Once you achieve Financial Independence, you may choose to leave salaried employment but with decades of vibrant life ahead, it’s too soon to do nothing. The new stage of life between traditional employment and Full Retirement we call Victory Lap, or Victory Lap Retirement (also the title of a new book to be published in August 2016. You can pre-order now at VictoryLapRetirement.com). You may choose to start a business, go back to school or launch an Encore Act or Legacy Career. Perhaps you become a free agent, consultant, freelance writer or to change careers and re-enter the corporate world or government.

Shortly after Donald Trump was elected, I sold some of my Canadian index (XIU) holdings in Canadian dollars and bought a small-cap stock index in the U.S. called the Russell 2000, in U.S. dollars.

The Russell 2000 is a stock market index that represents the 2,000 smallest publicly traded stocks in the U.S. I purchased the ETF IWM, which tracks the Russell 2000, at $240.

What are small companies?

Small companies are those with a market value between $300 million and $2 billion. These companies are underrepresented in major indexes such as the S&P 500.

Reading the writing on the wall

I usually don’t let politics influence my investment decisions, but sometimes you have to read the writing on the wall.

In this case, Donald Trump made it clear that he:

Wanted to reduce taxes

Wanted lower interest rates

Wanted to increase tariffs

More precisely, he intended to impose a 25% tariff on Canadian goods. It would have been irresponsible for me to ignore this information and do nothing.

Reducing Canadian Exposure

My decision to sell the Canadian index was partially motivated by fear. Donald Trump’s clear stance on imposing tariffs on Canadian products signaled potential trouble for the Canadian economy and currency. Based on this, I decided to reduce my Canadian exposure and increase my U.S. exposure.

Why Small-Cap Stocks and Not Large-Cap?

Since much of my wealth is already invested in the S&P 500, which represents large corporations, I thought diversifying by market capitalization would be beneficial. Continue Reading…

In his 2024 re-election campaign, U.S. President Donald Trump vowed to pursue an aggressive trade policy that aimed to reduce or altogether eliminate what he viewed as unacceptable deficits between adversaries and allies alike. Following his January inauguration, President Trump has put Canada and Mexico into his crosshairs. Tariffs continue to be one of his favourite tools, if his rhetoric is any indication.

A tariff is a tax that is imposed by a country on the goods imported from another country. It is typically collected by a country’s customs authority. Some economists have argued that this results in a larger burden being paid by consumers, as companies will pass on tariff costs to the consumer.

In this piece, we will look at how ongoing trade tensions could impact world economies and markets. After that, we will zero in on ETFs that can potentially provide protection against the current bout of volatility.

Trade policy volatility and Canada

Last month, we looked at the impact the new GOP administration could have on the industrials space. That piece explored the trade policy volatility that existed in the first Trump administration.

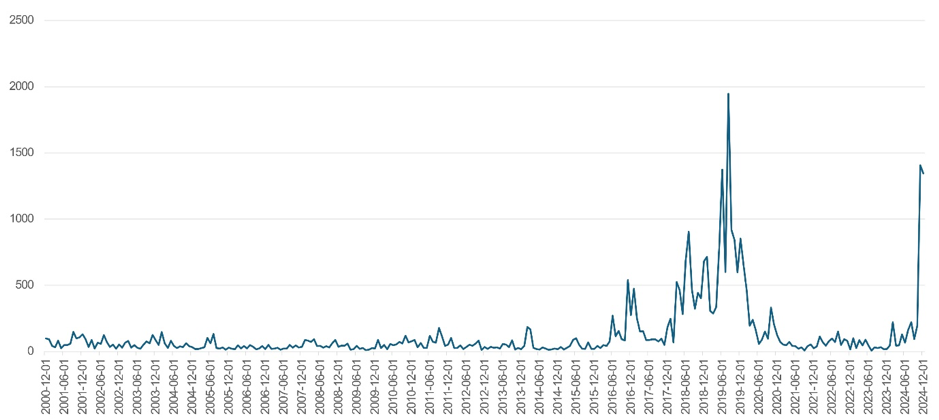

Baker, Bloom & Davis

US Categorical Economic Policy Uncertainty Index – Trade Policy

Source: Baker, Bloom & Davis. Bloomberg, Harvest ETFs, as of January 21, 2025.

On Monday, February 3, 2025, U.S. and global markets suffered sharp pullbacks in the morning hours. However, markets recovered after the Trump administration announced that tariffs on Mexico and Canada would be delayed for 30 days.

Canada finds itself at a crossroads as it contends with unprecedented pressure from a long-time ally, political uncertainty on the domestic front, and muted and decelerating economic data. The Bank of Canada must weigh these pressures as it determines how much it can slash interest rates to bolster economic activity..

That aside, Canada is home to many great companies with oligopolistic qualities. We detailed their strengths in a piece in October 2024. The Harvest Canadian Equity Leaders Income ETF (HLIF:TSX) invests in 30 of Canada’s most powerful and largest companies for their traits and growth potential. It overlays an active covered call strategy, which seeks to generate high monthly cash distributions.

Combat trade volatility with defence and diversification

Defensive sectors contain businesses that are stable, possess key barriers to entry, and are relatively immune to economic fluctuations.

Healthcare falls in this defensive category and is unique in its diversity. It includes companies that manufacture medical devices and equipment, as well as those that are involved in the making of diagnostic tools and lab equipment, companies involved in the ownership of doctors’ networks, as well as facilities and companies in the Managed Care segment.

The Harvest Healthcare Leaders Income ETF (HHL:TSX) is an equally weighted portfolio of 20 large-cap global healthcare companies. HHL aims to generate an attractive monthly distribution through an active covered call writing strategy. This ETF has paid out over $500 million in total monthly distributions to unit holders since its inception.

Utilities is a space that is often targeted by investors who are looking to shore up a defensive position in their portfolios. Companies in the utilities space possess enormous scale, significant barriers to entry, and dominance in their respective markets. The Harvest Equal Weight Global Utilities ETF (HUTL:TSX) offers access to a globally diversified portfolio of utilities equities. That global diversification offers benefits like reducing interest rate and natural disaster risk with exposure to different countries and regions. Continue Reading…

The following is an edited transcript of the podcast Two Way Traffic hosted by financial advisor Darren Coleman with his two guests: tax lawyer Trevor Parry and Kim Moody of Moodys Private Client which provides law, and cross-border tax and accounting services. Trevor Parry once told Stephen Harper that Canada has more auditors than infantry. Not to be outdone, Kim Moody says in the eyes of the Canada Revenue Agency a cocaine dealer can deduct expenses in this country, but not an Air bnb operator.

Click below for full link (interview conducted early January):

I’m joined today by Kim Moody of Moodys Private Client in Calgary, Alberta, and tax lawyer Trevor Perry, who is based in Ancaster. They are two of Canada’s most prolific tax fighters. We’re going to discuss where are we right now in terms of tax policy and what should Canadian investors be thinking about. Also, we have a new government in the United States.

Why don’t we begin with a little bit of kind of where are we right now? We just had the fall economic statement that was not delivered by your Finance Minister. But they came in at more than 50% higher than the fiscal guardrail that they set for themselves. So this is an astonishing amount of capital that they’ve spent, and not even remotely close to where they said they were going to be. Even $40 billion was a big number. So now that it’s 60 and there’s really no one to stand there and take accountability for it, and we had the Finance Minister resign just hours before she delivered that statement. So I’d want to focus on where does that leave taxpayers right now because there are a number of items. I’ll focus on the capital gains inclusion rate change as probably the most significant one. Where are we now? Is that going to go through? Not going to go through? What should investors be doing? What should taxpayers be doing with the state of change that we have in Ottawa?

Kim Moody

To your question on capital gains, where are we today? This is certainly one of the most unusual times in my career where we had proposed tax legislation that looks like it’s not going to get through. Trevor and I have been around a long time, and seen lots of tax legislation not get through. If I was a betting man, I’d say probably about 98% certainty that it’s not going to go through. And I’ve written about that in my Financial Post articles. So Trevor, do you know of any other, you know, broad based piece of legislation?

Trevor Perry

There was a lot of tumult when income trusts were attacked and all that kind of stuff. But the panic that was engineered this year to create some kind of revenue event because of forced selling, and it’s going to die because they prorogued Parliament. No, I’ve never seen anything like this before, and it’s just part and parcel of the worst in the history of this country, the worst tax policy from day one going on.

Darren Coleman

It’s really a quandary for investors and taxpayers, because the general rule has been, if I’m correct, that even though the legislation may not be enacted, one has to act as if it was going to pass, right? But as you guys have said, it’s very likely this will not pass. Should people, as they go into the tax year, be assuming that the new capital gains inclusion rate applies and act accordingly? Or should they act as if no, a betting man says it’s not going to happen, so I should just keep the old rates. What should you do?

Kim Moody

The CRA has a long-standing policy of encouraging taxpayers to act on proposed legislation. I think there’s a good reason for that, and I support them on that because 98% if not higher of tax legislation and proposed tax legislation gets passed even with retroactive applicability, which is very common in tax law. There were some recent statements attributed to the CRA saying they’re going to continue to administer the capital gains stuff on the basis that it’s law, even if an election is called. This stuff is not going to get passed if an election is called, and therefore you’re going to continue to administer it. Well, I can tell you, in my client base, I’m giving the exact opposite advice because I think there is a 98% chance this thing is not going through. So if you want to amend your tax returns for the two-thirds inclusion rate, go right ahead, but you’re going to do it without my blessing because I think it’s wrong, and you’re going to fight to get that money back. It’ll take a long time. So that that’s my approach.

Darren Coleman

How easy is it to fight to get your money back? Is that pretty standard? Like, no, don’t worry, they’ll refund it within five business days, or is it a big argument?

Kim Moody

No, it’s not usually a fight, per se, although there’s always exceptions to that, but it’s a matter of timing. You know when you amend your tax return? Number one, Have you filed your tax return? If so, then do you have the ability to amend it? Which, in most cases, you do, and then how long is it going to take for them to process it? Those are usually the pillars, and it’s that last one that takes a long time,

Trevor Perry

It’s part and parcel of a tax administration system that needs a complete overhaul. Given that they know everything you’re doing already we need some basic respect for the taxpayer, which is something we don’t have. I remember telling our last Prime Minister that there were more auditors in Canada than Canada has infantry. That’s the nature of the beast right now.

Kim Moody

And that’s increased by a lot. I think 29,000 CRA employees. So I think it’s almost 60,000 if I’m not mistaken.

Trevor Perry

And we have about 12,000 infantry, of which we cannot deploy them all at the same time.

Darren Coleman

Let’s go back over that greatest hits of outstanding tax policy that we’ve seen over the last year. Kim, you actually wrote about that in the Financial Post recently (late January). We’ve had the flipping tax. We’ve had the changes to AMT. We’ve had the unused, underused housing tax. We just had the move the date of which you can make a charitable contribution, because we had the postal strike.

Kim Moody

Kim Moody

Trevor knows I’m certainly no fan of the capital gains one, which I had ranked number one in the article as the worst policy. But number two is the prohibition of deductions on certain short-term rental owners. So if you happen to be an evil owner and operator of an Airbnb that operates in a jurisdiction that prohibits that, you’re denied all your expense deductions. A complete prohibition of deductions. So let’s pretend Trevor is a cocaine dealer. He’s out selling snow, but I’m just a lowly Airbnb operator. So Trevor makes 10 grand selling snow. But he’s got a bunch of people running around for him. He’s got burner cell phones. He’s got cost of his inventory, etc. So he makes net 2000 bucks, and he comes to me and says, Hey, Kim, I know I’m doing something illegal here. I’m selling drugs, but I don’t want to be a criminal twice. I want to make sure I file my tax returns because I don’t want to be a tax evader. So can you file my tax returns for me? So we go ahead and I file the tax returns. Do you think I’m claiming his deductions? His $8,000 of deductions? Sure, yeah. And there’s nothing in the Income Tax Act that prohibits that. But now I file the tax returns from my evil Airbnb operation that I’m operating illegally in a jurisdiction because I need to pay some bills, and I have the same $8,000 of expenses. Nope, I can’t deduct those, so I’m paying tax on $10,000. Now from a public-policy perspective, what does that say to the average Canadian? It tells me that the drug dealer in this fictional world, Trevor, is better off and should be treated better from a tax perspective, than me, the lowly Airbnb. That’s ridiculous policy. It’s dangerous policy, and it’s something that needs to go immediately.

Trevor Perry

For me as a lawyer and as a political junkie, I think our 1982 constitutional exercise needs to be reopened. Until we enshrine property rights in the Constitution, I believe, as a fundamental conservative that we do have property rights. Tax policy is horrible. But in terms of tax practice, having done lots of work for professional athletes, CRA running at baseball players and …

Darren Coleman

… The John Tavares situation.

Trevor Perry

If Tavares loses that you’re going to start seeing Canadian teams fold up and move again. It’s just absolutely stupid. And again, it goes to the whole issue of, why are we taxing people into oblivion at $245,000?

Darren Coleman

Darren Coleman

We did a podcast episode with Kevin Nightingale and Shlomi Levy talking about that. They don’t represent Mr. Tavares, so it was safe for them to comment. Listeners can go back and hear that podcast. We’ve also had some Toronto Blue Jays baseball players who had similar predicaments. They look like they’ve been resolved positively for the players. But those are not exactly the same situation as Mr. Tavares, so we’ll have to see what unfolds here. And as a big sports fan yourself, I know that one’s pretty close to your heart.

Darren Coleman

So now that we got into hockey, let me lure back our American listeners for a minute. Let’s pivot into what’s happening with our American cousins. They are going to go into a very interesting 2025. They have a new president. So the difference, I think, is going to be very significant between how the U.S. is going to adopt tax policy, and it’s a little concerning, I think, for many people that Canada doesn’t, apparently seem to have a functioning government at the moment. So what do you guys think Mr. Trump might do in his first year in terms of tax policy? What should investors be getting ready for?

Trevor Perry

I think you’re going to see them make the tax changes he brought in in his first term permanent. I think you’re going to get that lower corporate tax rate, which is going to cause great tumult in this country and in other countries, but particularly Canada. I think there’s going to be pressure here to have some kind of sensible corporate tax rate, the estate tax change. There won’t be any changes to estate taxation in the US for the foreseeable future. So there will be again, more reasons for, as Ross Perot called it, that great sucking sound of Canadian capital, both real and human, to leave the country.

Darren Coleman

But are they actually doing it? So gentlemen, have you actually seen evidence in your own practices of Canadians saying, I’m done, I’m out of here, and they’re actually making the steps they’re making, the move to leave, to lower tax jurisdiction. How many people are really doing it?

Kim Moody

Yeah, 1,000% and I’ve written about this a lot. I’ve spoken about it publicly. I’ve spoken at conferences about this. At one particular conference I spoke about this and there was an academic who was pro capital gains changes. So I showed the statistics but his rebuttal was, I don’t believe you. Here’s the statistics coming out of my office in Calgary. And we’re not a big office, but we’re about 85 people. We act for high net worth, ultra high net worth, private companies and individuals. In the first 23 years of my career — I’ve been practicing for roughly 31 years now — in the first roughly 23 years of my career, I did maybe a dozen departure tax files. It was really easy to leave Canada without incurring departure tax. That all changed. I want to say late 90s, am I right? Trevor, something like that, and and they made it a lot more difficult. And so in the last nine years, this increased with a new high personal tax rate. And then fast forward to the attack on small businesses in 2017 that caused a whole bunch of angst. COVID caused a whole bunch of out-of-control spending. And then the capital gains stuff was just kind of over the top. So all to say, in the last, especially five years, the number of files that I’ve worked on in the, you know, departure tax. You want to take a guess, Darren? Continue Reading…

The article was from the Harvard Business Review and highlighted 7 Hidden Traps of Retirement, which the writers discovered during interviews with “dozens of highly respected former chief executives.”

As I read the article, I realized the traps of retirement don’t apply only to folks retiring from top management positions.

These traps present a risk to all of us.

Today, I’m presenting each of the 7 Hidden Traps of Retirement and my thoughts on how best to avoid them.

The article that made me think was The Challenges of Retiring from a High-Powered Job, written by three founders of ONYX, an invitation-only group designed to build a community for current and former CEOs. I encourage you to read the article, but I’ll summarize the key points below.

In their work helping CEOs prepare for retirement, the team has discovered seven hidden traps of retirement. While focused on senior managers, I’m taking a different twist with their list and considering how these traps apply to all of us. I’ve taken the liberty of renaming each of the seven hidden traps of retirement to better align with the readers of this blog and providing my thoughts on how to avoid falling into each.

The risks apply during our planning for and transition into retirement. If you’re struggling with the transition into retirement, perhaps it’s because you’ve fallen into one of these traps.

1. Focusing on who you are, instead of who you want to become.

Original Title: Looking through the lens of the present impedes you from seeing future possibilities.

In your final years of work, it’s easy to procrastinate on retirement planning and focus on your current role. You’re busy doing your job and you can deal with that retirement stuff after you’re done working. That’s a dangerous approach that far too many people follow. It’s one of the traps of retirement for a reason. Seeing beyond your current role requires a creative imagination, the type that has likely been dormant for years. Losing your sense of identity can be a shock in retirement, but the impact can be minimized by the appropriate planning.

How to Avoid the Trap:

Forget about your current role for a minute. After all, it will be irrelevant the day after you retire. (Let that sink in)

Think about what you want your life to BECOME in retirement. You’ll no longer have that title, and that sense of identity you get from your work will be gone. That’s scary, and something a lot of people avoid thinking about. Don’t be that person. Rather, think about your new identity in retirement. What do you want to be known for? What areas are you curious about? What did you do as a child that you’d like to revisit now that you’re free from those chains of work? Carve out time to think about what impact you want to have with your newfound freedom. It takes some time, so be patient. The important thing is to think beyond your current role and imagine what you can do to make a difference once the job is gone.

In What I’ve Learned From Writing 400 Articles About Retirement, I wrote about my new identities in retirement (writer, running a charity, grandfather, etc). A quote from that article is relevant here, and I’d encourage you to adopt it as one of your goals in retirement:

“I’m not who I used to be, and I love who I’ve become.”

2. Focusing on too many options.

Original Title: A wealth of options can overwhelm and paralyze decision-making.

That busy schedule and rigid structure will disappear when you retire, and you’ll be looking at a “blank sheet of paper.” Having no schedule or structure to your day sounds appealing, but it becomes disorienting after a surprisingly short period. Your brain will start searching for something to do, and you’ll have difficulty prioritizing what you want to do with your life.

How to Avoid the Trap:

Take some quiet time to think about what impact you want to make with your retirement years. Think about the causes you have a passion for. Listen to your inner curiosity, and take that first step to see where it leads. When you’re thinking about something you could do, compare it to that list of things that matter to you. For example, you may have enjoyed working with younger people during your career and would like to find a way to do that in retirement. Perhaps you’ll become a mentor, a Big Brother, or a business coach to the next generation.

Find your “North Star” and pursue only those opportunities with strong alignment to the things that matter to you. Don’t pursue “busyness” for the sake of being busy. Rather, invest your time in areas where you have a real interest (lack of experience doesn’t matter, as I’ll demonstrate below).

Using your time to impact an area you care about is the true path to happiness.

3. Not building relationships outside of work.

Original Title: Relying on your old network can distract you from the critical task of building your new one.

Everybody thinks they’ll keep in touch with folks they worked with. Almost no one does. It’s one of those strange realities of retirement, and it will likely happen to you. (Note this statistic in “Shining The Light on Retirement Blind Spots”: 62% of retirees missed the relationships from work, whereas only 29% of pre-retirees expected it to be an issue).The relationships at work are about “work.” Once you’re out of the scene, it becomes difficult and awkward to maintain those relationships.

And yet, relationships matter.

I dedicated an entire chapter in my book to relationships. People think about their paycheck stopping when they retire, but they often overlook the “softer” benefits they receive from work which will also disappear:

Structure

Sense of Identity

Relationships

Sense of Purpose

Sense of Accomplishment

Ironically, these 7 traps of retirement align almost perfectly with that list. That doesn’t surprise me in the least. If you’re a regular reader, you know I’m passionate about the importance of the “soft side” of retirement.

How to Avoid the Trap:

In your final year or two of work, be intentional about building relationships outside your workplace. Your mission: build relationships that will be there after you retire. Spend a few Saturdays volunteering at a local charity. Get involved with a few Facebook groups in your area that do things that interest you. Join a gym and learn to play pickleball. Join a local hiking club. Go to a Trout Unlimited meeting. Call an old friend. Attend a local church.

Explore whatever interests you and pay attention to the people in the groups you visit. In time, you’ll find a group that feels “right.” Pay attention, that’s where you’ll get your retirement relationships.

They matter more than you expect.

4. Waiting to figure out retirement until after you retire.

Original Title: Delaying retirement planning can lead to urgent, anxious, and awkward outcomes.

A quote from the original article is telling:

“The majority of CEOs and executives we talked with told us they failed to appropriately plan for their retirement — and nearly all told us they waited too long to start.”

It is, perhaps, the most common of the traps of retirement. Many people are nervous about retirement, and procrastination is a common response. “I’ll deal with it when I’m retired,” many people think. That’s one approach, but research has shown that taking that route will lead to a difficult transition. The cliff is coming, and you can prepare your parachute or just take the leap and figure it out once airborne. I recommend the former approach, it makes for a much smoother landing.

How to Avoid the Trap:

As I was in my final working years, I was interested obsessed with figuring out why some people had a smooth transition to retirement, whereas others struggled. As I’ve written before, there’s one single element that is the most highly correlated with the smoothness of your transition. That element?

The amount of time you spend planning for retirement in your final years of work (both on financial and non-financial issues).

Spend a lot of time planning, and your retirement will be smooth. Ignore it until you retire, and buckle in for a rough ride. As I wrote in The 4 Phases of Retirement, only 15% of retirees skip over the dreaded Phase II. I was lucky enough to be one of them. So can you. Continue Reading…

A key concern many investors have at the moment is the impact of Trump’s tariffs on goods produced outside the U.S. on the markets. I’m hearing from those wondering if they should do something to protect their wealth; their primary question is: What should I do with my investments?

My answer (as it usually is when investors are concerned about the geopolitical impact on the markets): stick with the plan because, by the time the news is public and you become concerned, the markets have already accounted for it/priced it in, so any reaction you take is too late.

A useful historical reference on tariffs is President Trump’s first term. Starting in 2017, his administration targeted China, implementing tariffs on a broad range of products by 2018. The following years saw ongoing trade negotiations that led to an agreement, though many tariffs remained. Despite the uncertainty, both U.S. and Chinese markets outperformed the MSCI World ex USA Index over Trump’s four-year term. Have a look at the data from 2017 to 2020, as Dimensional compares China MSCI Index to US S&P 500 Index to MSCI World ex USA Index.

Markets are forward-looking, meaning that the potential economic effects of tariffs are likely already factored into current prices. As a result, when these anticipated changes materialize, their impact on markets may be limited.

Understanding how Market Pricing Works

Let’s talk about the price of stocks.

It stands to reason: To make money in the market, you need to sell your holdings for more than you paid. Of course, we’re all familiar with good old “buy low, sell high.” But despite its simplicity, many investors fall short. Instead, they end up doing just the opposite, or at least leaving returns on the table that could have been theirs to keep.

You can defend against these human foibles by understanding how stock pricing works and using that knowledge to your advantage.

Good News, Bad News, and Market Views

How do you know when a stock or stock fund is priced for buying or selling?

The short answer is, we don’t.

And yet, many investors still let current events dominate their decisions. They sell when they fear bad news means prices are going to fall. Or they buy when good news breaks. They invest in funds that do the same.

While this may seem logical, there’s a problem with it: You’re betting you or your fund manager can place winning trades before markets have already priced in the news.

To be blunt, that’s a losing bet.

You’re betting that you know more about what the price should be at any given point than what the formidable force of the market has already decided. Every so often, you might be right. But the preponderance of the evidence suggests any “wins” are more a matter of luck than skill.

Me and You against the World

Whenever you try to buy low or sell high, who is the force on the other side of the trading table?

It’s the market.

The market includes millions of individuals, institutions, banks, and brokerages trading hundreds of billions of dollars every moment of every day. It includes highly paid analysts continuously watching every move the markets make. It includes AI-driven engines seeking to get their trades in nanoseconds ahead of everyone else.

And you think you can beat that?

We believe it’s far more reasonable to assume, by the time you’ve heard the news, the collective market has too, and has already priced it in.

News of a recession, under way or avoided? It’s already priced in.

Inflation on the rise, or abating? It’s already priced in.

A company suffers a calamity or makes a major breakthrough? It’s already priced in.

The government passes critical legislation that helps or hinders global trading? It’s…

And so on. Here’s your best assumption:

If it’s public knowledge, it’s already priced in.(And if it’s insider information, it’s illegal to trade on it.)

What we don’t yet Know

As soon as an event is priced in, several things make it difficult to profitably trade on the news:

You’re Buying High, Selling Low: If you trade on news after it’s been priced in, odds are you’ll buy at a higher price (after good news) or sell at a lower price (based on bad news). Continue Reading…