By Dale Roberts, cutthecrapinvesting

Special to the Financial Independence Hub

Bonds are the adult in the room. And when they speak, we should probably hear them out. This week [late June] bonds went on a tear. What were bonds trying to say? They were listening to the ‘Fed Speak’ in the U.S. that left many confused. Of course, the Federal Reserve and the Federal Reserve Chairman set the overnight rates that affect bond markets and our borrowing costs. It’s an economic lever. Maybe the adults in the room are suggesting that inflation is not a threat? We’ll see deflation in the near future? Or maybe a recession is closer than we think?

Here’s a good barometer for the bond market and economic sentiment – long term U.S. treasuries.

They’ve had a good month (and more) and they had an explosive week. The index ETF was up about 3% over the last two days. Long term treasuries are known as some of the best stock market risk managers. They punch above their weight.

Must read: Bonds are the adult in the room.

Recently I suggested that the stock and bond markets are buying the transitory inflation argument.

And in my most recent MoneySense weekly I had a look at some of the economic data for Canada and the U.S., including that recent Fed Speak and reaction.

Perhaps the bond market is going well beyond saying ‘inflation is transitory’. Let’s have a listen to what a few experts say about this weeks stock and bond activity.

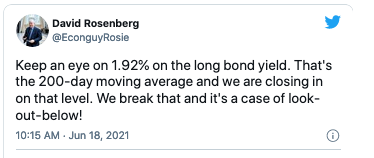

David Rosenberg says look out below.

In a recent Globe and Mail piece Mr. Rosenberg suggested that inflation jitters will turn into deflation fear by year end. (pay wall) Of course bonds like deflation. And that’s one reason why we hold bonds right? Even though almost no one thinks that we could enter a long period of economic contraction and deflation. From Mr. Rosenberg …

“When these temporary disturbances fall out of the data, people are going to be surprised at how low the readings are going to be on these official inflation statistics,” the famed Canadian economist said in an interview Friday.

“I think we’re going to go back to talking about disinflation and deflation [by] the end of the year.”

The boring balanced portfolio is having its way these days. Stocks for growth and bonds for ballast and no-growth scenarios. Readers will know that I am also a fan of covering off inflation as well, you’ll read about that in the new balanced portfolio.

Investing is like a box of chocolates.

To quote Forrest Gump, you just never know what you’re going to get. This past week gave us that big and important reminder. Who would have thought that bond investors would have a such a sweet week? I’m happy to hold long term treasuries and that TLT and the BMO Canadian dollar version in ZTL.

Mike Philbrick at ReSolve Asset Management offered via Twitter …

No one knows the future price of any asset class so diversification is incredibly important as the first line of defense.

And as an example, pick your poison of inflation or deflation or economic shocks of any variety. More from Mike …

Another great example, why making sure investors are always exposed to inflation shocks rather than trying to time it … Money and mindshare piled in recently but all the returns came months before that, when investors were not noticing.

Perhaps there is no real economic growth?

Perhaps the bond markets echo Lance Roberts (no relation), CIO and partner at RIA Advisors, with respect to what is real and sustainable economic growth?

The reason that rates are discounting the current “economic growth” story is that artificial stimulus does not create sustainable organic economic activity.

And on the inflation front from Lance, you can’t create real inflation from artificial growth. From that post …

Yes, we see that word “deflation” again.

Rethinking the 60/40 portfolio?

That has been a hot topic for quite some time given the low yield environment. Many suggest tweaking up your equity exposure to the 70% level or so, if you have the risk tolerance. That was certainly covered in this post on the Horizons one ticket ETFs. Those portfolios employ U.S. Treasuries that help dampen the volatility of increasing equity exposure. Continue Reading…