As Didi says in the novel (Findependence Day), “There’s no point climbing the Tower of Wealth when you’re still mired in the basement of debt.” If you owe credit-card debt still charging an usurous 20% per annum, forget about building wealth: focus on eliminating that debt. And once done, focus on paying off your mortgage. As Theo says in the novel, “The foundation of financial independence is a paid-for house.”

I have to admit that over the years, I have personally favoured cash or debit cards, on the theory that you can’t get in too much trouble spending money you’ve at least already earned. To me, overspending to rack up “Points” for even more consumption is just not worth it, especially if it also means ever having to pay the dreaded double-digit interest rates that accompany most every credit card these days.

Reluctantly, however, I’ve come round to the view that with proper discipline, credit cards can provide convenience, a paper trail and most important, more security than debit cards in several situations. And yes, while I’m not driven by it, there may also be the convenience of “points” on purchases, points the writer says can amount to 2 to 6%.

The key, as it always is with credit cards, is to make sure you never get caught paying those exorbitant rates of interest. I’ve never quite understood how it is we’ve been in an era of almost-zero interest rates the last five years when you’re lending out money (via bonds or GICs) but when you’re a debtor suddenly the rate is close to 20%. Am I the only one who thinks there’s a major disconnect here? Better to be on the receiving end of that deal rather than the dishing it out deal: I wish I’d bought Visa or Mastercard stock a few years ago.

Using credit cards as if they were debit cards

The valuable point made by the writer — Jeffrey Weber — is that he finally “learned how to use my credit card like a debit card.” By paying off the full balance each month, never spending more than he can afford and “eliminating interest from the equation,” he is able to avoid using debit cards at all while enjoying the few advantages that go with prudent use of credit cards.

Personally, I do one of two things now, both of which are variants of Weber’s approach. Earlier this week, with Christmas presents for others high on the agenda, I loaded up my MasterCard with several transactions. I also did the same with my business Visa card for some needed equipment. In both cases, when I returned from the shopping spree, I signed on to my home computer and immediately used my online banking to pay off the newly incurred debts instantly. Yes, I realize I could have delayed a few weeks to benefit from the free “float” but I don’t wish to tempt the fates. If you’re going to use a credit card like a debit card, in my mind that means moving the funds out of your bank account the moment (or at least by end of day) you’re incurred the purchases. Besides, who wants to have a fabulous holiday season only to have it all ruined by humungous bills to be paid by the middle of January. That’s TFSA season after all!

The second variant is more foolproof and will even let you take advantage of that float I’m missing out with the “ad hoc” method. Just ask your friendly local financial institution to automatically move funds from your bank account to pay off any outstanding balances before any interest charges come due.

The 5 places you never should use debit cards

Weber’s article lists five specific situations where someone still juggling both credit cards and debit cards should use only credit cards. I’ve just listed the headings: go to the original link for his rationale on each point:

From US News -Money, Intuit Inc.’s consumer money expert Holly Perez describes five ways Millennials Can Achieve Financial Independence. The article is a straightforward account showing five ways American millennials can and should be preparing themselves for future financial security. Take these steps in your 20s and you may even find yourself a millionaire by your 60s!

Remember Budgeting 101 — Even if you don’t think you need a budget, creating one will help you become more aware of exactly where your money is going, which will help you eliminate any possible over/ unnecessary spending

Ditch the Debt — Pay off all your debts immediately, starting with those high-interest credit cards. Student loans and car payments should be dealt with after.

Make Savings a Priority — A habit that every millennial should get into is to save a few hundred dollars a month. for Americans, ensuring they are contributing to, and understanding their company’s 401(k) is an essential part of this step.

Think About the Future — Make sure to set concrete goals about what you want from your future finances. Making these decisions while you’re young, and sticking with them will be immensely beneficial to your future self. Putting these goals in writing- either on paper or with the help of an app- will help you to follow-through and stay on track.

Track your Credit Score — Your credit score will be invaluable to you when you go to make a big purchase one day, so ensuring it is the best it can be is quite important to maintaining financial independence later on. To keep this number high, the article includes tips like keeping your oldest credit cards open, paying bills on time, and avoiding maxing out cards.

I haven’t noticed many changes since Scotiabank bought out ING Direct in 2012, except for two:

They changed the name to Tangerine

Why did they do this? Is it a fruit? Is it a colour? WHY? People like my parents already think ING is a fake bank that will steal all my money: calling it something as light and fluffy as Tangerine does not help my case that it is a real bank with real interest rates, and that banks with tellers and real estate are as 20th century as AOL.

I will forgive them, however, because CEO Peter Aceto told Canadian Business that they weren’t allowed to use the name ING anymore. Here’s the rationale behind that decision:

“Simplicity”and “innovation”were two things the bank wanted to come across in its new name—the idea was to hearken back to its earlier days (being an alternative, simplified place to do your banking), but push the brand forward at the same time. The name Orange was considered on the shortlist, but was considered to be “too safe or obvious of a choice.”Tangerine makes reference to ING Direct’s orange history, (Ed Note [DK]:by orange history, do they mean just using the colour orange? How does a bank have colour history?) while also being significantly different.

Aceto says part of the branding discussion also took into account the more “fun”aspects of the name.

“We understood the risk that a name like that could be interpreted as being silly, or not serious,”he says. “Banking is important, it’s serious. We’re asking you to give us your life savings, or to help you buy a home or invest.”

That’s why there won’t be any references to fruit in any of Tangerine’s advertising materials or promotional campaigns. The fun name “does a lot of work for us”in sparking interest in Tangerine, Aceto says, but service at the customer level needs to be thoughtful and earnest in order to build a client base.

“I want people to think, oh, they’re different. They’re not like everyone else.”

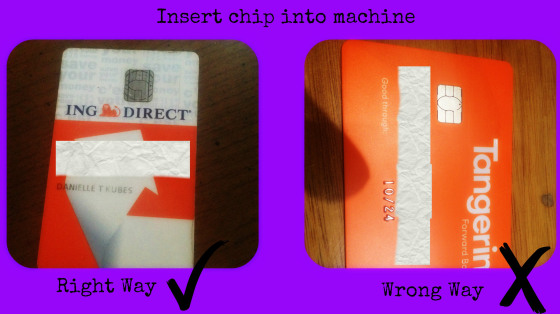

They changed the debit card by making it flimsier and WRONG

Writing the bank name horizontally across a debit card made sense when we signed for things.

Now we use a chip and PIN# method of payment. The chip is always entered vertically.

So why, on all debit cards, is the bank name still horizontal?

ING was the only card to write its name vertically, which was logical and made them seem the most current.

With the buyout, it has gone backwards and written its company name horizontally.

Also, while you can’t see this in a picture, the new card is very flimsy and bendy. It’s not really a problem but coupled with Tangerine it just kind of makes the bank seem flimsy.

Now, these are all personal pet peeves that have no affect on how they do business; banking with them hasn’t changed. They don’t have the best interest rates anymore; that award would go to credit unions in Western Canada, but they are still way better than the Big Five banks and they also have lower fees (no fees!) than the credit unions.

All in all, it’s still my favourite Canadian bank with which to do my daily banking, but it’s no longer my favourite choice with which to invest in GICs, which will be the subject of another post.

Here’s how this article originally appeared at Danielle’s Pretty Little Poor Girl blog. And you should click on the link because apart from Danielle’s awesome slogan, she includes an extra paragraph at the bottom of her original post that further teases the good folks at Tangerine: JC.

Below is the text for a speech I delivered Monday evening at Toastmasters Port Credit. I’ll be devoting some full blogs to Toastmasters in time, probably under the Entrepreneurship section, because it helps people of any age cultivate two critical skills: public speaking and leadership. Since the idea is to speak without notes, my actual delivery was not identical to what you see below. It has been adapted for the blog but in a few days I may put up a video of my performance, which was clocked at around eight minutes. I imagine this expanded version would take 15!

Jon Chevreau (Twitter).

Thank you Mr. Toastmaster, fellow Toastmasters and esteemed guests. As I look around this room, I see a mix of people: everyone from students and those just embarking on the workforce to people who are already retired.

I’ve worked as a financial journalist for more than 20 years and can tell you the word Retirement is a favorite word of both the financial industry and the media. It’s a handy way to depict a far-in-the future “dream” that conveniently helps banks, mutual fund companies, insurance companies and others sell various financial products, from funds to annuities. And we in the media are almost as fond of the term retirement: I’ve seldom witnessed a newspaper, magazine or web site that turned away financial advertising!

I’m 61 and you could call me semi-retired. But my message to the younger people in the audience, and even some of the middle-aged ones who fear they’ve not saved enough, is FORGET RETIREMENT!

Is this heresy? Not at all. Because there is a better term: Financial Independence. As some of you may know, a month ago I launched a new web site called the Financial Independence Hub and everything I’m saying here can be found at the site.

XY Planning’s Alan Moore

In fact, it includes a guest blog by Alan Moore of XY Planning Network in the US who posted a blog on exactly the topic I’m talking about here. The X and Y refers to Generations X and Y, so he is providing financial planning advice to millennials and young people. And he too is telling them to forget about retirement but instead to seek Financial Independence.

Aren’t the two terms the same thing? Not really. To me, Retirement is the full-stop retirement our parents or grandparents enjoyed if they were lucky. They got a job out of college, enrolled in a Defined Benefit pension that guaranteed a certain steady future stream of income, hung in for the gold watch for 30 or 35 years, then retired at the traditional retirement age of 65. They could now watch day-time TV, golf, nap, play bridge or putter in the garden to their heart’s content for a decade or three. This is what I call the “full-stop” sudden retirement.

Perhaps some of you here are now enjoying such a retirement. Like Mark over there.

Show of hands: how many of you younger people here think they’ll be able to rely on a DB pension when they’re as old as Mark or me? And how many think they’ll stay with a single employer long enough to collect a big enough pension that they’ll never have to work again?

To the young, Retirement is a remote unattainable concept

The problem with the term Retirement is that it seems so terribly far away for young people. The official retirement age keeps rising: it’s now 67 for younger folk instead of 65, if you’re talking about the eligibility age for Old Age Security, and I wouldn’t be surprised if it reached 70 at some point. So telling a 20-year old they should cancel their SmartPhone service in order to save money for a retirement half a century away is hardly an inspiring message, is it?

But that’s what all the retirement peddlers want you to do: put away 10% or preferably 20% of your income by practicing delayed gratification. They may tell you that you’ll need a million dollars or more in order to retire one day. Too often, sadly, young people hear that and figure it’s so impossible they may as well give up and spend it while they have it.

In other words, they are telling young people that in order to enjoy a decade or two of leisure when you’re old and grey, that you need to deny yourself pleasures like travel or eating out while you’re enjoying your youth.

Let me tell you, any of the grey hairs here would probably love to take their retirement savings and use it to book passage on a time machine that would let them relive the Swinging Sixties. If you’re 20 today, I imagine that your 70-year old future self would feel the same way about your life right now.

A more attainable goal

So what do I suggest as a substitute for the word Retirement? I call it Findependence, which is just a contraction of Financial Independence. I’ve written a book, Findependence Day, which is just the day you’ve reached Financial Independence. The ebook I talked about in my third speech here is a sort of “Coles Notes” summary of that book.

Financial independence is generally used to describe the state of having sufficient personal wealth to live, without having to work actively for basic necessities.[1] For financially independent people, their assets generate income that is greater than their expenses.

In practice, I think this means being able to survive without the single stream of income most call a full-time job.

Leaving the nest at 27 is NOT Financial Independence!

Defined this way, Findependence can occur decades before the traditional Retirement, so it’s a goal that young people may find is more worth shooting for. Interestingly, last week I blogged at MoneySense and at the Hub about a study about young people and their financial readiness to leave home. They used what I consider an incorrect definition of financial independence: that if they left the nest and stopped depending on the Bank of Mum and Dad, that they were therefore financially independent. If they could get a job and pay their rent, that was the definition, which resulted in the absurd headline that most millennials hope to be financially independent by age 27.

I don’t think so. Even with DB pensions, the earliest most people aspired to Financial Independence was 55, which is the earliest some pensions permit early retirement. Anyone hear of Freedom 55? That London life campaign was one of the most successful sales pitches for Early Retirement. Yet only a few government workers or business executives who strike it rich ever retire that early.

Why do billionaires keep working?

Why is that billionaires like Warren Buffett continue to work? Or young tech entrepreneurs like Mark Zuckerburg? Don’t you think Zuckerburg, who’s all of age 31 or so, couldn’t be findependent by now? Obviously, they have passion and are driven by purpose.

What does that tell you? Age 55 is way too young to “retire’ in the classic sense of doing nothing: playing golf, watching daytime TV, reading all day. Yes, many people THINK they’ll travel all the time once they retire but as I wrote on another blog last week, travel is overrated and expensive, and is really something you would only want to do some of the time, not ALL of the time.

Integrating the Three Boxes of Life

Findependence is about integrating education, work and play. On my sister site, Findependence.TV, I’m interviewed about a concept called The Three Boxes of Life, which is the title of a classic book by Richard Bolles. In the old days, we started life in the first box, Education, spent 15 or so years there, then graduated to the second box, Work. We stayed there for 35 to 50 years, and then came traditional Retirement, the third box of total play and leisure.

On the video, I talk about there being really only a single day: you work a bit each day and make money, you learn a bit each day and at the end of the day, you may “play” by getting some exercise, reading, watching TV or whatever.

On the site, there are blogs on concepts like mini-retirements and the four-hour workweek. Wouldn’t it make more sense to take the occasional mid-career sabattical or series of three-month vacations earlier in life, rather than saving it all for ten or 20 years of doing nothing when you’re too feeble to appreciate it? That’s why the subtitle of Findependence Day as well as The Financial Independence Hub is “While you’re still young enough to enjoy it.”

Plan for Longevity, not Retirement

Meta celebrates her 98th birthday. With Alizon Sharon (c) and Ruth Snowden (r).

Life expectancies are on the rise because of advances in medical science and more of us are practicing better health habits, with a focus on proper diet and exercise.

We can all expect to live a lot longer than we once thought, which is why the “Hub” ends with a section on Aging and Longevity. There you’ll find some blogs by Mark Venning of ChangeRangers.com, who coined the phrase “Plan for Longevity, Not Retirement.” I think it’s a great concept.

And it isn’t just a theoretical concept. On Sunday, we had a dinner party for a female friend of ours who celebrated her 98th birthday. She showed us a custom-printed card from – get this – her co-workers. You see, Meta still works two half-days a week at a local printing company. So she still spends a little time in the Work box. She also reads a lot, swapping books with my wife (Ruth, above), so part of her days are in the Education box. And she still travels and parties, so that’s the Leisure box.

Overspending is a common problem for many people; it creates debt, anxiety and relationship problems, even among high income earners. All too often, people’s spending habits seem to rise to meet – and exceed – their incomes.

So why does this happen? What compels people to overspend when they already have the items they truly need? The answer lies deep within each person’s spending personality. Recently, I read Dr. April Benson’s book I Shop Therefore I Am, and was fascinated by what the contributing authors uncover about the emotional and psychological factors influencing our buying habits.

I thought it would interesting, and beneficial, to touch on the six key spending personalities they explore: image spenders, bargain hunters, collectors, compulsive shoppers, co-dependent spenders (a.k.a. gift-givers) and bulimic spenders. Continue Reading…

From Daily Finance comes this useful (and timely, given the season) article on the times when debit cards should be avoided in favour of credit cards.

From Daily Finance comes this useful (and timely, given the season) article on the times when debit cards should be avoided in favour of credit cards.