There is something very wrong with the work world today. It is far too common to find employees who are tired, over-worked, stressed out, and living in fear of an uncertain future.

There is something very wrong with the work world today. It is far too common to find employees who are tired, over-worked, stressed out, and living in fear of an uncertain future.

As a result, people are eating too much, watching too much television, and complaining too much, often self-medicating with drugs and/or alcohol or taking prescription medication to cope with their stress.

How can it be that in North America, with two of the most prosperous societies in the world, people are taking more medications for anxiety, depression, and sleep disorders than ever before?

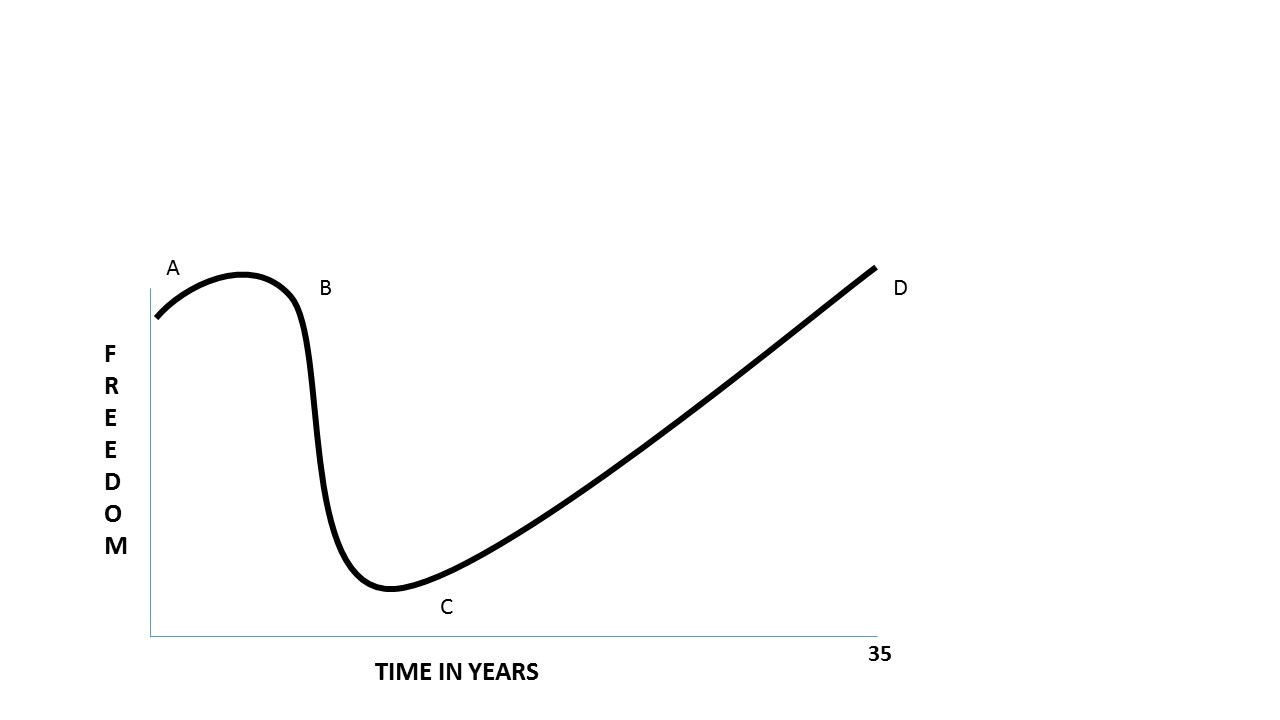

Blame it on the big dip.

The graph above represents a typical person’s (mine) working lifecycle. I call it the “big dip” as it’s only fair to recognize Seth’s influence on the development of the concept.

You will note two axises, the vertical one representing personal freedom and the horizontal one representing time spent in years. The graph isn’t to scale but it does get the point of the story across. Be warned, it might scare you: it gave me the jitters when I first drew it so you might want to sit down for this one.

Entry point A is when you leave school and start working, maybe in a “corp.,” like I did. It’s a happy time. Life is fun and exciting and you do not have any significant worries. You are finally making some real money for the first time. One could reasonably say a person at this point is financially independent. They carry no personal debt, their parents still provide them with a roof over their head and food on the table. Life is as simple as it could be. Work-Eat-Have Fun-Repeat.

Everyone’s goal at this point is similar. Work hard, get promoted and make more money. This was the path to success as taught to them by their parents and teachers and every kid wants to look successful in the eyes of their parents, right? Continue Reading…