A majority of nearly retired Canadian households — 55 per cent — will have to make lifestyle changes to avoid running out of money in their old age, says a Deloitte Canada report released on Wednesday.

Worse, that percentage jumps to almost three quarters (73%) if you factor in unexpected costs like health care, long-term care costs and occasional one-off expenses. You can find the full release here from Canada Newswire.

Some 4,000 retired and near-retired Canadian households were surveyed, all between ages 55 and 64.

Only 14% of 3 million soon-to-retire households can retire with confidence and be able to absorb unexpected costs without much stress. This fortunate group tends to have at least $900,000 in financial assets and likely have a paid-for home.

31% of near-retirees will require support in the form of the government’s public pension system: nearly a million households are expected to rely mainly on the Canada Pension Plan in retirement.

Only 24% of private-sector workers participate in employer-sponsored pension plans

40% of retirees have not purchased health insurance, of which 44% cite expensive premiums as the primary reason for not doing so

73% of near-retiree households will be at risk of financial hardships in later stages of life if they require long-term care

58% of near-retiree and retiree households do not have a formal or detailed retirement plan in place

44% of working Canadians were dipping into their retirement savings to pay for non-retirement-related expenses

“By employing a host of radical and innovative solutions, Canada can help to protect those vulnerable both near and in-retirement, and set a global standard for how it tackles retirement on the world stage,” says Hwan Kim, Partner, Financial Services Innovation and Open Banking at Deloitte Canada in the press release, “Given roughly 40 per cent of retirement wealth inequality is due to a lack of financial knowledge, the financial services ecosystem must collaborate with the health care system and public sector to equip Canadians with accessible retirement advice, holistic near-retirement offerings, updated pension planning, quality health care, and new resources to retire confidently.”

The report concedes the saving for Retirement has always been “a daunting challenge for working Canadians,” things have gotten worse the last few years. The shift from employer-provided guaranteed Defined Benefit pensions to group RRSPs and Defined Contribution pensions that fluctuate with financial markets is a major hurdle. The report also cites the rising costs of retirement, a lack of high-quality, near-retirement planning resources, and unexpected expenses during late-stage retirement.

According to the report, 55 per cent of near-retiree households will need to make lifestyle changes to avoid outliving their financial savings – a number that is expected to jump to 73% when factoring in unexpected expenses such as healthcare, long-term care costs, and one-off expenditures.

A Bank of Montreal survey released early in 2023 found Canadians believe they need $1.7 million to retire. My blog on this in February asked whether this was doable or not.

Financial services silos must collaborate

The Deloitte report says the Canadian financial services “ecosystem must collaborate across banking, wealth management, insurance, and the public sector.” This ecosystem needs to focus on three main categories of commercially viable solutions: improve the quality and accessibility of near-retirement advice and products, help retirees manage rising retirement costs, and help Canadians build healthy saving habits early on. Continue Reading…

By Alizay Fatema, Associate Portfolio Manager, BMO ETFs

(Sponsor Blog)

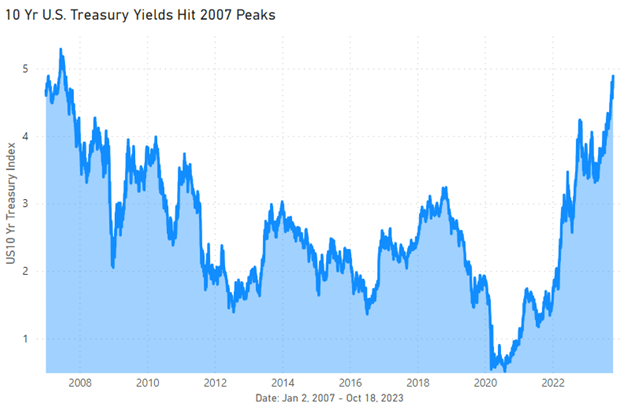

The latest economic data unveils a captivating narrative of a strong and resilient economy in both Canada and the U.S. The current inflation stickiness and robust job market numbers make a solid case for the central banks in both countries to keep interest rates higher for longer.

Towards the end of September 2023, markets basked in record-high yields. However, earlier this month, based on the current situation in the Middle East, bond yields fell owing to an increase in demand for safer assets and caused longer-term bond prices to surge. U.S. consumer prices remained elevated for the month of September and a pullback in demand for a treasury auction pushed longer-term yields higher again, resulting in 10-yr U.S Treasury yields touching their highest point since 2007. On the contrary, the recent CPI printed lower than expectations in Canada, yet the yields remain high as hot economic data continues to build pressure south of the border.

Source: Bloomberg

Given the current two-decade-high interest rates, yields on Aggregate Bond ETFs have surpassed 5%, making them an interesting avenue for fixed-income investors. Before we dive in further, let’s discuss some aggregate bond ETFs in detail along with their benefits.

Aggregate Bond ETFs as the Core of your Investment Strategy

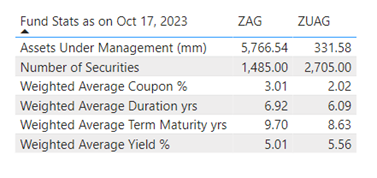

Aggregate bond ETFs are exchange traded funds that aim to track performance of a diversified portfolio of bonds. These ETFs are referred to as core because it reflects their status as a foundational building block of a well-rounded investment portfolio. These ETFs can help investors achieve diversification, steady income & stability within their investment portfolios. BMO currently offers two Aggregate Bond ETFs:

BMO Aggregate Bond Index ETF (ZAG) aims to replicate the performance of the FTSE Canada Universe Bond Index. This ETF primarily invests in a Canadian investment-grade fixed income securities consisting of Federal, Provincial and Corporate bonds, with a term to maturity greater than one year.

BMO US Aggregate Bond Index ETF (ZUAG) tracks the performance of the Bloomberg US Aggregate Bond Index. It invests in U.S. investment-grade bonds such as U.S. treasury bonds, government-related bonds, corporate bonds, mortgage-backed pass-through securities, and asset backed securities with a term to maturity greater than one year. ZUAG is also offered as hedged to CAD (ZUAG.F) and in USD (ZUAG.U).

Source: BMO Asset Management.

These aggregate bond ETFs have proven to be an extremely viable investment solution owing to their key features:

The Symphony of Diversification: Aggregate Bond ETFs provide exposure to a broad spectrum of bond market offering diversification across the curve, various sectors and segments, maturities, issuers, and credit qualities; making them resilient for any market environment.

For example, in the current high-interest rate environment, exposure to short duration bonds might provide some down-side protection. On the other hand, if central banks start cutting rates, then longer duration can provide some upside potential.

Aggregate Bond ETFs can also be considered an equity market hedge. Given the inverse correlation between equities and bonds, they can provide a cushion against market turbulence and can potentially outperform stocks during selloffs.

Harnessing Cost Efficiency through Lower Fees: These ETFs are passively managed with the aim to track performance of the aforesaid indices. Their expense ratios are lower as compared to some actively managed funds, thereby reducing overall investment costs and improving net returns for investors. BMO is currently charging a Management Expense Ratio of 0.09% for both ZAG & ZUAG.

Liquidity & Ease of Trading: Like all other ETFs, ZAG & ZUAG are traded on stock exchanges, enabling investors to easily buy and sell shares throughout the trading day, allowing them to see real-time prices. The bid-ask spreads on these products are lower in contrast with the underlying bonds which enhances their liquidity compared to traditional bonds, making them a cost-effective way to attain the exposure to the aggregate bond market.

Navigating Risk Management through High Credit Quality: Aggregate Bond ETFs are perceived as a stable and safer investment option as they provide exposure to investment-grade bonds, which are considered to have lower risk as opposed to high-yield or junk bonds. In the current rising interest rate environment, the credit quality & relative stability of the investment grade bonds make them an appealing choice for investors seeking to minimize risk & preserve capital.

Combined with the key features mentioned above, these Aggregate Bond ETFs provide investors with a low-cost core in any investment portfolio. They distribute monthly interest payments, providing a steady stream of income. These ETFs emphasize on preservation of capital and provide transparency and visibility into the funds’ composition and their underlying assets. Continue Reading…

The following is an edited transcript of an interview with Michael Kovacs, CEO of Harvest ETFs, conducted by Financial Independence Hub CFO Jonathan Chevreau.

Jon Chevreau (JC)

Thanks for taking the time today, Michael. We all know that 2022 was a pretty bad year as markets were impacted by higher interest rates. That turbulence bled into much of 2023, although the last few weeks have seemed much rosier.

How do you respond to unitholders of funds who are currently down year over year? Does your covered call writing protect retirees?

Michael Kovacs

Michael Kovacs (MK)

Thanks for having me, Jon. It is important to remember that we offer equity income funds. That means that you have to look at the total return of the product, which includes the price of the ETF and its accumulating distributions.

Yes, there has been turbulence in 2022 and through much of 2023. However, over that period, products like the Harvest Healthcare Leaders Income Fund (HHL) have paid consistent distributions.

Let’s look at the Harvest Diversified Monthly Income ETF (HDIF). In terms of actual returns, this ETF is down nearly double-digit percentage-wise in the year-over-year period (as of early November). But, when you look at the distributions paid over that same period, HDIF has delivered positive cashflow for its unitholders, which reduces the decline by more than half.

JC

Are you saying that between the covered calls, the distribution and the leverage plus the underlying equity income, that a retiree could expect annual yields as high as 10% or 12% or higher?

MK

Yes. Yields are anywhere from 1.5% to 3%, depending on the equity category. Then you have option writing. We can go right up to 33% on any of those portfolios, which generates additional yield. So, to be able to generate 9-10% is very achievable. And we’ve been able to do that consistently for a quite a few years now.

Jon Chevreau

JC

What is your view on the current interest rate climate? Have we reached a top? If so, when will they start to come down?

MK

Many of us remember the high interest rates of the 1980s, especially some of your readers who were trying to obtain their first mortgages. We have experienced a big jump in interest rates over the past two years. However, we believe that we have probably seen the top for rates for now. Or, if we haven’t, we are very close to the top. That means there are going to be some great opportunities in fixed-income markets. The next move for interest rates may be down by mid-to-late 2024.

That said, there are still great opportunities that will benefit equities and bonds in the current climate. Our first launch in the Bond area is the Harvest Premium Yield Treasury ETF (HPYT). We’ve launched with a high current yield. We are targeting long treasury bonds in this fund. This is about generating a high level of income while owning a very good credit-worthy security like a U.S. Treasury. So, if rates start declining next year, it is a great time to be holding fixed income.

JC

Findependence Hub readers tend to be retirees who want steady cash flow. What is Harvest’s view of cash flow for retirees?

MK

I think cash flow for retirees is essential. Once your employment income has gone, you must depend on your investments, your pensions, your CPP, and so on. The recent increases in interest rates have been good for retirees in the short term. Higher rates allow retirees to keep shorter-term cash and generate a safe yield of 5% or more.

Our longer-term equity products aim to have that heavy bias toward equities. For example, the Harvest Healthcare Leaders Income ETF (HHL) is typically written at about 25-28% average, with the other 70% or so fully exposed to health care stocks. The covered call option writing strategy allows us to generate a high level of income.

Cash flow is the basis behind our name: Harvest. People have spent decades building up capital, sowing the seeds. Our products allow them to harvest the fruits of their life-long labour.

We believe our equity-income and fixed-income products are a fantastic way to do that. If we can help you preserve capital and generate consistent income, we are doing our job.

JC

There is also interest among investors in asset allocation ETFs. Is HDIF essentially your answer to that demand?

MK

You’re correct. Some people prefer to allocate to specific funds, but the idea behind HDIF is to allocate to the best of Harvest’s top products that generate cash flow. In the case of HDIF, you do have a leverage component. You are increasing the yield but at the same time, you do increase your risk as well. Continue Reading…

Joe Biden this week carrying a copy of Democracy Awakening, via Threads.

While the Hub’s focus is primarily on investing, personal finance and Retirement, Findependence has given me sufficient leisure time to absorb a lot of content on politics and the ongoing battle to preserve democracy and in particular American democracy. What’s the point of achieving Financial Independence for oneself and one’s family, if you find yourself suddenly living in a fascist autocracy?

To that end, I have recently read two excellent books that summarize where we are, where we have come from and where we likely may be going. These books came to my attention from two relatively new social media sites I joined in the past year.

For those who care, I am still on Twitter (now X) but restrict most of my posts there to the financial matters on which this blog focuses. I post there as @JonChevreau, which is the same handle I have on Mastodon (since Nov 6, 2022) and Threads, which I joined a week after its early July launch this summer. Threads is now almost the polar opposite of X politically, a veritable Blue haven: just last week Joe & Jill Biden both signed on as @potus and @flotus respectively, as well as under their real names. So did vice president Kamala Harris (posting as @VP and @kamalaharris).

Amazon.ca

But back to the books. The first must read is Prequel, by the brilliant U.S. broadcaster Rachel Maddow [cover image shown on the left]. Tellingly, it’s subtitled An American Fight Against Fascism.

The second is Democracy Awakening, by Heather Cox Richardson [cover shown below]. Both are available as ebooks on the Libby app, through (hopefully) your local library. I couldn’t find either book on Scribd (now called Everand) but they do have ebook Summaries of both.

An American Hitler?

Given that the 2024 U.S. election is now about 12 months away, there is a certain urgency to these books. The Maddow book I’d read first since it’s a brilliant historical recap of the rise of German Fascism in the 1930s and — the shocking bit! — how close Germany came to installing fascists in America. It’s literally about Germany’s search for an American Hitler it hoped to install. It’s full of sinister characters you’ve probably not heard about before, like the assassinated Huey Long.

Maddow credits the reader with enough intelligence to extrapolate from that period into the current dangerous environment. One is left to infer how she feels about the parallels to the modern GOP and its fascist leader and would-be dictator: she never says their names although she is usually more explicit in her MSNBC and podcast commentaries.

Modern readers could easily substitute Putin’s Russia for Hitler’s Germany and draw their own conclusions about the parallels to collusion with foreign powers. There are also similarities between protracted attempts by the U.S. government to try the perpetrators in court and the protracted Delay tactics of the Defence — including many U.S. senators of the 1930s and early 1940s. And as is currently the case, these tactics largely seemed to work, since the Allies won World War II before most of the collaborators were brought to justice. Frustrating indeed, as many of today’s Americans bristled at the ultimate futility of the Mueller Report around 2019 and other protracted legal proceedings that may not be resolved before the 2024 election.

Maddow of course hints at this right at the end, quoting one frustrated prosecutor (O. John Rogge) from the 1940s:

“The study of how one totalitarian government attempted to penetrate our country may help us with another totalitarian country attempting to do the same thing …the American people should be told about the fascist threat to democracy.”

To help you on your journey towards financial independence, we’ve gathered 15 frugal living tips from financial advisors, founders, and other professionals.

From delaying big-ticket purchases, to asking for deals to save money, these experts share their best practices for frugality and financial independence.

Delay Big-Ticket Purchases

Master Budgeting and Tracking Spending

Align Budget with Personal Values

Plan Meals to Control Food Budget

Distinguish Between Needs and Wants

Prepare Lunch at Home for Savings

Leverage “Stoozing” for Mortgage Savings

Track Expenses for Financial Insight

Eliminate Unnecessary Subscriptions

Use Technology for Financial Management

Prioritize Spending with Budget Tracking

Cut Expenses from Seldom-Used Subscriptions

Invest in Experiences, Not Impulse Buys

Wait a Month Before Impulse Buying

Ask for Deals to Save Money

Delay Big-Ticket Purchases

When climbing the pay ladder, I purposefully delayed purchasing big-ticket items such as a newer or more expensive home, car, or luxury item. When I review my spending in detail, I’ve found it typically isn’t an $8 latte (or several of them) that puts me over the discretionary-spending edge, but rather something like a luxury handbag that I felt I deserved at the time, yet doesn’t bring me sustained happiness.

That is to say, in hindsight, it would feel better to see my investment portfolio increase than to have a closet of designer wares. It’s important to build a budget for yourself, but equally or more important, to reconcile your past spending and decide whether to make an adjustment to the budget or your spending to be more accurate moving forward. — Morgan Jarod, Financial Advisor, Royal Private Wealth

Master Budgeting and Tracking Spending

There are many clever ways to cut expenses or generate extra income, but there is no replacement for the discipline of budgeting. A budget is the daily application of your long-term goals. It serves as a compass for your financial journey, making sure you are consistently moving towards your destination.

There are two parts to every great budget: planning and tracking. First, you need to write out a plan for how you are going to spend every dollar of income you will earn in a given month. Then, you need to track your spending to ensure you are following your plan.

It would amaze most people at how much progress they can make toward their financial goals by simply using a budget to align their spending with their goals.

Luckily, becoming a master budgeter is easier today than it has ever been thanks to several budgeting apps that make the process simple and convenient.

When meeting with someone serious about their financial goals, the first recommendation is almost always a budget. — Ty Johnson, Financial Planner, Peak Financial Management

Align Budget with Personal Values

Review your budget so that it aligns with your values, not what society tells you to value. Many of us get trapped in consumerism and in looking the part. Society tells us that, in order to prove that you are wealthy, you must have an expensive car, home, and wardrobe.

What happens if you value none of those things? You spend more money than necessary, proving you have money. Look at your expenses. Do they truly align with what you care about? If they don’t, change it and be free. — Tremaine Wills, MBA, CFEI, Financial Planner | Investment Advisor, Mind Over Money

Plan Meals to Control Food Budget

Plan your meals for the week on the weekend before. Make your grocery list from your established menu. This habit keeps you from buying groceries you don’t need and helps avoid the late-afternoon query, “What should I make for dinner tonight?” that often ends up with something quick and less healthy, or convenient but more expensive.

Additionally, planning out your menu helps maintain variety. In our home, we have an outline we tend to follow: Sunday’s meal has pork; Monday tends to be a hearty soup or salad; Tuesday is “Breakfast for dinner” (egg bake, blueberry crepes, etc.); Wednesday is a chicken dish; Thursday’s dinner has fish or sausage as a base ingredient; Friday is Pizza night (make yourself or order out), and Saturday is a beef dish. — Keith Piscitello, Certified Financial Planner, S2 Wealth Planning

Distinguish between Needs and Wants

Frugality is about mindset and intentionality more than deprivation. One of the most impactful practices for me has been to shift my mindset around needs versus wants. It’s easy to fall into the trap of feeling like we “need” the latest technology, furniture, clothes, cars, etc. But most of these are simply wants. Focusing on true needs — food, shelter, basic clothing, transportation to work — frees up a lot of money.

I ask myself, “Do I really need this, or just want it? Will this purchase add value and enjoyment to my life, or am I buying it just to have it?” Distinguishing needs from wants has allowed me to dramatically cut discretionary spending. I buy very few material items now, and focus my time and money on experiences, relationships, and personal growth. — Brian Meiggs, Founder, My Millennial Guide

Prepare Lunch at Home for Savings

Wherever possible, prep your lunch at home if you’re eating at the office or somewhere other than your home. Over the course of a month, the savings really stack up! This could be as easy as batch-cooking at the weekends, ready for the week, or just making a homemade sandwich in the morning. — Jordan White, Financial Planner, A Money Thing Happened

Leverage “Stoozing” for Mortgage Savings

In financial strategies, one unique money-saving hack I’ve employed is using an offset mortgage combined with savings. This approach, popularly known in England as “Stoozing,” can significantly reduce monthly mortgage payments.

Stoozing involves utilizing the funds from 0%-interest credit-card offers. Instead of spending this money, one deposits it into a bank account linked to an offset mortgage. This approach effectively reduces the mortgage balance temporarily, leading to significant savings on mortgage interest.

As the 0% period on the credit card nears its end, the “stoozer” then pays off the credit card using the deposited funds, having benefited from reduced mortgage costs in the interim. At one point, I had over £100,000 on credit cards, but this was sitting in my bank account, significantly reducing the interest payments on my mortgage. It accelerated my financial independence by at least 10 years. — Shane McEvoy, MD, Flycast Media

Track Expenses for Financial Insight

As a wealth-management specialist, one frugal-living tip I recommend to new clients is to track and record all your expenses. While this may seem time-consuming, it’s a great way to gain insight into where you are spending your money and how much you’re actually saving each month.

Making sure you can see exactly where your money goes will help keep it in check and prevent impulse purchases that add up quickly. This is especially important when trying to reach financial independence because every dollar saved means more freedom for the future. — Adam Fayed, CEO, AdamFayed.com

Eliminate Unnecessary Subscriptions

Getting rid of subscriptions and simplifying my monthly budget has played a significant role in speeding up my journey towards financial independence.

Subscriptions might seem harmless, but the costs can really sneak up on you if you’re not careful. For years, I was paying over $100 a month for cable. I also was spending $50 on various streaming services, had an expensive gym membership, and would occasionally try services like meal delivery kits. And I hadn’t negotiated my Internet or phone bills in years.

One day, I realized I was spending well over $350 per month on these services, some of which I wasn’t using. I cut cable out completely, got a cheaper phone plan, and moved to a more affordable gym near me. I also scrapped the meal delivery kits and just cook myself now. This saves me $200+ a month easily, and it hasn’t impacted my quality of life.

I suggest other people take a look at their monthly spending to find sneaky recurring charges they can trim quickly. — Tom Blake, Founder, This Online WorldContinue Reading…