Hub Blogs contains fresh contributions written by Financial Independence Hub staff or contributors that have not appeared elsewhere first, or have been modified or customized for the Hub by the original blogger. In contrast, Top Blogs shows links to the best external financial blogs around the world.

While investing in technology companies can be lucrative, it’s also risky. With great risk comes great reward, so the saying goes. However, not everyone has the luxury of risking their savings. Is there a way to maximize returns while minimizing risks?

Volatility is the Name of the Game in the Tech Sector

The COVID-19 pandemic was a catalyst for exponential growth. Venture capital (VC) activity set records in 2021. In the United States, VC-backed businesses raised around $329.9 billion, almost doubling 2020’s $166.6 billion in funding. Approximately $774.1 billion in annual exit value was created that year.

The potential for high returns is tempting, but this trend has slowed as peoples’ reliance on technology has waned. Startups are burning through their cash reserves. Those looking to make money from the tech sector should be strategic about their investments.

In the tech sector, volatility can make investors disgustingly rich — or cause them to lose everything. Technological advancement, driven by fierce competitiveness, happens fast, frequently disrupting the status quo. This allows unknown disruptors to rise to the top quickly.

Take DeepSeek, for example. A Chinese artificial intelligence company built an open-source large language model (LLM) of the same name to compete with ChatGPT for a fraction of the cost. NVIDIA stock — which has risen 285 times higherover the last 10 years — was down nearly 17% on the day this new competitor was unveiled.

Rumor has it DeepSeek was built for drastically less with subpar technology, which makes its disruption all that more consequential. While analysts expected OpenAI’s revenue would exceed $11.6 billion in 2025, it may not be so lucky. The AI companies dominating the market have just been undercut, affecting investments thought to be relatively safe.

How Rapid Innovation can lead to Substantial Gains

The tech sector thrives on innovation because technology goes hand in hand with modernity. The industry is also fiercely competitive, driving research and development. Continual reinvention provokes disruption, making this landscape fertile ground for dramatic, abrupt growth. Often, firms don’t have to fight hard to break into new markets.

Investing in a Volatile, High-Growth Sector is Risky

Market volatility won’t always work in your favor. Even industry giants — seemingly unshakable leaders — can fall to a previously unknown disruptor. Think back to DeepSeek’s impact on NVIDIA. Everything from changing market conditions to regulatory changes can quickly sour a strong investment.

Take Zoom, for example. Zoom didn’t see widespread adoption until the COVID-19 pandemic when it ousted Skype as the most well-known videoconferencing platform. Its share price peaked at $559 in October 2020. One month later, Pfizer and BioNTech announced a vaccine candidate against COVID-19. The next day, it dropped to $403.58. Since then, it has further plummeted, remaining just above $50 for much of 2023 and 2024. Continue Reading…

Even before the Tariffs threats emerged under Trump 2.0, Canadian seniors were starting to find the economic uncertainty and rising living costs to be unmanageable. No surprise then that many seniors approaching Retirement Age are delaying their exit from the workforce.

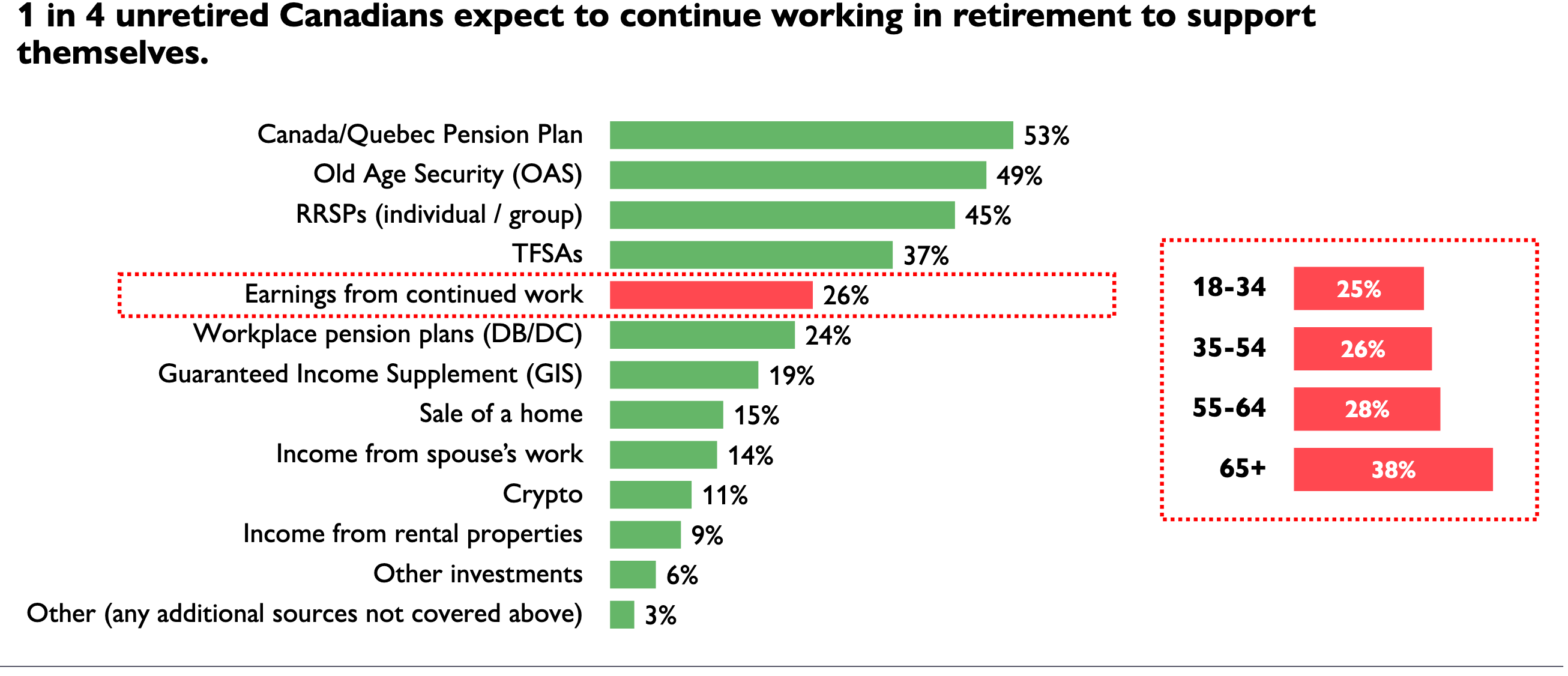

According to a report by HealthCare of Ontario Pension Plan, 28% of unretired Canadians aged 55-64 say they expect to continue working in retirement to support themselves financially. Here’s a screenshot from the HOOPP survey:

The Healthcare of Ontario Pension Plan (HOOPP) commissioned Abacus Data to conduct its sixth annual Canadian Retirement Survey in the spring of 2024. The latest survey finds “persistent high interest rates and a rising cost of living continue to have a significant negative impact on Canadians’ ability to save and manage the cost of daily life, threatening their retirement preparedness.” While all Canadians are struggling, “women and those closest to retirement are especially hard hit with lower savings and higher levels of financial stress.”

While most Canadians are struggling to save amidst a high cost of living, HOOPP finds women are particularly affected. Half (49%) of all Canadian women have less than $5,000 in savings and almost a third (28%) have no savings (compared to 33% and 17% of men, respectively), similar to the 2023 results

The MoneySense column also looks at more recent Retirement surveys that also reveal anxiety about rising costs of living. One is from Bloom Finance Co. Ltd., conducted by founder Ben McCabe after Trump’s Tariffs started to kick in this year.

A Bloom study conducted with Angus Reid found 46% of Canadians thinking of working part-time in Retirement. That’s in line with a Fidelity survey in 2024 that found half of Canadians plan to delay Retirement. According to the Bloom Report [in March 2024], 67% of Canadian homeowners over 55 were concerned their savings would not sustain their quality of life through retirement. Only 29% considered downsizing or alternative living situations to access their home equity earlier than expected. 59% of the same cohort agreed accessing micro-amounts of their home’s equity would help maintain their desired living standard. Continue Reading…

Navigating the complexities of personal finance can be overwhelming, but strategic approaches lead to significant stress reduction. This article delves into the transformative power of Financial Independence, drawing on the expertise of seasoned professionals. Gain actionable insights on how to fortify financial health and secure a more serene state of mind.

Automate Investments and Minimize Unnecessary Expenses

Prioritize Savings to Build Financial Cushion

Build Financial Resilience for Future Security

Automate Finances to Improve Sleep Patterns

Pay Off Debt to Reduce Mental Strain

Diversify Income to Ease Financial Stress

Maintain Safety Net for Peace of Mind

Pursue Financial Independence for Strategic Decisions

Financial Stability Empowers Value-Based Choices

Automate Investments and Minimize Unnecessary Expenses

Before discovering Financial Independence, every surprise expense felt like a mini heart attack. A sudden car repair or an unplanned medical bill would throw my whole month into chaos. I used to track my expenses obsessively, but it felt more like watching a sinking ship than steering it.

When I embraced the principles of Financial Independence, everything changed. I automated my investments to ensure consistent growth, minimized unnecessary expenses, and started treating my net worth like leveling up in a video game. Each step forward brought a tangible sense of progress, like gaining “health points” for life’s challenges.

The real difference came when the unexpected happened. For instance, when my car needed a major repair last year, I calmly paid cash instead of scrambling for a solution. That moment solidified my newfound confidence: I was prepared, not panicked.

Pursuing financial independence has been transformative for my stress levels. It’s not just about the numbers-it’s about turning fear into opportunity and anxiety into control. Every step toward independence feels like reclaiming a piece of peace. — Ahmed Yousuf, Financial Author & SEO Expert Manager, CoinTime

Prioritize Savings to Build Financial Cushion

Breaking free from the paycheck-to-paycheck cycle was one of the most transformative changes in my life, and it significantly reduced my stress and anxiety. Early on, I found myself constantly worrying about covering expenses, with little room to plan ahead. It felt like I was stuck in a cycle of survival, with no opportunity to build stability or security for the future. That constant financial uncertainty weighed heavily on me, affecting my focus, decision-making, and even my health.

The turning point came when I decided to prioritize savings. Even with modest means, I began setting aside a small percentage of each paycheck into a high-yield savings account. At first, it required discipline, sacrificing small luxuries like dining out or unnecessary purchases, but over time, the effort began to pay off. Watching my savings grow gave me a sense of control that I had never felt before. Instead of reacting to emergencies, I started feeling prepared for them.

A defining moment came during a time of professional uncertainty when layoffs were happening at my workplace. Previously, the prospect of losing a job would have left me in a panic, consumed by questions about how to pay for rent, bills, or necessities. This time, however, I had built a financial cushion that gave me peace of mind. Knowing I had several months of living expenses saved, I was able to remain calm, evaluate my options, and focus on finding the right path forward instead of making decisions out of desperation.

That experience taught me the profound power of financial stability. It not only reduced my anxiety but also allowed me to approach challenges with clarity and resilience. Building that security was a key step toward greater personal and professional confidence, reinforcing my commitment to the values of preparation and intentionality. — Sean Smith, CEO & ex Head of HR, Alpas Wellness

Build Financial Resilience for Future Security

Pursuing Financial Independence has had a profoundly positive impact on my stress levels and anxiety by creating a sense of security, freedom, and control over my future. The process of building financial resilience has allowed me to approach challenges with more confidence and reduced the mental burden of living paycheck to paycheck.

How It Reduced Stress:

Peace of Mind: Knowing I have a financial cushion reduces the worry about unexpected expenses, such as medical bills or job loss.

Freedom to Make Choices: Financial independence provides the ability to take calculated risks, whether in career changes, starting a business, or investing.

Clear Goals: The structured process of saving, investing, and reducing debt brings a sense of purpose and direction, alleviating financial uncertainty.

In 2023, a major opportunity arose for me to transition from a salaried role to building my company. While exciting, the leap into entrepreneurship came with inherent risks, including the loss of a stable income. However, my pursuit of financial independence over the years had equipped me with:

An emergency fund covering 12 months of living expenses.

A diversified portfolio generating passive income.

This financial safety net allowed me to focus on growing the business without the anxiety of immediate financial pressure. Instead of stressing over daily operational costs, I was able to make thoughtful decisions about hiring, marketing, and product development. The result was not only professional growth but also improved mental health, as I could prioritize long-term success over short-term survival.

Pursuing financial independence isn’t just about wealth: it’s about reducing uncertainty and empowering yourself to lead a balanced, fulfilling life. It’s one of the most impactful ways to mitigate stress and foster a sense of control. — Kalpi Prasad, Finance Partner, Renown Lending

Automate Finances to Improve Sleep Patterns

Reducing financial stress has profoundly improved my overall well-being, and one of the most noticeable changes has been in my sleep patterns. Before I began focusing on financial stability, my nights were filled with worry, whether it was about unexpected bills, looming due dates, or just the general uncertainty of not having a financial plan. I often found myself lying awake, replaying scenarios about how I might manage in case of emergencies. This mental turmoil not only disrupted my sleep but also impacted my ability to fully show up for others during the day, especially in my personal and professional life.

One of the most transformative steps I took was automating my finances. By creating a system where a portion of my income automatically went into savings and setting up automatic bill payments, I removed the risk of late fees and the constant fear of forgetting due dates. For instance, I prioritized building an emergency fund by setting aside a small percentage of my income every month. Slowly but surely, watching that fund grow gave me a sense of security I hadn’t felt before. My recurring expenses were handled without the stress of constantly monitoring them, which freed up mental space for more meaningful pursuits.

This sense of order allowed me to sleep peacefully for the first time in years. Knowing that my financial house was in order provided a deep sense of relief, allowing me to let go of the endless cycle of “what-ifs” that had previously kept me awake. A pivotal moment for me came when an unexpected family expense arose. In the past, I would have spiraled into worry, trying to figure out how to manage. Instead, I was able to handle the situation calmly, knowing I had prepared for moments like this. That experience reinforced how much my financial independence was improving my life.

Now, I wake up rested, focused, and ready to continue serving others, which has always been my greatest passion. Recovery taught me the importance of building stability in all areas of life, and Financial Independence has become a key part of that journey. It’s a reminder that taking small, consistent steps toward stability creates a foundation for lasting peace and purpose. — Tyler Bowman, Founder & CEO, Brooks Healing Center

Pay off Debt to Reduce Mental Strain

Paying off debt was a transformative milestone in my journey toward Financial Independence and significantly reduced my stress and anxiety. The weight of monthly payments was a constant source of mental strain, creating a cycle of worry that seemed impossible to break. I vividly remember how overwhelming it was to see interest charges pile up, making progress feel out of reach. It often felt like no matter how much I tried, I was stuck in a loop that only deepened my stress.

To address this, I took a methodical approach, prioritizing high-interest debts and creating a structured repayment plan. Each payment became a small victory, reinforcing my determination to push forward. It wasn’t always easy, but focusing on the long-term goal of freedom kept me motivated even during challenging moments. The day I cleared my debt was nothing short of life-changing. The relief I felt was profound, like a weight I had been carrying for years was suddenly gone. Continue Reading…

Dealing with the new administration in Washington won’t be easy, but it may offer opportunities for Canada and for investors. So says Darren Coleman’s guest Dennis Mitchell [pictured left] on the latest episode of the podcast, Two Way Traffic.

Mitchell is CEO and CIO of Starlight Capital, which is a wholly-owned subsidiary of Starlight Investments, a global real estate investment and asset management firm based in Toronto.

Mitchell advises investors to take President Donald Trump “seriously, but not literally.” In lieu of the on-again-off-again tariffs, he singled out an industry like auto manufacturing. “It would take decades for the U.S. to replicate Southern Ontario auto manufacturing,” Mitchell said, implying this won’t happen anytime soon. He also said Canada’s biggest challenge right now involves inter-provincial trade barriers and that Trump presents an opportunity to get this right and diversify our domestic economy. With an eye to prudent investing, the discussion with Coleman and Mitchell explored the following …

Investors should take a hard look at technology because the Trump administration will give the sector carte blanche over the next four years.

Don’t forget Canada has what the world needs in terms of energy, valuable minerals, water, etc.

Investing in the right sector but with the wrong company is a mistake which is why it’s best to seek professional advice.

Today I’m joined by my friend, Dennis Mitchell, CEO and Chief Investment Officer for Starlight Capital in Etobicoke, Ontario. He’s been a fixture of the Canadian investment and U.S. investment landscape for a long time. He’s regularly on BNN and CNBC and has been a successful investor in North America. We’re going to talk about Canada and what we do. We’re dealing with the Trump tariff tantrum and we have a lot of concern, not just in Canada, but globally. Is President Trump using tariffs as a bit of a stick to get his policy decisions implemented? So I want to talk about your impression as a very successful investment manager. How much should we be worrying about this? What action are you taking, or should investors be thinking about? I’ll open it there and get your thoughts and comments and what should we be focused on.

Dennis Mitchell

With Trump, a number of people have said you have to take him seriously, but not literally. And I think that’s great advice for markets as well. Two ways to evaluate Trump’s impact on markets. The first is longer term: what can you expect versus the trajectory we were on before. So longer term, what you can expect is less regulation and more growth. You can expect a focus on manufacturing domestically, driving more foreign investment into the United States. And a focus more on fossil fuels and less on renewable energy. So that’s sort of a longer-term playbook.

As for an investment strategy, to the extent that you need to tweak, it should be tweaked along those longer-term trends. In the short term, you have to ask yourself: How is this? How does Trump usually operate? To put it charitably, he operates chaotically. I think you have to use the volatility that he creates around things like seizing the Panama Canal, acquiring Greenland, turning Gaza into a resort, and implementing tariffs against allies. You have to use the volatility of those announcements and those actions to invest along your long-term trajectory. Because long term we should all be investing in high-quality businesses that are driving free cash flow growth. To the extent that Trump volatility creates a sell-off in any of those types of companies, that’s where you should be allocating your capital to capture those outsized returns that his chaos and volatility create.

Darren Coleman

Many people have not read The Art of the Deal, where he gives a guidebook to the way he’s going to play the game, and it might be a little too early to pick definite winners and losers. There are certain winners and losers, for example, like hybrid cars or electric cars. It looks like some of the subsidies might be going away. It looks like they’re on a real mission to eliminate a lot of government spending, which makes sense given the size of the debt. Are there certain industries right now that you like?

Dennis Mitchell

I think based on not just Trump, but who he’s put in Cabinet, you can look at energy, the traditional fossil fuel energy industry, as an area that’s going to be attractive going forward. Clearly, technology. The tech oligarchs have all lined up, not just at his inauguration, but they’ve all lined up to pay fealty to Trump and work with him. And you have to look at anything being manufactured outside the United States that could conceivably shift to the U.S. I say conceivably, because I think a lot of people are concerned about the auto industry in Canada. It would take decades to replicate the supply chain of southwestern Ontario within the continental US. So that is not an industry investors, in the short and intermediate term, have to worry about in terms of replication and capital flowing outside of the country and into the U.S.

I mentioned his Cabinet, RFK Jr. taking over Health and Human Services. That is of concern for healthcare businesses. You have to think there will be continued downward pressure on drug costs. There will be increased review and oversight and downright skepticism around some of the treatments that exist out there, whether it’s women’s reproductive health, vaccines, even the vaccines that Trump himself spearheaded and created for COVID 19. You have to be concerned about increased oversight and questioning and potential outright bans of some of these industries and some of these treatments and technologies based on who Trump has put in various Cabinet positions. But I think technology and energy, specifically, are two areas that will benefit from a Trump administration. The previous administration was very focused on renewable energy and was not necessarily a big fan and partner of the tech oligarchy.

Darren Coleman

Let’s spend some time on those two industries. On the energy side, in his first day, he said ‘Drill baby drill’ in his speech. So that was pretty clear that fossil fuels are going to be around a long time. And he’s signing agreements with places like Japan for liquid natural gas. Canada had a shot at those agreements, and we decided not to. So if we’re going to see a focus on the energy sector, is that good for American energy companies, or positive for Canadian energy companies?

Dennis Mitchell

I think it’s good for both and the simple reason is that the demand for energy in the U.S. in particular is almost insatiable and will not be met without significant investment on both sides of the border. So if we take a step back, the energy industry, the traditional fossil fuel energy industry in North America, has gone through a significant restructuring over the last 20 years. Gone are the days where guys are going door-to-door and raising capital to drill.

Diversifying your portfolio is a cornerstone of smart investing, reducing risk and potentially enhancing returns. While the Canadian market offers diversification by sector, it represents only about 3% of the world’s capital market. 1

This means that Canadian investors are missing out on a staggering 97% of global investment opportunities. However, the hurdles of currency conversion, foreign exchange costs and currency risk often deter Canadian investors from going global. Enter CDRs, a revolutionary tool that bridges this gap.

What exactly are CDRs?

Canadian Depositary Receipts (CDRs) are financial instruments that represent beneficial ownership in shares of foreign companies but are traded in Canadian dollars on Cboe, a Canadian stock exchange. This innovation simplifies global investing for Canadians, eliminating the need to navigate foreign exchanges and manage currency fluctuations.

Comparing CDRs to traditional Stocks and American Depositary Receipts (ADRs)

While traditional stocks directly represent ownership in companies, CDRs offer a streamlined approach to investing in international firms. Unlike ADRs that trade in U.S. dollars, CDRs cater specifically to Canadians, providing similar exposure to global markets without the complexities of trading at foreign exchanges and in foreign currencies.

A quick look at CDR History

The concept of depositary receipts traces back nearly a century, with ADRs emerging in the 1920s. By 2023, major banks listed over 2400 ADRs in the U.S. market. Canada joined the depositary receipt market in 2021 with offerings focused on U.S.-based companies. In 2025, Bank of Montreal (BMO) introduced its own CDR program, expanding access to global giants from Japan, Germany, Switzerland, Denmark, and the Netherlands.

Benefits of CDRs Explained

Global Access: CDRs open doors to international investment opportunities, broadening investment horizons for Canadian investors.

Currency Risk Management: CDRs mitigate the impact of foreign currency fluctuations on returns through a notional currency hedge.

Fractional Shares: With a starting price of around CAD $10, investors can afford fractional exposure to shares of otherwise expensive global companies.

Diversification: CDRs enable effortless geographic diversification, reducing reliance on any single market.

Understanding CDR Features

Currency Efficiency: CDRs allow Canadians to get exposure to global stocks in Canadian dollars, eliminating currency conversion costs.

Currency Hedge: CDRs minimize the impact of currency fluctuations while reflecting the performance of the underlying foreign company.

Fractional Exposure: Affordable entry-point to high-priced stocks as CDRs are generally issued at a price lower than the underlying share effectively providing Canadians with fractional exposure to listed stocks of large global companies.

Dividends: Investors will be entitled to any distributions paid on the underlying shares in Canadian dollars proportional to the number of underlying shares to which they are entitled. Taxes on distributions may be withheld by the CDR underlying company’s local or national tax authority. Whether distributions, such as dividends, are subject to foreign withholding tax in the same manner as if the underlying share were directly held by the investor will vary by jurisdiction Since the dividends are paid in Canadian dollars, investors do not have to subsequently go through the process of any currency conversion.

Market Accessibility: CDRs trade seamlessly on a Canadian exchange, ensuring ease of buying and selling.

How do CDRs work in practice?

Each series of CDRs provides economic exposure corresponding to a number of underlying shares. The specific number of shares that each series of CDRs represents is called the CDR ratio. For example, if the CDR ratio for a particular series is 0.50, this means that such series of CDR represent 0.50, or half, of a company share, so an investor would need to purchase 2 CDRs of the series to obtain the economic exposure corresponding to 1 underlying share. The CDR ratio for each series of CDRs is adjusted daily to provide the notional currency hedge as the foreign currency increases/decreases in value to the Canadian dollar. Continue Reading…