By Dale Roberts, CutTheCrap Investing, Retirement Club

Special to Financial Independence Hub

Schwab’s SCHD is a popular U.S. dividend ETF that has been disappointing investors for a long time. Does that disappointment mean that the fund is going to shine when (if) the AI bubble bursts? And speaking of shining, we’ll take a look at gold. Can it go even higher? Plus, Canada’s most defensive sector ETF has a surprising history of outperformance.

What to expect from the U.S. stock market over the next 10 years? Not much.

Once again, having lived through it, and invested through it I remember:

He pointed to a JPMorgan chart from late last year that looked at what an investor’s annual return on average over the next 10 years would be if they had bought S&P 500 at a given price/earnings ratio. The P/E was 23 at the time, meaning that average return would be 2% to minus 2%, he said.

Of course there are other lost decades, such as the Depression era and the stagflation era of the late 60s into the early 8’s. But don’t worry: it was all ‘easily handled by a balanced portfolio with some inflation protection. We call that an all-weather portfolio of course.

Even a 5% allocation to gold during the stagflation era would have allowed you to breeze through the period. Add in oil and gas stocks and yer laughing.

That portfolio idea (not advice) uses defensive sectors in concert with dedicated inflation fighters.

Is SCHD well-positioned for a dot.com-like correction?

I’ve penned extensively on the concept that retirees might pay attention to valuation issues and hedge that risk with a U.S. value-oriented holding. We’d continue to hold some U.S. market or U.S. growth, but layer in a value holding. The Schwab Dividend ETF SCHD is a popular choice. What’s up with SCHD? Or what’s down might be the appropriate question.

I created a meaningful position in iShares Quality Dividend ETF XDU-T (Canadian Dollars) as a valuation slant. It outperformed SCHD in 2024 and that continues in 2025. In price terms SCHD was down 1.7% in 2025 while XDU-T was up 4.4% (at time of writing late in October 2025). We might attribute about 2% of that gain to the Canadian currency weakness vs the U.S. Dollar.

The S&P 500 was up 13.66% in 2025. The Nasdaq 100, QQQ was up 18.36%. Money continues to flow to growth-oriented stocks in the U.S.

This article on Seeking Alpha (sign up or sub required) suggests that SCHD might be well-positioned if we do get a major correction and rotation to value and quality.

The top 3 sectors for SCHD were leading sectors when the dot com bubble burst …

That chart tracks Energy, Consumer Staples and Healthcare vs Tech.

Who knows, but SCHD’s stubborn decline might be creating even greater value. Here’s an interesting table on sectors and valuation.

worldperatio.com

In the search for value you might also consider small cap, or mid cap or a classic value index ETF such as iShares VLUE. As I wrote for Findependence Hub, these might be challenging times for recent retirees who do not pay attention to valuation. You’ll find more bubble-bursting ideas in that post 😉

Accumulators with decades to go might ignore the valuation “issue.”

I’m happy with XDU and some of my other U.S. value-oriented stocks. In my U.S. RRSP account, my individual U.S. stock portfolio was up 20.7% in 2025 (again, as of time of writing). The core stocks are still driving the bus.

For years, I have been telling friends: “Just buy the market, don’t waste your time with individual stocks.”

The problem is that most of them don’t know what I am talking about, and to be honest, sometimes I don’t know what I am talking about either. Because not all “markets” are created equal. They don’t behave the same way, and they aren’t all appropriate for every investor.

Today, I will talk about the three primary markets people discuss, how each one behaves, and how a regular Canadian can choose between them. Those three markets are:

QQQ, the

S&P 500, and the

TSX index.

Once you understand the differences, you will be able to judge which is a better fit for your portfolio and where they should be placed.

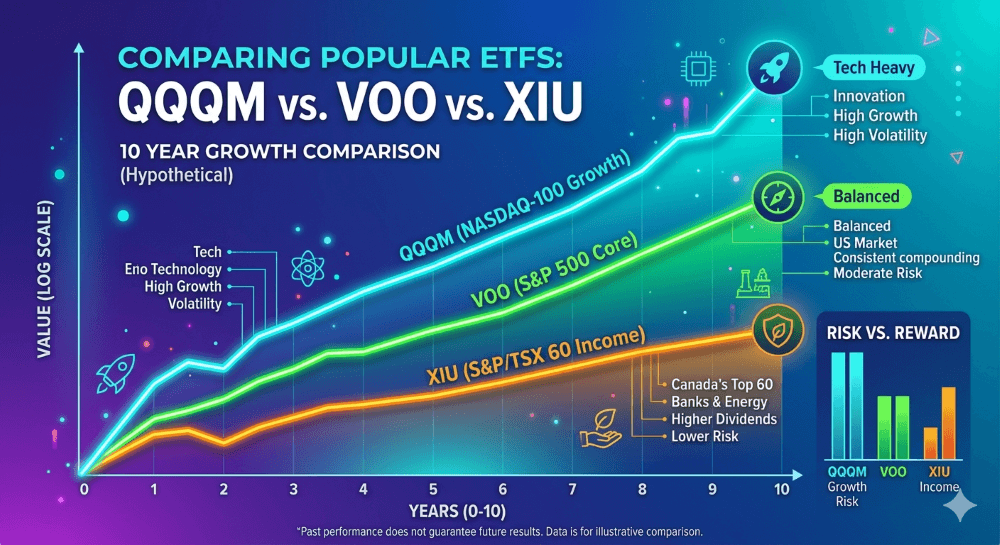

Higher Returns always come with Higher Risk

If we stack our three indexes on a risk-return basis, this is what we get:

QQQ has the highest returns and the highest risk.

The S&P 500 is less risky and has lower returns than QQQ.

The TSX has lower returns than the S&P 500 but offers different sector exposure.

My preferred ETFs to buy these indexes are:

For QQQ: I like an ETF called QQQM.

For the S&P 500: I like VOO.

For the Canadian TSX: I like XIU.

For your information, there are different ETF which cover the same indexes. I like the above mentioned because they have low management fees, they are highly liquid, and they have a good reputation.

To give you an idea of the difference in total returns for these three investments over the past 10 years (approximate):

This is why the returns are high; most of these companies’ business models are scalable globally. But be careful: in a single year, the QQQ was down 32.58%. You need a strong stomach to tolerate a drop of that magnitude.

VOO: The S&P 500 Standard

The S&P 500 is composed of the 500 largest corporations in the U.S. The risk is lower than QQQM because it is diversified across many industrial sectors.

Annualized return: About 14%.

Highest annual return: About 31%.

Lowest annual return: About -18%.

XIU: The TSX for Canadian Patriots

XIU is composed of the 60 biggest Canadian companies.

Dominated by banks, oil, and mining.

Higher dividend yield than the U.S. indexes.

Lower long-term growth potential.

Risk vs. Reward Table

Index

Returns

Risk

Role

QQQ

Highest

Highest

Aggressive Growth

S&P 500

Strong

Moderate

Core Portfolio

TSX

Lower

Cyclical

Income & Diversification

Summary: QQQ makes you rich faster (and scares you more); the S&P 500 makes you rich steadily; the TSX pays you while you wait.

How should a Canadian Investor use this Information?

Everything in this account grows tax-free. This is the place for your highest-return investments. If you make a 100% return, it is 100% tax-free.

Best for: QQQM or high-growth individual stocks. You keep all capital gains; $0 goes to the government.

2. RRSP (Registered Retirement Savings Plan)

Capital gains and dividend income are tax-deferred until you withdraw the money. Furthermore, there is no U.S. withholding tax on dividends in an RRSP. Normally, the IRS imposes a 15% tax on dividends paid to non-residents, but the Canada-U.S. tax treaty waives this for the RRSP.

Best for: VOO (S&P 500) or any U.S. dividend-paying stocks.

3. Non-Registered Account (Taxable)

Once you hit your TFSA and RRSP contribution limits, you use a regular investment account. In Canada, domestic dividends receive favorable tax treatment through the Dividend Tax Credit.

Best for: XIU (TSX Index) or Canadian bank stocks that pay regular quarterly dividends

RRSP → S&P 500 / U.S. equities (Avoid U.S. withholding tax).

Non-registered → Canadian dividend stocks (Utilize Dividend Tax Credit).

Final Thought: Stop looking for the “Best” Index

There is no single “best” index. There is only the one that matches your risk tolerance, time horizon, and emotional discipline. QQQ will outperform until it doesn’t. The TSX will lag until commodities surge. The S&P 500 will quietly compound in the background. The real edge isn’t picking the winner—it’s understanding why each one wins at different times and positioning yourself accordingly.

Frequently Asked Questions (FAQ)

Which is better for Canadians: VOO or XIU? It depends on your goal. VOO (S&P 500) offers higher historical growth and U.S. tech exposure, while XIU (TSX 60) offers higher dividends and stability through Canadian banks and energy.

Why should I hold U.S. stocks in my RRSP instead of my TFSA? While both are great, the RRSP is uniquely exempt from the 15% U.S. withholding tax on dividends. If you hold a U.S. dividend-payer in a TFSA, the IRS takes 15% before you see it.

Is QQQM the same as QQQ? Essentially, yes. They track the same index (Nasdaq-100), but QQQM has a lower management fee, making it better for long-term “buy and hold” investors.

What is the “Dividend Tax Credit” for Canadians? It is a tax incentive that reduces the amount of tax you pay on dividends received from taxable Canadian corporations, making the TSX very attractive for non-registered accounts.

Alain Guillot is a part time event photographer, part time Salsa teacher, and part time personal finance blogger. He came to Quebec as an immigrant from Colombia. Due to his mediocre French he was never able to find a suitable job, so he opened a Salsa/Tango dance school and started his entrepreneurship journey. Entrepreneurship got him started into personal finance and eventually into blogging. Now he lives a Lean FIRE lifestyle and shares his thoughts in his blog AlainGuillot.com. This blog appeared first on his blog and is republished here with permission.

My latest MoneySense Retired Money column expands on a blog written by Devin Partida on my site while we were away in Malta and Italy. In there you can see three photos from our trip, including the one shown here.

For MoneySense, I reached out through Linked In and Featured.com to bounce this idea off various Retirement Experts and Business Owners in North America.

The full Retired Money column can be accessed by clicking this hyperlink: Financial Independence and Travel: Can you have both? The column runs a normal 1200 words or so but the actual responses ran about five times that long, which you can find by clicking on this link also on Findependence Hub. (It ran over the weekend, as did the MoneySense summary of it).

Naturally, I agree with Devin’s original topline conclusion: that “maintaining Financial Independence while traveling is entirely possible with a proper strategy.” As some of the sources indicate, technology and the Internet means most professionals or so-called “Knowledge Workers” can really practice their craft most anywhere in the world that has Web access.

Digital Nomads

The colourful term “Digital Nomad” is often used to describe such globe-trotting workers. Of course, travelling the world by Baby Boomers like myself is relatively straightforward if you spent decades building up pensions and a Retirement nest egg. Ideally at the end of 30 or 40 years of “working for the man (or woman)”, you end up with the lovely combination of relatively endless time and sufficient financial resources to indulge your globe-trotting desires.

Leisure

But the MoneySense column also passes on several tips that can be used by those who are only semi-retired, or even decades from Retirement but who have embraced the so-called FIRE movement: Financial Independence Retire Early. There’s even a term I hadn’t encountered until I researched this piece: Bleisure, which is of course a contraction of the words Business and Pleasure. Continue Reading…

That blog inspired me to reach out to multiple financial experts and business owners, with the assistance of Linked In and Featured.com, which has been supplying this site with quality content for several years.

Here’s how we posed the question:

Can you pursue Financial Independence (or Retirement or Semi-Retirement) without giving up Travel? See this blog for one opinion on this topic:

Malta: where we spent most of February this year. Photo by J. Chevreau

This particular topic attracted 84 comments by the April 20th deadline: this blog presents 25 or so that I selected. It’s long so I’ve summarized the main points with subheadings.

Note also that my latest MoneySense Retired Money column summarizes some of the main points, more succinctly as there is limited space for that column (about 1300 words, compared to the nearly 6,000 words that appear in the particular blog you are now reading).

To ease the reading burden, I’ve added subheads, some of which include:

Geoarbitrage: Live where cost of Living is lower

Renting RVs for Extended Travel Stretches

Make Travel a regular fixed expense you plan on incurring every month

Treat Travel as a budget category, not a luxury to eliminate

Embrace slow travel, house-sitting, points travel hacking and off-season destinations

Buy property in tourist spots to fund Travel

Majority of Professionals can now work remotely

The “goal isn’t to eliminate travel, but rather to make it more intentional.”

“Bleisure”: Let your career fund your transit

As President of Safe Harbors Travel Group, I’ve spent decades helping organizations use strategic logistics and “Bleisure” to explore the world without draining the bottom line. You can reach Financial Independence by letting your career fund your transit; we often help clients integrate vacation days into business trips to eliminate personal airfare and lodging costs.

A key strategy for the budget-conscious traveler is utilizing “humanitarian airfares,” a specialized airline product Safe Harbors provides that offers significant savings for anyone doing charitable, religious, or mission-based work. These fares are a powerful hack for those pursuing a purpose-driven life while keeping their personal travel expenses at a minimum.

By leveraging our elite tech partnerships for data-driven booking, you can ensure “duty of care” and response speed that prevents the costly emergencies often associated with unmanaged travel. This structured approach allows you to focus on wealth building while Safe Harbors handles the complexities of your global footprint. — Jay Ellenby, President, Safe Harbors

Build Travel into the system, not just a later Reward

Yes: you can chase FI or semi-retirement and keep travelling if you build travel into the system instead of treating it like a reward you “earn later.” I’ve run logistics/transportation businesses for years and now my wife and I host 15 furnished units in Detroit/Chicago, so I’m used to designing operations that still run when I’m not physically there.

What made it work for us is shifting travel from “big expensive trips” to “repeatable, planned mobility.” We use our Detroit-focused blog as a planning engine: when we travel, we test neighborhoods, transit (Q-Line/SMART/MoGo), and local routines the same way a guest would: then we bake that learning back into listings and guest guides so travel time also improves the business.

The practical FI move is making your income less dependent on your daily presence. Guest reviews told us people wanted clearer walkthroughs, so we added walkthrough videos to each property page and saw a 15% increase in booking conversions: less back-and-forth, fewer preventable questions, more freedom to be away while keeping standards consistent.

If you want one tactic you can copy: record a 5-8 minute “first night in the unit” walkthrough (lockbox – thermostat – Wi-Fi – parking – trash) and reuse it forever. That single asset cuts support load while you’re on the road, and it’s the difference between “I can travel” and “travel breaks my cashflow.” — Sean Swain, Company Owner, Detroit Furnished Rentals LLC

Geoarbitrage: Live where cost of Living is lower

Geoarbitrage allows you to live in an area with a lower cost of living for your family while allowing your investment portfolio to grow. The combination of using travel rewards on credit cards and traveling during less expensive times reduces your travel costs. This approach to finding money saving ways to see the world makes international exploration a viable way to maintain your lifestyle versus making it a luxury. — Zack Moorin, Founder, Zack Buys Houses

Geoarbitrage and the Second Act Advantage

In The Second Act Advantage, I show how geoarbitrage lets anyone achieve financial independence without sacrificing travel: in fact, it makes travel the strategy. By earning in strong currencies while living and exploring more affordable parts of the world, everyone can enjoy a richer, more adventurous life while actually spending less. The book teaches readers how to design a life where freedom, fulfillment, and financial efficiency all work together. — Jay Samit, Bestselling Author, The Second Act Advantage

Transitioning from Vacationing to Geo-arbitrage

The Travel-First Strategy: Designing FI Without Sacrifice

A common misconception in the FIRE (Financial Independence, Retire Early) community is that travel is a luxury to be deferred until the finish line. However, in my experience advising lifestyle-focused entrepreneurs, pursuing financial independence without giving up travel isn’t just possible it’s often a more sustainable strategy for preventing burnout.

Shifting from Consumer to Global Resident

The key is transitioning from vacationing to Geo-arbitrage. Traditional travel involves paying retail prices for short-term stays, which can cripple a savings rate. A strategic traveler focusing on FI prioritizes medium-term stays in regions where the cost of living is lower than their home base. By spending months in hubs like Portugal, Mexico, or Southeast Asia, you can often live a high-quality lifestyle for 40% less than in major Western cities. In this model, travel actually accelerates your path to financial independence by lowering your monthly burn rate.

Leveraging Credit Strategy as an Asset Class

From a PR and financial positioning standpoint, we should treat travel rewards not as points, but as a shadow asset class. A sophisticated FI seeker uses strategic credit card optimization to ensure that their transportation and lodging line items remain near zero. When flights and hotels are covered by systemic spending, travel stops being a drain on investment capital and becomes a tool for lifestyle maintenance.

The Semi-Retirement Pivot

The all-or-nothing approach to retirement is becoming obsolete. We are seeing a rise in Coast FIRE, where individuals reach a baseline of savings and then transition into remote-first or consulting roles. This allows for perpetual travel while the core nest egg continues to compound undisturbed. By integrating travel into the pursuit of FI rather than viewing it as a reward for the end of it, you create a life you don’t feel the need to escape from. This ensures that when you finally reach full independence, you already possess the global literacy to enjoy it. — James Tech, SEO Marketer, TripFrog

58% of Millennials and GenZ prioritize Travel over Material Accumulation

Financial Independence and travel are not mutually exclusive; in fact, they increasingly reinforce each other when approached strategically. A growing body of research highlights the rise of “geo-arbitrage,” where professionals leverage remote work or location flexibility to reduce living costs while continuing to explore new destinations.

According to a 2024 report by Deloitte, nearly 58% of Gen Z and millennials prioritize experiences like travel over material accumulation, reshaping traditional financial planning models. At the same time, the World Tourism Organization notes a steady increase in long-stay and work-from-anywhere travel patterns, indicating that travel is no longer viewed as a luxury pause but as an integrated lifestyle choice.

From a workforce perspective, continuous upskilling and digital proficiency — particularly in areas like project management, agile practices, and cybersecurity — enable professionals to maintain income streams while remaining location-independent.

Financial independence, therefore, is less about restriction and more about intentional design: aligning income strategies, skill development, and lifestyle priorities in a way that sustains both economic security and personal fulfillment. — Arvind Rongala, CEO, Invensis Learning

Renting RVs for Extended Travel Stretches

Absolutely yes: and I’ll tell you why from an angle most people overlook: your cost of living on the road can actually shrink dramatically while you’re building toward FI.

I run DFW RV Rentals, placing travel trailers for displaced families and insurance claims. What I see constantly is people discovering — often during the worst moments of their lives — that a well-equipped travel trailer is genuinely livable, comfortable, and cheap compared to a mortgage or apartment lease.

Here’s the FI angle nobody talks about: renting an RV for an extended travel stretch eliminates storage fees, maintenance headaches, depreciation, and insurance costs that crush RV owners. I’ve watched people romanticize ownership, buy a unit, and watch it become a financial anchor: whereas someone renting strategically keeps capital free and mobile.

If you’re pursuing FI and want travel woven in, think of RV rental as a variable living expense you control, not a lifestyle luxury. A few months on the road in a rented trailer can cost less than your fixed housing back home: and that gap is real money compounding toward independence. — Jonathan Dies, Owner, DFW RV Rentals

Maintenance-free Retirement communities

As Executive Director of The Village at Mint Spring and Stuarts Draft Retirement Community for over 16 years, I’ve guided hundreds toward maintenance-free retirement living that supports financial goals without homeownership burdens.

Yes, financial independence or semi-retirement pairs perfectly with travel when you eliminate upkeep costs like repairs, lawn care, snow removal, and property taxes: freeing budget and time for trips.

Our residents use the shuttle for local outings while traveling afar, knowing onsite care partners like Visiting Angels handle needs back home.

Fall incentives like up to $3,500 moving allowance make the shift easier, letting you lock in FI sooner and explore without stress. — David Brenneman, Owner, The Village at Mint Spring

Adopt a “Cash Rules Everything” mindset

As an advisor to business owners earning $400K+, I’ve found that financial independence is about aligning your strategy with your personal values rather than following generic industry models. I build plans for my clients that prioritize clarity and lifestyle flexibility, ensuring travel is a core component of the strategy rather than a sacrifice.

When the April 2025 market volatility caused equities to waver due to new tariffs, clients with high-liquidity strategies avoided the “dash for cash” and kept their travel plans intact. I focus on a “cash rules everything” mindset during periods of uncertainty to ensure market jitters don’t interrupt your personal milestones or global adventures.

I use the Altruist platform to give my clients a technology-driven, transparent view of their wealth from any location. This allows entrepreneurs to monitor their progress toward retirement and make confident decisions via mobile tools without being tethered to an office.

True financial guidance starts with understanding your long-term vision so your portfolio serves your life, not the other way around. By creating a practical action plan focused on stability and growth, you can pursue financial freedom while maintaining the lifestyle you have already worked to build. — Daniel Delaney, Owner, Seek & Find Financial

Make Travel a regular fixed expense you plan on incurring every month

Many people misunderstand the idea of being financially independent as a way to have nothing but austerity during their time of independence; however, the reality is that it’s just about allocating your money in a conscious manner. Too often, people will make travel an ‘additional’ expense that must be eliminated in order to achieve their savings goals: this can lead to burn out and a living arrangement that does not continue.

The problem is that travel is often treated as an item that has been paid for with ‘loose change’ after all of the other ‘necessary’ expenses have been paid each month; therefore when budgeting, travel should be included as a regular fixed expense you plan on incurring every month.

To have travel as part of your work-life balance, you will need to establish your savings plan with this in mind. Business places do this as well; you do not build a business just by lowering your cost structure, you have to build a company based on what gives you the highest return on your investment for the long-term. The same should be true for any travel related goal that you desire to achieve. One of the pitfalls that many individuals fall into when comparing their way of saving to the ways that people in the ‘lifestyle’ mode of saving demonstrate is that they fail to establish their own pace and their definition of ‘enough.’

Finding that work-life balance about not simply doing the math correctly, but making certain to build a lifestyle in which you would prefer to ‘Get up and do it!’ every single day. — Abhishek Pareek, Founder & Director, Coders.dev Continue Reading…

Second Quarter 2026 BMO Macro Regime Model – Strategy Report

By Bipan Rai, BMO ETF & Structured Solutions

(Sponsor Blog)

Upon reflecting on the current state of markets, we’re reminded of the lessons from Barbara Tuchman’s The Guns of August, which illustrates how hubris and rigid systems can override rational decision-making.

While we are not drawing direct parallels to the current situation in the Middle East, the book offers important lessons for investors as they navigate portfolio construction in the months ahead.

As an example, periods of higher inflation generally increase the co-movement between U.S. stocks and interest rates, requiring a more pragmatic approach to diversification. This often leads to greater interest in real assets like gold, as we’ve seen in recent years.

But what happens when even gold fails to provide adequate diversification during a geopolitical shock? Tuchman’s work reminds us of the importance of stress-testing assumptions before a crisis unfolds. When correlation structures break down and traditional hedges falter, investors who have considered tail risks in advance are better positioned.

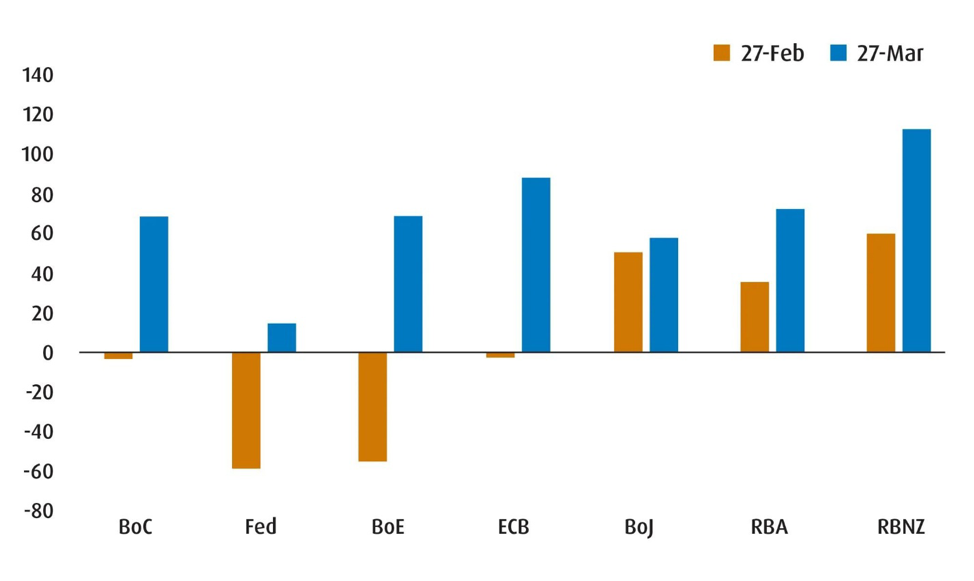

With that in mind, let’s consider the present environment. Even if the Middle East conflict is resolved quickly, the economic and market consequences will likely persist. Inflation risks are no longer symmetrically distributed, and price pressures appear likely to rise. Damage to energy-related infrastructure points to a prolonged period of crude oil and LNG supply disruption, pushing prices higher for longer. This affects refined products (such as gasoline, jet fuel, and kerosene), fertilizer production, and the supply of helium: complicating central bank messaging. Markets have responded by pricing out expected Federal Reserve rate cuts and pricing in aggressive hikes for other developed-market central banks (Chart 1).

Chart 1 – Markets Have Priced in Tighter Central Bank Policy by End-2026

Source: BMO Global Asset Management, as of March 27, 2026.

At the same time, growth risks are shifting in the opposite direction. Higher input costs act as a tax on consumers and weigh on corporate margins. The speed at which rising energy prices feed into slower growth depends largely on a country’s economic slack, which explains why some central banks have recently acknowledged growth risks more explicitly than they did in early 2022.

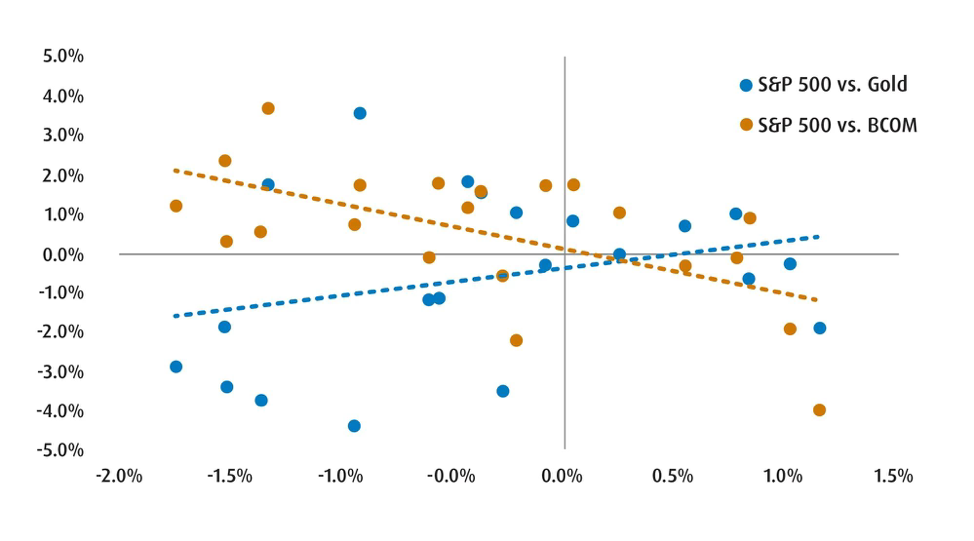

Indeed, our own proprietary macro regime model is signaling that we are transitioning from a ‘reflation’ backdrop to a more stagflation-like regime (Chart 2).1 This emerging stagflation regime need not mirror the 1970s, but we are still positioning our portfolios to be more robust and resilient. We’re broadening our commodity exposure to provide a more direct hedge against supply shocks. In an environment where inflation surprises are more likely to be positive, this type of convexity is valuable.2

We are also allocating to front-end TIPS (Treasury Inflation-Protected Securities) as a hedge against inflation pressures. While breakevens3 have moderated with recent disinflation progress, they do not fully reflect a sustained energy shock. TIPS offer a cleaner way to express inflation risk without requiring a strong view on nominal growth.

Within equities, we are tilting toward quality and low volatility. If growth slows while cost pressures persist, companies with strong balance sheets, durable margins, and stable cash flows should outperform more cyclical or highly leveraged peers. Low-volatility exposures can also help reduce drawdowns during headline-driven market swings.

History teaches us that conflict does not guarantee crisis. But periods of stress often reveal underlying fragilities. Our role as stewards of capital is not to forecast every geopolitical development, but to recognize that the distribution of macro outcomes is tilting toward a stagflation-like environment: and to position portfolios accordingly.

Chart 2 – Broad Commodity Exposure is Now a Better Diversification Strategy than Just Relying on Metals

Source: BMO Global Asset Management, Bloomberg. Daily returns from February 27 to March 27.

Asset Allocation

Relative to the Q1 edition, we’re making some modest changes to our asset allocation splits. The most notable shifts are that we are paring our positions in the equity and alternative sleeves and reallocating them towards fixed income. Of course, these aren’t big changes: as we still remain underweight fixed income and overweight both equities (slightly) and alts.

Our macro regime model suggests that we are in the midst of a transition from reflation to stagflation: characterized by low growth and high inflation. This is still consistent with the late cycle feel of the macroeconomic backdrop.

Despite the challenging backdrop, the underlying fundamentals remain sound enough to maintain a neutral/slightly overweight broad equity position for now. Ahead of the conflict, we did see earnings growth across several sectors in the U.S. and Canada. At the same time, the situation in the Middle East remains fluid, which requires us to be nimbler and more flexible.

In the fixed-income sleeve, the increase in weight reflects our view that the Canadian yield curve4 provides better value and that we feel U.S. TIPS should outperform in the months ahead. For the alts sleeve, the reduction in weight reflects our shift away from gold and towards a broader set of diversifiers in the commodity and infrastructure spaces.

Importantly, we are bullish on the U.S. dollar (USD) for the coming months. This means that our preference is to keep our U.S. exposure unhedged on a tactical basis. The main reasons for this view are the following:

We expect the CAD swaps market to price out rate hikes for the Bank of Canada in 2026.

We expect USD upside as net long positioning remains relatively light.

Equities

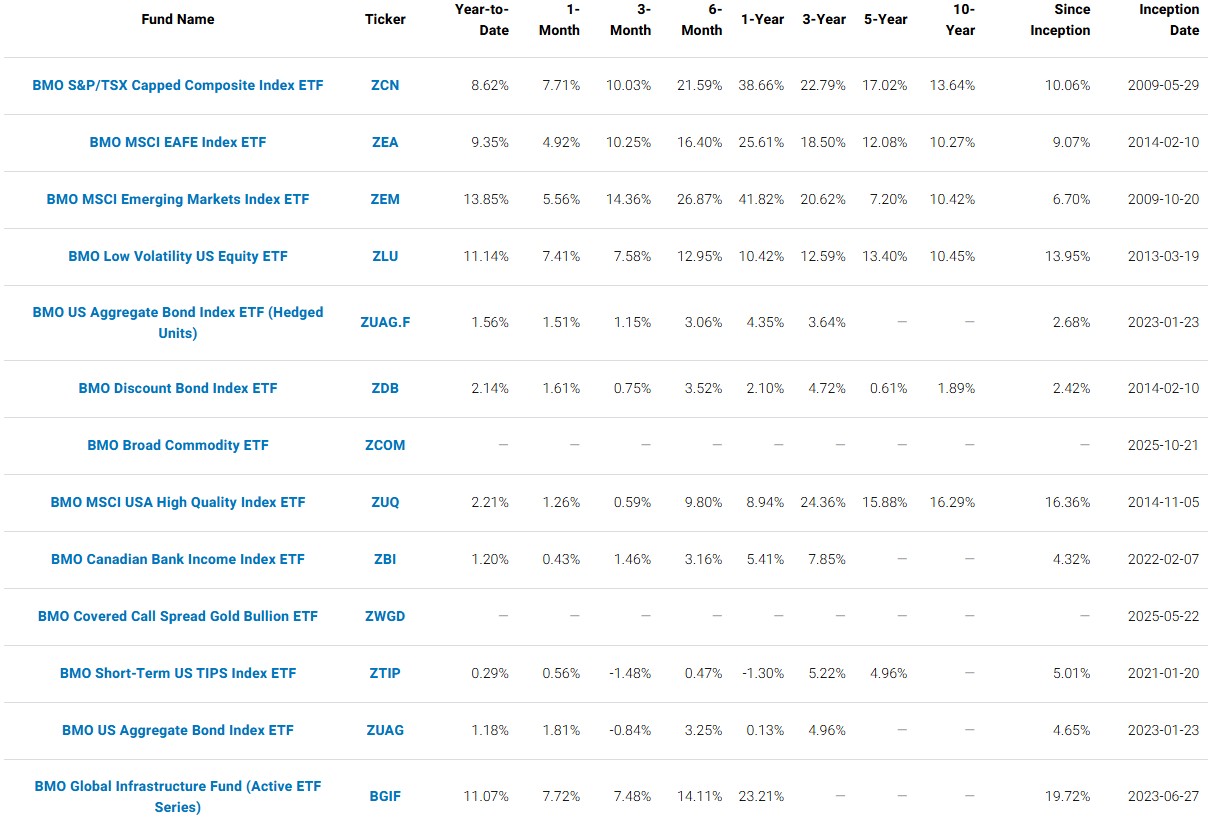

We are increasing our allocation to ZCN (BMO S&P/TSX Capped Composite Index ETF)as Canada remains well positioned as a commodity and energy producer. With energy prices supported by ongoing geopolitical uncertainty, the Canadian equity market should continue to benefit, though outcomes will remain sensitive to the duration of the conflict in the Middle East.

For our U.S. position, we are adding ZLU (BMO Low Volatility US Equity ETF)to complement our existing exposure through ZUQ (BMO MSCI USA High Quality Index ETF). This combination reflects a preference for defensive characteristics and earnings resilience during a period whereby investors remain selective on valuation and fundamentals.

We’ve also added ZTIP (BMO Short‑Term US TIPS Index ETF)as a tactical position as we expect inflation risks to stay firm given energy and broader commodity pressures.

Alts/Hybrids

The most notable change we’ve made in Alts/Hybrids is adding a tactical allocation to ZCOM (BMO Broad Commodity ETF)to broaden our inflation and geopolitical hedge. Energy has led performance on a year‑to‑date basis, but a persistent risk premium can support a wider set of commodities, which improves diversification if equity volatility picks up.

We’ve also upgraded the weight for BGIF (BMO Global Infrastructure Fund ETF)as we continue to constructive on infrastructure, including electric grids, and engineering/construction projects.

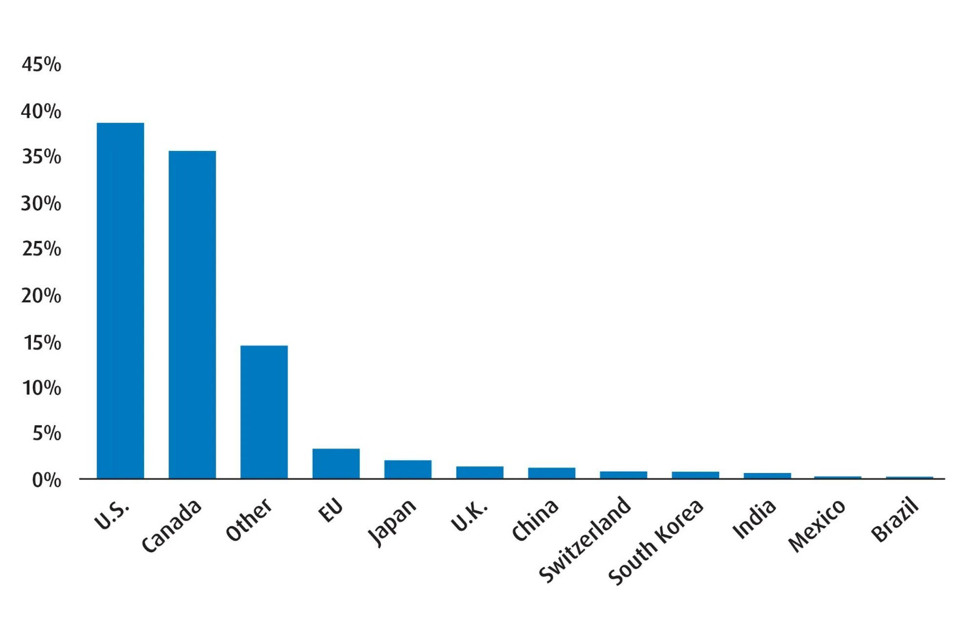

Chart 3 – Q2 2026 Regional Exposure

Source: BMO Global Asset Management, as of March 31, 2026.

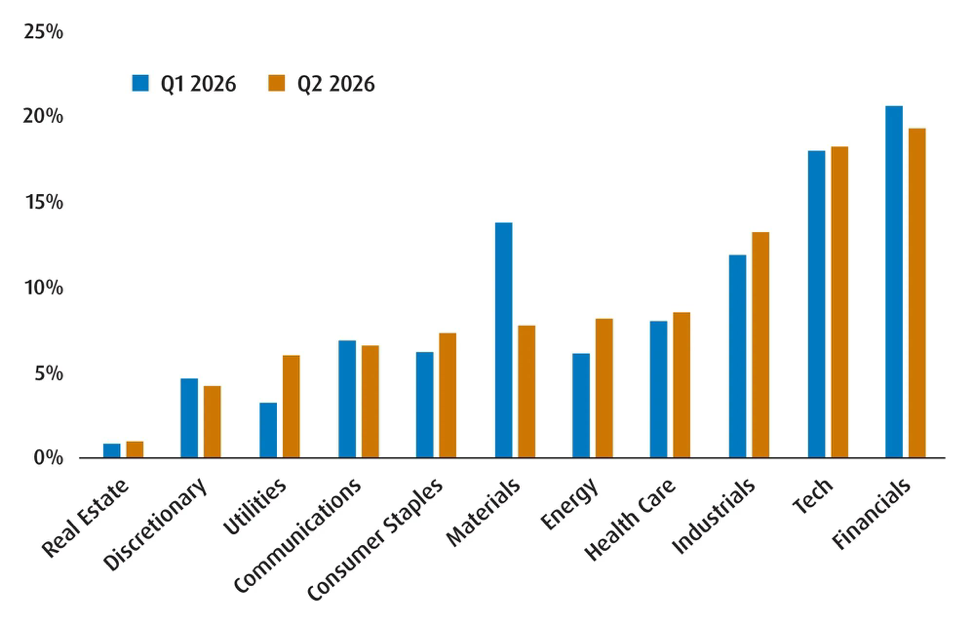

Chart 4 – Global Equity Sector Breakdown

Source: BMO Global Asset Management, as of March 31, 2026.