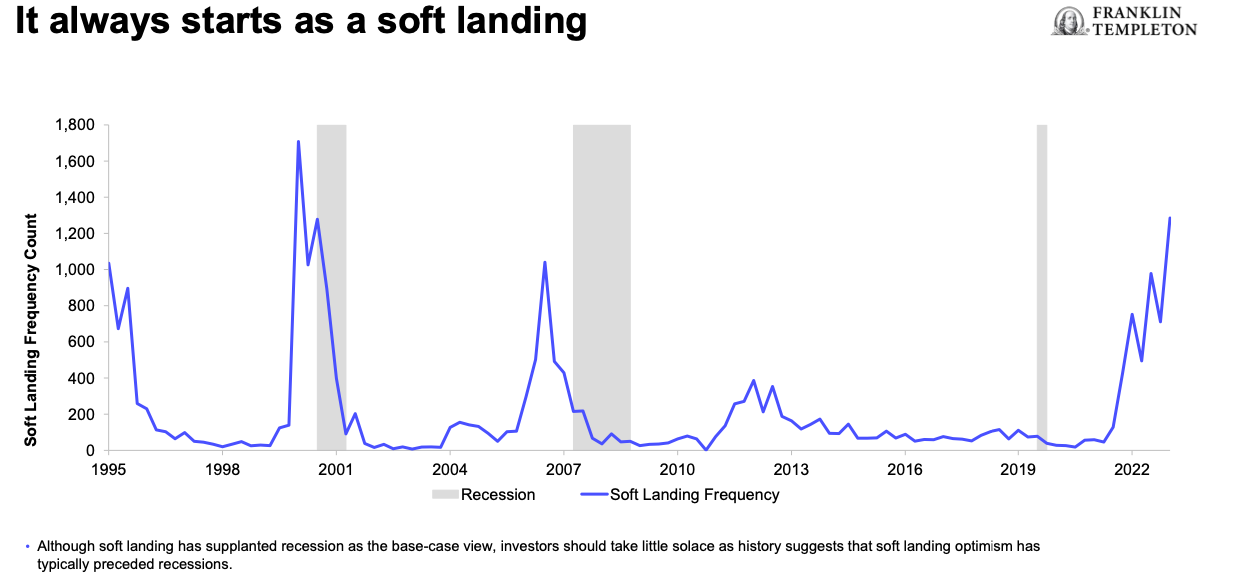

Jeff Schulze, Head of Economic and Market Strategy, ClearBridge Investments (part of Franklin Templeton) gave a presentation titled “Anatomy of a Recession.” A recession always starts as a “soft landing,” as the slide below illustrates. “We’re not out of danger. Leading indicators point to Recession,” he said, “The base case is Recession.” While the S&P500 consensus is for earnings growth, the U.S. GDP is expected to worsen.

He described himself not as a permabear but a permabull, at least until a year ago. If as he expects there’s a “soft landing” with stocks possibly correcting by 15 to 20% in 2024 Schulze would view that as an opportunity to add to U.S. equities in preparation for the next secular bull market.

One of the catalysts will be A.I., not just for the Magnificent 7 but also for the S&P500 laggards. As the chart below illustrates, economic growth often holds up well leading into a recession, with a rapid decline coming only just before the onset of a recession. Continue Reading…