Retirement should feel like a reward for decades of hard work, not a financial tightrope walk. As the cost of living fluctuates, many Canadians near or in retirement worry about their nest egg stretching far enough.

You can take control of your financial future by making strategic adjustments today. Simple life changes can help you preserve your wealth and enjoy greater peace of mind.

Below, we explore the top ways to lower your monthly expenses in 2026 so you can navigate the year with confidence.

1.) Review your Auto Insurance Policy

Auto insurance premiums often creep up unnoticed and eat away at your monthly budget. A renewal notice might arrive showing a higher rate than the previous term. There are several reasons why your car insurance premium might suddenly go up, such as a change in address, adding a new driver to your policy, or a lapse in coverage. Even a minor speeding ticket can impact your rates for years.

Furthermore, industry-wide inflation raises repair costs, which insurers pass on to policyholders. If you notice a spike in your bill, take some time to address the root cause. You might lower this cost by shopping for new quotes, increasing your deductible, or bundling your home and auto policies.

2.) Track your Daily Spending

You cannot fix what you do not measure. Many individuals know their income figures but lack clarity on exactly where money exits their accounts. To solve this, subtract your savings from your after-tax earnings to determine what you actually spend. This simple calculation often reveals surprising leaks in your budget.

Once you identify where funds go, you can decide which expenses add value and which you can eliminate. Maintaining positive cash is a great financial New Year’s resolution for 2026 that will keep your retirement plan on track regardless of market volatility.

3.) Audit your Digital Subscriptions

Automatic payments quietly drain bank accounts. It’s easy to accumulate streaming services, cloud storage plans, and app subscriptions that you rarely use. Sit down with your credit-card statement, and identify every recurring charge. Cancel any service that you have not used in the last three months. Check whether family plans or annual payment options offer a lower overall rate for the services you choose to keep. Continue Reading…

Here’s a look at some of your best retirement investment management options and choices. These include pensions, RRSPs, RRIFs and more.

TSInetwork.ca

Your retirement investment management plan should build in contingencies for long-term medical needs and supplemental health insurance. As well, you should factor in caring for loved ones who are unable to take care of themselves.

When you work out a plan for your retirement, make sure that you aren’t basing your future income on overly-optimistic calculations that will end up leaving you short. Retirement income can come from many different sources, such as personal savings, Canada Pension Plan, Old Age Security, company pensions, RRSPs, RRIFs, and other types of investment accounts.

Learn how your retirement investment management works in a Canada Pension Plan (CPP)

The Canada Pension Plan, or CPP, is the name for the Canadian national social insurance program. The program pays out based on contributions, and it provides income protection for individuals or their survivors in the instance of retirement, disability or death. Since 1999, the CPP has been legally permitted to invest in the stock market.

Nearly all individuals working in Canada contribute to the CPP, unless they live in Quebec, where the Quebec Pension Plan (QPP) exists and provides comparable benefits.

Applicants can apply to receive full CPP benefits at age 65. The CPP can be received as early as age 60 at a reduced rate. It can also be received as late as age 70, at an increased rate.

Here’s a look at some of the pensions or benefits provided by the Canada Pension Plan:

Retirement pension

Post-retirement pension

Death benefit

Child rearing provision

Credit splitting for divorced or separated couples

Survivor benefits

Pension sharing

Disability benefits

Use a Registered Retirement Savings Plan (RRSP) as a starting place when you look into retirement investment management

RRSPs were introduced by the federal government in 1957 to encourage Canadians to save for retirement. Before RRSPs, only individuals who belonged to employer-sponsored registered pension plans could deduct pension contributions from their taxable income.

RRSPs are a form of tax-deferred savings plan. They are a little like other investment accounts, except for their tax treatment. RRSP contributions are tax deductible, and the investments grow tax-free.

You might think of investment gains in an RRSP as a double profit. Instead of paying up to, say, 50% of your profit to the government in taxes and keeping 50% to work for you, you keep 100% of your profit working for you, until you take it out.

Convert an RRSP to a RRIF to create one of the best investments for retirement

Converting your RRSP to a RRIF is clearly one of the best of three alternatives at age 71. That’s because RRIFs offer more flexibility and tax savings than annuities or a lump-sum withdrawal (which in most cases is a poor retirement investing option, since you’ll be taxed on the entire amount in that year as ordinary income). Continue Reading…

Utilities have long played an important role in investor portfolios, often valued for their stability and diversification benefits. As providers of essential services such as electricity, natural gas, and infrastructure, these businesses tend to exhibit steady demand across economic cycles. In terms of investing, how investors access the utilities sector can matter just as much as the characteristics of the sector itself.

Many traditional utilities ETFs track market-cap-weighted benchmarks designed to own the entire utilities universe. While this approach provides broad exposure, it can also introduce structural inefficiencies. Market-cap weighting can overweight the largest companies, resulting in portfolios where a small number of names dominate overall exposure (i.e. concentration risk). In addition, market-cap weighting continues to increase allocations to companies as their market values grow, reinforcing exposure to recent top performers rather than maintaining a more even distribution across the sector.

The HAMILTON CHAMPIONS™ Utilities Index ETF (UMVP) follows the Solactive Canadian Utility Services High Dividend Index GTR(“Utilities Index”), which was designed to take a more selective approach. Rather than owning the entire utilities universe, the Utilities Index expands beyond traditional utilities to include pipelines and telecommunications companies, focusing on the largest companies across each sub-sector. These sub-sectors share similar business characteristics, including infrastructure-heavy operations and relatively stable demand. By equally weighting its holdings and rebalancing semi-annually, UMVP aims to provide a more balanced and diversified way to access essential services at a low management fee of 0.19%.

Why Invest in Utilities

Investors often allocate to utilities to help diversify their equity portfolios and moderate overall volatility. Demand for essential services tends to be less sensitive to economic cycles, which can make utilities a stabilizing component within a broader portfolio. Over time, these characteristics have made utilities a popular core allocation for investors seeking reliability alongside growth.

UMVP’s Utilities Index builds on this role by broadening the opportunity set beyond traditional utilities. By including pipelines and telecommunications companies, the Utilities Index captures a wider range of essential service providers while maintaining a focus on businesses with similar operating profiles.

This performance reflects a more balanced approach to essential services investing. By expanding beyond traditional utilities and avoiding the overconcentration that can arise in market-cap-weighted indexes, the index UMVP tracks has benefited from exposure to proven companies across a broader opportunity set for low cost (0.19% management fee).

UMVP — Index Outperformance¹

The Limits of Traditional Utility Indices

Most traditional utility indices are built with two structural features that can limit their effectiveness:

First, market-cap weighting can lead to concentration risk, as the largest companies in the sector receive the largest weights. Over time, this can result in a portfolio where a small number of holdings account for a disproportionate share of total exposure.

Second, market-cap-weighted indexes tend to increase allocations to companies as they grow larger, reinforcing exposure to recent top performers. This structure can limit the opportunity to maintain balanced exposure across the sector, particularly when leadership shifts over time.

UMVP’s Utilities Index addresses both shortcomings with three key differences:

Expanding the universe beyond traditional utilities to include telecoms and pipelines

Selecting the largest companies in each sub-sector: utilities (6), telecoms (3), pipelines (3)

Equally weighting the 12 holdings to minimize overconcentration (rebalanced semi-annually)

Where UMVP Fits in a Portfolio

We believe UMVP can serve as a low-cost core utility holding within a diversified equity portfolio. By focusing on the largest companies across essential service providers, UMVP provides exposure to businesses that tend to exhibit more stable demand while participating in long-term equity growth, all at an annual management fee of 0.19%. Continue Reading…

Should I stay, or should I go? If I go, there will be trouble

And if I stay, it will be double

So come on and let me know Should I stay or should I go?

— Should I Stay or Should I Go, by The Clash

Bubble or No Bubble?

During the latter part of 2025, one of the most common topics in both the media and in conversations with clients was whether markets are in a bubble, particularly with respect to AI-related companies. Given the spectacular multi-year ascent of many tech stocks and their sky-high valuations, it is unsurprising that many investors harbour serious concerns regarding a potential comeuppance.

Nobody can know for certain whether such a bubble exists, let alone how and when the proverbial story will end. However, analyzing the current environment from a risk-reward standpoint can provide investors with a useful framework to consider their current portfolio allocations and to determine whether changes are warranted.

Between a Rock & a Hard Place: Loss vs. Opportunity Cost

All bubbles, both perceived and actual, harbour the two key risks of loss and opportunity cost (i.e., missing the boat).

All bubbles eventually burst and leave a wake of losses when they do. However, in instances of false alarm where suspicions of a bubble prove unfounded, those who run for the hills suffer the opportunity cost of missing the proverbial party and leaving significant sums of money on the table.

Even in cases where the bubble moniker has proven to be accurate, things have not been straightforward. Given that irrationality and emotions are the root cause of excesses, bubbles tend to grow much bigger and to persist far longer than what may seem possible (one need look no further than Japanese stocks in the 1980s or tech stocks in the late 1990s to validate this statement). Unlike the false alarm scenario, significant losses do eventually materialize. However, this does not change the fact that investors who step aside before the comeuppance can nonetheless suffer significant opportunity costs as prices continue their often-parabolic extent long after alarm bells begin ringing.

That being said, opportunity cost is not merely comprised of the returns on the investments you forsake, but rather how those missed returns compare to those of the assets for which you forsake them. Even in instances where shunned assets deliver positive returns, if their returns are no greater or less than those of the holdings which replaced them, then the net opportunity cost is zero. Alternately stated, it’s not just about the returns you’re missing, but rather about the returns of what you’re missing vs. the returns you’re getting in their stead.

Not all Bubbles are Created Equal: A Trip down Bad Memory Lane

Historically, different bubbles have been accompanied by very different investment environments, which in turn have presented investors with vastly different prospective risks and returns. This fact is clearly evident across the three debacles of the new millennium, which include the dotcom bubble of the late 1990s/early 2000s, the global financial crisis of 2008-9, and the fixed-income duration bubble of 2021-22.

Whereas there is no such thing as a good bubble (by definition, they all eventually burst), some bubbles occur in environments that are far more ominous than others. In the worst cases, the prospective opportunity costs of avoiding them are acute. Conversely, there are bubbles during which the prospective opportunity costs of avoidance are far less pronounced. In essence, the greater the potential returns are for non-bubble assets, the lower the associated opportunity costs of avoiding the bubble.

The Dotcom Bubble (2000-3): Attractive Alternatives aplenty

The aftermath of the dotcom bubble resulted in significant losses for many investors. In early 2000, U.S. large-cap stocks stood at their highest valuations in modern history. Given the historically inverse relationship between valuations and future returns, it should have been no surprise that disappointment ensued. Between the summer of 2000 and the spring of 2003, the S&P 500 Index declined by 45% in inflation-adjusted terms, while the tech-oriented Nasdaq Composite Index fell 79%.

However, these losses were largely avoidable while simultaneously achieving reasonable returns elsewhere. Emerging-market equities, emerging-market bonds, and REITs exhibited valuations that suggested decent returns over the medium term. While not particularly inspiring, even TIPS and cash were yielding 4% and 2% above inflation, respectively. In essence, investors who were willing to re-allocate based on relative valuations were not backed into a corner: they were not forced to endure meaningfully subpar returns by avoiding what appeared to be (and were subsequently proven to be) overvalued assets.

The Everything Bubble (2007-8): Nowhere to Hide except Bonds

The “Everything Bubble” of 2007-8 and the global financial crisis that followed were entirely different animals. By the time the good times had peaked in 2007, practically all risky equity markets had become overpriced, foreshadowing negative returns over the next several years regardless of country or region.

Unlike the case with the dotcom bubble, only safe-harbour assets such as TIPS, government bonds, and cash offered positive albeit meagre returns. The only way to avoid significant losses was to liquidate all risk assets (as opposed to reallocating within them), hide in safe assets, and accept lackluster albeit positive returns. While doing so would not have been ideal, it nonetheless would have been the least bad alternative.

The Duration Bubble (2021): Nowhere to Hide

The duration bubble of 2021 bore a far greater resemblance to its 2007-8 predecessor than to the dotcom bubble, and in some respects was even more problematic. Investors were stuck between the “rock” of overvalued equities and the “hard place” of bond yields that were substantially below inflation levels. Only cash, which was the only asset that didn’t suffer losses, failed to keep pace with inflation. Continue Reading…

By Bipan Rai, Managing Director, BMO Global Asset Management

(Sponsor Blog)

The end of the year is a special time. The slowing modulation of the markets gives many an analyst time to unplug, which inevitably leads to reflection about what the next year will bring. And as ideas begin to take shape, convictions start to form and a general sense of where the market is headed is reached.

It is almost always a humbling exercise.

For instance, just consider a subset of the important macro/market events from 2025:

The repeated rounds of tariffs and counter-tariffs between the U.S. and its largest trading partners (Canada/Mexico/China/EU).

A massive sell-off in the spring that took the S&P 500 into bear market territory.

The U.S. toying with the idea of raising taxes on foreign investors (Section 899).

Inflation remaining above target across many jurisdictions for most of the year.

Israel and Iran exchanging strikes: with the U.S. also getting involved by attacking Iranian nuclear sites.

Repeated attacks by the U.S. president on the sitting Fed chair, with the president openly admitting that he’d like to fire the chair and replace him with someone who is more aligned to his views.

The U.S. president attempting to remove a sitting Fed board member.

The longest U.S. government shutdown in history.

Market concentration remaining high with AI tiptoeing further into ‘bubble’ territory.

If, at the end of 2024, you had given us the above observations for 2025 there is little chance we would have expected U.S. equities to return 15-16% that year. We would have probably gotten the direction on gold right, but almost certainly whiffed on the magnitude of gains (at around 60%).

That is why we are going into this exercise clear-eyed and with a sense of trepidation (and maybe a bit of dread). What we can say is, given the current set-up the below trades are best positioned to serve our readers well as they look to calibrate for 2026. Please note, this is a very different exercise than our portfolio strategy (which will be out later in the new year). Instead of constructing a portfolio tailored for a particular investing approach, we are selecting ETF trades that we feel will outperform given the available information on the macro that we have on hand now.

First, some basic assumptions:

We expect the U.S. economy to grow at trend (1.8-2.0%1) in 2026 with inflation remaining above the 2% target for the year. Additionally, the labour sector should remain under some modest pressure, which leads the Federal Reserve to cut interest rates 1-2 more times in 25 basis-point (bps) increments.

For Canada, growth is likely to slow from this past year and settle at around 1.4-1.5%. That is still slightly below potential, which implies that inflationary pressures should remain contained. The Bank of Canada (BoC) is likely done easing for now and talks of rate hikes in late 2026 still feel premature.

We expect the S&P 500 to rally by about 8-10% in 2026.

We expect a consolidative environment for CAD and U.S. yields to start the year, which should give way to upside as the year progresses.

We see downside risks to USD/CAD2 over the next three months.

With that out of the way, let’s get started.

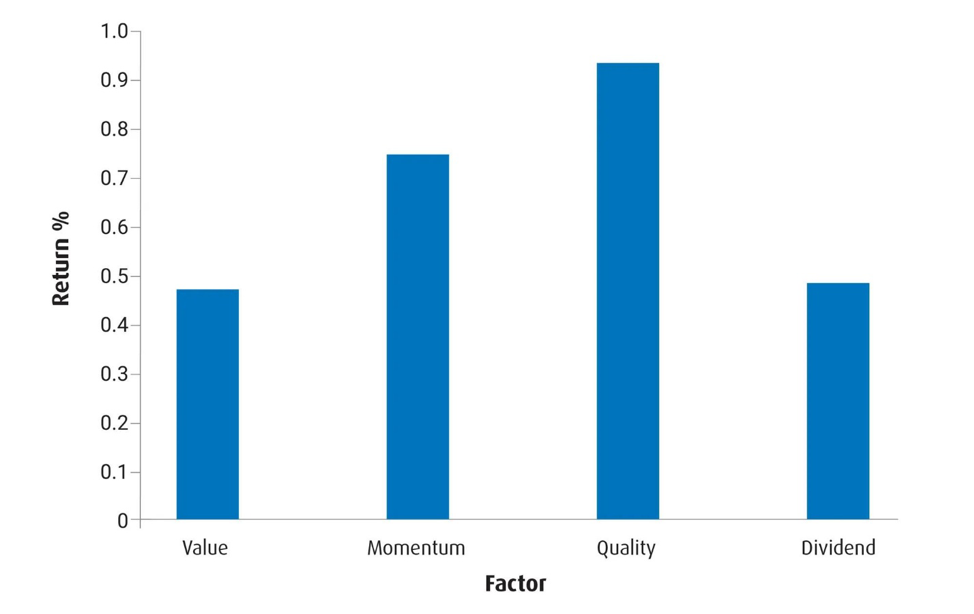

Theme #1: Late-cycle dynamics still favour Quality …

Into 2026, we’d characterize the backdrop for the U.S. economy as one that favours resilience over cyclicality. That is not least given that the current phase of economic expansion feels a bit long in the tooth and the combination of fiscal and monetary measures might lead to an economy that runs hot (i.e., higher prices, moderate growth). In such an environment, we expect investors to prioritize companies with strong balance sheets and stable earnings: important ‘Quality’ characteristics.

Chart 1 – Average monthly returns for months when Core CPI is > 2%3

Source: BMO Global Asset Management / MSCI. For U.S. factors; observations go back by 14 years.

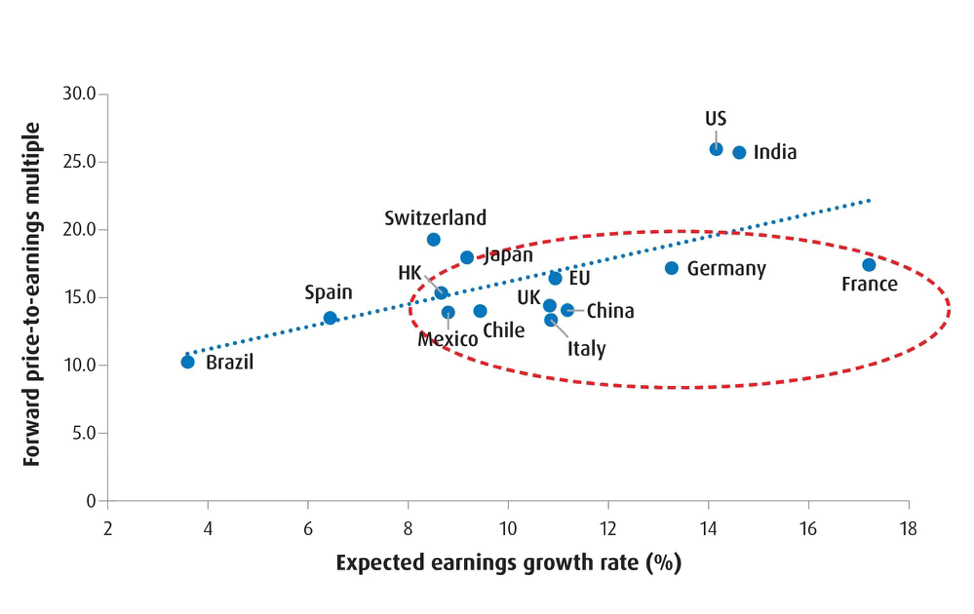

Theme #2: … But with broader leadership …

Much of 2025 was characterized by a migration of flows out of the U.S. and into EAFE and EM markets.4 Given the strength and stability of earnings outside of North America, we expect this theme to continue into 2026.

Aside from valuation (see Chart 2), two other catalysts for this resiliency will be the widespread adoption of new technologies in non-U.S. markets, and fiscal expansion in many countries. Both should work together to improve productivity trends outside of the U.S.

In the emerging world, we see the alignment of different themes working together to attract additional capital to these regions. Indeed, commodity exporters in Latam5 should continue to benefit from rising prices, while an improving backdrop in China should boost activity in smaller Asian markets.

Chart 2 – Several international markets still look cheap relative to the U.S.

Source: BMO Global Asset Management / MSCI. A forward price-to-earnings ratio (Fwd P/E) is a stock valuation metric that compares a company or stock index’s current share value to estimated future earnings over the next 12 months.

Theme #3: … And a rotation away from AI

The delicate rotation away from AI/Tech and into other sectors should continue and will likely engender further uncertainty. However, greater adoption of technology outside of Tech/Communications sectors will likely shift capital over to cheaper segments of the U.S. market.

Within the Tech/Communications sectors, we feel active strategies will be better placed to perform. That is largely because the market will become judicious about picking winners and losers in the AI race as increased reliance on debt financing will mean that existing capital structures are more heavily scrutinized. That should portend a more consolidative environment for broad tech: which supports a product like ZWT, given its generous yield.

Outside of tech, two sectors that we feel are best positioned are U.S. Health Care and Financials. In particular, Health Care has emerged as an effective hedge against AI-related concerns. The sector is still a bit ‘cheap’ as well, which has also worked to support its performance over the past months.

For Financials, we expect demand for loans in the U.S. economy to remain strong: not least as household balance sheets remain in good standing and as valuations remain cheap when compared to other sectors. An additional tailwind comes from regulatory changes that should free up more capital for deployment.

In Canada, we remain constructive on Financials but also acknowledge that the market is likely to be one in which alpha6 can be generated through more active strategies.

Indeed, we continue to like Canadian banks. Strong capital positions and the ability to generate revenues outside of traditional retail-based lending means there are plenty of opportunities for capital deployment in 2026. However, valuation remains a bit of a headwind. As such, we favour a covered call strategy instead of a beta7 one. Continue Reading…