My latest MoneySense Retired Money column looks at the currently near record high valuations of U.S. stocks and the risks that may pose to those in the Retirement Risk Zone. Full column can be accessed by clicking on the highlighted headline: Why retirement planners are getting defensive.

Retirement Club co-founder Dale Roberts recently posted a typical anxious link to a Globe & Mail column by Dr. Norman Rothery, (CFA) which suggested the current environment of Trump-inspired Tariffs and global Trade Wars, are causing plenty of anxiety for this group.

In the piece posted under Managing Risk in Retirement – and headlined With today’s market, investors close to retirement face precarious times – Rothery said investors on the cusp of retirement are “facing peril from a combination of the unusually lofty U.S. stock market and political uncertainty that’s disrupting world trade.”

U.S. stocks trading at “worrying levels”

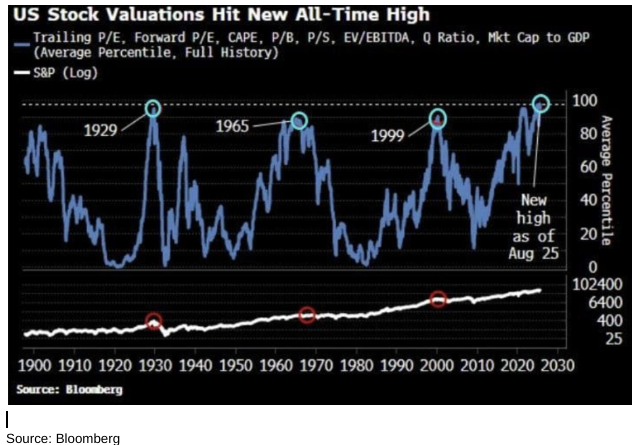

The U.S. stock market is “trading at worrying levels,” based on several Value factors, Rothery said: the S&P 500 Index is “trading at a cyclically adjusted price-to-earnings ratio (developed by Robert Shiller) near 39, which is above its peak of 33 in 1929 and it is approaching its top of 44 in late 1999, based on monthly data. Similarly the index’s price-to-sales ratio is approaching its 1999 high. A broader composite measure that includes many different market factors indicates that the U.S. market’s valuation is at record levels. “

The U.S. stock market is “trading at worrying levels,” based on several Value factors, Rothery said: the S&P 500 Index is “trading at a cyclically adjusted price-to-earnings ratio (developed by Robert Shiller) near 39, which is above its peak of 33 in 1929 and it is approaching its top of 44 in late 1999, based on monthly data. Similarly the index’s price-to-sales ratio is approaching its 1999 high. A broader composite measure that includes many different market factors indicates that the U.S. market’s valuation is at record levels. “

Rothery, who also publishes StingyInvestor.com, concluded that it’s “likely that the U.S. stock market will generate unusually poor average real returns over the next decade or so.” Unfortunately, the U.S. stock market now represents about 65% of the world’s market by market capitalization based on its weight in the MSCI All-Country World Index at the end of August. So if the U.S. market flops, “It’ll likely take the rest of the world with it – at least temporarily,” Rothery cautioned.

This could impact recent retirees just beginning to draw down portfolios, due to “sequence of returns risk.” That means that those in the so-called Retirement Risk Zone who suffer early losses could down the road be in danger of outliving their savings. Rothery also reference the famous 4% Rule of financial planner and author William Bengen: the theory that investors in a 55/40/5 portfolio should be able to sustain retirement savings for 30 years provided the annual “SafeMax” withdrawal not exceed 4% a year (actually 4.7%) after adjusting for inflation. Bengen just released a new book titled A Richer Retirement: Supercharging the 4% Rule to Spend More and Enjoy More, which the Retired Money column plans to review next month.

What recent Retirees can do to lower their risk

Retirement Club members anxiously posed questions on the related chat room about whether they should be moving to cash and bonds, gold or other alternatives to U.S. stocks. To this, Dale Roberts – who also runs his own Cutthecrapinvesting blog – warned against getting too defensive but agreed a move to a 70% fixed income/30% stocks allocation might work for some nervous early retirees. Personally, he has trimmed back on his US growth stock exposure and added to defensive ETF sectors like consumer staples, healthcare and utilities. He also mentioned a US equity ETF trading in Canadian dollars: XDU.T

Advisors and their clients suffer from Optimist bias

Advisor John De Goey came to a similar cautious stance in a recent (Sept 12) speech at the MoneyShow in Toronto, archived here on YouTube. Titled Bullshift and Misguided beliefs (see this recent Hub blog) De Goey expanded on his usual themes of advisor bullishness and complacent investors, also articulated in his book Bullshift. Continue Reading…