Thanks to high-fee mutual funds, Canadians are leaving a lot of money on the table. While superior ETF investment options have been available for more than two decades, Canadians are slow to help themselves out. Those fees are wealth destroyers. We’re not making the move to ETFs at the pace of the rest of the developed world. It’s a no-brainer. Canadians can find investment options at less than 1/10th the cost. But too much money is still going into the wrong pockets – that of advisors and the mutual fund providers. We’re leaving too much money on the table, in the Sunday Reads.

Here’s the graphic that shows Canada is slow on the uptake …

The irony is that Canadians need to embrace low-cost index funds more than most people on earth. We pay some of the highest fees on the planet. And those high-fee mutual funds most often come attached to an advisor who offers no advice, or poor advice. They are salespersons, not real advisors. From the Globe & Mail piece …

Canadian investors, on the other hand, have been far slower to shift their allegiances to indexing. Since 2013, Canadian passive funds increased their market share from 10.4 per cent to just 15.5 per cent currently. Continue Reading…

When I ask clients and prospective clients about the return expectations they have for their portfolios, the responses vary wildly … anywhere from ‘about 5%’ to ‘over 10%.’ Almost all of these expectations are too high.

Admittedly, clients have different risk profiles leading to different asset allocations and ultimately, different outcomes. That’s reasonable. A problem crops up when otherwise reasonable people have been socialized into having out-sized expectations. How does one ethically re-calibrate expectations for irrational optimists who nonetheless think they’re within their rights to have those expectations?

The behavioural finance concept is overconfidence, although the attitude involves elements of optimism bias, cognitive dissonance and old-fashioned hubris, too. To quote J.M. Keynes: “Markets can remain irrational longer than you can remain solvent.” Few investors are prepared to acknowledge that the recent bull market seems unlikely to continue and that a recession appears to be on the horizon.

Learning from past Crashes

If we have learned anything from the great crashes of 1929, 1974, 2001 and more recently, the global financial crisis, it is that investors (often spurred by accommodative policy positions) can come to think of themselves as being all but invincible when central bankers are accommodative. Too often, they also lose their nerve when markets tumble and stay low for a prolonged period.

A good deal of personal finance is grounded in social psychology: especially group psychology. People can get ahead through investing not only by being shrewd about valuations and such, but also by accurately anticipating how other market participants might react to a given set of circumstances. Of course, it cuts both ways: and having reasonable expectations in the first place often assists investors in staying the course.

My concern is with the messaging being offered by many in the personal finance community these days is something I call “Bullshift.” The industry shifts peoples’ attention to make them feel more bullish. To hear many in the business tell it, there’s no appreciable need to be concerned about high valuations, high debt levels (both public and private), a long-inverted yield curve and interest rates at generational highs. Any one of these considerations would ordinarily give a rational investor pause. Taken together, they pose a clear and present danger for investors in the second half of 2024. Few seem concerned and it is that very lack of concern that concerns me.

Misleading investors with “Bullshift”

There is a directionally and mathematically accurate ad running by Questrade making the rounds that doesn’t tell the whole picture, either. Again, even the ‘good guys’ tend to mislead the average investor with Bullshift. The advertisement shows what you would earn over a long timeframe at 8% and what you would earn at 6%.

My question to you is simple: is it reasonable to assume an 8% return is even possible? There is longstanding evidence that higher-cost active investment strategies actually fail to outperform cheaper strategies such as passive index investing and that product cost certainly does matter. Continue Reading…

Markets can be Scary but more importantly, they are Resilient

LowrieFinancial.com: Canva custom creation

By Steve Lowrie, CFA

Special to the Financial Independence Hub

Most investors understand or perhaps accept the fact that they are not able to time stock markets (sell out before they go down or buy in before they advance).

The simple rationale is that stock markets are forward looking by anticipating or “pricing in” future expectations.

While the screaming negative headlines may capture attention, stock markets are looking out to what may happen well into the future.

Timing bond markets is even harder than timing stock markets

When it comes to interest rates and inflation, my observation is that the opposite is true. Most investors seem to think they can zig or zag their bond investments ahead of interest rate changes. This is perplexing, as you can easily make the case based on evidence that trying to time bond markets is even more difficult than trying to time equity markets.

Another observation is that many investors tend to be slow to over-react. Reacting to today’s deafening headlines ignores that fact that all financial markets are extremely resilient. Whether good or bad economic news, good or bad geopolitical events, markets will work themselves out and march onto new highs, albeit sometimes punctuated by sharp and unnerving declines. Put another way, declines are temporary, whereas advances are permanent. And remember, this applies to both bond and stock markets.

It is easy to understand why we might be scared about the recent headline inflation numbers and concerned about rising interest. It is very important to keep this in context, which is what we will address today.

In my experience — over 40 years of advising investors on how to build wealth — too few fellow Canadians have diversified their stock holdings into U.S. stocks.

Unfortunately, most Canadian investors still believe — falsely — that it’s too costly or too much hassle to buy U.S. stocks.

Most importantly, these investors have also ignored U.S. stocks’ tremendous safety and profit advantages to Canadians.

I believe that up to 30% of every Canadian stock market portfolio should consist of U.S. stocks, for the following three reasons:

U.S. stocks give you risk-reducing diversity. Canadian stocks are great, but so many are focused on natural resources —so when such commodities sink, so do your returns. U.S. stocks are spread across far more industries, giving you a broader cushion during market volatility.

U.S. stocks give you international opportunities. Top U.S. stocks are multi-national revenue earners, so you benefit from booming international markets. It means your portfolio is safer and stronger than just relying on Toronto exchange stocks.

Investing in U.S. stocks is easy and extremely profitable. Don’t worry: Buying U.S. stocks through your regular broker is as easy as buying Canadian stocks. And no matter the dollar exchange rate, when you get good returns, the currency exchange costs are insignificant.

If your portfolio has no U.S. stocks —or if you’re not satisfied with the performance of your current U.S. stocks — I recommend you take a free look at Wall Street Stock Forecaster.

Here’s how to spot the best U.S. stocks

Now is a particularly good time to follow our three-part Successful Investor investment approach — including for U.S. stocks:

Rule #1: Invest mainly in well-established, profitable, dividend-paying U.S. stocks.

Our first rule in the most successful investment strategies will help you stay out of high-risk, low-quality investments. These investments are always available, in good and bad markets. They come with hidden risks due to conflicts of interest and other negatives. Every year, they lead many inexperienced investors to substantial losses.

Recent standout losers include bitcoin and other cryptocurrencies; a disappointing crop of new issues (IPOs), which tend to come to market when it’s a good time for the new-issue company or its insiders to sell, but not a good time for you to buy; and slapped-together promotional stocks that hit the market thanks to the SPAC phenomenon, which offers a short cut to IPO status.

Instead, focus on well-established, profitable, dividend paying U.S. stocks. But, when looking for dividend-paying stocks, you should avoid the temptation of seeking out stocks with the highest yields — simply because they have above-average yields. That’s because a high yield may signal danger rather than a bargain if it reflects widespread investor skepticism that a company can keep paying its current dividend. In short, high dividend paying stocks can come with pitfalls. Dividend cuts will always undermine investor confidence, and can quickly push down a company’s stock price.

Above all, for a true measure of stability, focus on stocks with a high dividend yield that has been maintained or raised during economic or stock-market downturns. Generally, these firms leave themselves enough room to handle periods of earnings volatility. By continually rewarding investors, and retaining enough cash to finance their businesses, they also provide an attractive mix of safety, income and growth. A track record of dividend payments is a strong sign of reliability and an indication that investing in the stock will be profitable for you in the future.

Rule #2: Spread your money out across most if not all of the five main economic sectors.

This is our key to successful diversification and the widely disparaged resource sector saw some major winners last year. On the other hand, if you had disregarded resource stocks with the intention of doubling down on tech stocks, you might have wound up with excessive holdings in tech stocks just as they entered a plunge. Continue Reading…

I see the bad moon a-risin’

I see trouble on the way

I see earthquakes and lightnin’

I see bad times today

Don’t go around tonight Well it’s bound to take your life There’s a bad moon on the rise

Creedence Clearwater Revival

The Curious Case of Missing Inflation

Image by Shutterstock/Outcome

Prior to the global financial crisis of 2008, if you had asked me what would happen if the Fed and other central banks slashed rates to zero and then left them there for over a decade, I would have told you that it wouldn’t be long before the world faced a serious inflation problem. I would have been dead wrong!

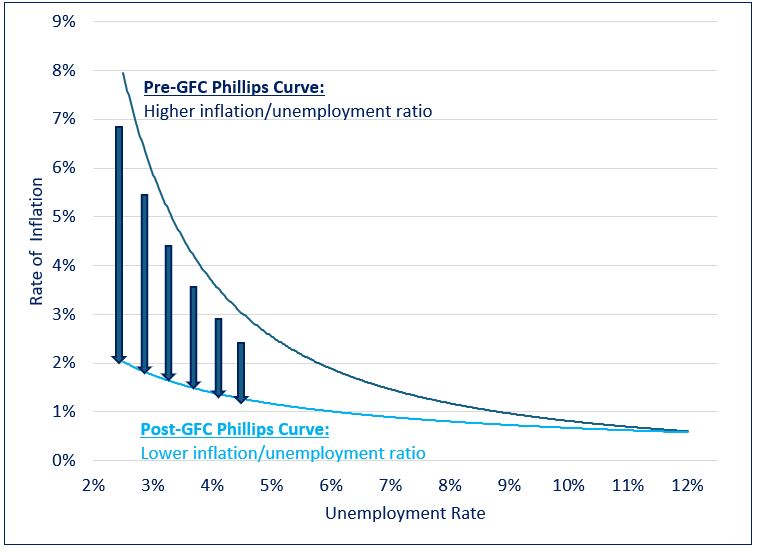

The Phillips curve is an economic concept developed by A. W. Phillips that describes the relationship between inflation and unemployment. The theory holds that there is an inverse tradeoff between the two variables. All else being equal, lower unemployment leads to higher inflation, while higher unemployment is associated with lower inflation.

Phillips’ theory proved largely resilient for most of the postwar era. However, a notable exception occurred in the years following the global financial crisis (GFC). From 2009 to 2021, despite unprecedented amounts of monetary and fiscal stimulus and record low unemployment, global prices remained unexpectedly subdued.

The Evolution of the Phillips Curve

As the chart above illustrates, in the years following the GFC the Phillips curve seemed to have shifted downward. This change allowed global economies to sustain low levels of unemployment that historically would have been accompanied by runaway inflation.

The classic unemployment vs. inflation tradeoff seemed to have vanished, leaving central bankers in the enviable position of being able to leave rates at uber stimulative levels for an extended period without spurring runaway inflation. This dynamic remained in place until 2021, when the rubber of unprecedented quantities of monetary and fiscal stimulus met the road of Covid-related supply-chain disruptions. This combination brought an abrupt end to the disinflation party of the past decade, causing central banks to raise rates at a blistering pace the likes of which had not been seen since the Volcker era of the 1980s.

Declining Interest Rates: How do love thee?

The long-term effects of low inflation and record low rates on asset prices cannot be overstated. On the earnings front, low rates make it easier for consumers to borrow money for purchases, thereby increasing companies’ sales volumes and revenues. They also enhance companies’ profitability by lowering their cost of capital and making it easier for them to invest in facilities, equipment, and inventory. Lastly, higher asset prices create a virtuous cycle: they cause a wealth effect where people feel richer and more willing to spend, thereby further spurring company profits and even higher asset prices. Continue Reading…