By Jean Salvadore, Director, Wealth Insurance, RBC Insurance

By Jean Salvadore, Director, Wealth Insurance, RBC Insurance

(Sponsored Content)

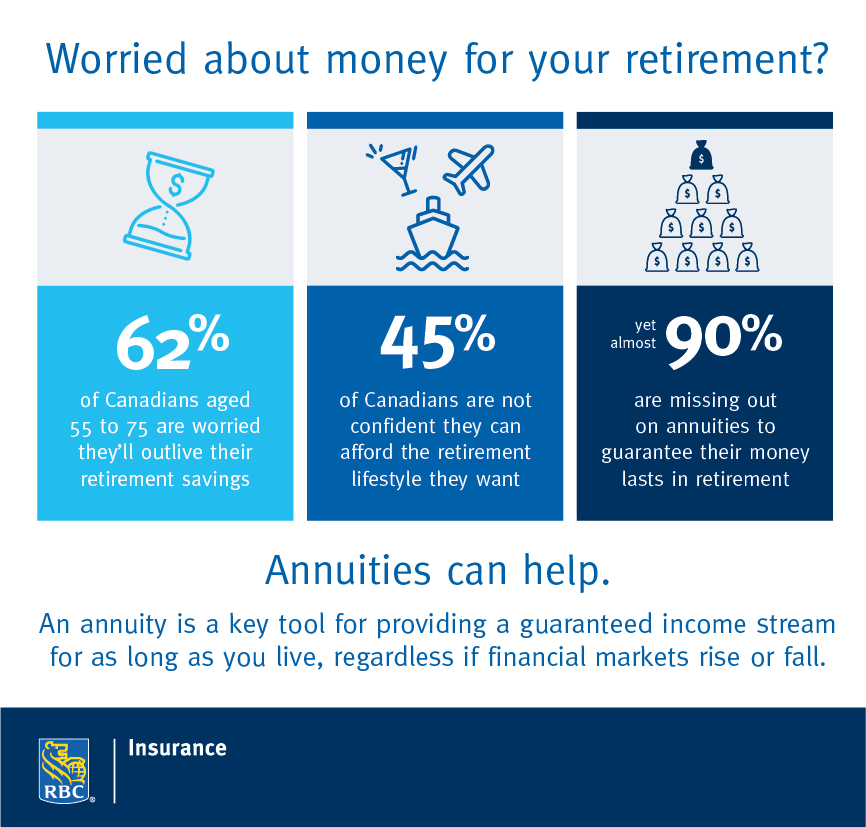

Summary: While Canadians want to live a full lifestyle in their retirement, a majority (62 per cent) are worried about outliving their retirement savings. The majority are missing annuities in their portfolio that can help guarantee an income stream in their retirement.

If you’re like most Canadians, your vision for retirement includes a full roster of activities such as travel, dining out and shopping for the things you want. But while many of us look to our retirement years as a time to enjoy life to the fullest, having enough money to support that lifestyle is a real concern. Canadians are living longer than ever before and, according to a recent survey by Ipsos for RBC Insurance, the majority (62 per cent) are worried that they’ll outlive their retirement savings.

In fact, even with various financial tools in place such as RRSPs and TFSAs, almost half of Canadians are still not confident that they will be able to afford the lifestyle they want. And perhaps not surprisingly, what’s most important to that lifestyle is keeping a sense of independence. Among those between the ages of 55 to 75, eight out of ten want to live at home for as long as they can and 72 per cent say it’s important to own a car. On top of that, almost three-quarters (68 per cent) would like to be able to travel at least once a year, shop for the things they want (62 per cent), and go out for lunch or dinner a few times a week (53 per cent). Continue Reading…