Once you achieve Financial Independence, you may choose to leave salaried employment but with decades of vibrant life ahead, it’s too soon to do nothing. The new stage of life between traditional employment and Full Retirement we call Victory Lap, or Victory Lap Retirement (also the title of a new book to be published in August 2016. You can pre-order now at VictoryLapRetirement.com). You may choose to start a business, go back to school or launch an Encore Act or Legacy Career. Perhaps you become a free agent, consultant, freelance writer or to change careers and re-enter the corporate world or government.

Spending from retirement savings, or decumulation, in a way that maximizes what you have left to spend after taxes is surprisingly complex. I’ve done extensive simulations of various strategies for my situation, including strategies that change over time, to find what works best for me. Here I describe how I’m managing my RRSP in retirement, but it’s important to remember that it may or may not work well for you depending on your particular circumstances.

Looking for the fully optimal financial strategy is futile. I ran my simulations and chose a simple enough strategy that worked well across a wide range of investment outcomes. The only reason for changing my strategy is if something happens that is far outside my expectations. Those who constantly seek perfection waste their time and hurt their outcomes with constant tinkering.

Our portfolio and goals

My wife and I have RRSPs, TFSAs, and non-registered accounts. I prefer not to discuss exact amounts, but broadly speaking, our combined RRSPs are larger than our combined non-registered accounts, which are larger than our combined TFSAs. In addition to the exact sizes of these accounts, two other figures that are significant for simulations are our unrealized capital gains in the non-registered accounts and our deferred capital losses from previous years.

My wife and I have roughly the same net worth. Although we consider all our assets to be owned by both of us, CRA doesn’t see it that way. We spent decades carefully choosing whose money to spend each year so that we’d have close to the same net worth now.

Our goal is to maximize the amount we can safely spend each year, rising with inflation, for the rest of our lives. We have no interest in scrimping now just so we can live rich when we’re much older. Some might even choose to spend more in their 50s and 60s than they will spend later, but I can’t see any logic in living poor early on just to be rich later.

The main tax challenge we face is high taxes and possibly OAS clawbacks on forced RRIF withdrawals after we turn 72. These taxes will be even higher after one of us passes away, and higher still after the second passes away. The remedy here is to make modest RRSP/RRIF withdrawals in the years before we turn 72. The goal is to make lightly taxed RRSP/RRIF withdrawals early rather than heavily taxed withdrawals later. This gap in tax rates has to be large enough to overcome the value of continuing to defer taxes.

This is where the simulations help. At one extreme, we could be spending entirely from our TFSAs to keep our incomes very low. My simulations show that this “collect the GST rebate” strategy is not optimal for us (nor do I find it palatable). At the other extreme, winding down our RRSPs quickly is far from optimal as well. Something in between is best.

Our decumulation strategy

My simulations tell me that we’re best to target a particular income level each year. Note that our income is not the same thing as how much we spend. The amounts we spend from non-registered accounts create only modest declared income for taxes. By adjusting how much we spend from each type of account, we can target different amounts for how much we spend and how much we declare on our income taxes. Continue Reading…

Retirement may last longer than you expect. The question is: is your portfolio built to keep up?

Image courtesy BMO ETFs/Getty Images

By Alain Desbiens, Vice-Chair BMO ETFs

(Sponsor Blog)

Canada is undergoing a profound demographic transformation that will influence the nation’s economic trajectory and long‑term investment landscape for decades to come. By 2036, Canadians aged 65 and older will account for roughly 23% of the population, up from approximately 19% today. 1

This aging shift is propelled by three powerful forces: rising life expectancy, persistently low birth rates, and immigration serving as the country’s primary source of population growth. Together, these drivers are reshaping not only the size and composition of Canada’s population but also the way investors and financial professionals must approach planning and portfolio construction.

For investors, these demographic changes create a dual reality. On one hand, the economy faces challenges such as higher healthcare and social‑support spending, and increasing strain on retirement income systems. On the other hand, new long‑horizon opportunities are emerging.

Sectors tied to aging populations, innovation in healthcare, longevity planning, and intergenerational wealth transfer all stand to benefit. Exchange‑traded funds (ETFs), with their cost‑effectiveness, diversification, and transparency, offer an efficient toolkit for capturing these evolving trends.

Key Demographic Trends

1.) Aging Profile & Generational Mix

Baby Boomers still represent about one quarter of Canada’s population, but by 2029, Millennials are projected to surpass Boomers in absolute numbers. 2 This generational shift will reshape demand across housing, consumption, and financial services. Millennials tend to prefer digital-first advice, sustainable investing, and simple yet sophisticated products — including ETFs — while Boomers continue to prioritize income generation, capital preservation, and tax‑efficient3 decumulation strategies. This changing balance in generational influence will increasingly dictate the types of investment solutions that gain traction in the market.

2.) Retirement Wave

Canada is entering a period where record numbers of Boomers are exiting the workforce and see increasing need for accumulation and decumulation strategies, and a higher demand for financial, will and decumulation strategies.

3.) Longevity Realities

Canadians are living longer than ever before, with meaningful implications for retirement planning.

Women 65+: Over half are expected to live to age 90. 4

Men 65+: More than half reach age 90 as well, though only about 39 per 1,000 do so without a major critical illness. 5

FP Canada/IQPF: A 50-60-70‑year‑old has roughly a 25% probability of living to age 94 (men) or 96 (women).6

This extended lifespan introduces significant longevity risk: the risk of outliving one’s capital. Financial plans must now be stress‑tested for longer retirement horizons, rising living costs, and variable health outcomes.

4.) Rising Costs for Aging‑in‑Place & Care

Healthcare inflation, long‑term care, and home‑care services are expected to grow sharply. These realities underline the need for specialized insurance solutions, inflation‑aware portfolios, and steady income vehicles that can sustain retirees across multi‑decade retirement periods.

5.) Wealth Distribution & Investor Segmentation

Canada is on the cusp of a major wealth transition:

Gen X is set to surpass Boomers in total net worth. 7

An estimated $450 billion will transfer to Gen X over the next decade.8

Total household wealth is projected to reach $10 trillion by 2030, reshaping investor behavior, risk profile8, and demand for advice.9

The Bottom Line

Canada’s aging demographic is more than a statistic: it is a structural force that will shape markets, spending patterns, and investment requirements. Investors who proactively position for these changes can build portfolios that are both resilient and growth‑oriented. With their flexibility, transparency, and broad exposure to demographic‑driven themes, ETFs remain one of the most effective vehicles for navigating this new era.

ETF Investment Opportunities

1.) Income Solutions for Retirees

• Longer lifespans + market volatility = demand for stable, tax-efficient income

If retirement is on the horizon, now is the time to look beyond when you plan to stop working and focus on how long your portfolio will need to support you. Longer lifespans mean portfolios must balance growth, income, and flexibility before the first paycheque replacement ever begins. Reviewing your asset mix, understanding your future income needs, and considering simple, diversified ETF solutions today can help reduce stress and create more confidence tomorrow. The years leading up to retirement aren’t just a finish line, they’re the foundation for decades ahead.

Want to learn more? Join Alain Desbiens and host Michelle Allen as they explore why longer retirements demand smarter strategies: inflation-aware portfolios and steady income that lasts decades, not just years. Listen to the podcast episode now!

8: Risk Profile – Comprised of a client’s risk tolerance (i.e., client’s willingness to accept risk) and risk capacity (i.e., a client’s ability to endure potential financial loss).

Alain Desbiens is Vice Chair, BMO ETFs. Alain brings more than 30 years of financial services experience to his new role. A seasoned financial expert and former broker, Alain has raised awareness of ETF benefits among advisors, direct and institutional clients through both individual discussions and impactful presentations. Alain is also active in multiple media formats helping provide insights on both the industry and investments. Over his career, Alain held roles as wholesaler, sales manager, branch manager, and investment advisor. He is a graduate of Laval University with a BA in Industrial Relations and has been recognized multiple times at the Canadian Wealth Professional Awards, including winning “Wholesaler of the Year” Award three times.

Disclaimer:

Commissions, management fees and expenses all may be associated with investments in exchange-traded funds. Please read the ETF Facts or prospectus of the BMO ETFs before investing. Exchange-traded funds are not guaranteed, their values change frequently and past performance may not be repeated.

Distribution yields are calculated by using the most recent regular distribution, or expected distribution, (which may be based on income, dividends, return of capital, and option premiums, as applicable) and excluding additional year end distributions, and special reinvested distributions annualized for frequency, divided by current net asset value (NAV). The yield calculation does not include reinvested distributions. [Bold]Distributions are not guaranteed, may fluctuate and are subject to change and/or elimination. Distribution rates may change without notice (up or down) depending on market conditions and NAV fluctuations. The payment of distributions should not be confused with the BMO ETF’s performance, rate of return or yield. If distributions paid by a BMO ETF are greater than the performance of the investment fund, your original investment will shrink. Distributions paid as a result of capital gains realized by a BMO ETF, and income and dividends earned by a BMO ETF, are taxable in your hands in the year they are paid. BOLDYour adjusted cost base will be reduced by the amount of any returns of capital. If your adjusted cost base goes below zero, you will have to pay capital gains tax on the amount below zero.

Cash distributions, if any, on units of a BMO ETF (other than accumulating units or units subject to a distribution reinvestment plan) are expected to be paid primarily out of dividends or distributions, and other income or gains, received by the BMO ETF less the expenses of the BMO ETF, but may also consist of non-taxable amounts including returns of capital, which may be paid in the manager’s sole discretion. To the extent that the expenses of a BMO ETF exceed the income generated by such BMO ETF in any given month, quarter, or year, as the case may be, it is not expected that a monthly, quarterly, or annual distribution will be paid. Non-resident unitholders may have the number of securities reduced due to withholding tax. Certain BMO ETFs have adopted a distribution reinvestment plan, which provides that a unitholder may elect to automatically reinvest all cash distributions paid on units held by that unitholder in additional units of the applicable BMO ETF in accordance with the terms of the distribution reinvestment plan. For further information, see the distribution policy in the BMO ETFs’ prospectus.

This article may contain links to other sites that BMO Global Asset Management does not own or operate. Any content from or links to a third-party website are not reviewed or endorsed by us. You use any external websites or third-party content at your own risk. Accordingly, we disclaim any responsibility for them.

BMO ETFs are managed by BMO Asset Management Inc., an investment fund manager, a portfolio manager, and a separate legal entity from Bank of Montreal.

“BMO (M-bar roundel symbol)” is a registered trademark of Bank of Montreal, used under licence.

My latest MoneySense Retired Money column looks at the Iran conflict that erupted suddenly late in February: you can find the full column here: How Retirees should respond to the Iran Crisis.

On Tuesday, the day after Trump TACO’d over his threat to attack Iran’s oil infrastructure (a 5-day reprieve that calmed stock markets at least for the week ending March 27th) Findependence Hub ran a blog that collected input from 14 financial advisors and business owners based largely in the United States. Those sources were collected via a partnership with long-time contributor Featured.com, which works with Linked In to select input. You can find the resulting column here: Financial Experts and Business Owners on what if any moves Retirees should consider if Iran War drags on.

You can get the gist of the messages those experts sent by quickly scrolling down through an admittedly long blog and reading the subheadings highlighted in Blue in the original post. Below I append my favourites, some of which I flagged on social media. If you find the headline summaries intriguing, you’ll find the accompanying observations useful, if not actionable:

Avoid Knee-jerk Liquidation

This is more of a rebalance-and-defend moment than a reason to overhaul the portfolio

Put Capital Preservation over Aggressive Growth

Seek Robust diversification across asset classes and sectors

Rebalance toward defense, yes. Blow up your entire strategy? No.

Make sure existing Allocation is suitably Defensive and Liquid

Don’t over-rotate into a single ‘safe’ bet that can whipsaw when the narrative changes

Remain diversified enough to absorb uncertainty

Reduce volatile individual Growth Names but maintain Diversified Index Funds

Move from Sector Rotation to Structural Resilience

Canadian perspective, with CUSMA renewal looming

The MoneySense column focuses more on the Canadian situation, with input from Toronto-based advisors like John De Goey, Matthew Ardrey and Steve Lowrie, all of which should be familiar to readers of this site and the Retired Money column.

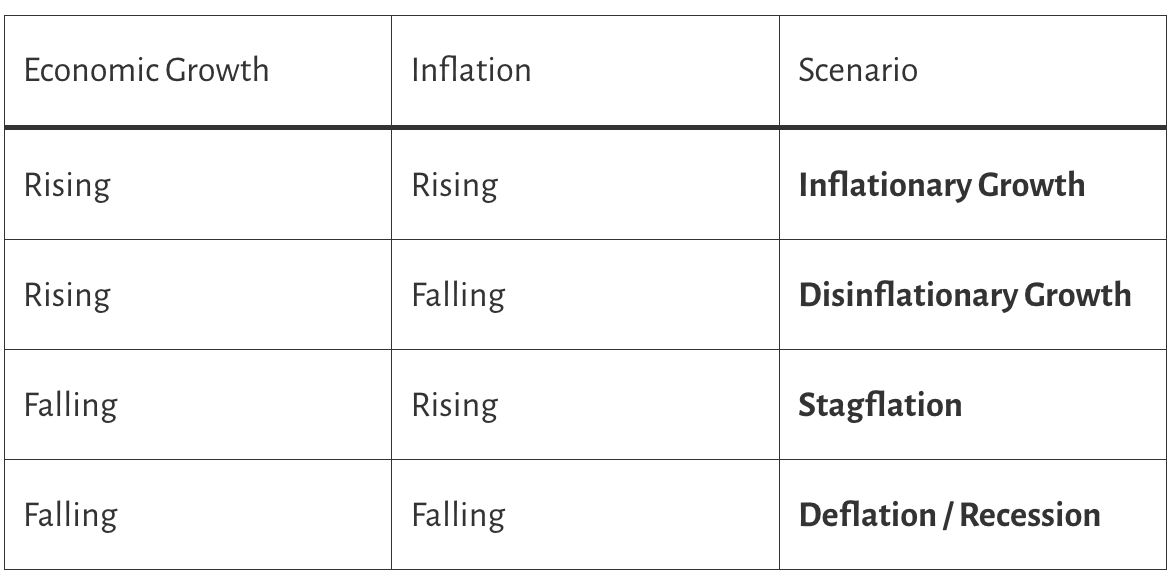

See also a recent blog on Stagflation penned by Dale Roberts of the Retirement Club and cutthecrap investing. Among his many suggestions, the most valuable may be his emphasis on maintaining an “All-Weather Portfolio” catering to all four possible economic quadrants: Inflationary Growth, Disinflationary Growth, Stagflation and Deflation/Recession. Continue Reading…

By Dale Roberts, Retirement Club/Cutthecrapinvesting

Special to Financial Independence Hub

It has been more than two weeks since the U.S. attacked Iran. And while the U.S. was quick to knock out much of Iran’s traditional military capability, Iran has turned to asymmetric war and has also weaponized oil, fertilizers and other materials that pass through the Hormuz Strait. With threats and some strategic attacks on shipping, Iran has essentially closed the Hormuz Strait. About 20-25% of the world’s oil and a third of the world’s fertilizer needs flow through the Strait. We now face a potential energy shock and there are rumblings that we might experience a period of stagflation. In the 1970s an energy crisis created the conditions for stagflation. How do we defend against stagflation?

As always, the following is not advice.

First off, and as always, no one knows what will happen. No one knows how this war will proceed and what it will mean for investment assets and the economies of the world. Trump could announce today that he’s packing up and heading home or this could continue for years. That said, history does teach us how assets react. History teaches us how to hedge most any threat.

What is Stagflation?

Stagflation happens when several factors combine to create an especially difficult economic environment. To get stagflation, three things must occur together:

Slow economic growth

High inflation

A high unemployment rate

Stagflation is an economic double-whammy where stagnant growth and high unemployment collide with rising inflation. This rare, painful cycle is difficult to fix because traditional policies to lower inflation often worsen unemployment, and vice versa.

Market strategists have been quick to point out that rarely do conflicts have any long-lasting impact on stock prices. In 20 major episodes since the Second World War compiled by analysts at RBC Wealth Management, the S&P 500 index fell by an average of just 6 per cent.

The outliers in that list, however, involve major oil market disruptions, like the Arab oil embargo in 1973 and the Iraqi invasion of Kuwait in 1990. We had more significant drawdowns.

It has been the most common message on this blog: get an investment plan and stick to it like glue. Here’s the full graphic that was shared at Retirement Club (and on X (Twitter).

War is something we can ignore like every other risk, when we have our stock-solid investment plan and retirement plan.

The 4 economic scenarios

The economy can shift along two axes:

Economic growth (rising or falling)

Inflation (rising or falling)

Combining them gives four possible economic scenarios:

1. Inflationary Growth

Growth ↑ + Inflation ↑

Economy expanding strongly

Demand pushes prices higher

Often occurs during late expansions

Assets that tend to do well

Commodities

Real estate

Some stocks

Example period: parts of the global economy during the early 2000’s commodity boom.

2. Disinflationary Growth

Growth ↑ + Inflation ↓

Economy grows but inflation stays low or falls

Considered the best environment for stocks

Assets that tend to do well

Stocks

Growth companies

Corporate credit

Bond market

Example: much of the period after the Global Financial Crisis recovery.

3. Stagflation

Growth ↓ + Inflation ↑

Economy slows but prices keep rising

Very difficult for policymakers

Assets that tend to do well

Commodities

Gold

Inflation-protected assets

Oil and gas stocks

Classic example: the 1970’s Oil Crisis.

4. Deflation / Recession

Growth ↓ + Inflation ↓

Demand collapses

Prices and wages fall

Debt burdens become heavier

Assets that tend to do well

Government bonds

Cash

Defensive assets

Example: the Great Depression and recessions

Fortunately we are almost always in scenario 2 and some of scenario 1. High inflation and stagflation is rare. Deflation or a Depression is rare and market recessions shown in scenario 4 is why many will embrace bonds and cash to create a balanced portfolio that is lower risk. Continue Reading…

I’ve had many of you ask how I spend my time in retirement, and when I realized I spend only 0.23% of my time managing our money, it made me ask myself the same question.

What do I do with all of my time now that I’m retired?

Today, I’ll answer that question.

As a bonus, I’ve made a “Before vs. After” comparison, showing how my time allocation has changed since retirement. It’s an interesting look at what areas have replaced the time previously consumed by commuting and work. This one’s for you, Chuck (hey, you’ve read every one of my articles, you deserve an answer. Thank you for your loyalty!)

It’s the first time I’ve taken on this task, and it’s been enlightening.

I trust you’ll find it of interest …

How I spend my Time in Retirement

Time is an interesting concept in retirement.

The loss of the structure previously imposed by paid work adds a new element to the consumption of time. Whereas a large chunk of my time was once consumed by work and commuting, today it’s entirely available to use as I choose.

24 hours a day. 7 days a week.

(If you’re curious, that’s 8,760 hours per year. Actually, it’s 8,760 hours even if you’re not curious. Wink.)

That’s imposing to a lot of pre-retirees, as well it should be. I encourage any of you who’ve not yet crossed The Starting Line to spend some of your precious time thinking about how you’re going to use it when you get to “the other side”. It’s an important question, and one of the most important you need to ponder to ensure a smooth transition into retirement.

With that as my introduction, here’s how I spend my time in retirement…

How I spend my Time (“Awake Time”)

For the sake of simplicity, I’m omitting sleep from the pie chart above. For the record, I’ll touch on sleep first, then get into how I spend my “Awake Time”.

Sleep – 2,920 Hours/Year (33% of Total Time)

On average, I sleep about 8 hours/night. I typically go to bed ~10:00 pm, and wake between 6:00 – 7:00 am. Assuming my math is correct, that means I sleep 2,920 hours/year, an increase of 365 hours versus my working years. For you math geniuses out there, that equates to 1 hour of additional sleep per night since I’ve retired. Yep, that seems about right.

Now let’s get on to the fun stuff, which consumes the remaining 67% of “Awake Time” in a year. For consistency, I’ll present these in the same order as shown in the pie chart above, starting with exercise.

Swimming for exercise in nearby Lake Blue Ridge

Exercise – 858 Hours/Year (15% of “Awake Time”)

I like a bit of structure to start my day and every Mon/Wed/Fri that means arriving at the gym by 7:15 for Spin Class. I love Spin, and I know I’ll be much more consistent with my exercise if I have a scheduled class to hold me accountable. Following Spin, I take a Cross-Fit class, which focuses more on interval and weight training. Combining the two makes a great start to the day, and I’m ready to take on the world when I return home shortly after 9:00 am.

In addition to the structured classes at the gym, I walk our dogs for 1 – 1.5 hours every day. We have a scenic 1.3-mile loop in the woods behind our cabin, and I typically walk it twice a day. When the weather is nice, I’ll throw in a weekly swim, or a mountain bike ride, or a hike. If we’re spending time at our condo in Alabama, I’ll add some morning runs to my routine. I like to mix it up, but always make exercise part of the structured component to my day.

Meals – 548 Hours/Year (9% of “Awake Time”)

My wife and I make it a routine to have lunch and dinner together. Breakfast is a more haphazard affair, typically a quick bowl of cereal before I head to the gym, or a more leisurely time with several cups of coffee on a “non-gym” day. Assuming ~1.5 hours/day for all meals combined, I spend 548 hours/year eating.

Family time with my granddaughter = Priceless.

Family – 1,152 Hours/Year (13% of “Awake Time”)

I spend 850 hours more time with my family each year now that I’m retired than I did when I was working. The vast majority of that increase comes from a lifestyle decision we made when we Purchased a Second Home in Retirementshortly after our daughter moved from the Pacific Northwest to Southern Alabama. As mentioned in that post, we’re now spending a week every month in our Alabama condo, with our primary focus being quality time with our daughter and 3-year-old granddaughter. We wouldn’t trade that time for anything, and consider it one of the greatest joys in our current retirement lifestyle.

Entertainment – 802 Hours/Year (14% of “Awake Time”)

According to FitBit, I’ve averaged 13,330 steps over the past month, only falling below 10k steps twice in that timeframe. In writing this post, I also discovered that I’ve walked 4,478,654 steps (1,989 miles) in the past year, an average of 12.3k per day. Bottom Line: I don’t sit around much during the day…

After my typically busy day in retirement, I have no problem admitting that I like to take it easy in the evenings. Every night after dinner, my wife and I like to “chill out” in front of the TV with our dogs in our laps. We’ve earned that right, and I make no apologies in announcing to the world that I spend the majority of my “9% Entertainment Time” watching Netflix, the news, documentaries, etc. We also seldom miss an Atlanta Braves game and enjoyed watching “our Braves” win the World Series this year! We also go out with friends more frequently now that we’re retired, and that’s included in the number. Continue Reading…