For young couples starting families, buying their first home and/or other real estate. Covers mortgages, credit cards, interest rates, children’s education savings plans, joint accounts for couples and the like.

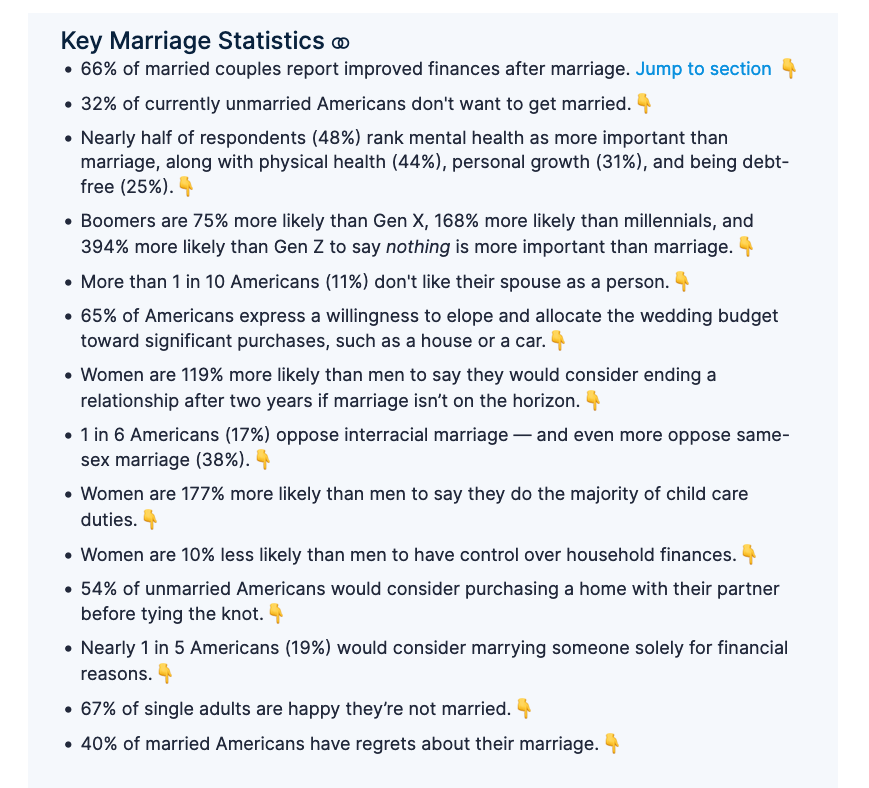

65% of Americans say their partner having too much debt is a dealbreaker in deciding to get married. Little wonder that the national marriage rate in the United States has declined 60% over the last 50 years.

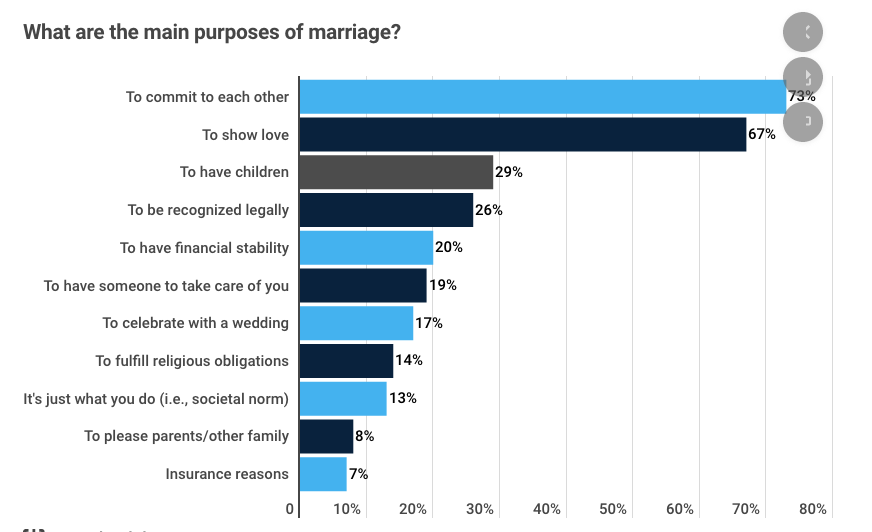

Source: Clever Real Estate — Marriage Survey, May 2023

According to the Marriage Survey of 1,000 American adults conducted by Clever Real Estate in May (see graph above), financial stability is a primary purpose for marriage, as reported by 1 in 5 Americans (20%). In fact, 19% admit they would marry solely for money reasons (19%). Entering into the calculation are factors like high inflation, escalating living costs, and an expensive real estate market.

While marriage positively impacts finances for 66% of couples, only 54% of married couples discuss finances regularly, and 7% never broach the topic. 53% favor separate bank accounts. However, married women are 10% less likely to manage finances in their marriage than men. Money-related issues contribute to about 1 in 6 divorces (16%). Looking back at their lives, 10% of married respondents wish they chose a partner more financially responsible.

As a mother, I know the importance of raising my daughter to be independent and confident. One of the most significant ways I can do this is by instilling in her the value of financial literacy. By teaching her to be financially independent, I am setting her up for a future where she can make sound decisions with money and have the freedom to achieve her dreams. I feel every mother should share this responsibility and nurture the financial skills of their children, especially when we consider the uncertainties of the current global economic climate.

Growing up and learning to manage money through lived experiences, I discovered that some of those life lessons can be painful. My immigrant parents were so focused on working hard to provide the basics for the family, financial literacy lessons weren’t really a priority for my sister and me. All we were taught was to save and keep on saving. In fact, my sister and I would sometimes skip lunch at school just to save the allowance our parents gave us. I learned the hard way that while saving is part of being financially literate, it can’t just stop there; a significant next step is to find safe, reliable methods to growing your wealth.

Not knowing better, when I was 18, one of the earliest financial mistakes I made was getting multiple credit cards, which eventually resulted in a lot of debt (because which teenage girl doesn’t like shopping?). I had to work hard to pay it off and it was a tough lesson to learn, but it was valuable because it made me realize the importance of being smart about money from a young age.

After that, I started seeking support to become more financially literate from any source I could get my hands on. The internet was my best friend and I got into the habit of listening to podcasts about investing and best financial practices. When I started working, I was lucky enough to find a trusted mentor who taught me that putting 75 per cent of my paycheque toward smart investments was smarter than spending the money on any big-ticket item immediately.

As I became better with money, I went from only knowing how to save money to growing my wealth through investing in stocks (ETFs) and real estate and having a diverse portfolio. When it comes to investments, I now know it’s important to maintain both passive and aggressive investments. Having said that, choosing between good investments and bad ones can be daunting and that’s where financial advisors come in. Engaging a trusted advisor who is experienced in investing in different asset classes can make all the difference in the world because they often have access to wealth management tools and data that make investment proposals more reliable and easier to understand.

Teaching children about saving and investing — and the mindset behind both

Although I eventually found my financial footing, others are not so lucky and many have never been able to recover once they get into debt, which can be crippling. Now that I have a family of my own, one of my top priorities is to make sure my daughter has a strong foundation in financial literacy, with all the tools she needs to make better decisions when managing money.

One of the things that we’ve started working on together is to get her to save regularly, like I did as a child. But more than teaching my daughter good saving habits, I believe what’s important is to show her the difference between the money-going-out and money-going-in concept. Very often, children are no strangers to the former because they see us making purchases daily and this makes it easy for them to learn spending (or worse, impulse spending). The latter, however, is more difficult to emulate because they rarely witness the act of saving. This is especially true now that we live in a world where most financial transactions are digital. Though this speaks to the convenience of innovation, how do we curb impulse spending in our children beyond merely saying “no” (and parents, I’m sure you’ll agree that saying “no” doesn’t always elicit the best response from children)? Continue Reading…

May marks the arrival of Mother’s Day, a time to recognize the influence and sacrifice that comes in tandem with motherhood. While the old adage of “parenting isn’t easy” rings true, the financial planning component doesn’t have to be hard. Childhood is a series of stages woven together: each brings a new opportunity for parents to maximize key fiscal benefits and underpin good financial habits for the next generation.

Pre-Baby

Before your baby is born, there are pre-emptive financial strategies that you can implement to get your affairs in order. Firstly, you want to arm yourself with knowledge. Get informed about the benefits provided by the government and your employer to determine what your expected income will be while on parental leave. Take time to research childcare costs and calculate whether you have adequate life and critical insurance.

Most importantly, make sure you have a will in place that designates a guardian to care for your minor child, a trustee to manage the money for your child and an executor who will run the administration of your estate. Finally, review your financial plan with your advisor to account for the addition of a new family member.

Infants and Toddlers (0-5 years)

There are a series of government benefits available for parents with young children. In most provinces, you can automatically apply for a Social Insurance Number and the Canada Child Benefit (CCB) when you register your child’s birth. The CCB is a tax-free monthly payment made to eligible families to help with the cost of raising children under 18 years of age.

You should also consider opening a Registered Education Savings Plan (RESP) to help save for your child’s education. To this same point, you may be eligible for a Canada Education Savings Grant, which provides a 20 per cent grant to be paid on yearly contributions up to an annual limit of $500 and a lifetime limit of $7,200. Your family may qualify to receive the Canada Learning Bond based on your family income and other benefits under a provincial education savings program. You may also be able to claim childcare expenses if you (or your spouse or partner) paid someone to look after an eligible child so that one or both of you could work or attend school. Talk to your financial advisor about the options available to you.

Middle Childhood (6-11 years)

While they may not have a wealth of knowledge yet, children at this age can understand basic money concepts and can start developing good habits. Consider opening a savings account for your child and encourage them to make deposits from allowance, holiday or birthday present money.

Teenagers and Adolescents (12-19 years)

At this stage, the Mirror-Window Effect is at its peak. Mirrors offer reflections, while windows open up new views. By practicing wise money management, you can be the mirror your child needs to develop early but strong financial habits. Continue Reading…

By Michael Kovacs, President & CEO of Harvest ETFs

(Sponsor Blog)

The Harvest Diversified Monthly Income ETF (HDIF:TSX) was built to meet Canadian investors’ need for income and sector diversity. We built it with a straightforward thesis, by holding an equal weight portfolio of established Harvest Equity Income ETFs, we could deliver growth potential and high monthly income. That made it one of the most popular Canadian ETFs launched in 2022.

Each of the ETFs held in HDIF captures a portfolio of leading large-cap businesses. They also each employ an active and flexible covered call option strategy to generate high income yields, offset downside, and monetize volatility. HDIF combined those ETFs with modest leverage at approximately 25% to deliver an enhanced income yield.

In April of this year, we launched the Harvest Diversified Equity Income ETF (HRIF:TSX). It holds the same equal-weight portfolio of Harvest ETFs, but without the use of leverage. Put simply, leverage adds a level of risk that some investors are not comfortable with. Therefore HRIF can deliver that same diversified portfolio of underlying ETFs and a high income yield in a package that more risk-averse investors may want to consider.

A truly diversified portfolio

At Harvest ETFs, we always start with portfolios of what we see as high-quality businesses. The ETFs held in HRIF capture companies that lead their sectors. By combining those portfolios into a single ETF, HRIF delivers a very diverse exposure to these companies.

The equal-weight portfolio held by HRIF at launch holds the following six ETFs.

Each ETF holds a portfolio of leading companies in their particular sector and market area. We define that leadership through quantitative and qualitative metrics such as market cap, market share, performance history and — in the case of certain underlying ETFs — dividend payment history. The companies selected in each ETF’s portfolio demonstrate leadership across those metrics.

HRIF also delivers a diverse set of performance drivers. Tech has been a market growth leader for over a decade and remains a key allocation for investors. Healthcare shows significant defensive qualities, especially during inflationary and recessionary times. The brand leaders in HBF and Canadian leaders in HLIF are selected in large part due to their resilience across market cycles, market shares, and dividend payment history. US banks have faced headwinds lately but have long-term positive exposure to interest rate increases and remain structurally important to the global economy. Utilities are an almost textbook definition of defensiveness, providing stability and ballast for the ETF.

Taken together, HRIF delivers leadership from a wide set of companies which, combined with its high income yield, makes it an attractive ETF for many investors.

HRIF’s High Income Yield Explained

HRIF launched with an initial target yield of 8.0% annually, paid as monthly cash distributions. That yield is earned by combining the underlying yields of its component ETFs, each of which employ an active & flexible covered call option strategy.

Covered call option ETFs effectively trade some upside potential for earned income premiums by ‘writing’ calls on a percentage of the ETF’s holdings. Where many covered call option ETFs use a passive strategy, writing calls on the same percentage of holdings each month, the Harvest ETFs held in HRIF use an active strategy. Continue Reading…

For people with bad credit, the experience of buying a home can be quite difficult and daunting. It’s a tricky time that necessitates careful planning and preparation.

However, despite the difficulties that low credit scores may present, there are several tips and strategies you can employ to help you navigate the home-buying process. This article highlights some of these innovative strategies.

How to Buy a Home with Less than Stellar Credit

Here are some pointers to help you buy a home even if you have bad credit:

Consider Special Programs

There are numerous loan programs that do not require a high credit score or a down payment if you are a first-time homebuyer or have a low income. Some options [in the United States] to consider include USDA loans, VA loans, and the Fannie Mae HomeReady and Freddie Mac HomeOne and Home Possible loan programs.

Look for the Best Deal

Different mortgage brokers offer various rates of interest, so shop around to find the best deal. According to studies, trying to compare multiple rate quotes could save you a substantial amount of money in the long run.

Look into Down Payment Assistance

If you’re concerned about saving for a down payment, there are more than 2,500 down payment support programs available across the country for which you could be eligible. However, you need to avoid major financial changes. Taking on new debt or making a large purchase can lower your credit score, so avoid doing so while applying for a mortgage.

Things you should know about the Homebuying Process

Before you start looking for a house, you should educate yourself on the ins and outs of house purchases. Here’s a rundown of some key points to keep in mind:

Recognize why you want to Buy a House

Buying a house is a significant investment that shouldn’t be taken lightly. If you don’t know why you would like to buy a house, you may come to regret your decision later on.

Check your Credit Score

Your credit score will help you in evaluating your payment plans; lenders use it to set loan pricing and determine if you can repay your mortgage. The more favorable your credit history, the better your chances of obtaining financing at the best terms and rates. Continue Reading…