By Aman Raina, SageInvestors.ca

By Aman Raina, SageInvestors.ca

Special to the Financial Independence Hub

NOTE: This review was initially undertaken using data compiled as of January 30, 2020, which marked the 5-year anniversary during which the portfolio was active but prior to the severe market turbulence that occurred in February and March 2020. As it became apparent that the market pullback was becoming an epic meltdown, additional data was compiled and included into the review.

Five years ago I embarked on a personal experiment. I was having a hard time getting any insights on the effectiveness of a new investment services that was shaking the ground at the time in 2015.

Known or labeled as Robo Advisors, these new wealth management companies offered services to invest on behalf of others using an online platform and a combination of algorithms and computer coding to buy and sell specific investments and manage portfolios. Five years ago these firms were just stepping into the investing consciousness, but since then they have mushroomed and even traditional investment companies are now offering some flavor of online investment management services.

It all seemed quite appealing; however, there was one thing that many marketing materials, blogs, and mainstream media were avoiding … do these types of services make money for investors? Is this the type of service that would successfully bring more people, who naturally feel intimidated and frustrated by the whole investing concept into the investing domain?

Since no robo advisor company back then was interested in disclosing their performance (they still avoid it) other than citing research that their low cost/passive oriented strategy is superior, I decided five years ago to try an experiment to get some more insights that did not involve boilerplate marketing speak. I set up an account with one of the “large” Robo Adviser firms and invested $5000 of my own money into it.

My goal was to go through the process and blog about my experience using the service, how the ROBO went about making decisions and how it managed my portfolio, and more importantly, the results. I’ve always said that we need a good five years to really get a handle on how effective these services are compared to traditional wealth management services. Well, I just crossed the five-year mark of my ROBO journey, so let’s check back in and take a look at how it’s been doing. I’ve also said that I would reserve my opinions about this service until we reached that five-year threshold. Well here we are and I’m ready to unload my takes.

2019 was an epic year for stocks. US major stock indexes were up just over 30 per cent on the year. Fantastic returns. Hopefully my ROBO got a good piece of that action.

Performance

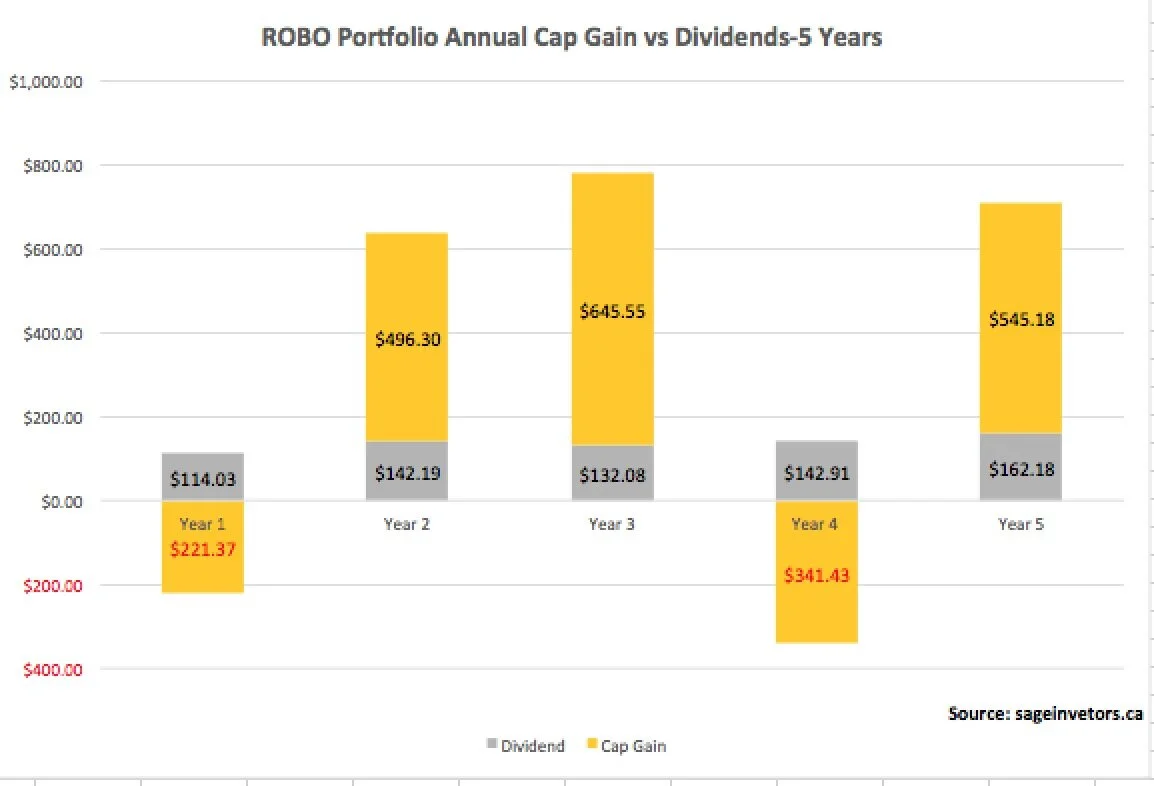

Overall, my ROBO portfolio posted a solid year. The portfolio was up 11.6 per cent year over year, a nice rebound from the previous year where it lost 2.1 per cent. Over the 5 years, the portfolio generated positive returns in three of the 5 years, and posted double-digit returns in those three years. The portfolio increased by $707, of which $162 came from dividend income while the remaining $545 came from capital gains. Over the year period, the ROBO portfolio increased from my initial $5000 to $6817, a cumulative return of 36 per cent. Of the $1817 increase, 1/3 was from dividends while the remainders was from capital gains. The portfolio continued to benefit from higher concentration of US and Canadian equities, which again hit it out of the park the past year.

Below is the breakdown of the portfolio. Five years ago when I set up the account I answered a series of questions about my financial literacy and risk tolerance. ROBO took my responses and crafted a portfolio that it felt was compatible with my profile. Continue Reading…