And the seasons they go round and round

And the painted ponies go up and down

We’re captive on the carousel of time

We can’t return we can only look behind

From where we came

And go round and round and round

In the circle game

- The Circle Game, by Joni Mitchell

By Noah Solomon

Special to Financial Independence Hub

This month, I will discuss mean reversion and momentum, which are arguably the two most powerful forces in markets. I will demonstrate that while these two influences can sometimes work in tandem, they often stand in fierce opposition. Lastly, I will discuss mean reversion and momentum in the context of the current market environment, including the related implications for investors.

Mean Reversion: Valuation’s Revenge

One of the most conclusively documented phenomena in modern markets is mean reversion, which is based on the historical tendency of returns to gravitate toward their long-term average. Above-average returns tend to be followed by below-average returns, and vice versa, thereby resulting in a reversion to “normal” levels over the long term.

Buffett succinctly summarized this observation in his statement, “I would rather sustain the penalties resulting from over-conservatism than face the consequences of error, perhaps with permanent capital loss, resulting from the adoption of a ‘New Era’ philosophy where trees really do grow to the sky.“

Mean reversion has been pervasive across geographies, sectors, individual stocks, and broad asset classes. Countries whose markets have outperformed their peers by large amounts have subsequently underperformed, while previously unloved regions have gone on to be investor favourites. Similarly, “winning” stocks and sectors have morphed into stragglers, while those that were neglected have become market heroes. Lastly, at times when broad asset classes have experienced higher than average returns, they have subsequently delivered subpar performance, while producing streaks of better than average performance after periods of subpar returns.

At the heart of mean reversion lie valuations. Whenever a given stock, sector, or market has delivered higher than average returns for an extended period, this outperformance is usually accompanied by lofty valuations which are fundamentally unjustifiable. These excessive multiples begin to weigh on prices, leading to underperformance and the return of valuations to more rational levels. By the same token, at times when a given asset or group of assets have experienced below average returns for a prolonged period, their multiples tend to become unreasonably depressed. The resultant “bargains” ultimately attract investor interest, which in turn leads to outperformance and the establishment of more rational valuations.

Momentum: The Road to Valhalla and Dystopia

The other principal force that drives markets is mean reversion’s volatile counterpart, momentum. Momentum investing capitalizes on the tendency for trends to persist by buying into rising assets and selling into falling ones. As is the case with mean reversion, academic research has found momentum across individual securities, sectors, and broad asset classes.

Unlike mean reversion, which is based on fundamental valuation principles, momentum is best explained by behavioural biases and emotions. Spurred by fear of missing out (FOMO) and greed, investors tend to buy assets whose price has been rising, leading to further gains. In similar fashion, fear and despondency can cause people to sell assets whose price has been falling, thereby reinforcing negative trends and causing additional losses.

Mean Reversion, Momentum, & the Market Cycle

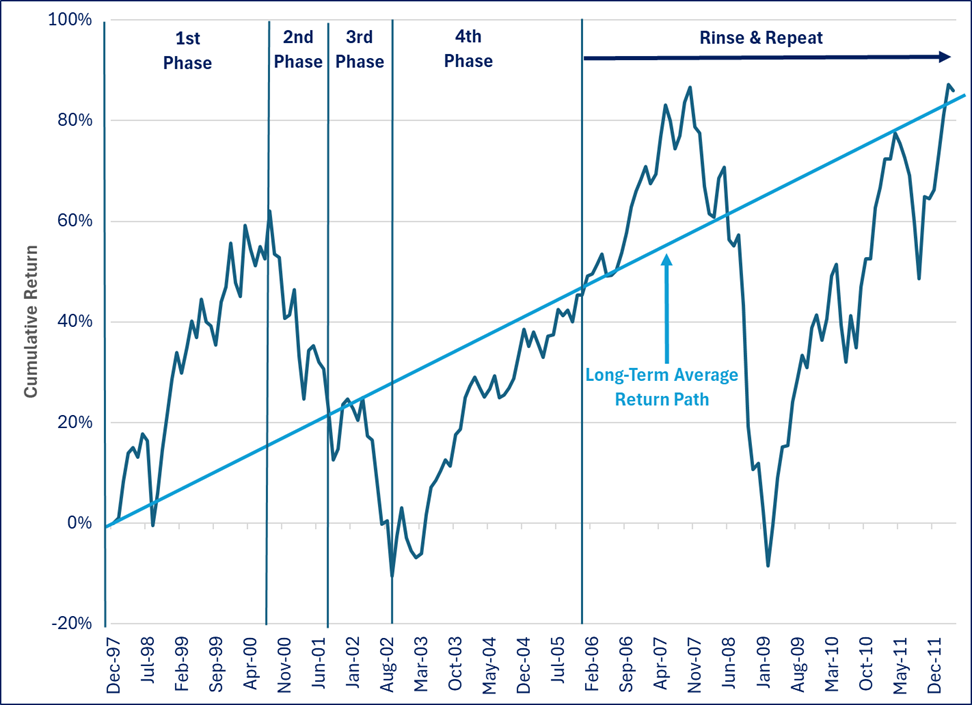

As illustrated in the graph below, the market cycle can be divided into four phases.

The Market Cycle: S&P 500 Index

1st Phase: The March to Valhalla

- At the beginning of this phase, markets are neither materially overvalued nor undervalued. Then, some catalyst or combination of factors causes prices to begin straying increasingly further above their “fair” or intrinsic values.

- This deviation is often caused by overly optimistic assumptions about the economy and/or profit growth. It can also stem from overexcitement about some theme du jour, like technology stocks during the dotcom bubble (as depicted in the 1st phase in the graph), real estate during the years preceding the great financial crisis, or (dare I say) today’s AI-related companies.

- Towards the end of the period, optimism morphs into full-blown euphoria and the momentum monster kicks into high gear. This dynamic eventually causes many assets to be priced to perfection, leaving them in the precarious position of offering little, if any upside while harbouring significant downside risks, as was the case in late 1999-early 2000.

2nd Phase: The Beginning of the End

- This period takes the reins from its predecessor when valuations stand well above average levels, broad sentiment starts to turn, and fear begins to take centre stage, thereby causing prices to start falling.

- As the phase progresses, negative momentum begins to take hold, and prices continue their decline. This process unfolds until they once again reflect reasonable assumptions regarding the future and assets are more or less fairly valued, as was the case between the peak of the dotcom bubble and the bear market bottom of late 2002.

3rd Phase: The End of the World is Nigh – I Will Never Invest in Anything Again

- At this point, fear and skepticism begin to metastasize into full-blown panic, accompanied by a widespread belief that things can only get worse. Relatedly, negative momentum reaches its nadir, leading to a final cyclical swoon in prices, as occurred towards the end of the tech-wreck in mid-to-late 2002.

- By the end of the period, sentiment becomes completely washed out, leaving many assets at materially depressed valuations that offer significant upside for relatively low risk.

4th Phase: Maybe Things Aren’t So Bad – I Like Bargains

- At the beginning of this phase, all but the most steel-nerved investors have run for the exits in one form or another, as was the case at the bottom of the early 2000s bear market.

- Tempted by bargain basement valuations, a minority of rational and courageous contrarians begin stepping in to scoop up bargains.

- The advent of fresh buying, combined with a dearth of remaining sellers, sparks a recovery in prices.

- This recovery begins to attract additional buyers to the party and reawakens the ghost of positive momentum, leading to further gains until the end of the period, when assets are neither materially undervalued nor overvalued.

Postscript:

- Repeat phases 1-4 in tragic (or comedic) fashion of Shakespearean proportions.

Momentum is a Fairweather Friend. Value is Forever

Over the short term, momentum and sentiment are the primary determinants of asset prices. At times when FOMO, greed and optimism are most pronounced, the power of momentum cannot be understated. Rationality and traditional valuation principles are widely forgotten, which can lead to irrationally high and unsustainable prices. Conversely, when fear and pessimism rule the roost, negative momentum can easily overshadow the fact that many beaten down assets present unusually attractive opportunities, which in turn can lead to senselessly low prices.

Notwithstanding that extreme environments have historically reverted, investors have time and again failed to take advantage of this fact, joining the overwhelming chorus of “this time it’s different.” According to famed economist John Kenneth Galbraith:

“When the same or closely similar circumstances occur again, sometimes in only a few years, they are hailed by a new, often youthful, and always supremely self-confident generation as a brilliantly innovative discovery in the financial and larger economic world. There can be few fields of human endeavor in which history counts for so little as the world of finance. Past experience, to the extent that it is part of memory at all, is dismissed as the primitive refuge of those who do not have the insight to appreciate the incredible wonders of the present.”

However, sentiment and momentum are fickle beasts that are extremely difficult, if not impossible to time. While they can sustain for extended periods and carry prices to fundamentally absurd extremes at both ends of the spectrum, they also have a tendency to suddenly and violently turn, leaving those who had been riding the momentum express caught in a train wreck of losses. As legendary trader Ed Seykota stated, “The trend is your friend except at the end where it bends.” Continue Reading…