Once you achieve Financial Independence, you may choose to leave salaried employment but with decades of vibrant life ahead, it’s too soon to do nothing. The new stage of life between traditional employment and Full Retirement we call Victory Lap, or Victory Lap Retirement (also the title of a new book to be published in August 2016. You can pre-order now at VictoryLapRetirement.com). You may choose to start a business, go back to school or launch an Encore Act or Legacy Career. Perhaps you become a free agent, consultant, freelance writer or to change careers and re-enter the corporate world or government.

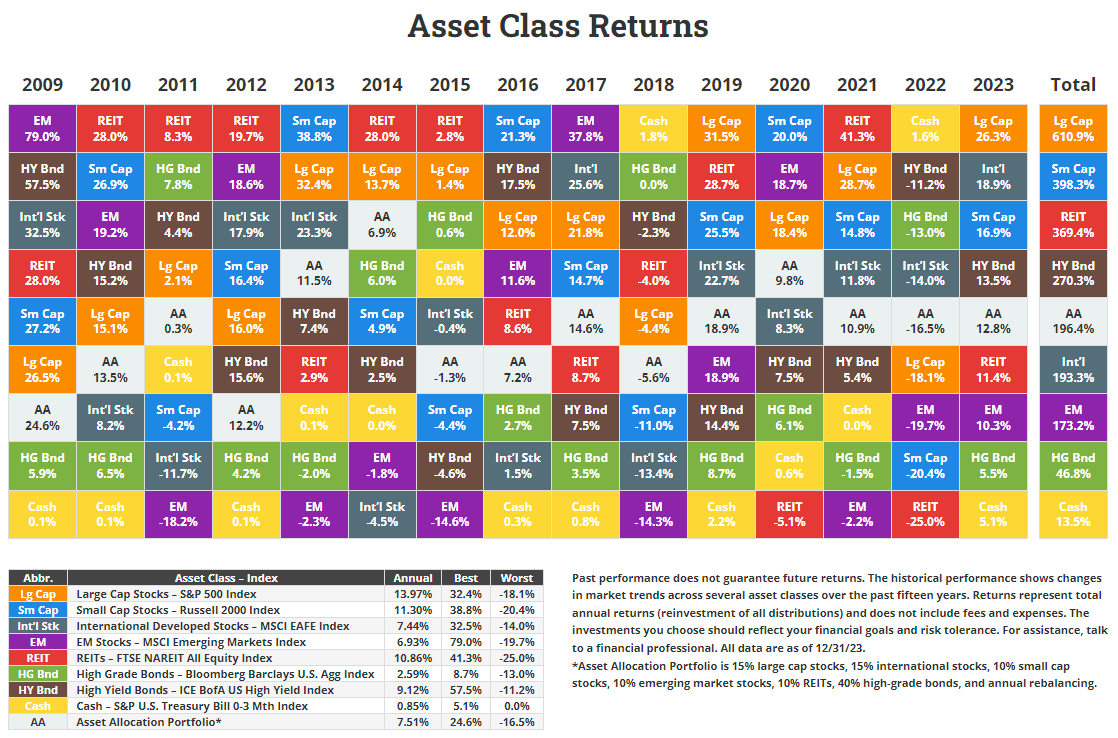

Overall, if you were in low-cost, diversified ETFs, including some all-in-one ETFs, it should have been a VERY good year for you!

To answer the question, our portfolio performed just fine – since I/we tend to focus on the meaningful income our portfolio generates to eventually cover expenses along with returns. Staying invested in a number of stocks and low-cost ETFs as we do are designed to generate market-like returns since we don’t trade nor tinker with the portfolio, and low-cost ETFs invested in stocks outside Canada offer growth.

If your bias was more simplicity than my approach and seeking total returns, then these ETFs including some great all-in-one ETFs might have done very well for you in 2023 after a terrible 2022:

ETF

2023

2022

VEQT (100% equity)

16.95%

-10.92%

XEQT (100% equity)

17.05%

-10.93%

ZEQT (100% equity)

16.75%

-5.25%

HEQT (100% equity

22.64%

-19.20%

XAW (100% equity ex-Canada)

18.16%

-11.77%

Beyond some of these great all-equity ETFs for your portfolio, consider these in this post that might hold a mix of stocks and bonds to match your risk tolerance and investing objectives:

No financial advisor or money manager needed for these ETFs. The wise ones would tell you to index invest in some diversified ETFs anyhow. Just food for thought in 2024 if you haven’t considered DIY investing.

Here are some interesting, early YTD returns from the oil and gas sector. Gurgen is a must-follow IMO.

What does 2024 have in store?

I have a few (fun) predictions that I will share soon but they are just that, some thoughts and this is a good reminder that experts know nothing about what the financial future might hold – but they have to put food on the table as well…

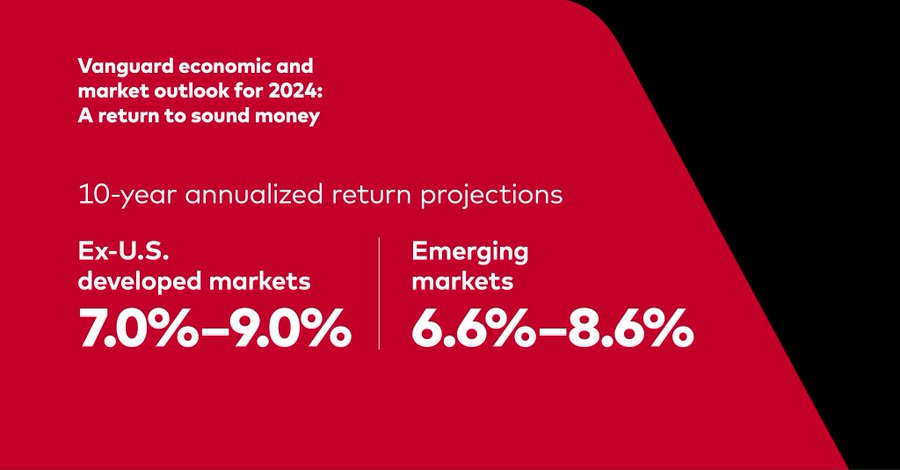

Vanguard still took a leap of faith though, will they be right in 2024?

Mark Seed is a passionate DIY investor who lives in Ottawa. He invests in Canadian and U.S. dividend paying stocks and low-cost Exchange Traded Funds on his quest to own a $1 million portfolio for an early retirement. You can follow Mark’s insights and perspectives on investing, and much more, by visiting My Own Advisor. This blog originally appeared on his site Jan. 6, 2024 and is republished on the Hub with his permission.

The link between financial well-being and physical wellness is clearer than ever in the fast-paced world of today.

The purpose of this article is to present a thorough understanding of this complex relationship and emphasize the need of implementing preventative measures in order to ensure long-term security.

Recognizing the Connection

Stress related to money can harm our physical well-being and result in a variety of problems, including chronic illnesses, anxiety, and insomnia. Similarly, low physical health can financially burden finances due to higher medical costs and lower productivity at work. Acknowledging this interdependence is essential to implementing a comprehensive strategy for overall wellness.

How Financial Stress affects your Health and Vice Versa

Financial Stress

Financial stress is the emotional and psychological strain arising from financial problems or uncertainties.

Causes: It can stem from various factors such as debt, job loss, inadequate savings, unexpected expenses, or economic instability. Individuals and families may experience financial stress when they perceive a gap between their financial resources and their lifestyle demands.

Impact of Financial Stress on Health

Mental Health: Persistent financial stress is strongly linked to mental health issues, including anxiety and depression. The constant worry about making ends meet or dealing with debt can contribute to heightened stress levels.

Physical Health: Chronic stress has been associated with a range of physical health problems, including cardiovascular issues, sleep disturbances, and compromised immune function.

Behavioural Responses to Financial Stress

Unhealthy Coping Mechanisms: Some individuals may adopt harmful coping mechanisms, such as excessive alcohol or substance use, overeating, or neglecting self-care, as a response to financial stress. These behaviours can further exacerbate health problems.

Reduced Access to Healthcare: Financial Barriers to Healthcare: Individuals facing financial stress may delay or avoid seeking medical attention due to the cost of healthcare services. This can result in undiagnosed or untreated health conditions, leading to more significant health issues over time.

Job Performance and Productivity

Impact on Employment: Financial stress can affect job performance and may even lead to job loss in extreme cases. The loss of employment not only exacerbates financial stress but also disrupts one’s sense of security and stability, impacting mental health.

Vice Versa: How Health affects Finances

Medical Expenses: Poor health can lead to increased medical expenses, including doctor visits, medications, and possible hospitalization. These costs can contribute to financial strain, especially if the individual does not have adequate health insurance coverage.

Work Productivity and Income

Reduced Productivity: Health issues can result in decreased work productivity, absenteeism, or the inability to perform specific job functions. Financial stress may then be exacerbated due to lower income or job loss.

Breaking the Cycle

Financial Literacy and Planning: Improving financial literacy and implementing effective financial planning strategies can help individuals mitigate financial stress. Understanding budgeting, savings, and investment can contribute to a sense of control and security.

Practices for Health and Well-Being: In a similar vein, embracing a healthy lifestyle, learning stress-reduction strategies, and promptly seeking medical attention can enhance both physical and mental health by interrupting the vicious cycle of stress and its negative effects on finances and health.

Proactive Financial Strategies

Financial Planning and Budgeting for a Secure Future

The first step toward securing your financial future is to create and stick to a budget. Goal-setting, tracking expenses, and making decisions are all included in this section on the practical aspects of budgeting. A well-structured budget acts as a roadmap for obtaining financial stability.

Investment and Savings Tips for Long-Term Stability

Long-term financial stability depends on having a solid savings and investing plan. From determining your risk tolerance to researching various investment options, this section offers helpful advice on accumulating wealth and guaranteeing a secure financial future. Continue Reading…

From strategic moves in real estate to the expansion of businesses, twelve seasoned professionals share their stories of how calculated risks have shaped their wealth-building journeys.

Spanning from lessons learned in real estate investing to calculated risks propelling business expansion, these insights delve into the pivotal decisions that can make or break financial growth. Discover the risks that reaped rewards and the wisdom gained from taking chances in the world of investment and entrepreneurship.

As a successful real estate investor, taking calculated risks plays a big part in my wealth-building journey, but it’s not something I’ve done well from the beginning. For example, the first property I ever invested in was an old house that ended up having a lot of issues, like animal infestations.

Clearly, I took a poorly calculated risk by buying that property because I wasn’t aware of the problems before investing. But it did help me learn an important lesson: Taking risks becomes a lot more manageable when you’ve done your research and understand the magnitude of the risks involved. If you go in blind, like I did that first time, it’s much harder to make smart decisions.

Thankfully, I did end up earning big returns on that property (and properties I’ve invested in since), so the investment did pay off. And now, I always do my research before signing on the dotted line to help minimize risk. –– Ryan Chaw, Founder and Real Estate Investor, Newbie Real Estate Investing

Successful Shift to Hotel Investments

As real estate investors, my husband and I take calculated risks regularly. The biggest risk we took was transitioning from apartment complexes to hotels six years ago. Moving into a completely unknown industry was an enormous risk, since our entire knowledge base and experience was around long-term rentals. Hotels go beyond rentals; they are a section of the commercial real estate market; they are full businesses with significant demands around 24/7 daily operations.

Our decision to move into this market was driven by reduced ROI in the multifamily space, and we sought a more profitable investment opportunity. This transition wasn’t just about moving into a completely unknown industry; it also required us to place trust in a business partner because, in order to secure financing, we needed to demonstrate an experienced operator who could soundly manage the hotel.

The risk paid off. This particular hotel has consistently delivered high returns: even during the pandemic. It’s led to additional hotel acquisitions and a strong friendship with our hotel operator partner. We’ve built up our expertise in the hotel industry through our experience with this first successful hotel, expanded, and gained a solid understanding of what it takes to run hotels profitably.

We’re exploring international opportunities. All because we took a calculated risk six years ago and moved into hotels. That initial leap of faith opened doors we never could have imagined at the time. –– Nic Stohler, Creator, Nic’s Guide

Daily Risk-Taking yields Flipping Success

I take calculated risks every day in making offers on properties that I’m going to close on and list, or close on and flip. This risk comes in many forms, such as often not having 100% of the information from a seller, not knowing where the market is going to be a couple of months from now, or simply having a project run longer than expected.

These calculated risks that I take daily have helped tremendously in the wealth-building journey, as I’ve been able to complete some very successful flip projects, such as one I purchased last year for $460,000. In this scenario, I opted for the seller to finance me 80% of the purchase price; it was a hoarder house, and I didn’t really know where the market was going to be by the time we finished.

Fortunately for us, by the time we listed it three months later, we were able to get 20 offers and sell the property for $770,000. — Sebastian Jania, CEO, Ontario Property Buyers

Investing in Personal Digital Brand Growth

They say insanity is doing the same thing and expecting different results. Building wealth is rarely easy and requires some level of risk. This year, I risked spending dozens of hours and thousands of dollars to grow my digital brand.

To most people, pouring a lot of energy and money into a business that isn’t guaranteed success is scary and irrational. However, I took the risk anyway because I’d already spent years learning different skills and believed in what I was doing. Despite spending thousands of dollars, my business is now profitable after taxes and expenses.

Even if my business had failed, I would’ve gained invaluable experience I could use toward my next investment. Building wealth can be risky, but you can reduce your risk by taking the time to understand your investment and assess your risk tolerance.-– Chris Alarcon, Journalist/Owner, Financially Well Off

Authenticity drives Startup’s Viral Growth

As an entrepreneur trying to grow a personal finance startup, risks are inevitable. However, one risk that I took early on that paid off immensely was getting vulnerable and sharing my personal story so openly.

Deciding to base my entire brand voice and messaging around my own memoir was risky. I shared details about my failures and shortcomings during my debt repayment journey: not ideals I thought people might want to hear about. But I knew if I only showed the highlights, it wouldn’t be authentic or establish trust. I had to risk being judged or dismissed to remain genuine.

It ended up paying off hugely. By bravely recounting even my toughest setbacks on my blog and social platforms, readers connected with my transparency. They saw themselves in my story. This drove immense word-of-mouth growth for My Millennial Guide in those early days when marketing budgets were non-existent.

Had I played it safe and kept my journey vague and surface-level, I doubt my message would have resonated so strongly. I’m grateful every day that I took the risk to stay true to my vulnerable, unconventional backstory: it fueled my wealth-building journey tremendously. — Brian Meiggs, Founder, My Millennial Guide

Life is all about risk, and your wealth-building is an area that’s no different. Over the years, I’ve taken plenty of risks that have helped me grow my wealth.

One of those is investing in a local comic convention. I saw them make a call for investors to seed some of the celebrity stars they were looking to bring in. This seemed like a great opportunity to invest but also a risky proposition. Thoughts of “What if the stars don’t pan out?” or “How will this impact other opportunities?” flooded my mind.

Thankfully, I took the risk, and it’s paid off not only in my wealth but also in the relationships that I have built. Due to the investments, I’ve received annual returns and opportunities to see new investment opportunities through the people I’ve met. –– Joseph Lalonde, Leadership Coach and Author, Reel Leadership

Google Ads Gamble secures Clientele

I took an $8,000 risk that led to my financial success. When I started my content writing agency in my twenties, I had about $8,000 in my bank account. I knew it would take a while to gain traction and find writing clients, so I took a risk.

I invested $1,000 monthly into Google Ads in an effort to get clients. I gave it my all and knew that if I couldn’t find a new, high-paying client within the next eight months, I’d have to return to my 9-to-5 job.

Fortunately, this risk paid off because I got my first client after four months, and by month six, I filled up my schedule. Because I took this calculated risk early on, I can now live a comfortable life and travel the world.— Scott Lieberman, Owner, Touchdown Money

Toronto Condo purchase defies Market Pessimism

Living in one of the most expensive housing markets in the world means hearing a lot about a supposed real estate bubble. For decades, people in Toronto have claimed we’re on the verge of a mega-correction, and because of this, I’ve watched friends stay out of the housing market; for some of them, it’s now too late to buy in.

It’s a good lesson not to let unwarranted negativity seep in. Continue Reading…

U.S. stocks can provide Canadian investors with all the foreign exposure they need

I’ve been advising Canadian investors to include U.S. stocks in their portfolios for more than 30 years. I continue to recommend them today. The U.S. stock market offers the widest variety and highest investment grade of companies to invest in of any country in the world. It also offers a wider selection of growth opportunities for those companies to pursue, in North America and around the world.

For our portfolio management clients, our general preference is to invest one quarter to one third of their holdings in U.S. stocks and the remainder in Canadian stocks.

Many major financial institutions recommend investing in North America. Some also recommend investing outside North America, especially in developing nations. They say that countries outside North America also offer great opportunities, and they may be right in some cases. They note that foreign investing offers an additional chance for diversification. This may be true, but we see it as irrelevant. Our view is that North America offers all the diversification that you really need.

Many promoters of emerging-market investing are also motivated at least in part by a conflict of interest.

By offering imported investments in their home market, they can earn higher profit margins than they get with domestic investments alone. That is, they make more money by promoting foreign investments. Investors may not make any more money, but they undoubtedly face more risk.

We have occasionally offered favourable advice about a handful of high-quality foreign stocks in the past few decades, while mentioning the added risk. But we’ve stressed our view that the U.S. and Canadian markets provide all the investment opportunities that you need to succeed as an investor.

Of course, the Canadian market offers opportunities that beat those available in the U.S.: in bank stocks, in the Resources & Commodities sector, and in specialists like CAE Inc. But Canada has nothing to compare with, say, Alphabet, Microsoft, McDonald’s and any number of other household names.

Neither too hot nor too cold

Some investors say they agree with our view on U.S. stocks in principle, but they disagree with our timing. They think the U.S. dollar is just too high at present levels: too hot, you might say. These folks seem to think that the natural foreign exchange rate between the U.S. and Canadian dollars should be around parity.

As of late 2023, the U.S. dollar has traded at around one-third higher than the Canadian dollar. Way above parity! In fact, the U.S.-Canada exchange rate has not been anywhere near parity in the past decade.

The U.S. dollar has mostly stayed between $1.20 Cdn. and $1.46 Cdn. since the start of 2015. It’s now around the middle of that 8-year range.

Since 1971, the U.S. dollar has stayed between $0.94 Cdn. and $1.60 Cdn. It’s now around the middle of that 52-year range.

Timing is worth a look. But if you make it the deciding factor in your investment decisions, it’s apt to cost you money, in the long run if not in the short.

“Has-been” U.S. dollar has a long life ahead

A lot of foreign governments share the view that the U.S. dollar is overvalued.

In March 2023, in a meeting in New Delhi, the representative from Russia revealed that his country is spearheading the development of a new currency. It is to be used for cross-border trade by the BRICS countries: Brazil, Russia, India, China, and South Africa. (Potential recruits include Iran, Syria and North Korea.)

I put this ambition on a par with the claims of cryptocurrency promoters. Some of them still predict that cryptocurrencies will take the place of the U.S. dollar. Continue Reading…

As retirement approaches, you ask yourself if you should work after retirement. Here’s a list of pros and cons to find out which path is right for you.

Image courtesy Arista Reality Group

By Dan Coconate

Special to Financial Independence Hub

Retirement is something we dream about. After years of hard work, we look forward to a slow life. However, for many people, the thought of stopping work altogether can be a little daunting.

There’s a big question looming over your head: Should you work after retirement? Find out the pros and cons to make an educated decision.

PRO: Mental Stimulation

Many older individuals discover that they thrive on the challenge and stimulation that work provides. This is especially true when the work involves using skills and experience, as it adds a sense of fulfillment and purpose to your life.

Engaging in such work will keep your brain sharp to enhance cognitive abilities as you age. You can feel fulfilled while reaping the benefits of an agile mind.

CON: Reduced Free Time

The beauty of retirement is the substantial freedom to spend your time as you wish. However, a new job may limit your abilities to embark on new hobbies, travel, and spend time with loved ones.

If you want to pursue a job during retirement, be sure to select a position that’s part-time and flexible. This will ensure that you have the free time you deserve to partake in the activities you desire.

PRO: Extra Income

It’s no secret that with a job comes additional income. While you most likely have a retirement fund arranged, a little extra money can go a long way.

Extra income can contribute to new hobbies, traveling, and treating your family with gifts. But that’s not all it’s good for.

The big question when buying a retirement home is how you will fund the endeavour. Purchasing a house is a costly investment, even if you’re planning to downsize. An additional income can cover portions of mortgage payments, property taxes, and maintenance costs for a more manageable investment.

CON: Social Security Benefits

While the additional income earned from working post-retirement can be advantageous, remember that it may impact your Social Security benefits. In certain circumstances, the Social Security Administration might reduce your benefits if you earn above a specific limit while receiving monthly payments. This could mean that they withhold a portion of your Social Security benefits.

PRO: Social Interaction

Retirement brings about one of the most significant changes: the loss of daily social interaction. Many individuals struggle to adapt to the sudden absence of colleagues and feel a sense of missing out. Continuing to work after Retirement lets you enjoy the much-needed social connection and fostering of new friendships. Continue Reading…

Mark Seed is a passionate DIY investor who lives in Ottawa. He invests in Canadian and U.S. dividend paying stocks and low-cost Exchange Traded Funds on his quest to own a $1 million portfolio for an early retirement. You can follow Mark’s insights and perspectives on investing, and much more, by visiting My Own Advisor. This blog originally appeared on his site Jan. 6, 2024 and is republished on the Hub with his permission.

Mark Seed is a passionate DIY investor who lives in Ottawa. He invests in Canadian and U.S. dividend paying stocks and low-cost Exchange Traded Funds on his quest to own a $1 million portfolio for an early retirement. You can follow Mark’s insights and perspectives on investing, and much more, by visiting My Own Advisor. This blog originally appeared on his site Jan. 6, 2024 and is republished on the Hub with his permission.