Hub Blogs contains fresh contributions written by Financial Independence Hub staff or contributors that have not appeared elsewhere first, or have been modified or customized for the Hub by the original blogger. In contrast, Top Blogs shows links to the best external financial blogs around the world.

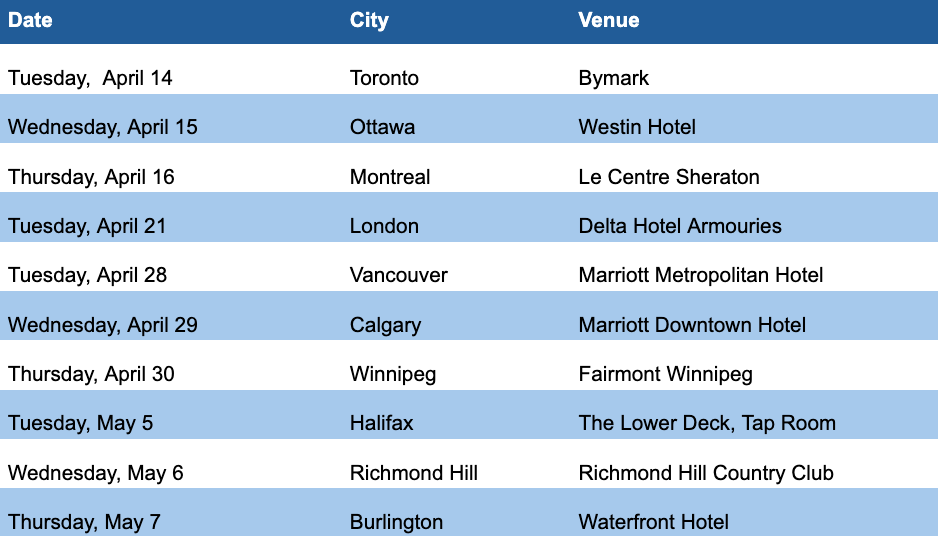

On Tuesday, I attended the Toronto instalment of BMO ETFs’ Spring Road Tour, the first of a 10-city Canadian tour that extends into early May.

The title is We’ve got you covered, which is a sly allusion to one of the main themes of the series: Covered Call ETFs.

Aimed primarily at financial advisors, the sessions are roughly an hour long, coinciding either with breakfast or lunch, depending on the city. There are three main segments:

Bipan Rai, Head of ETFs & Alternatives Strategy, provides insights into BMO’s current macroeconomic outlook, including positioning across asset classes and risk models

Jimmy Xu, Head, Liquid Alts and Non linear ETFs, manager of BMO’s flagship Covered Call ETFs, discusss these innovative solutions designed to help clients meet their cash flow needs while maximizing long term growth.

The road show ends with an introduction to BMO’s new Portfolio Consulting Services, designed to help advisors navigate an increasingly complex investment landscape. Senior Portfolio Consultant, Hilly Cutler shares how BMO supports advisors in optimizing their model portfolios—reducing costs, enhancing diversification, and managing risk as CRM3 approaches.

As the chart below summarizes, the road shows ends in Burlington on May 7th:

Except the Toronto event, which was a breakfast session, the other sessions all begin at either 12 pm or 1 pm. Below we reproduce some of the slides presented at the show.

Current Market outlook and Positioning by Bipan Rai

Bipan Rai, BMO ETFs

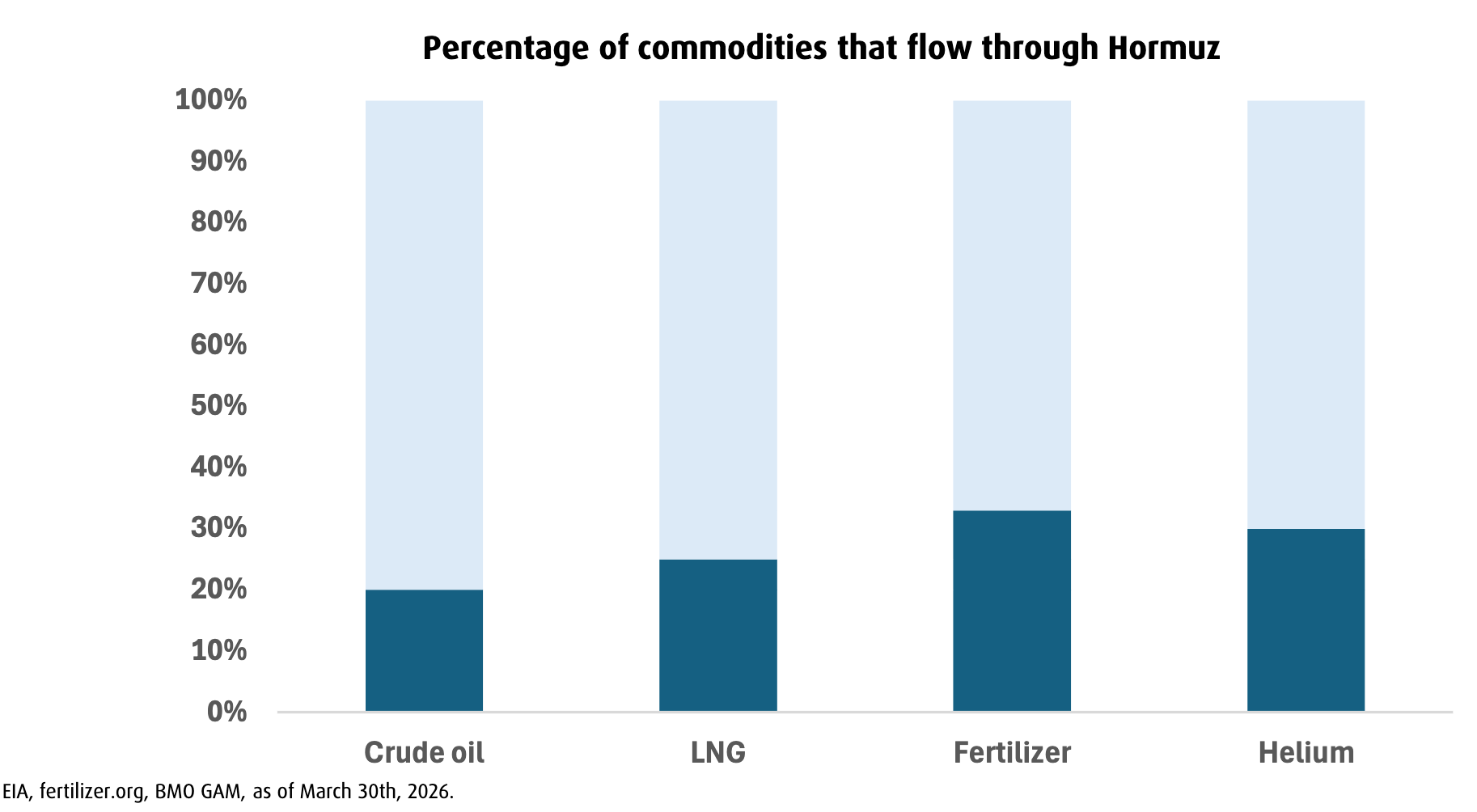

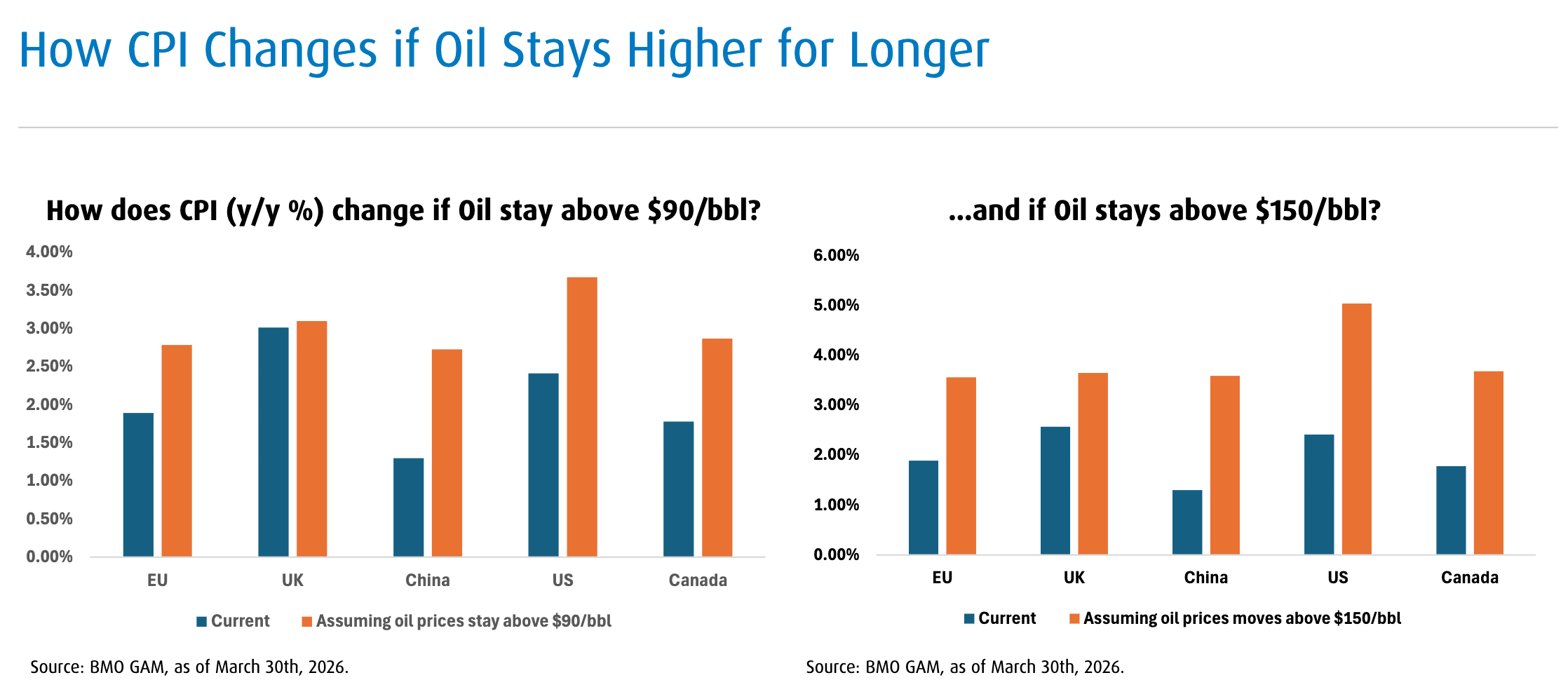

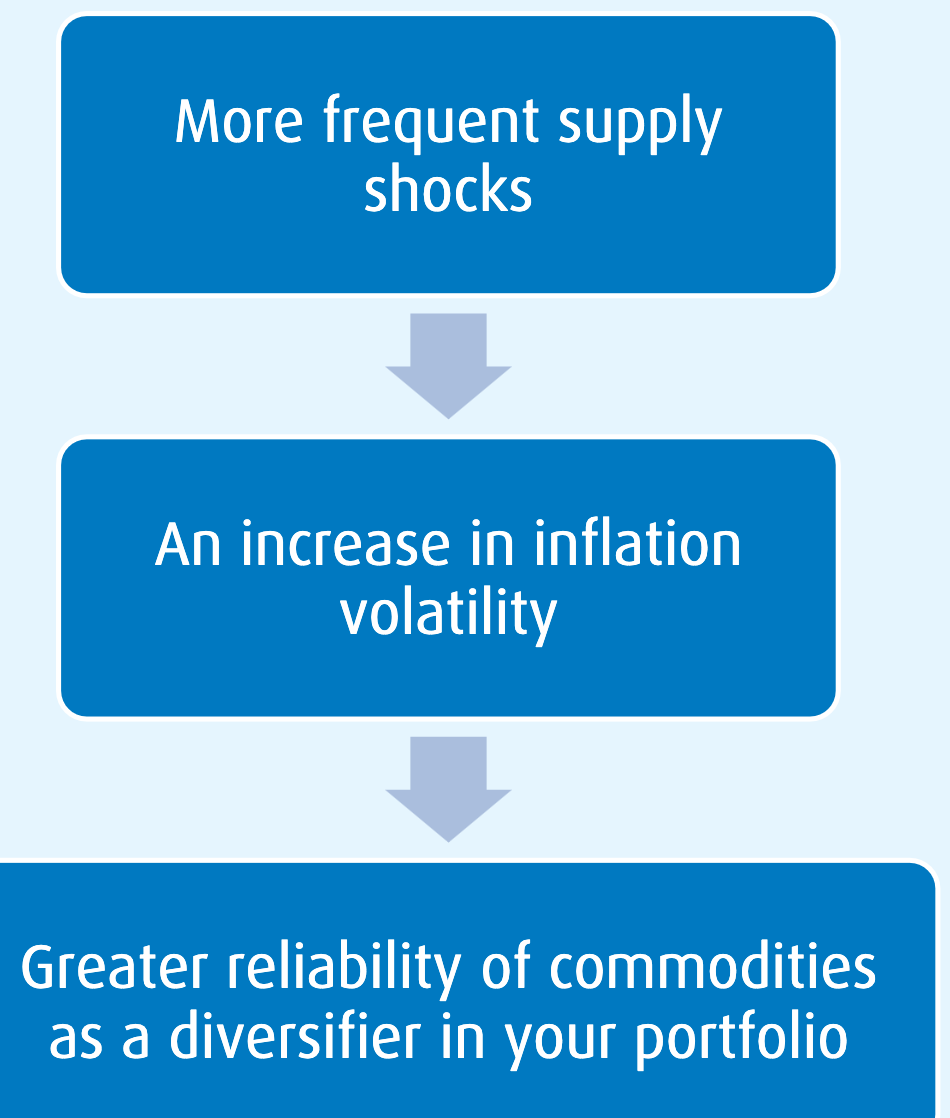

The sessions kick off with a current market outlook delivered by Bipan Rai, who focused on the impacts of the ongoing Iran war, which began at the end of February. He confessed to having a few sleepless nights about the closing of the Hormuz Strait. Not surprisingly most investors suffered negative returns in both stocks and bonds during March. Hormuz matters for the macroeconomic picture, not just because of oil, but also because of Liquid Natural Gas, fertilizers and Helium: the latter helps cool AI systems. (shown below).

Rai also showed the following two charts, which illustrate how the Consumer Price Index changes the longer the price of oil stays higher. The longer the Strait is closed or traffic severely constrained, the more it will create inflation and create risks to economic growth.

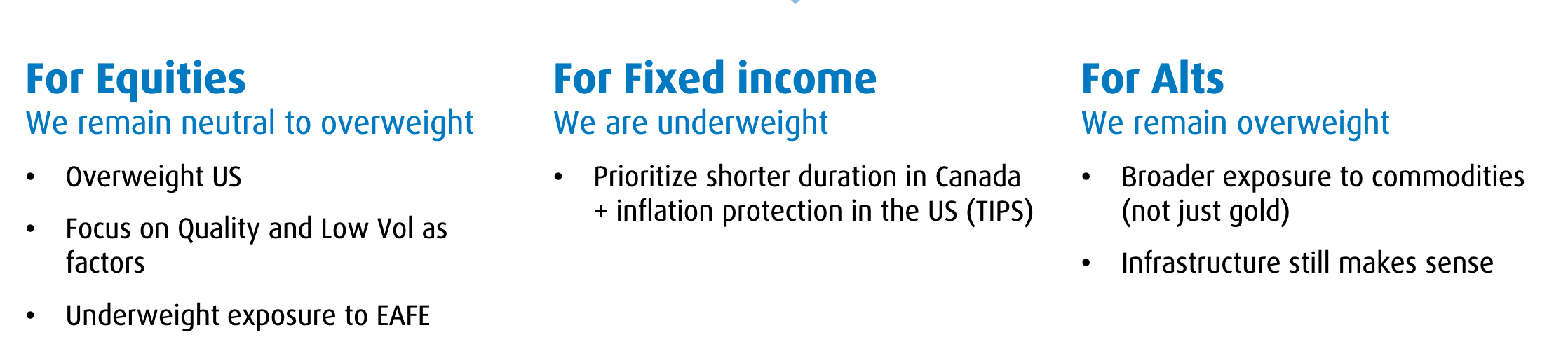

If the price of Oil does stay higher for longer, Rai commented that investors may want to take a more defensive tilt to equities, emphasize quality and low volatility as factors, diversify with Treasury Inflation Protected Securities and embrace broad commodities. BMO has of course ETFs for all of these: such as ZTIP (BMO Short-term US TIPS Index ETF) or the new ZCOM for broad commodity exposure.

Rai’s “big takeaway” is that while Commodities are the “source of the shock,” they also “benefit from supply constraints, fiscal demand and de-globalization.”

Knowing that Inflation risks are “to the upside” and “growth risks are to the downside” Rai concludes that “We are most likely migrating from a ‘reflation’ to ‘mild stagflation.’ ”

He says we are likely in a transition from Strong Growth and High Inflation to Slower Growth and High Inflation, while North American banks are “likely to keep rates on hold.”

As a result, as shown below, BMO is neutral to overweight Equities, underweight Fixed Income, and overweight Alternatives:

Jimmy Xu on the Benefits of Covered Call ETFs

Jimmy Xu, CFA, BMO ETFs

The second talk is by Jimmy Xu, Head of Liquid Alts and Non linear ETFs. His focus was on Covered Call ETFs, which BMO has pioneered in the Canadian market. While investors often buy covered call ETFs just for yield, yield is not the most important consideration, Xu said. “Chasing yield is the quickest way to have unstable income, capital erosion and unhappy clients.” Continue Reading…

I’ve noticed a flurry of articles recently about how investors, including nearing or in the Retirement Risk Zone, might consider moving beyond the traditional 60/40 balanced portfolio of stocks and bonds to consider multiple alternative asset classes.

Indeed, here at FindependenceHub.com we have in the past week run two blogs on specific alternative assets classes: Gold and Bitcoin.

Click on the following headlines to read them if you missed them the first time around:

Admittedly both blogs have a strong point of view that comes from the respective authors. It happens that these two bloggers don’t think much of Gold and Bitcoin respectively. I value their opinion and felt it was worth passing along to readers, who can make their own judgements. Personally, I’ve always believed 5% in Gold or Precious Metals bullion and/or mining stocks is a risk worth taking. I’m a little more skeptical about cryptocurrency but have written in the past that for those inclined to take a flyer on Bitcoin, a 1 or 2% position could work. That 1% could soar and become 10% or more of a total portfolio but it’s also possible that it might indeed descend to zero.

The rest of this blog canvases a baker’s dozen of financial experts and business owners and you’ll see that several of them take a stance on gold and bitcoin, both positively and negatively, as well as numerous other asset classes, such as real estate, private equity, hedge funds and many more.

With the assistance of Featured.com, which has been supplying Findependence Hub with quality content for several years, we recently polled a number of these experts on LinkedIn, as you can see by clicking on their profiles below.

Here’s how we posed the question:

Beyond traditional stocks and bonds, represented in Balanced ETFs, what, if any, alternative asset classes do you recommend, and in what proportions? For example: precious metals (gold or silver bullion or related stocks, or ETFs holding the same), commodities in general, Bitcoin, Ethereum and other cryptocurrencies, real estate held directly or via REITs or certain publicly traded stocks, or any other alternatives not mentioned here, such as Private Equity or Hedge Funds.

1. I recommend gold primarily as geopolitical and inflation insurance, not as a growth asset. Allocate 5-10% of your portfolio to gold via ETFs like GLD or physical bullion if you have secure storage. Silver is more volatile and industrial, so treat it as a smaller speculative position (2-3%) if at all. Gold doesn’t pay dividends or interest, so it’s dead weight in a bull market, but it’s the ultimate “crisis hedge” when currencies or governments misbehave.

2. Direct real estate ownership is capital-intensive and illiquid, so for most investors, publicly traded REITs (Real Estate Investment Trusts) are the smarter play. They provide exposure to commercial, residential, or industrial property with daily liquidity and mandatory dividend payouts. I prefer diversified REIT ETFs like VNQ. This gives you inflation protection (rents rise with prices) and income generation without the headache of being a landlord. Avoid over-concentration here; real estate correlates heavily with the broader economy during downturns.

3. Crypto is not an investment; it’s a volatility lottery ticket with a philosophical thesis. I recommend limiting exposure to 2-5% of your portfolio, and only in the “blue chips” (Bitcoin and Ethereum). Treat this as venture capital: money you can afford to lose entirely. Do not buy crypto with debt, and do not FOMO into altcoins. Store it in a hardware wallet (Ledger, Trezor) if you hold significant amounts; exchanges are not banks. This allocation satisfies your urge to participate in the “future of finance” without risking your retirement if it all goes to zero.

4. Commodities (oil, natural gas, agricultural products) via ETFs like DBC provide inflation protection and diversification, but they are mean-reverting and volatile. Allocate 3-5% as a tactical hedge, especially during inflationary periods. Avoid direct futures contracts unless you are a professional; the contango and rollover costs will eat you alive.

5. Unless you are an accredited investor with $10M+ in liquid net worth, private equity and hedge funds are legally and financially inaccessible or impractical. They charge egregious fees (2% management + 20% performance), lock up your capital for years, and studies show most underperform public markets after fees. If you insist, access them via interval funds or publicly traded BDCs (Business Development Companies), but understand you are paying for illiquidity and complexity, not guaranteed outperformance. — Lyle Solomon, Principal Attorney, Oak View Law Group

Alternative investments should represent twenty per cent of an investor’s total portfolio. In terms of specific allocations, I recommend ten percent in physical gold as a hedge against loss or theft, five percent in real estate investment trusts (REITs) for income generation and three percent in Bitcoin for growth opportunities. Finally, I suggest two per cent be allocated to private equity for both capital gains and diversification purposes. A combination of these types of alternative investments will help protect investors from future inflationary pressures and contribute greatly to their long term performance. Geremy Yamamoto, Founder, Eazy House Sale

Put the most money into things you understand best

My bigger principle is this: Put the most money into the things you understand best.

In my case, that has always been real estate and housing because I know how value gets created there. I know what distress looks like. I know where the discount comes from. I know how people get in trouble. That matters. The more removed an asset is from your real-world understanding, the smaller it should probably be.

And one more thing. Liquidity matters. A lot. People forget that. An investment may look great on paper until you need cash and cannot get to it without taking a beating. That is why I like keeping things simple and staying out of anything that locks you up unless the reward is clearly worth it. — Don Wede, CEO, Heartland Funding Inc.

I’ll break the answer into two parts depending on what your goals are. Growing your assets is one thing, turning your capital into a lifetime income that never runs out is another and that is the #1 financial concern of the 50+ age group.

Purchasing Power Protection is the new Growth strategy:

Historically we used to achieve stable growth by balancing a risk-on asset class (equities) with a risk-off asset class (bonds). In good times the equities flew and the bonds did little; in bad times the bond performance offset declines in equities.

The problem is that in inflationary times, both fall. Inflation undermines the economics of established businesses which have to compete for limited resources that are increasing in price. Positioning for scarcity can insulate you against these circumstances. Gold, Silver and even Bitcoin are the most liquid scarce assets on the planet but they don’t move uniformly. Backing a portfolio with a scarce risk-on asset such as Silver or Bitcoin — while having the majority in a reliable, but occasionally boring, asset like gold — now gives you balance over the longer term. A 30/70 split seems to be the sweet spot.

Assets run out, Lifetime Income is forever:

70% of savers worry about one thing above all others. Can I afford my ideal lifestyle now at the risk of poverty if I live 25+ years? Not everyone will live 25+ years but if I spend now then I am betting against my own longevity. Insurers capitalize on this risk by pooling lives together and promising annuitants a fixed income for life. But fixed incomes lock in the loss of purchasing power. Your lifestyle is going to degrade over time.

It wasn’t always this way. Just over a century ago, 50% of U.S. households joined a longevity risk-sharing arrangement called a Tontine. Recent legislation has enabled modern Tontine Trusts which can be backed by assets that can resist inflation. The Tontine Trusts use your preferred assets to pay you a monthly income for life. When a member dies, their leftover assets top-up the trusts of survivors, typically enabling their monthly income to increase.

So the question the reader really needs to decide upon is: What matters most? The balance of the account or the lifestyle that I always want to enjoy. For generations past, the answer was not to play the markets but rather to invest in yourself.

[Potentially there is a far larger article here, contact us if you want to offer readers a $250 bonus and a similar reward for yourself] — Dean McClelland, Founder/CEO, Tontine Trust Europe KB Continue Reading…

A month ago, I wrote about how the cycles pointed out by Kuznets, Kondratieff, and Minsky, combined with the writings of Joseph Schumpeter seemed to be coming together at the same time. Now that the war in Iran is nearly a month old, it seems the match has been lit that will set the frightening confluence ablaze. It sure looks like we’re in a credit bubble that is beginning to burst.

The challenge when writing about major developments is to sound calm and purposeful when the natural inclination might be to be more animated. How to get people to take urgent action without coming across as an over-the-top doomsayer?

To begin, I need to stress that I do not see myself as a pessimist. I’ve been speaking to college students throughout southern Ontario for the past few months and when I tell them about something I call Bullshift (the optimism bias fomented by the financial services industry), they often ask if I’m not being biased and overly gloomy. I respond both with evidence and by conceding that everyone has biases, so their allegations against me, while not incorrect, are nonetheless likely to be overstated. My view is that better wealth decisions are made using facts, critical thinking and a dash of skepticism regarding the finance industry’s motives.

If Iran war lingers on, credit markets will be stressed

There are multiple indicators that are now showing credit markets in a state of high stress. The longer the war in Iran persists, the worse the situation is likely to become. As such, here are a few things you could do immediately to reduce your exposure to credit:

1.) If you have not already done so, build an emergency fund. Many people use the equity in their home for this. The caveat here is that real estate prices are likely to drop in the short term, as well, so be careful. Where possible, consider setting aside money in a high-yield savings account for emergencies. When you’re financially cushioned, you’re less likely to rely on more punitive alternatives when money is tight. Continue Reading…

Retirement may last longer than you expect. The question is: is your portfolio built to keep up?

Image courtesy BMO ETFs/Getty Images

By Alain Desbiens, Vice-Chair BMO ETFs

(Sponsor Blog)

Canada is undergoing a profound demographic transformation that will influence the nation’s economic trajectory and long‑term investment landscape for decades to come. By 2036, Canadians aged 65 and older will account for roughly 23% of the population, up from approximately 19% today. 1

This aging shift is propelled by three powerful forces: rising life expectancy, persistently low birth rates, and immigration serving as the country’s primary source of population growth. Together, these drivers are reshaping not only the size and composition of Canada’s population but also the way investors and financial professionals must approach planning and portfolio construction.

For investors, these demographic changes create a dual reality. On one hand, the economy faces challenges such as higher healthcare and social‑support spending, and increasing strain on retirement income systems. On the other hand, new long‑horizon opportunities are emerging.

Sectors tied to aging populations, innovation in healthcare, longevity planning, and intergenerational wealth transfer all stand to benefit. Exchange‑traded funds (ETFs), with their cost‑effectiveness, diversification, and transparency, offer an efficient toolkit for capturing these evolving trends.

Key Demographic Trends

1.) Aging Profile & Generational Mix

Baby Boomers still represent about one quarter of Canada’s population, but by 2029, Millennials are projected to surpass Boomers in absolute numbers. 2 This generational shift will reshape demand across housing, consumption, and financial services. Millennials tend to prefer digital-first advice, sustainable investing, and simple yet sophisticated products — including ETFs — while Boomers continue to prioritize income generation, capital preservation, and tax‑efficient3 decumulation strategies. This changing balance in generational influence will increasingly dictate the types of investment solutions that gain traction in the market.

2.) Retirement Wave

Canada is entering a period where record numbers of Boomers are exiting the workforce and see increasing need for accumulation and decumulation strategies, and a higher demand for financial, will and decumulation strategies.

3.) Longevity Realities

Canadians are living longer than ever before, with meaningful implications for retirement planning.

Women 65+: Over half are expected to live to age 90. 4

Men 65+: More than half reach age 90 as well, though only about 39 per 1,000 do so without a major critical illness. 5

FP Canada/IQPF: A 50-60-70‑year‑old has roughly a 25% probability of living to age 94 (men) or 96 (women).6

This extended lifespan introduces significant longevity risk: the risk of outliving one’s capital. Financial plans must now be stress‑tested for longer retirement horizons, rising living costs, and variable health outcomes.

4.) Rising Costs for Aging‑in‑Place & Care

Healthcare inflation, long‑term care, and home‑care services are expected to grow sharply. These realities underline the need for specialized insurance solutions, inflation‑aware portfolios, and steady income vehicles that can sustain retirees across multi‑decade retirement periods.

5.) Wealth Distribution & Investor Segmentation

Canada is on the cusp of a major wealth transition:

Gen X is set to surpass Boomers in total net worth. 7

An estimated $450 billion will transfer to Gen X over the next decade.8

Total household wealth is projected to reach $10 trillion by 2030, reshaping investor behavior, risk profile8, and demand for advice.9

The Bottom Line

Canada’s aging demographic is more than a statistic: it is a structural force that will shape markets, spending patterns, and investment requirements. Investors who proactively position for these changes can build portfolios that are both resilient and growth‑oriented. With their flexibility, transparency, and broad exposure to demographic‑driven themes, ETFs remain one of the most effective vehicles for navigating this new era.

ETF Investment Opportunities

1.) Income Solutions for Retirees

• Longer lifespans + market volatility = demand for stable, tax-efficient income

If retirement is on the horizon, now is the time to look beyond when you plan to stop working and focus on how long your portfolio will need to support you. Longer lifespans mean portfolios must balance growth, income, and flexibility before the first paycheque replacement ever begins. Reviewing your asset mix, understanding your future income needs, and considering simple, diversified ETF solutions today can help reduce stress and create more confidence tomorrow. The years leading up to retirement aren’t just a finish line, they’re the foundation for decades ahead.

Want to learn more? Join Alain Desbiens and host Michelle Allen as they explore why longer retirements demand smarter strategies: inflation-aware portfolios and steady income that lasts decades, not just years. Listen to the podcast episode now!

8: Risk Profile – Comprised of a client’s risk tolerance (i.e., client’s willingness to accept risk) and risk capacity (i.e., a client’s ability to endure potential financial loss).

Alain Desbiens is Vice Chair, BMO ETFs. Alain brings more than 30 years of financial services experience to his new role. A seasoned financial expert and former broker, Alain has raised awareness of ETF benefits among advisors, direct and institutional clients through both individual discussions and impactful presentations. Alain is also active in multiple media formats helping provide insights on both the industry and investments. Over his career, Alain held roles as wholesaler, sales manager, branch manager, and investment advisor. He is a graduate of Laval University with a BA in Industrial Relations and has been recognized multiple times at the Canadian Wealth Professional Awards, including winning “Wholesaler of the Year” Award three times.

Disclaimer:

Commissions, management fees and expenses all may be associated with investments in exchange-traded funds. Please read the ETF Facts or prospectus of the BMO ETFs before investing. Exchange-traded funds are not guaranteed, their values change frequently and past performance may not be repeated.

Distribution yields are calculated by using the most recent regular distribution, or expected distribution, (which may be based on income, dividends, return of capital, and option premiums, as applicable) and excluding additional year end distributions, and special reinvested distributions annualized for frequency, divided by current net asset value (NAV). The yield calculation does not include reinvested distributions. [Bold]Distributions are not guaranteed, may fluctuate and are subject to change and/or elimination. Distribution rates may change without notice (up or down) depending on market conditions and NAV fluctuations. The payment of distributions should not be confused with the BMO ETF’s performance, rate of return or yield. If distributions paid by a BMO ETF are greater than the performance of the investment fund, your original investment will shrink. Distributions paid as a result of capital gains realized by a BMO ETF, and income and dividends earned by a BMO ETF, are taxable in your hands in the year they are paid. BOLDYour adjusted cost base will be reduced by the amount of any returns of capital. If your adjusted cost base goes below zero, you will have to pay capital gains tax on the amount below zero.

Cash distributions, if any, on units of a BMO ETF (other than accumulating units or units subject to a distribution reinvestment plan) are expected to be paid primarily out of dividends or distributions, and other income or gains, received by the BMO ETF less the expenses of the BMO ETF, but may also consist of non-taxable amounts including returns of capital, which may be paid in the manager’s sole discretion. To the extent that the expenses of a BMO ETF exceed the income generated by such BMO ETF in any given month, quarter, or year, as the case may be, it is not expected that a monthly, quarterly, or annual distribution will be paid. Non-resident unitholders may have the number of securities reduced due to withholding tax. Certain BMO ETFs have adopted a distribution reinvestment plan, which provides that a unitholder may elect to automatically reinvest all cash distributions paid on units held by that unitholder in additional units of the applicable BMO ETF in accordance with the terms of the distribution reinvestment plan. For further information, see the distribution policy in the BMO ETFs’ prospectus.

This article may contain links to other sites that BMO Global Asset Management does not own or operate. Any content from or links to a third-party website are not reviewed or endorsed by us. You use any external websites or third-party content at your own risk. Accordingly, we disclaim any responsibility for them.

BMO ETFs are managed by BMO Asset Management Inc., an investment fund manager, a portfolio manager, and a separate legal entity from Bank of Montreal.

“BMO (M-bar roundel symbol)” is a registered trademark of Bank of Montreal, used under licence.

On Tuesday, I attended the Toronto instalment of BMO ETFs’ Spring Road Tour, the first of a 10-city Canadian tour that extends into early May.

On Tuesday, I attended the Toronto instalment of BMO ETFs’ Spring Road Tour, the first of a 10-city Canadian tour that extends into early May.

Rai’s “big takeaway” is that while Commodities are the “source of the shock,” they also “benefit from supply constraints, fiscal demand and de-globalization.”

Rai’s “big takeaway” is that while Commodities are the “source of the shock,” they also “benefit from supply constraints, fiscal demand and de-globalization.”